Interactive Brokers Review 2026: Pros & Cons

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Are you looking for a great broker? Look no further!

Interactive Brokers (IB) has all the features you need as a passive investor. Plus, their fees are almost unbeatable in the industry.

I have been using IB for several years and could not be more satisfied. They offer a wide range of products at excellent prices.

In this review, you will find all you need to know about Interactive Brokers, what you can do with IB, how much IB will cost you, and much more!

By the end of this review, you will know whether IB is a good broker for you!

| Custody Fees | 0% per year |

|---|---|

| Inactivity Fees | 0 CHF |

| Buy Swiss ETF | 5-15 CHF |

| Buy American Stock | 0.50 – 1 USD |

| Currency Exchange Fee | 2 USD |

| Languages | English, French, German, and Italian |

| Mobile Application | Yes |

| Web Application | Yes |

| Custodian Bank | 8 different US banks |

| Established | 1978 |

| Headquarters | United States |

What is Interactive Brokers?

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Interactive Brokers (IB) is a well-established brokerage firm (a broker) from the United States. IB was founded in 1978 already.

Today, Interactive Brokers is a huge brokerage company. They are the largest electronic brokerage firm in the United States. They are also leading the forex broker market. IB is also profitable, with over one billion US dollars in yearly revenue. IB employs more than 1500 employees worldwide.

IB offers access to stocks, bonds, options, futures, and other financial instruments on the leading stock exchange in the world. You will have access to all the investing instruments you will ever need. As of 2026, they offer access to more than 170 different markets in many countries.

If you are going to trade US bonds, it is worth mentioning that IB offers access to the US bond market 22 hours a day, 5 days a week. This makes it very available to buy US bonds during European hours.

So, here is precisely what IB offers as a broker.

Interactive Brokers Account Types

Interactive Brokers offers two types of accounts.

The default account type is the Cash account. With this account, you can only trade with the money you have in it. I am using this account type, which is good for most people.

The other account type is the Margin account. With this account, you can trade on margin, which means that you can buy stocks with money you do not have. So, IB will lend you money to trade on the stock market, and you will pay interest on the money loaned to you.

Generally, with margin accounts, you have a certain level of margin. For instance, if you have 10K cash and a 4:1 margin, you will have 40K available.

If you are interested in margin accounts, you should first read IB’s page on Margin accounts. You should also be careful about the risks of trading on margin.

For most people, a Cash account will be the best choice. If you do not know about margin accounts, do not consider getting a Margin account. You could lose a lot of money if you do not know what you are doing. On the other hand, if you know what you are doing and want to use leverage, you can choose a Margin account.

It is also worth noting that you can get a free trial. In this trial, you will get paper money. And you can simulate investments in the stock market with your paper money. This is a good way to start investing without putting any of your money. For many people, this is a good way to put them at ease with investments. Once they have mastered the account, they can seamlessly upgrade the free trial account to a live account and start trading for real.

Interactive Brokers Fees

In the long term, you need to reduce your fees. Investing fees are extremely important.

Interactive Brokers has two fee systems:

- Fixed Fee System

- Tiered Fee System

The fixed fee system is straightforward. You will pay a fixed fee for each exchange. For instance, you will pay 0.10% on transactions on the Swiss Stock Exchange (with a minimum of 10 CHF).

The tiered fee system is much more complicated. You pay individual fees, such as clearing fees, trade reporting fees, and transaction fees. The rules are different for each stock exchange.

The complexity of the tiered fee system turns many people away. However, for simple investors, the tiered system is often significantly cheaper. In most of my calculations, the tiered fee system was less expensive than the fixed system. So, if you want the lowest fees possible, you should generally opt for the tiered system.

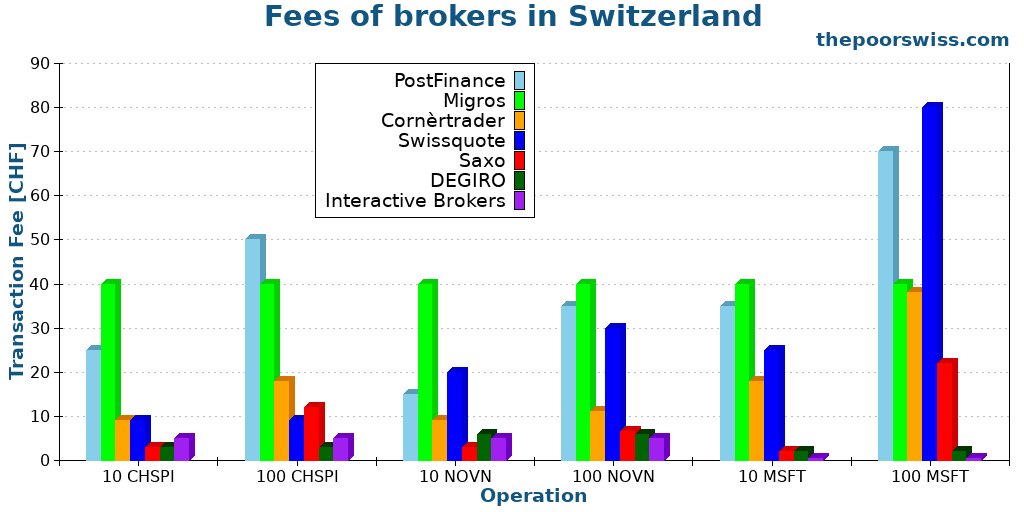

I will not go into details about all the fees of Interactive Brokers because they are complex. But overall, the fees of Interactive Brokers are really low. For instance, here is a comparison I did for the best brokers in Switzerland:

When you compare IB with other brokers available in Switzerland, we can see that the fees of Interactive Brokers are excellent. If you trade a few times per month, your costs will be really low!

We use Interactive Brokers as our primary broker because of its excellent fees and its wide access to ETFs.

Currency Conversion Fee

IB is doing currency conversion at the best rate available. However, conversions are not free.

If you are doing a manual conversion, you will pay 0.002% of the conversion, with a minimum of 2 USD. Unless you are doing massive conversions, you can assume you will pay 2 USD.

If you are letting IB do automated conversions (with a cash account only), you will pay 0.03% of the conversion size, without a minimum.

The automated system is cheaper for conversions below 6500 CHF, and manual conversions are cheaper after that.

Overall, these fees are incredibly cheap! This is among the best available fees for currency conversions. And this is orders of magnitude better than a Swiss broker.

However, it is worth mentioning that Interactive Brokers does not like accounts that are solely used for currency conversions, without investing. Some people had some features blocked on their accounts for doing that.

Custody and inactivity fees

Fortunately, there are no custody fees or inactivity fees at IB!

IB’s no custody fee advantage over most other brokers is fantastic! Not only do they have outstanding transaction fees, but having no custody fees is fantastic!

Cash Interest Rates

The interest rate on CHF cash was negative in the past. However, it has been growing steadily since 2023.

Currently, the interest rate on CHF balances is 0.0% (as of April 2025). And the interest rate on USD balances is 0.0% up to 10'000 USD and 4.080% above that (as of December 2024).

You can get the current interest rate on this page.

Other fees

One fee that is worth mentioning is the withdrawal fee. Indeed, you are only allowed one withdrawal per month. If you do more than one withdrawal in a month, you will pay for each one starting from the second one. Each paid withdrawal is 11 CHF for a CHF withdrawal, 8 EUR for an EUR withdrawal, and 10 USD for a USD withdrawal.

If you want to register your Swiss shares in the share register, you will have to pay 150 CHF. This is relatively expensive, even compared to Swiss brokers. However, this is something not everybody needs and is not necessary for each position. But if you are planning to register your shares, it is important to know this fee.

Opening an account with Interactive Brokers

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

Opening an account with Interactive Brokers is not complicated, but it will take some time. The procedure asks many questions and has many steps.

First, they will ask for general information about you (name, address, and such). You will also need to select the type of account you want. This choice is essential. This step is also where you will choose the base currency of your account.

The second step of the procedure is to provide financial information. IB will ask you how much money you have and how much experience you have with stocks. And you will have to choose which instruments you want to invest in. Do not worry too much since you can register for new investing instruments later.

The next step is about accepting the terms and conditions of Interactive Brokers. I would recommend at least skimming through them. After this, they will ask for proof of your identity and extra tax-related information.

Finally, you only need to fund your account for it to be complete. While this is not the most straightforward procedure, it is not too complicated.

If you want more information on the process, I have a guide on creating an Interactive Brokers account.

Subaccounts

It is worth mentioning that you can have subaccounts in your Interactive Brokers account. It means that you can manage several accounts in the same primary account.

The best usage of subaccounts is if you want to invest for your children and easily separate your stocks from theirs. Legally, the stocks are still yours since you cannot create accounts for minors. Nevertheless, it is good to see them separate. I have bought a share of VT every month for my son.

If you want further information, I have an article about investing in stocks for your children.

Using IB to trade

Interestingly, IB has many user interfaces:

- The standard web application

- The mobile application (IBKR Mobile)

- The WebTrader web interface

- The IBKR Desktop application, for Windows and Mac

- The Trading Workstation (TWS) desktop application

So, there should be an interface for everybody!

You can do most things from all interfaces. For instance, you can trade stocks from each of these interfaces. The problem with IB is that many people have been discussing the TWS interface. So, many beginners believe they should use it. However, the TWS interface is the most complicated of these interfaces by far.

I have never used the TWS application for trading. It is just too complicated for most investors. You only need the Account Management interface if you are a simple investor and invest in ETFs. If you prefer phones, you can also use the IBKR Mobile application to trade.

From account management, you can trade everything you want. And you can also transfer money to and from your account. All these operations are relatively simple.

You can fund your account for free with a bank transfer. First, you must declare your bank account in IB, and then you can make a deposit. Withdrawals work the same way. You can only send money to accounts in your name. I never had any issues with either deposits or withdrawals.

For currencies, you have multiple choices:

- You can do a forex trade directly. For instance, you could buy USD.CHF, which is buying USD with CHF.

- You can use the currency converter and let IB do the operation for you.

- Since April 2024, you can let IB do the currency conversion for you by buying shares in a currency you do not have. For instance, if you buy VT in USD and only have CHF, IB will do the conversion for you. This will only work on a cash account, since a margin account would go negative on the currency you do not have.

In any case, IB is outstanding at converting currencies. They use an excellent rate and have very low fees.

It is also worth noting that you can automate your investments with IB. You can set up standing orders starting weekly or monthly. If you use a recurring order for the transfer, you can entirely automate your investments. This feature is something some people are looking for.

If you want further instructions, I have a guide on how to fund your IB account and trade an ETF.

Other features

IBKR has some other interesting features.

I would like to mention the Stock Yield Enhancement Program. If you enable this option in the settings, IB can lend your shares to other investors. This system is called securities lending.

I like that IB shares 50% of the profit with you if you use that option. This sharing starkly contrasts with other brokers that would lend your shares to other people by default without giving you any profits.

I am not saying everybody should enable this option, but for me, this indicates that IB is a great broker.

Another interesting feature is that you can trade fractional shares. This feature allows you to buy fractions of shares. This feature is helpful if you want to buy some expensive shares or if you want to purchase many companies without having a large portfolio. You can read more about fractional trading at IB.

One thing that is missing from Interactive Brokers is the ability to register Swiss shares as a shareholder. Some people want to be registered so they can attend shareholder meetings and receive some gifts.

While IB itself does not provide e-tax statements, Datalevel AG, a Swiss company, is offering this service. With them, you can generate e-tax statements from your IB account.

Is IB safe?

If you invest significant money, you want your broker to be safe. So, we must look at the safety and security of IB.

Regulations

First, we can take a look at regulations.

Interactive Brokers has seven legal entities depending on the customers’ country. For instance, Interactive Brokers LLC works in the US, while Interactive Brokers (UK) Limited works for European clients.

Each of these entities is regulated. For instance, the US entity is regulated by the Securities and Exchange Commission (SEC), and the UK entity is regulated by the Financial Conduct Authority (FCA). So, overall, IB is extremely well-regulated.

Financial Strength

Currently, Interactive Brokers is considered very strong financially. They have a strong capital position and advanced risk controls.

The company manages over two million accounts and executes almost two million daily trades. These are substantial numbers showing that IB has many active users.

In April 2023, IB had over 7 billion USD above the regulatory capital they needed. The company invests mostly in the short term to ensure it has enough money to cover issues in the short term. So, IB’s money is not locked when it needs to be available.

Overall, Interactive Brokers’ financials are good. The company has not shown any signs of financial trouble.

Protections

Moreover, protection in case of bankruptcy is also critical. Even though IB is financially strong, we still want to know what would happen should it go bankrupt.

It is important to know that IB does not segregate each country. This means a Swiss investor using IB UK will use the same trading system as a US investor. This is great news for protection!

The SIPC will protect US investors. It protects your assets up to 500K USD, but it will only protect your cash up to 250K USD. And since Swiss investors are protected like US customers, we also get SIPC protection!

Now, there is an exception for some instruments. For instance, Contracts for Difference (CFDs) are prohibited in the United States. But they are offered to other investors. If you use them, the protection for your CFDs will fall to the FCA protection, up to 85K GBP.

Again, you have excellent protection against bankruptcy with Interactive Brokers. We have higher protection with IB than with a Swiss broker.

It is important to note that since Brexit, European investors have been using other entities of IB. In that case, the protection is worse since you will not get SIPC protection on stocks, only FCA. But Swiss investors still have SIPC protection. We should note that SIPC has a global limit of about 7.5 billion USD.

If you would like to learn more, I have an entire article about Interactive Brokers safety.

Technical security

Finally, technical security is also essential.

With Interactive Brokers, you will have strong technical security. All communications with the server are encrypted, but all honest brokers use encrypted traffic.

Most importantly, you can use Two-Factor Authentication for your account. You have two choices for that. First, you will be able to use the IBKR Mobile Application for that. Every time you log in from the web interface, you must confirm the login and enter one more code on your phone. But you can also use your standard TOTP application to generate a code. This second factor adds a great layer of security to your account.

So, Interactive Brokers has excellent security!

My Experience with IB

I started investing with Interactive Brokers when DEGIRO suddenly blocked access to US ETFs to Swiss Investors. Since then, I have been delighted with Interactive Brokers. I have been investing with IB for more than three years.

My entire stock portfolio is in my IB account. I buy new ETF shares every month from the default web interface, but I have also tried other interfaces. The IBKR Mobile application is very well done, but I generally prefer using my desktop computer rather than my phone.

I do everything from the Account Management interface, which suits all my needs. IB also fits my needs perfectly well. With time, I have learned to ignore most of the tool’s features. I only need a few features for my trading.

Since I sometimes get paid in USD, I can wire the money directly to my Interactive Brokers account. That way, I would not have to pay any currency exchange fees and could invest the money directly.

Overall, I am happy with my experience with IB. I never had an issue with the broker, and all my transfers reached IB very quickly. When I needed to withdraw money for the down payment on our house, I had no problems. All my trades have been flawlessly executed. The reporting on the web interface is also precisely what I need. I can only recommend IB!

IB Reputation

It is essential to look at a broker’s reputation before using it to invest in the stock market.

As a source of review, I always use TrustPilot. So, we look at the reviews of IB on TrustPilot. On average, users rate IB at 3.3 stars. Before looking at this, I was expecting a higher score.

First, we look at what people do not like about IB. We can categorize most of the negative reviews into two categories:

- Poor user interfaces. It takes a while to get used to the IB user interface. But after some time, it is straightforward to use.

- Poor customer service. It seems that many people have issues getting help from customer service. I cannot comment on that since I have never used their customer service. But I know people in Switzerland who did and have never had issues with them.

Overall, I am not too worried about these negative comments. A lot of them do not seem serious. And many commenters seem pissed off at making mistakes with the platform. But of course, it would be better if they are fewer negative reviews.

One good thing is that most reviews (39%) rate IB at five stars. So, we should also look at what positive reviews are saying:

- Excellent customer service. It is interesting to note that there are both negative and positive reviews of IB’s customer service.

- Excellent fee system

- Excellent order execution

- Good platforms

So, we can see that overall the reviews are mixed for IB. I think it comes from the fact that it takes a while to get used to it. Once you get used to it and focus only on the things you need, IB is quite simple to use.

Interactive Brokers Awards

One way to see how a broker is doing is to check out the awards they got from external sources. Over the years, Interactive Brokers has received many awards.

They received seven awards only in the year 2022:

- Best Online Brokers of 2022, by Barron’s

- Three awards from Investopedia, including best broker for international investing

- Several award titles from stockbrokers.com

- Several award titles from forexbrokers.com

- Several award titles from brokerchooser

While this is not the only thing that matters, awards are a good sign for Interactive Brokers.

Alternatives to Interactive Brokers

There are many alternatives out there.

The one that is the most interesting for a Swiss investor is DEGIRO. However, we should also compare IB with Swiss brokers.

Interactive Brokers vs Saxo

Start investing with a Swiss broker at incredible fees! Start trading with Saxo Bank and get 200 CHF in trading credits.

- Low currency conversion fee

- Swiss broker

Many Swiss investors prefer to use a Swiss broker. So, we should compare Interactive Brokers vs Saxo, my favorite online Swiss broker.

Both brokers have a ton of features, and simple investors will not miss a feature on either service. Both brokers offer access to US ETFs as well.

Saxo is the most affordable of the Swiss brokers. However, it will still be more expensive than IB. Neither of the two brokers has custody fees. The transaction fees are significantly higher at Saxo than at IB, especially on foreign stocks. Currency conversions are also cheaper at IB.

If you want to purely optimize your investing for fees, you should opt for Interactive Brokers. If you want to opt in for the cheapest Swiss broker and retain Swiss custody, you should opt for Saxo and accept higher fees.

Overall, both of these brokers are great and I am actually using both.

Interactive Brokers vs Swissquote

|

Best broker overall

|

Great Swiss Broker

|

|

Primary Rating:

5.0

|

Primary Rating:

4.5

|

|

Extremely cheap

|

Very affordable

|

|

Pros:

|

Pros:

|

|

Cons:

|

Cons:

|

- Outstanding prices

- Many investing instruments

- Excellent execution

- Access to US ETFs

- Good reputation

- A little intimidating at first

- Swiss broker

- Easy to use

- Many investing instruments

- Access to US ETFs

- Good reputation

- Expensive to trade US shares

- Expensive currency conversion

Another interesting Swiss broker is Swissquote, probably the most established Swiss broker. Both brokers offer access to US ETFs and have roughly the same features. If you are a simple passive investor like me, both brokers will have more than enough features for you.

You can trade with both brokers from your computer and your mobile phone or tablet. Swissquote is slightly easier to use than Interactive Brokers, but not by a long shot.

The main difference between these two brokers is price. If you use a stock exchange other than the Swiss Stock Exchange, IB is much cheaper than Swissquote. In some cases, IB can be 100 times cheaper than SQ. This difference can be very significant.

In addition, SQ has some custody fees, while IB has zero account management fees. So, if you are looking to optimize the price, IB is the clear winner.

For many investors, Swissquote will have the advantage of being in Switzerland. It may make it easier to deal with them if you have issues, while it could be complicated with IB. So, if you are looking for an affordable (not cheap) Swiss broker, Swissquote is an interesting alternative.

For more information, read my review of Swissquote or my comparison of Swissquote vs Interactive Brokers.

Interactive Brokers vs DEGIRO

|

My top pick

|

Good broker for Europe

|

|

5.0

|

4.0

|

|

No custody fees

|

Very affordable

|

|

|

|

|

- Great prices

- Many investing instruments

- Excellent execution

- Access to US ETFs

- A little intimidating at first

- Affordable

- Wide range of investing instruments

- Expensive currency conversions

- No access to US ETFs

- Lend your shares by default

For European investors, DEGIRO is another interesting alternative. So, it is interesting to compare these two brokers.

The first main difference between the two brokers is that only Interactive Brokers offers access to US ETFs to Swiss investors. This difference makes IB a much better choice than DEGIRO for Swiss investors. It will make a significant difference in the performance of your portfolio. If you invest with DEGIRO, you must invest in inferior European funds.

But we can also look at the fees of both brokers. There are a few differences between DEGIRO and IB:

- IB is much cheaper for the American Stock Market

- DEGIRO is very slightly cheaper for the European Stock Market

- IB is much cheaper for Foreign Exchange (FOREX)

There are a few differences in the features part as well. IB is also a FOREX broker, so you can hold many currencies in your account. And foreign currency exchanges are cheap. On the other hand, DEGIRO offers automatic currency exchanges when you buy and sell, but it is much more expensive than IB (unless you do small conversions).

You can also opt for manual currency conversions on DEGIRO, making currency conversions even more expensive. Overall, DEGIRO is not a great choice for trading currencies.

For the user interface, DEGIRO is slightly easier to use than IB. On the other hand, IB has many more features, but simple investors will likely not need many of these features.

Finally, IB was established in 1978, while DEGIRO only started offering brokerage accounts to retail investors in 2013. So, IB has more extensive experience.

So, overall, Interactive Brokers is a much better broker than DEGIRO. You will be able to access US ETF if you are Swiss. And you will be able to get excellent service at very low prices.

If you want more details, you can read my DEGIRO Review.

Interactive Brokers FAQ

What is the minimum deposit for Interactive Brokers?

There is no minimum deposit at Interactive Brokers. You can open an account without any money inside. Since there are no inactivity fees, this is perfectly fine for a small amount.

Is Interactive Brokers safe?

Yes. Interactive Brokers has been around for more than 40 years and has a great reputation. On top of that, it is well regulated in several different countries. Finally, your money is insured at Interactive Brokers for up to 500’000 USD, thanks to SIPC.

Is Interactive Brokers good for beginners?

Yes. While it is not the simplest broker out there, IB allows you to get started with little money and very low fees. The basic interface is simple enough to use and will allow you to do everything you need to start investing in the stock market.

What Interactive Brokers entity should I use?

As a Swiss investor, I recommend using the Interactive Brokers UK entity that offers the best regulations, protection, and features.

Who is Interactive Brokers good for?

Interactive Brokers is great for all investors that want to trade themselves and do not mind a foreign broker.

Who is Interactive Brokers not good for?

Interactive Brokers is not the best if you want to keep it very simple. If you are afraid of using a foreign, there are some Swiss alternatives, but at higher fees.

Can you use an IB account for currency conversions only?

No. IB may block your account if you use it only for currency conversions, without investing.

Can you register Swiss shares in your name with IB?

No, you cannot. Currently, it is not possible to register Swiss shares in your name as a shareholder with Interactive Brokers.

Interactive Brokers Summary

Interactive Brokers is an excellent broker with everything you need to buy stocks and ETFs, reliably and at extremely affordable prices. With IB, you can trade U.S. stocks for as little as 0.5 USD!

Product Brand: Interactive Brokers

5

Interactive Brokers Pros

Let's summarize the main advantages of Interactive Brokers:

- A vast range of investments

- Very low fees

- No custody or inactivity fees

- Very professional service

- Offers US ETFs to Swiss Investors

- Good overall reputation

- Long experience

- Excellent security

Interactive Brokers Cons

Let's summarize the main disadvantages of Interactive Brokers:

- It can be intimidating at first

- Too many user interfaces

- Cannot register Swiss shares as a shareholder

Conclusion

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Overall, Interactive Brokers is an excellent broker. Their fees are incredible, and their service is top-notch. Interactive Brokers should be your choice if you want a professional broker at a very fair price.

Since they are still offering US ETFs to Swiss investors (why US ETFs are the best), Interactive Brokers is currently the best broker for Swiss investors. No other broker even comes close if you want to optimize your portfolio.

I have been using Interactive Brokers for more than five years now. IB is the broker I am currently recommending to Swiss investors. It is also an excellent choice for European investors. I am pleased about IB and plan to continue using it for a long time.

Many people argue that we should not pay fees for brokers since there are free brokers. However, you have to be careful. There are many downsides to commission-free brokers. I much prefer paying very little for a great broker than not paying for a bad broker.

If you are interested in IB, I have a guide on opening an IB account.

What about you? What do you think of Interactive Brokers?

More reading

TradeDirect Review 2026 – Pros & Cons

BCV's broker. Read our 2026 review of TradeDirect. We check their trading fees and platform to see if they are a good alternative to Swissquote.

Guide to Interactive Brokers Multiple User Interfaces

Master IBKR. A guide to the different Interactive Brokers interfaces (Mobile, Web, TWS) and which one is best for Swiss DIY investors.

IBKR Desktop Review 2026

New trading platform. Read our review of the new IBKR Desktop application. Is it easier to use than TWS for buying stocks and ETFs?

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Poor Swiss,

I’ve read several of your posts regarding investing and interactive brokers. As an American what stocks, etfs, and mutual funds can I purchase on the Swiss exchange while residing in the U.S? What does the Swiss government expect in Taxes? My experience so far is etfs, mutual funds all not available for purchase though interactive brokers.

Thank you,

Poor American

Hi,

Normally, you should be able to access all stocks and ETFs from the Swiss Stock Exchange even as an American. As for mutual funds, I would not be surprised if they are indeed restricted.

As for taxes, I am no expert, but I would say that you would not have to pay taxes in Switzerland if you invest in Swiss shares from abroad. But if you want to be sure, you will need to consult a tax advisor or lawyer.

Dear all

I just opened an IB account and intend to buy a US ETF on a two monthly basis for 500 CHF.

Basis currency is CHF and of course then I need USD to buy the VTI.

Tiered pricing is then only 0.35 cents times 6 = USD 2.10 for the whole year.

HOWEVER, each time I need to exchange USD, I always heard that the exchange fee is super low at IB. In my case at the moment it will each time deduct me USD2 only for exchanging CHF500 into USD. Is that right? Do I do something wrong or how can I optimise that? Its good to have low 0.35 cents, however plus the 2 USD which then equals to 2.35 usd, cost is 0.47% otherwise would be 0.07% (only the 0.35).

Investing CHF500 is the max at the moment.

Hi Tom,

Even 0.40% is a great fee for Switzerland. The best broker in Switzerland has a 0.5% fee and the average is 1%.

But it’s true that a flat fee means that the lower amounts are more expensive. On the other hand, the fee is 0.2% only on 1000 CHF and 0.02% on 10K CHF, which is nothing.

If you want to save money, you will have to invest less often but I would not recommend it.

Thanks for this nice content, Mr. ThePoorSwiss

I have a question regarding the currency to buy a VWRL (Vanguar FTSE All-World):

My base currency on IB is CHF as I’m a swiss resident. I wouldn’t buy the VWRL in CHF because of the low trading volume. So the question is whether i should buy in EUR or USD.

I believe that it would make more sense to buy in USD as the companys in the ETF invests in USD and the divends are payed out in USD anyway. If I would buy in EUR there would be 2 currency conversions: CHF->EUR (made by myself) and EUR->USD (ETF) so I would have more currency risks because of the EUR conversion.

As I don’t know whether I will live in Switzerland or Germany in 5-10 years, it’s maybe better to buy the ETF in USD?

Thanks for your advice

Toni

Hi Toni,

Actually, if you are Swiss and using IB, you should try to buy VT rather than VWRL because it’s more tax-efficient.

In your case, I would buy in USD because it’s the fund currency. But it makes very little difference. I would not buy it in CHF.

You would be exposed to EUR if you buy it in EUR, so this is not useful if you are not intending to use the EUR.

Hi there, could you please give us an advise on how to buy each time the etfs, like vt at a low price? My problem is every time I see it gets down, I would like to buy, but, I have my chf and have to exchange currencies, so this 2 usd fee is killing me alive. How often do you buy and fund in ibk? have you develop an strategy to try to buy the ETFs when at lowest price without having to pay for many fees and without having to compromise your cash (hedge) quantity?

Also, is there a way to have your chf not in the form of stock, fluctuating with the currency exchange? I see my chf currencies are losing value every time the chf gets down against usd…

thanks

Hi Cris,

My strategy is extremely easy: I buy stocks the day after my salary when my transfer arrives from my salary to my broker. That’s it. There is no point trying to time the market if you have a long-term horizon.

I don’t understand your second question. Your CHF should not fluctuate with currency exchange if your base currency is CHF.

Dear Poor Swiss,

Thanks for your review on Interactive Brokers, I am about to open an account, main purpose is to buy ETFs from UK so that I pay less tax on annual dividends, only 15% vs 30% if buy ETFs from USA. Do you have such issues?

If I opened an account, say, in Singapore, can I buy/sell ETFs at any exchanges? Any limitations?

Thanks

David

Hi,

Are you in Switzerland? If that’s the case, U.S. ETFs are more tax-efficient than U.K. ETFs.

If you are in Singapore, I do not know which ETFs are the most efficient. But I would guess that yes you should be able to buy in any exchanges, as permitted by local law. With a IB UK account, I can invest in any exchange.

I have recently opened IB account and was informed that Swiss retail investors cannot trade US ETFs unless one is classified as a professional investor. However, I am reading that people are still trading US ETFs. I have actually opened IB account to be able to trade US ETFs. Any help?

Hi Kani,

That’s not correct, Swiss investors do not need to be professional investor at this time to trade U.S. ETFs. This may come in the future, but it’s not yet in action.

Do you have a IB UK account?

Yes. And this is what I received from IB customer service.

Account Settings > MiFID Client Category. >

To my further message that I am a Swiss resident, they replied

Yes, I recently opened it.

This is a part of the reply I got from IB customer service. They also provided the criteria to be classified as a professional investor.

Hi TPS!

Thank you for this great article, and your whole blog in general! I find it very informative and is always a stop when looking for information in CH.

I am an EU citizen living in CH (so my reference currency are more EUR and CHF) interested in investing in ETFs, mostly if not all American-originated ETFs (but with denominations also in EUR).

In your article it seems you refer to the US-based branch of IB. However, I have seen IB has branches in EU countries as well.

My question is: is there any reason to prefer the US-based branch versus any of the EU-based?

E.g. I have seen than in the US-based branch stocks, bonds, funds, and US options are protected by the SIPC up to 500K USDs. This would be a good reason to go for the US-based.

Are there other reasons in terms on fees, costs, etc. to choose one or another?

Do you know if the SIPC covers ETFs too? I guess so.

Kind regards

Hi Epoxy,

Thanks :)

I am actually referring to the UK version, not the U.S. version. You can’t open an account with the U.S. version if you are in Europe.

* The SIPC protection also applies to the U.K. version and they do cover ETFs

The U.K. version has two advantages over the other European versions: access to U.S. ETFs and better protection in case of bankruptcy.

Nice to see that they removed the monthly inactivity fees. It makes IBKR much easier to recommend to people that want to invest below 100k.

Yes, it makes it great to recommend to everybody now!

Dear Poor Swiss,

IKBR introduced a zero custody fee. That makes in my opinion the best broker. Thanks for the content and all the valuable info you provide here on the website!!!

Stay the course and invest :-)

All the best,

Szymon

I think they already were the best broker before, but they just got better :)

First time I am annoyed by your recommendation, poor Swiss.

Interactive Brokers turned out to be a nightmare for me.

Lessons learnt:

1) Don’t start with a Family (F) Account: You cannot even use their Client Portal and need to settle with the WebTrade platform – Java-based (outdated version) and slow.

2) Don’t fund your Family (F) Account: You cannot use that money for actual transfers.

3) Don’t rely on the support advice by the offshore Live Chat team: They had me convert in the wrong currency and I got interest charged for two months – in the F account!

4) You need to buy and sell FX manually – and not all currency pairs are available to you (like CHF.CAD for example). A huge waste of money to triangulate and then to learn that…

5) You can no longer (!) buy EFTs on NOAM stock exchanges as of this writing. So, they included in Swiss customers in MiFiD now.

Especially with the last drawback, IBKR is no longer worth the pain. It’s outdated, it’s shit – unless you like linking your portfolio to Seeking Alpha and pay another USD 15 there for the same Dividend King subscriptions day in day out.

Long story short: IBKR turned out to be a nightmare. Stick to Degiro. If you want to buy NOAM EFTs, buy the puts on the EFT and then cash in.

Did I mention that they charged me interest after instructing a transfer in the wrong currency?

Right, I did, well, IBKR is shit.

Hi Gene,

Sorry to hear about your experience.

1) 2) I never used family accounts, but it sounds really bad indeed. I will have to research that more.

4) While it is still manual, there is a feature to convert any currency directly without having to look for CHF.CAD directly. This is much simpler and works well.

5) What’s NOAM? North America? I bought some shares of VT today, so it’s definitely still possible to buy shares of U.S. ETFs.

I never had an issue with IB so far.

My two cents:

4.) That’s the only broker I know that offers manual FX conversion. All the others do it for you… for a 0.25%-1.00% fee. IB charges about $2.5 flat. I prefer the fees over minor convenience.

5.) Apart from “what’s NOAM?” I’d also ask “What are EFTs?”.

An F-account is not a family account, these are two distinct things.

The F-Account is an account you automatically have when opening an account at IBKR UK for trading metals and CFDs (see here: https://www.interactivebrokers.com/en/software/am/am/manageaccount/tradingukcfdsandmetals.htm ).

Family accounts work like having several individual accounts where one account is like the adminstrator and can trade, transfer funds etc. and the other(s) can only view their account. This is not an F-account but you should just have several regular account numbers, but I wouldn’t know for sure.

Currency transfer is manual but can be easily done in the web app or mobile app, the Java-tool is much more complicated and feels really outdated. All currencies are available, if you can’t find a pair you can invert it (so CHF.CAD instead of CAD.CHF sometimes the search only works one way) and instead of buying you would then sell the currency (or vice-versa). The flat 2$ fee is so much cheaper than any (hidden) fee anywhere else that it is worth the hassle and once done for the first time really easy to continue.

I can still buy VT and other US-stocks on a US exchange. Maybe they have changed this for new members only or maybe you are with IBKR Luxemburg instead of UK. You can check in your account summary (html or pdf). Or maybe only new customers are affected by this. There was – I believe it was the Mustachian forum – some rumors that by 2022/2023 IBKR UK must not allow Swiss residents to buy US-ETFs nevertheless but I am not sure if that is more than a rumor.