What is Currency Inflation? How to Fight it?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

You have probably heard about inflation on this blog or another. But do you know what currency inflation exactly is? And especially, do you know what causes inflation and what it does to your personal finance?

Inflation can come from the economy, from the government, or from demand and supply effects. It can even be negative, something that is called deflation. And it has several consequences, the biggest of which is to make you lose purchasing power over time. So you need to protect yourself against inflation.

In this article, we look in detail at all these causes and effects of inflation. And we also look at some examples of inflation in the past.

Currency inflation

First, inflation is different for each currency. Generally speaking, this can be generalized as inflation for each country. But for countries that share the same currency, such as countries from the European Union, this is a bit more complicated.

In general, inflation is related to a country and its currency. For instance, inflation is different in Switzerland or the United States. Historically, it has been higher in the United States than in Switzerland.

More specifically, inflation is the rate at which the price of things evolves. If the price of items increases, there is inflation. Inflation is directly related to your purchasing power. If there is inflation, your purchasing power will decrease. If today, 100 dollars buy you 100 eggs, tomorrow, it may only buy you 99 eggs. This is because there has been inflation in the price of eggs. That means the same 100 dollars are not worth as much as before.

Compute inflation

There are a few specificities as to how to compute the inflation rate. First, you can calculate the inflation for each product independently: the inflation rate of butter or oil, for instance. It is relatively easy to compute this value. But generally, you are interested in the average inflation for many products. Therefore, we typically use a weighted average of different products. This composition of products is called a basket.

And unfortunately, there are many different ways to compute this average inflation. Most countries have an official metric for inflation. For instance, the most used index in the United States is the Consumer Price Index for all Urban Consumers (CPI-U).

To compute this index, they survey many people and calculate the rate based on their consumption. For instance, if people use one percent of their money on rice, rice inflation will make up one percent of the index.

In Switzerland, it is computed similarly and called the Consumer Price Index (CPI).

Inflation Numbers

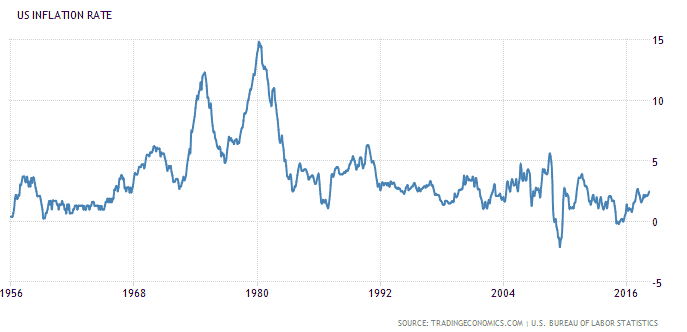

For instance, here is the inflation in the United States in the last 50 years or so:

In the 1980s, inflation was high. For several years, it was at more than 10%. 10% is a very high rate. Since 1992, inflation has been oscillating between two percent and five percent. It has only been negative for a few years.

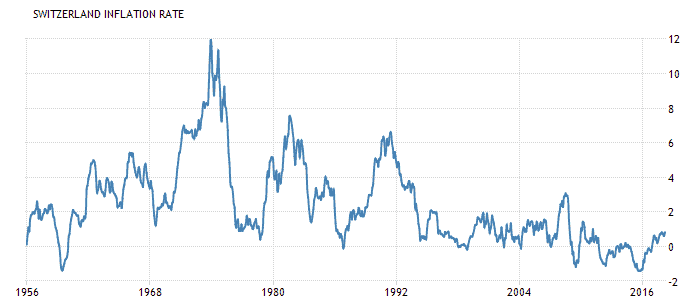

For comparison, here is the inflation in Switzerland for the same period:

As you can see, Switzerland’s inflation rate has historically been significantly lower than in the United States. Since 1992, it always stayed between two percent and minus two percent. It has been negative for several years in the last ten years. These last few years, it has always been very low.

It is important to know that in Switzerland, some things, such as health insurance, are not included in the inflation numbers. If you want to know, I will talk about whether inflation in Switzerland is really that low.

Deflation

Contrary to what a lot of people think, inflation can be negative. In that case, the price of things in the country is decreasing. Negative inflation is also called deflation. You may think that deflation can be good for people living in the country. But it may not be a great thing for businesses in the country. In Switzerland, we had several years where inflation was negative in the last decade.

Sustained and high deflation is generally a bad thing central banks try to fight.

It is pretty rare to have deflation in the entire country. However, it is pretty common for one product to decrease in price. For instance, things like wheat or milk have often decreased in price.

We will see later that while this seems an excellent thing, it may not be the case for everybody. Moreover, it can cause the bank yields to go down and can have adverse effects on the economy.

Personal Inflation

The official inflation is computed at the scale of an entire country.

In most cases, everybody will feel the impact of inflation differently on their budget. Indeed, everybody is buying different things. For example, if there is very strong inflation for gas and you ride your bicycle to work, you are less likely to feel this inflation.

Therefore, it is often more interesting to track your personal inflation. That is the rate at which your expenses are going up. However, you need to be careful with that since this will reflect price changes and changes in your lifestyle. And significant events such as weddings can make a huge difference in inflation.

Knowing your personal inflation rate can be beneficial to see where your expenses are going. If you have been tracking your expenses for a long time, you will have a lot of data to process!

If you like this metric, I have a list of 11 different financial metrics you could start tracking.

Causes of inflation

You may wonder why there is inflation.

Inflation does not happen without reason. There are many causes for inflation, to occur. Some of these reasons only apply to a few products. And some others apply to the entire purchasing power.

One thing that can drive the price up is the increase in demand. For most items, the demand increase as the number of people increases. There is a finite resource of most things on earth, yet there are more and more people. An increase in demand causes an increase in prices for some goods. For many possible reasons, some goods also become suddenly more demanded. And, of course, this can also go the other way. If the demand for one good goes down, its price will likely go down as well.

Not only can demand affect the price, but supply can also affect it. Too much supply may drive the price down. On the other hand, limited supply can drive the price up. And sometimes, supply becomes more difficult, pushing the price up. As said before, many things exist in a finite supply. And it can become more and more difficult to gather more of them.

One other possible reason is also that the government is printing too much money. If there is much more money, the value of the money decreases, and the prices increase. Such cases are rare and extreme because the government tends to avoid this situation.

There have been some extreme examples in the past. For instance, the currency in Germany after the First World War was almost not worth anything more. And recently, there has been some very high inflation in Venezuela. These extreme cases are sometimes called hyperinflation. Hyperinflation is never good!

Such a situation can only happen when no physical assets back the currency. These currencies are called fiat currencies, and they are the most common today. In the past, most currencies were backed by gold. For instance, the dollar was backed by gold until Richard Nixon changed this policy in 1973. Currently, there are still a few small currencies backed by oil. In that case, there is another factor that can make the currency lose value or gain value. If the physical asset price varies, so does the currency’s price. And so do the costs of the goods purchased with this currency. But these situations are more historical since you are probably unconcerned with this fact.

When there is inflation, there is also some pressure from employees to get raises in salary. That way, they can continue having the same purchasing power. Most companies will give a salary raise if inflation is going up. But the increase will most likely be below the real rate. But it can still be a significant raise. However, now companies have to pay more. And often, to continue having a good margin, they increase their prices. And this will drive inflation up once again. Inflation is a bit of a vicious cycle. If there were no inflation and no raise, nothing would change. But this is not the only reason, as we saw before.

Consequences of inflation

The main consequence of inflation is that you are losing purchasing power over time. If you think you need to save one million now to retire in 20 years, your one million may not be enough once the 20 years have passed. It could be only 80% of the target, for instance.

Some people think that inflation is making them lose money. This point of view is not accurate. Your money does not change. You can just do less with the money as inflation plays its role. So, you need more money in the future to offset inflation.

Also, some people believe that only money in the bank is subject to inflation. But this is entirely false. Cash under your pillow is equally subject to inflation as the money in your bank account. It is even worse for the money under your pillow since your bank may give you some interest while your pillow will not!

So the main consequence is that your hard-earned money is allowing you to purchase less and less. You are losing purchasing power. Losing purchasing power is quite sad. You probably worked very hard for that money!

Positive effects

Inflation can also have some positive effects. We do not talk much about them since most people focus on the negative side, but the positive effects exist.

The first positive effect is for people holding assets subject to inflation. The best example is a house. If there is a good inflation rate in the real estate market, the value of your house will appreciate. If you sell it ten years later, you may have made a nice profit. But do not forget that if you need to buy a new one after you sold the first one, you may also need to buy it at a higher price.

The second positive effect is for the economy. If the inflation rate is very low or negative, there is no difference between spending and saving. However, if there is higher inflation, people can see spending as more efficient than saving since you bought something at a smaller price than you would have if you waited longer. Inflation promotes spending in the entire country and thus helps the economy. It is why inflation is not always a bad thing. However, too much inflation is not a good thing. Indeed, when prices are growing quickly, people are growing afraid. In that case, people will start to stop spending, the economy will worsen, and the price may increase even more.

Relation to yield

Generally, you hear talking about inflation and bank yield together.

The reason is, in fact, quite simple. Bank yields and inflation are often following the same paths. That is not to say that yields are the same as inflation, not at all. But when inflation is high, the bank yields are generally high. And when it is low, so are yields. For instance, in Switzerland, it has been quite low in the last few years. Indeed, we have seen very low inflation as well. And now, as a result, the yields are extremely low, often zero for most banks.

It is because federal banks manage the treasury yield. For instance, in the United States, this is decided by the Federal Reserve. In Switzerland, the Swiss National Bank (SNB) is responsible for these yields. They may increase or decrease the yields based on the current economy.

We saw before that inflation has several effects, some positive and some negative. Central banks want to keep their rate in check and keep the economy running as well as possible. Sometimes, this means they have to lower the yields or increase them. Most of the time, they want to make people spend more. Because this is good for the economy, and a good economy is good for the people. But, of course, many other factors can make them change the yields, not only inflation. And increasing or lowering the yields can have significant effects on the economy as a whole.

What to do about it?

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

Now that we have seen many things about inflation, it is time to know what you can do about it. And in fact, this will be much easier.

The principal problem for simple investors is that your money is losing value for as long as sitting in a bank account. If today this money buys you a ton of sugar, it may only buy you half a ton in 20 years. So how do you buy a ton of sugar in 20 years with the same amount of money? The answer is pretty simple: you invest!

You must invest your money in a financial instrument yielding more than inflation. As long as your assets generate more returns than the inflation rate, you will be safe, and you will be able to buy a ton of sugar in 20 years. And if you are lucky with your investments and they yield significantly more than inflation, you may even e able to buy several tons of sugar. And probably pay large dentist bills if you eat all that sugar. But that is another story!

Several financial instruments will yield more than inflation in the long term. The first obvious instrument is stocks. If you invest in stocks, ideally with passive investing in a broad stock market index, you can expect a yield higher than inflation. Of course, this is only historical. We are just expecting it to be the same again in the future and hoping it to last.

You can also invest in bonds. While they generally yield less than stocks, they can still yield more than inflation, and they are less volatile than stocks. Once again, it is better and simpler to invest in a broad index of bonds.

There is a special treasury bond called Treasury Inflation-Protected Securities (TIPS). These bonds pay a fixed interest rate on the principal twice a year. But the principal goes up or down with inflation. That means you are protected from the effect of inflation. But, on the other hand, you are losing money if there is deflation.

And another way to fight inflation is to invest in assets whose prices will also inflate. For instance, you could invest in real estate. Generally, the cost of real estate assets increases over time. It is not guaranteed, and it may decrease depending on the situation of the real estate. For instance, the price of many houses went down after the financial crisis of 2008-2009. Nevertheless, owning some real estate assets and renting them could yield more than inflation, and you could be able to sell them for more than you bought them for.

FAQ

What is currency inflation?

Inflation is the rate at which the price of things evolves.

Can inflation be negative?

Yes. If inflation is negative, it means that the price of something is going down. Negative inflation is sometimes called deflation when it is sustained for a period.

How to fight inflation?

You can fight the effects of inflation by investing your money in assets that yield a return higher than inflation. For instance, you can invest in stocks, bonds, real estate, or precious metals.

Conclusion

As you can see by now, inflation is not a very simple subject. However, the defense against inflation is fairly straightforward: invest your money. You should not let your money lose value in a bank account. You should invest your money in the stock market.

Although you may think that inflation is evil, it is generally a necessary evil. It helps the economy run. And without the economy, there are no jobs, opportunities, or money. So a healthy inflation rate is necessary for the economy. On the other hand, a large one, be it negative or positive, is never good.

There is another essential inflation subject: lifestyle inflation. This other form of inflation is when people save less money even though they earn more income.

What do you think about inflation? How do you protect yourself against it?

More reading

Just Keep Buying – Book Review

My honest review about Just Keep Buying, by Nick Maggiuli: An excellent book about personal finance and investing.

Dollar Cost Averaging is more risky than you think

Lump Sum or DCA? We analyze whether you should invest all at once or spread it out over time (Dollar Cost Averaging) to maximize returns.

What is the Russell 3000 Index?

What is the Russell 3000? Discover this broad US market index, how it tracks the top 3000 companies, and how it differs from the S&P 500.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Could you also say that in this global economy, inflation is not just confined to where you are. As soon as you buy an avocado or an iphone in Switzerland, our inflation rates are influenced by the inflationary pressures of the regions where those items came from?

Hi Lisa,

Inflation in indeed not confined where you are. It’s true that the local inflation has a more direct (and often more significant) effect on you. But inflation in other countries will also impact companies in your local economy, could impact jobs and will in turn likely impact local inflation. With a global economy, inflation in a country like the united states can have a large global effect and cause global inflation to rise.

Great article again and agree with most of it. It would be interesting to round it off by the current discussion of ‘real inflation’ versus ‘official inflation’ rates. Many official inflation figures are underestimated as they choose a changing and limited basket of ‘typical’ items, including some and excluding others. Manipulation of the figures is not unheard off and in regards to retirement planning it is particularly important because we all know what 0.1% difference compounded over 50 years makes to our portfolio. The same 0.1% can greatly reduce our spending power in retirement.

To come back to your question on how to protect. I invest in real estate and plan to continue to do so. I do it in Emerging markets as inflation tends to be higher there. In comparison to where I want to retire this can make a big difference as emerging markets outperform developed countries. For example Poland (where I started investing) is the fastest EU country when it comes to growth and has further potential to grow.

Hi Financial Gladiator,

That’s a good point! Inflation is different for each product. And that means it’s also different for each household since nobody buys exactly the same things.

I will try to add more details as to how this is calculated in the future! Thanks for the suggestion.

It seems very sensible to invest in real estate based on which country has the most inflation. However, don’t forget to be careful about bubbles causing super-inflation. This may end up badly!

I am not a huge fan of real estate, but it is true that its returns are really nice!

Thanks a lot for commenting :)

Hello, Mr Poor Swiss

Here’s the message I have when I open one of your blog posts in my rss reader:

Warning: Illegal string offset ‘feed’ in /home/thepoors/public_html/wp-content/plugins/contextual-related-posts/includes/content.php on line 179

I don’t see any issues when I go directly to your website

Hi Thierry D and The Poor Swiss.

Just to say the rss feed works perfectly from feedly.

Cheers.

Hi Thierry,

Thanks a lot for letting me know! I have fixed the issue in the plugin that was causing this warning. It seems fine now :)

Thanks Cashfl0w for testing too!