Investing Instruments: Cash, Bonds and Stocks

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Previously, we covered the basics of investing. You should know a few essential rules you should follow before you invest. However, we did not include details about how to invest in financial instruments.

This article covers the most important financial instruments you can use to invest: Cash, Bonds, and Stocks.

All these instruments are different. They are all important. If you are serious about investing, you should know about them. We will see the advantages and disadvantages of each of these instruments.

By the end of this article, you should better understand them.

Cash

Cash is the primary form of money. You need cash. I am not necessarily talking about hard cash in notes in your wallet. I am talking here about directly available money if you need it. It can be the cash in your purse, your checking account, or your savings account. We cover all these forms.

If you have no cash available, you cannot make any purchases. You will not be able to handle emergencies where you need significant cash. Therefore, if you do not have cash, you should start by accumulating a few months of expenses in cash. This money is called an emergency fund. I would always recommend having a good emergency before investing in other financial instruments.

I keep three months of monthly expenses in cash. It depends on many things. If your job is very stable, you probably will not need more than three months. But some people need or want more. You probably want to store more cash if you are close to retirement.

Save cash

You should not let it sit under your mattress. Most of your cash is probably in a checking or savings account. Savings accounts will generally give you more interest. But your money will be locked for some time. There is usually a limit to the number of withdrawals you can make from savings accounts. Be careful to keep some money in a checking account for monthly expenses.

In these accounts, your money is earning some interest. It means that each year, you will make some money. If you are in Switzerland, the interest rates are close to zero. In the U.S., you can easily find accounts with more than 1% interest. It is good, of course. Who does not want to get more money?

The main advantage of cash is that it is safe and very quickly accessible (liquid). This is important because you sometimes need this liquidity.

However, there is one big problem with cash: Inflation

Inflation

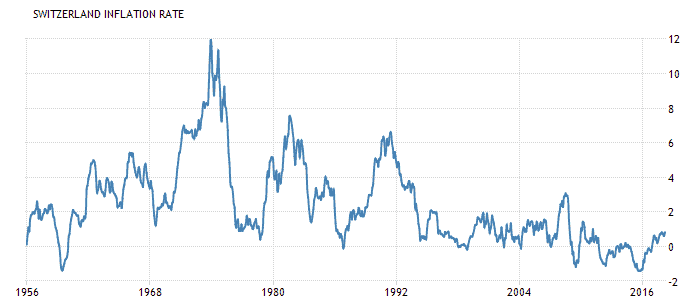

Inflation is the increase of prices in the economy for goods and services. Since the 1950s, Inflation has almost always been positive. So, each year, the average cost of goods and services increases. Of course, this highly depends on the country. For instance, here is the inflation rate in Switzerland since 1956:

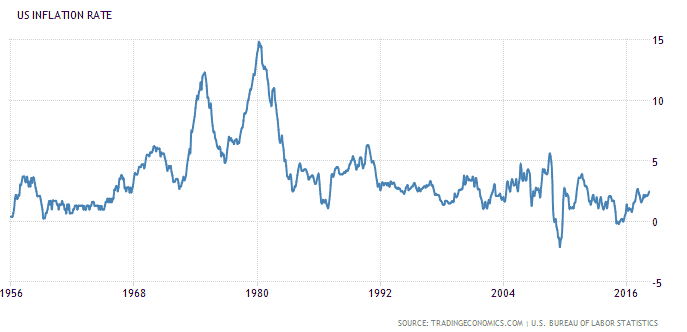

For instance, in Switzerland, inflation has been relatively low in the last 20 years. It only went once to more than 2 percent after the financial crisis of 2008. And we even had several years of negative inflation (deflation). In the United States, inflation has been much higher:

It has seen several years with more than 2-3 percent in the last 20 years.

We can see that in both cases, prices are going up. And this is the case for almost every developed country.

For more details and examples, read my guide on currency inflation and how to fight it.

Investing and inflation

What does inflation have to do with investing?

Inflation increases the prices of goods and services. So, each year of positive inflation, your money will get less than the previous year. That means that inflation is reducing the value of your money. Every year your money is worth less than it was the year before. Inflation is very important to know and understand. Many people do not realize this. It is eating into your purchasing power.

In most countries, interest rates are lower than inflation. We consider an average of 1% inflation. In Switzerland, interest rates are very low, around 0.1%. Each year, you lose 0.9% of your money. Your account will not reflect this loss, but your money will get you 0.9% less each year! Many people do not consider this since they do not see it.

Ideally, your salary would increase at the same pace as inflation. But for most people, this is not the case. In Switzerland, average salary increases are below inflation.

This concept is fundamental! If your interest rate exceeded inflation, you could still increase your buying power each year in a bank account. Around ten years ago, interest rates were higher than inflation. However, this is not possible anymore. It may come back. Unless you find a very high-interest-rate account (please tell me about it!), checking and savings accounts are not worth it anymore. You should still use it to store the cash you need. But you should invest the rest to fight inflation.

How to beat inflation?

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

How to find better returns than inflation?

Beating inflation is when investing starts to be a bit more complicated. But do not worry, it is not too difficult either! To fight inflation, you have to invest in bonds or stocks.

Bonds

The second financial instrument is to invest in bonds. While everybody has cash, not many people hold bonds.

A bond is a debt. In financial investing, you lend money to a government, a municipality, or a company. You are lending some amount of money to them. In return, you will receive some interest payments on your money. You may think it is the same as what your bank offers. But the bank offers a much lower interest rate than bonds. The reason is pretty simple. They are themselves using bonds as an investment. And they are getting most of the profit! What you want is to have a bond yourself and get the profit.

A bond works like this. You lend the issuer money for a certain amount of years. The bond issuer will then pay you some interest on the principal. The interests will be paid annually or semi-annually. The bond will mature at the end of the duration, and you will get your principal back. We will talk more in detail about bonds in another article. While they seem simple, they may not be as trivial as they seem.

Why not use bonds?

Why doesn’t everybody use bonds if it is better than a bank account?

For two reasons! First, for most people, bonds are not as convenient as bank accounts. You can get a bond directly from a company, municipality, or government. You can also get them from a broker or a bank. But you need to know what you are looking for. And secondly, there is some risk!

You will not get your principal back if the bond issuer goes bankrupt. Some issuers are very safe, such as treasury bonds from the U.S. government bond or the Swiss National Bank (SNB). However, their yield is not incredible. Generally, the lower the risk is, the lower the interest rate. You must take on some risks if you want a very high yield.

Historically, you could expect around a 2% interest rate on Swiss bonds. For many years, Swiss bonds have been negative, up to 2022. In 2022, with the return of inflation, interest rates have started to pick up. This makes Swiss bonds a better investment again.

You have another option to invest in companies. You can directly buy some stocks from them. By owning a company’s stocks (or shares), you own a part of it.

Stocks

A stock is a share of a company. It is a part of the company that you own. If you own some company shares, you own some part.

There are several advantages to stocks. First, if the company goes well, the stock price should go up. And as such, your investment should go up as well. Second, most companies pay dividends to their shareholders. You will receive, generally quarterly, some money for each share you own.

Finally, you own a part of a company. This has an actual value. If you like a company very much, it would be good to own part of it. And if you own enough company shares, you can be a part of the company’s decisions.

How good are stocks?

So, stocks are the best investment?

Stocks are a good investment but not a perfect one. Even though the stock price generally goes with the company’s financial health, it is also based on the market. The price is driven by demand and offer. If many people want to buy one specific stock, it will increase the price. There are some trends in stock investing. That means that the companies you are likely to be interested in will likely be overpriced. Moreover, sometimes even a very healthy company’s stock will fall.

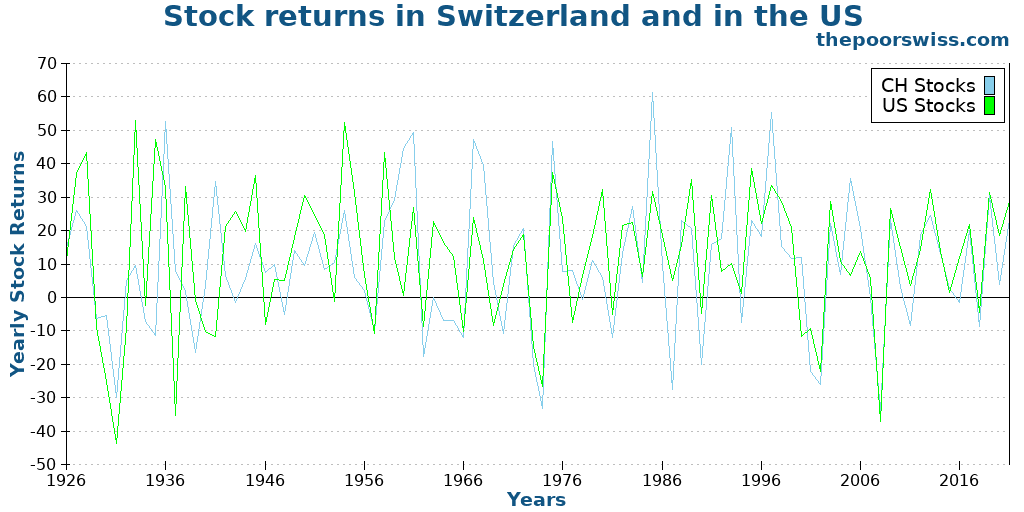

Historically, stocks have returned around 8% per year. Some years you can expect much more, and some years you can lose a large part of your investment. Stocks have more returns than bonds, but they are also more volatile. In the long run, stocks have historically been an excellent investment. But you need to be ready to take on some risks. Do not sell at the first time of loss!

As an example, here are the yearly stock returns of Swiss Stocks and United States stocks.

Given their volatility and high returns, stocks are the perfect instrument for long-term investing. But if you are investing for a shorter term, you will need to be careful.

How to choose stocks?

And owning stocks from a single company is a bad idea. If you only invest in one company and it goes bankrupt, you lose everything. And if the company you are investing in does not keep up with its competitors, you are missing a lot of growth. You should own stocks from many companies. Generally, experts recommend owning stocks from at least 20 companies. But this is only a rule of thumb.

But choosing the companies you want to own is a difficult choice. You need to look at a company’s financial characteristics to try to guess its future. How much debt does it have? How much potential for growth? What are the policies of the company? And so on. And answering these questions is not easy.

Even finding all the financial information about a company is not trivial. It is a job to find the best companies to invest in. Some people are very good at it, like Warren Buffett. Some people are terrible at it and lose a lot of money. Simply put, choosing a company to invest in is like gambling.

Choosing individual stocks is called stock picking. And it generally does not fare very well.

Diversification in the stock market

If you want to invest in the stock market, you must invest in many companies. You should probably invest in every possible company. The idea is to replicate the performance of the entire market. With this, your investment also goes up if the market goes up. Since nobody can consistently beat the market returns over a long period, you are better off with the market returns.

However, that is highly impractical. You surely do not have enough money to buy one share of every company in the stock market. If you do, you probably are not reading this blog. And even if you had enough money, it would be a lot of work. And a lot of trading fees.

However, there is a solution for you. Instead of buying all these shares, you can invest your money in a fund. A fund is a collection of stocks. You only purchase some shares of the fund itself. And via the fund, you own a part of all the companies’ shares inside the fund!

In the next installment of this investing guide, we cover funds in detail. Funds are what I am using to invest! This is what will work best for most investors.

Conclusion

Now, you should better understand the main financial instruments you can use to invest.

As we saw, cash only gets you so far. The returns are very low, and inflation is eating your small profits. You can use bonds to lend money to companies or governments. Bonds offer better investment returns, but you take more risks. And stocks allow you to own a part of a company. They will generally return more than bonds but expose you to more risks.

The biggest problem with bonds and stocks is how to pick them. How can you choose the best stocks in a portfolio? You need many of them to diversify. Fortunately, there is something called funds. There are bond funds and stock funds. Investing funds is the way I recommend investing.

To continue learning about investing, read my article about mutual funds and index investing.

Do you have any questions about these financial instruments? Did I miss something?

More reading

How to Choose a Stock Market Index for 2026

S&P 500 or MSCI World? Learn how to choose the best stock market index for your strategy and diversify your investments effectively.

The Three-Fund Portfolio Makes Investing Simple – 3 funds are enough

A Three-Fund Portfolio is a very simple, yet very efffective, way to invest. It is especially suited for beginners who do not know in what to invest.

How I Made $2’000’000 on the Stock Market – Book Review

Can you time the market? Read our review of "How I Made $2,000,000 in the Stock Market" and learn the lessons from this classic trading book.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

good morning dear,

I would like to ask you if you know whats the best way to avoid paying 35% dividends at the time of buying single stocks in Europe and or Switzerland. I actually hold just ETFs but would like to invest in some individual stocks, but from companies in Europe. I read your post on buying ETFs from Ireland. is it the same with single equities?

thanks a lot…

Hi Anto,

This is withheld, it then counts as taxes already paid, it’s not a huge deal if you can get it back.

But the 35% is indeed only on Swiss actions. If you buy Microsoft for instance, you will pay 15% (as a Swiss resident) withholding only.

I get it, thank you. What about stocks from companies in europe?, it doesn’t matter where you buy it (swiss stock market, NYSE or XETRA for instance, right?). Does the 15% withheld is fix in both EU and Switzerland then?

thank you so much.

Hi Antonio

Generally, Ireland is the preferred place for Europe. But I do not believe it makes a significant difference for European stocks.

I would personally buy European stocks on the European stock exchange and Swiss stocks on the Swiss stock exchanges.

Hey,

Just finished catching up with the entire blog, read all the posts. Great work! Thanks, much valuable information found, especially regarding the swiss perspective. Please keep doing!

I’ve just opened my DeGiro account, am on my way to selecting the ETFs and start investing, but taking time to get sufficiently informed.

On a side-note, I think you shouldn’t worry too much about the audience growth, as long a you produce quality content (which you do) it will eventually grow, just like a well balanced portfolio ;-) . Important thing is you bring value to people, quality over quantity… Word of mouth will do the rest. I’ve started to spread the word among my office colleagues ;-)

Cheers,

Jerome

Wow, thanks a lot Jérôme :)

Very good idea to take time before you do your choice. I did mine too fast and ended up having to review my portfolio entirely.

You are probably right about my audience ;) Nice analogy to a portfolio!

I’m probably biased too much after reading some many people having 1000 daily visits after 2 months :P

Thanks for spreading the word!

Cheers