US ETFs are the best ETFs for Swiss investors

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

I mostly invest in US ETFs, and I have recommended these ETFs many times on this blog. I consider US ETFs to be the best available ETFs. I have talked several times about what makes them great in various articles. But since I still get many questions, I will go into all the details of these US ETFs.

I am talking about Exchanged Traded Funds (ETFs) that invest in the United States. I talk specifically about ETFs from the United States. What matters here is the domicile of the ETF. This is more important than many people realize.

So, here is what makes these US ETFs great.

Availability of US ETFs

First, we need to address the issue of the availability of US ETFs, or lack thereof.

If you are in the United States, you will not have any issues. However, if you are in Europe, this is another story. Indeed, due to European regulations, many countries lost access to US ETFs.

In fact, in 2018, all the countries part of the European Union lost access to US ETFs. This is due to the PRIIPS regulations. These regulations are part of a bigger package known as MiFID II. These laws force the fund providers to provide a Key Investor Document (KID) in the investor’s language. And so far, US fund providers have not provided them, and they are unlikely to do it. So, for now, European investors cannot invest in US ETFs.

In theory, these laws protect investors by providing them more information on the instruments they are using. However, in practice, they are only here to force people to invest in European funds.

However, Switzerland is not part of the European Union. Therefore, Swiss investors still have access to US ETFs. However, this may change when the Swiss equivalent of the European laws enters into effect. Now, it is not entirely clear if this will apply to foreign brokers (like Interactive Brokers) or not. But for now, we are free to use these ETFs.

I believe these restrictions will not apply to execution-only brokers like Interactive Brokers. So, they should still be available in the future.

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Furthermore, not every broker provides us with access to these ETFs, even though they could do it by law. For now, only foreign brokers, like Interactive Brokers, give access to these ETFs. This is good since Interactive Brokers is the best broker for Swiss investors.

If you want more information on these regulations, you can read my article on the availability of US ETFs.

US ETFs have lower fees

The first advantage of US ETFs is that they have lower fees than their European alternatives.

What matters to us is the Total Expense Ratio (TER) of the ETFs. The TER is the total fee you pay for holding the money. This fee is expressed in percentage and is removed from your money over the year. So, if you have a TER of 0.1% and 100,000 CHF in the fund, you will lose 100 CHF each year to fees.

Since you will pay the fees each year, it is important to optimize them. If you are a passive investor, ongoing fees are the most important cost you can optimize. So, it is important to do it well. And the more money you have in the funds, the more fees you will pay.

We can compare a few ETFs to see the difference in fees:

- Vanguard S&P 500: The US ETF (VOO) has a TER of 0.03%, while the European ETF (VUSA) has a TER of 0.07%, twice as expensive

- Vanguard World: The US ETF (VT) has a TER of 0.06%, while the European ETF (VWRL) has a TER of 0.14%, more than two times more expensive

- iShares S&P 500: The US ETF (IVV) has a TER of 0.03%, while the European ETF (IUSA) has a TER of 0.07%, twice as expensive

- iShares World: The US ETF (URTH) has a TER of 0.24%, while the European ETF (IWRD) has a TER of 0.50%, twice as expensive

As you can see, the TER of European funds is significantly higher than US ETFs. Over the long term, this will make a significant difference in your returns.

When you are investing in ETFs, investing fees are not to be ignored. And this is especially true if you want to retire early based on your portfolio.

US ETFs are more tax-efficient

The second advantage is even more significant, but it is also a bit more complicated and is only for Swiss investors. Indeed, US ETFs are more tax-efficient for Swiss investors.

This tax efficiency is based on the way dividends are taxed. Especially how the US taxes dividends of US companies.

By default, the US government will tax 30% of the dividends emitted by US companies to foreign investors. Now, Switzerland has a tax treaty that reduces this withholding to 15% for Swiss investors, the same amount withheld for US investors. And moreover, we can reclaim the 15% left on our tax declaration.

But when we use an ETF in Europe, the dividends will be withheld before reaching the fund. For instance, if you invest in an ETF from Ireland with Coca-Cola shares, you will lose 15% of these dividends directly. But if these dividends are paid to a US fund, there is no loss!

This advantage is essential since US stocks make up 50% of the entire world stock market. Saving on the dividends of these stocks is very important.

The second-best domicile for ETFs after the US is Ireland. So, if you do not have access to US ETFs, Ireland (IE) ETFs are the next best thing.

Overall, how much you save will depend on the yield of the ETFs you are using. For a 2% yield, you will save 15% of 2%, which is 0.3%. So, by using US ETFs, you can save up to 0.3% in fees every year! On a 100’000 CHF portfolio, you can save 300 CHF per year!

However, it is critical to know that this deduction can only be claimed when it reaches 100 CHF. Below 100 CHF, taxes will reject this deduction. So you will need about 33’000 CHF in US ETFs before you can claim it.

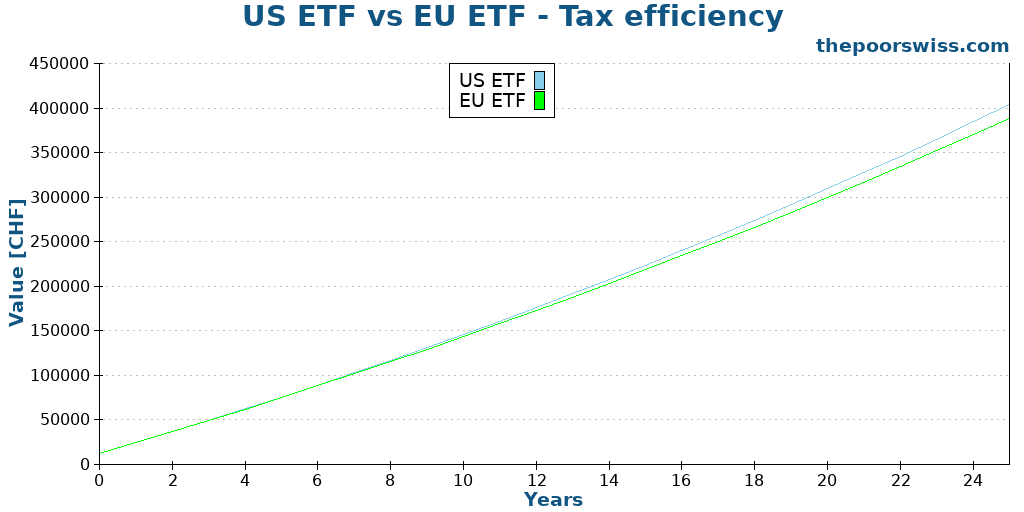

If you are wondering whether this is significant, you can take a look at the following graph. In this example, we are investing 1000 CHF per month over 25 years and the only difference is that we lose 15% of the dividends with

US ETFs are larger

A small advantage is that US ETFs are larger and more liquid. By large, I mean that they are managing more money. Generally, this is exposed as the Assets Under Management (AUM) metric.

A larger ETF has a few advantages over a smaller one:

- It shows more popularity. Larger funds are generally large because they are very popular (people put their money in them).

- It has a lower chance of being closed.

- A larger ETF has a higher trading volume. This has the advantage of the ETF being easier to sell. Generally, they also have a lower spread, which gives you better buying and selling prices.

- A larger ETF can better replicate the index since it will include more small companies than a smaller ETF.

For these reasons, large ETFs are generally better than small ETFs. But this should not be the primary argument in choosing an ETF.

US ETFs are cheaper to trade

The last advantage is that US ETFs are cheaper to trade (with a good broker) than European ETFs.

This is not directly due to the fund itself, but rather to the stock exchange they use.

For instance, my primary ETF, Vanguard Total World (VT), is traded on the New York Stock Exchange (NYSE). To buy or sell shares with Interactive Brokers costs me about 0.35 USD. I can buy many shares and still pay less than a dollar for the transaction.

On the other hand, buying 10’000 CHF of my Swiss ETF, iShares Core SPI ETF (CHSPI) on the Swiss Stock Exchange (SWX), cost me 10 CHF! That is about 30 times more expensive than my US ETFs.

And European ETFs are about in the middle of Swiss ETFs and US ETFs. To my knowledge, US ETFs are the cheapest to trade. Now, this may change if you use a service with free transactions. But there are very few good services like this available in Switzerland yet.

Risks: What about the US Estate Tax?

Many believe we should not invest in US ETFs because of the US Estate Tax. And in some cases, this is true. But in practice, for Swiss investors, there is almost no extra risk in investing in US ETFs.

The US estate tax law states that the inheritance of US ETFs is subject to a 40% inheritance tax. Nonresident aliens (basically, foreigners outside the United States) are exempted from this tax for assets up to 60,000 USD. After this, foreigners will have to pay a 40% tax.

This means that if you have many US assets, they could lose much value when you pass away, and your assets go through inheritance. You do not want this to happen to your estate.

However, many people miss that Switzerland has an estate tax treaty with the United States. And this treaty greatly increases the part exempted from this estate tax!

With this estate tax treaty, Swiss investors are exempted from the US estate tax for up to 11.18 million dollars, prorated to the proportion of US assets in your net worth. For instance, if US ETFs represent 10% of your estate, 1.118 million dollars (10% * 11.18 million) will be exempted from US Estate Tax!

So, in most cases, Swiss investors do not have to worry about the US estate tax! However, it is true that it may complicate your estate. If you have US ETFs, you will need to deal with the IRS.

If you want all the details and many more examples, you can read my in-depth article about the US Estate Tax law. This article also explains how to deal with US estate tax, in the specific case of Interactive Brokers.

What if you cannot use US ETFs?

Unfortunately, many people do not have access to these great US ETFs.

For these people, investing in European ETFs is still an excellent option. Using US ETFs is the best way to invest. However, it is an optimization over European ETFs. There is nothing wrong with investing in European ETFs!

If you want to be optimal, you must go with US ETFs. Now, it could be difficult (or even impossible) to use these ETFs. Even for Swiss investors, few brokers let us access them. If you do not want to go the extra mile and want to invest in good ETFs with lower effort, European ETFs are great!

What matters most is investing, not investing optimally!

What about mutual funds?

In this article, I have talked very specifically about US ETFs, but what about funds?

US mutual funds are also great. But it is interesting to know that Swiss mutual funds can also save you dividends. Indeed, funds are very different from ETFs in how they are held.

With a fund, each investor goes indirectly. With an ETF, you go through a broker who holds the shares in your name.

This allows the fund to be more efficient, directly depending on the treaty. So, a Swiss-domiciled mutual fund is as tax-efficient as a US-domiciled ETF. Of course, the Swiss mutual funds will likely have some other disadvantages (smaller and more expensive, mostly), but it is good to know that the main tax disadvantage of European ETFs is not present in Swiss mutual funds.

Conclusion

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

As you can see, there are many strong reasons to invest in US ETFs instead of European ETFs! These ETFs will let you save a significant amount of money in fees and taxes.

80% of my portfolio is invested in Vanguard Total World (VT), a US ETF. The rest is invested in a Swiss ETF for my home bias portion. So, I invest a considerable portion of my money into US ETFs. This is because I consider these ETFs to be the best available for Swiss investors.

However, these ETFs are more difficult to use. Investors from the European Union cannot invest in them anymore, and in Switzerland, only a few brokers let you use them.

As I mentioned, US ETFs are an optimization over European ETFs, but they are not a revolution. If you cannot (or do not want to) invest in US ETFs, investing in European ETFs will be a great way to invest!

If you want to start trading US ETFs, I recommend using Interactive Brokers. It is an excellent broker that lets you trade US ETFs with very low transaction fees. I have a guide on investing with Interactive Brokers.

Are you investing in US ETFs?

More reading

How I Made $2’000’000 on the Stock Market – Book Review

Can you time the market? Read our review of "How I Made $2,000,000 in the Stock Market" and learn the lessons from this classic trading book.

Swiss Investors almost lost Access to US-Domiciled ETFs

Starting in 2022, U.S. domiciled funds will not be available to Swiss investors. DEGIRO decided to enforce this early, in 2019. What can we do?

Distributing Funds vs Accumulating Funds: Which is better?

Dividends or Growth? Learn the difference between Distributing and Accumulating ETFs and which one is better for Swiss taxes and compound interest.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste,

First of all, thank you very much for your blog. I find it pretty useful.

I have opened and funded my IBKR account and I am now ready to invest. Since I am based in Switzerland, my account is funded in CHF. I would like to invest in VTI, which is traded in USD.

My question is about the currency conversion. Do you usually convert CHF to USD manually before buying the ETF, or do you let IBKR convert the currency automatically when placing the order? In other words, should I first convert my CHF balance into USD and only then buy VTI?

I also have a question about the order type. When buying an ETF such as VTI, would you normally use a market order, or would you recommend using a limit order?

Thanks a lot in advance for your help.

Kind regards,

Anita

Hi Anita

Congratulations on deciding to start investing with IB.

That’s a great question. If you are doing conversions below 6500 USD, you should do an automatic conversion, which will be cheaper. Afther that, a manual conversion is cheaper.

As for the order type, I am using market orders: Market orders are fine in 2026

Hi Baptiste, Superb site. Congratulations, and also a big thank you for being so attentive to people’s questions. It’s a big help. I have followed a number of your articles and advice. I am having difficulty at one point though and that is when I am asked to put down my Swiss tax ID, which it will not accept .. I am transposing it directly from my Swiss tax return. Are any other members having the same problem. It is in the format nnn.nnn.nn and it will not take it. There are no other IDs on the forms other than the unique one given to complete it year which is obviously not the right one. Any help gratefully received.

Thanks, Richard!

Actually, it’s indeed unclear. The tax number should be your AVS/AHV number, nothing related to tax. That’s what I entered, and it works as a unique identifier in Switzerland.