US ETFs are the best ETFs for Swiss investors

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

I mostly invest in US ETFs, and I have recommended these ETFs many times on this blog. I consider US ETFs to be the best available ETFs. I have talked several times about what makes them great in various articles. But since I still get many questions, I will go into all the details of these US ETFs.

I am talking about Exchanged Traded Funds (ETFs) that invest in the United States. I talk specifically about ETFs from the United States. What matters here is the domicile of the ETF. This is more important than many people realize.

So, here is what makes these US ETFs great.

Availability of US ETFs

First, we need to address the issue of the availability of US ETFs, or lack thereof.

If you are in the United States, you will not have any issues. However, if you are in Europe, this is another story. Indeed, due to European regulations, many countries lost access to US ETFs.

In fact, in 2018, all the countries part of the European Union lost access to US ETFs. This is due to the PRIIPS regulations. These regulations are part of a bigger package known as MiFID II. These laws force the fund providers to provide a Key Investor Document (KID) in the investor’s language. And so far, US fund providers have not provided them, and they are unlikely to do it. So, for now, European investors cannot invest in US ETFs.

In theory, these laws protect investors by providing them more information on the instruments they are using. However, in practice, they are only here to force people to invest in European funds.

However, Switzerland is not part of the European Union. Therefore, Swiss investors still have access to US ETFs. However, this may change when the Swiss equivalent of the European laws enters into effect. Now, it is not entirely clear if this will apply to foreign brokers (like Interactive Brokers) or not. But for now, we are free to use these ETFs.

I believe these restrictions will not apply to execution-only brokers like Interactive Brokers. So, they should still be available in the future.

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Furthermore, not every broker provides us with access to these ETFs, even though they could do it by law. For now, only foreign brokers, like Interactive Brokers, give access to these ETFs. This is good since Interactive Brokers is the best broker for Swiss investors.

If you want more information on these regulations, you can read my article on the availability of US ETFs.

US ETFs have lower fees

The first advantage of US ETFs is that they have lower fees than their European alternatives.

What matters to us is the Total Expense Ratio (TER) of the ETFs. The TER is the total fee you pay for holding the money. This fee is expressed in percentage and is removed from your money over the year. So, if you have a TER of 0.1% and 100,000 CHF in the fund, you will lose 100 CHF each year to fees.

Since you will pay the fees each year, it is important to optimize them. If you are a passive investor, ongoing fees are the most important cost you can optimize. So, it is important to do it well. And the more money you have in the funds, the more fees you will pay.

We can compare a few ETFs to see the difference in fees:

- Vanguard S&P 500: The US ETF (VOO) has a TER of 0.03%, while the European ETF (VUSA) has a TER of 0.07%, twice as expensive

- Vanguard World: The US ETF (VT) has a TER of 0.06%, while the European ETF (VWRL) has a TER of 0.14%, more than two times more expensive

- iShares S&P 500: The US ETF (IVV) has a TER of 0.03%, while the European ETF (IUSA) has a TER of 0.07%, twice as expensive

- iShares World: The US ETF (URTH) has a TER of 0.24%, while the European ETF (IWRD) has a TER of 0.50%, twice as expensive

As you can see, the TER of European funds is significantly higher than US ETFs. Over the long term, this will make a significant difference in your returns.

When you are investing in ETFs, investing fees are not to be ignored. And this is especially true if you want to retire early based on your portfolio.

US ETFs are more tax-efficient

The second advantage is even more significant, but it is also a bit more complicated and is only for Swiss investors. Indeed, US ETFs are more tax-efficient for Swiss investors.

This tax efficiency is based on the way dividends are taxed. Especially how the US taxes dividends of US companies.

By default, the US government will tax 30% of the dividends emitted by US companies to foreign investors. Now, Switzerland has a tax treaty that reduces this withholding to 15% for Swiss investors, the same amount withheld for US investors. And moreover, we can reclaim the 15% left on our tax declaration.

But when we use an ETF in Europe, the dividends will be withheld before reaching the fund. For instance, if you invest in an ETF from Ireland with Coca-Cola shares, you will lose 15% of these dividends directly. But if these dividends are paid to a US fund, there is no loss!

This advantage is essential since US stocks make up 50% of the entire world stock market. Saving on the dividends of these stocks is very important.

The second-best domicile for ETFs after the US is Ireland. So, if you do not have access to US ETFs, Ireland (IE) ETFs are the next best thing.

Overall, how much you save will depend on the yield of the ETFs you are using. For a 2% yield, you will save 15% of 2%, which is 0.3%. So, by using US ETFs, you can save up to 0.3% in fees every year! On a 100’000 CHF portfolio, you can save 300 CHF per year!

However, it is critical to know that this deduction can only be claimed when it reaches 100 CHF. Below 100 CHF, taxes will reject this deduction. So you will need about 33’000 CHF in US ETFs before you can claim it.

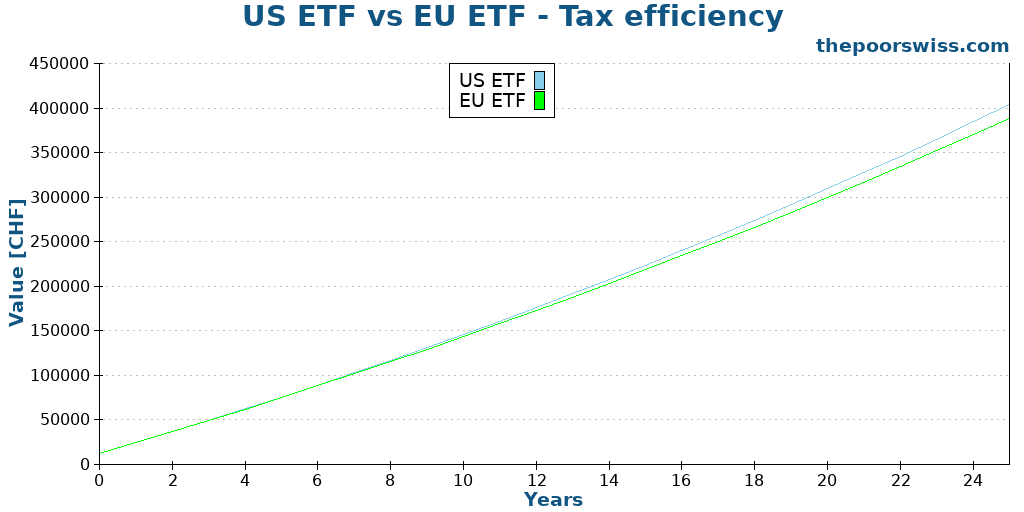

If you are wondering whether this is significant, you can take a look at the following graph. In this example, we are investing 1000 CHF per month over 25 years and the only difference is that we lose 15% of the dividends with

US ETFs are larger

A small advantage is that US ETFs are larger and more liquid. By large, I mean that they are managing more money. Generally, this is exposed as the Assets Under Management (AUM) metric.

A larger ETF has a few advantages over a smaller one:

- It shows more popularity. Larger funds are generally large because they are very popular (people put their money in them).

- It has a lower chance of being closed.

- A larger ETF has a higher trading volume. This has the advantage of the ETF being easier to sell. Generally, they also have a lower spread, which gives you better buying and selling prices.

- A larger ETF can better replicate the index since it will include more small companies than a smaller ETF.

For these reasons, large ETFs are generally better than small ETFs. But this should not be the primary argument in choosing an ETF.

US ETFs are cheaper to trade

The last advantage is that US ETFs are cheaper to trade (with a good broker) than European ETFs.

This is not directly due to the fund itself, but rather to the stock exchange they use.

For instance, my primary ETF, Vanguard Total World (VT), is traded on the New York Stock Exchange (NYSE). To buy or sell shares with Interactive Brokers costs me about 0.35 USD. I can buy many shares and still pay less than a dollar for the transaction.

On the other hand, buying 10’000 CHF of my Swiss ETF, iShares Core SPI ETF (CHSPI) on the Swiss Stock Exchange (SWX), cost me 10 CHF! That is about 30 times more expensive than my US ETFs.

And European ETFs are about in the middle of Swiss ETFs and US ETFs. To my knowledge, US ETFs are the cheapest to trade. Now, this may change if you use a service with free transactions. But there are very few good services like this available in Switzerland yet.

Risks: What about the US Estate Tax?

Many believe we should not invest in US ETFs because of the US Estate Tax. And in some cases, this is true. But in practice, for Swiss investors, there is almost no extra risk in investing in US ETFs.

The US estate tax law states that the inheritance of US ETFs is subject to a 40% inheritance tax. Nonresident aliens (basically, foreigners outside the United States) are exempted from this tax for assets up to 60,000 USD. After this, foreigners will have to pay a 40% tax.

This means that if you have many US assets, they could lose much value when you pass away, and your assets go through inheritance. You do not want this to happen to your estate.

However, many people miss that Switzerland has an estate tax treaty with the United States. And this treaty greatly increases the part exempted from this estate tax!

With this estate tax treaty, Swiss investors are exempted from the US estate tax for up to 11.18 million dollars, prorated to the proportion of US assets in your net worth. For instance, if US ETFs represent 10% of your estate, 1.118 million dollars (10% * 11.18 million) will be exempted from US Estate Tax!

So, in most cases, Swiss investors do not have to worry about the US estate tax! However, it is true that it may complicate your estate. If you have US ETFs, you will need to deal with the IRS.

If you want all the details and many more examples, you can read my in-depth article about the US Estate Tax law. This article also explains how to deal with US estate tax, in the specific case of Interactive Brokers.

What if you cannot use US ETFs?

Unfortunately, many people do not have access to these great US ETFs.

For these people, investing in European ETFs is still an excellent option. Using US ETFs is the best way to invest. However, it is an optimization over European ETFs. There is nothing wrong with investing in European ETFs!

If you want to be optimal, you must go with US ETFs. Now, it could be difficult (or even impossible) to use these ETFs. Even for Swiss investors, few brokers let us access them. If you do not want to go the extra mile and want to invest in good ETFs with lower effort, European ETFs are great!

What matters most is investing, not investing optimally!

What about mutual funds?

In this article, I have talked very specifically about US ETFs, but what about funds?

US mutual funds are also great. But it is interesting to know that Swiss mutual funds can also save you dividends. Indeed, funds are very different from ETFs in how they are held.

With a fund, each investor goes indirectly. With an ETF, you go through a broker who holds the shares in your name.

This allows the fund to be more efficient, directly depending on the treaty. So, a Swiss-domiciled mutual fund is as tax-efficient as a US-domiciled ETF. Of course, the Swiss mutual funds will likely have some other disadvantages (smaller and more expensive, mostly), but it is good to know that the main tax disadvantage of European ETFs is not present in Swiss mutual funds.

Conclusion

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

As you can see, there are many strong reasons to invest in US ETFs instead of European ETFs! These ETFs will let you save a significant amount of money in fees and taxes.

80% of my portfolio is invested in Vanguard Total World (VT), a US ETF. The rest is invested in a Swiss ETF for my home bias portion. So, I invest a considerable portion of my money into US ETFs. This is because I consider these ETFs to be the best available for Swiss investors.

However, these ETFs are more difficult to use. Investors from the European Union cannot invest in them anymore, and in Switzerland, only a few brokers let you use them.

As I mentioned, US ETFs are an optimization over European ETFs, but they are not a revolution. If you cannot (or do not want to) invest in US ETFs, investing in European ETFs will be a great way to invest!

If you want to start trading US ETFs, I recommend using Interactive Brokers. It is an excellent broker that lets you trade US ETFs with very low transaction fees. I have a guide on investing with Interactive Brokers.

Are you investing in US ETFs?

More reading

Should you use ChatGPT for your investing plan?

ChatGPT is capable of answering investing questions. So, should you rely on ChatGPT, like on a financial advisor? I asked it questions to find out.

Impact Investing Interview with Inyova

Invest for good. An interview on Impact Investing: Can you generate market returns while making a positive difference in the world?

One Hour Investor Book Review – Learn investing in one hour

One Hour Investor is a short beginner guide to investing, by Vishal Reddy. It will teach you the basics of investings in about one hour.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste,

I wanted to get your perspective on investing with a 5- to 10-year horizon.

In 2025, the VT ETF increased by approximately 12%, but the US dollar lost about 15% against the Swiss franc. In fact, the Swiss franc gained 10–15% against all major currencies. It turns out those who held savings in a simple CHF cash account last year were not wrong.

Given the current environment—international turmoil, challenges to US and dollar hegemony from BRICS, and the risk of an AI bubble bursting—I find myself rethinking some of the principles that have guided us until now. In this new context, I have a few questions:

1. If everyone begins buying VT (or similar global equity ETFs), could this create a significant bias or overconcentration that long-term investors might eventually pay for?

2. Would you still recommend continuing with an “Always Be Buying” (ABB) and Dollar-Cost Averaging (DCA) approach, with 2 ETfs: 85% in VT and 15% in a Swiss market ETF?

3. What is your view on further diversification in this challenging environment—specifically regarding assets like gold or South Asian ETFs for example?

4. Finally, could finally Swiss franc-hedged ETFs be intersting now?

Thank you—I always appreciate your insight.

Best regards,

Navid

Hi Navid

Yes, our performance was definitely impacted by the USD/CHF changes.

1) I don’t think so. Buying VT basically means buying everything. If everybody was buying a biased ETF, it could create concentration, but I don’t think this could happen with VT.

2) That’s the approach I am following, and I believe it will work for me.

3) Currently, I am not making any changes to our portfolio. Asian stocks are already included in VT.

4) If you believe that the Swiss franc will continue to strongly appreciate in the next few years, then yes.

Hello

It has been a while that I have been with IB but I have never checked whether I am taxed 15% or 30% on the dividends (I am in Switzerland). The reason is that I dont understand and know where the see this. There are so many reports but non has this information easyli accesible. I was able to generate a dividend report for 2024 for example, it provides entries for individual dividends received throughout the year.

Here I found for example the following entry for VEA 2024.03.20 (CHF)

– Qualified other/ Ordinary dividend: Gross 0.19; Withold -0.03

– Not qualfied /Ordinary dividend: Gross 0.07; Withold -0.01

And at the end there is a Revenu summary (CHF):

– Total ordinary dividends 136.43

– Total non USA ordinary dividends 3.78

– US tax paid 20.05

– Non US tax paid 1.32

– Return of capital distributions 0.36

– Total pazments in lieu received 1.01

My questions:

1) So does this look correct, they take only 15%, not 30%, correct? Is there a simpler way to see this?

2) Strange – I would have expexted more dividends as I had around 100K in assets – where can I investigate this further?

3) Also, from time to time I receive email alerts like the following one, but i dont know where to see what I actually got: Cash Dividend: IBKR@NASDAQ (Name: INTERACTIVE BROKERS GRO-CL A) announced a cash dividend with an ex-dividend date of 20251201 and a payable date of 20251212. The declared cash rate is USD 0.08. ISIN: US45841N1072

Please advice and sorry for my beginner questions..

Regards

Marco

Hi Marco

1) Yes, 20.05 appears to be about 15% of 136.43

2) If you have 100k in assets and 136 in dividends, this is very low, a yield of 0.13%. Are some of your ETFs accumulating maybe? You can generate an activity statement for the entire year and see all the divideneds.

3) If you do a full activity statement, you will see all the dividends you got

I hope this helps.

Hello There!

Thanks for your great work! Me and my wife are finally ready-sih to take the first step and start investing. We earn and spend in CHF and are looking to invest 20k and over the years add to it as we go and have disposable income. So far I have my eyes set on IB and probably a mix of US and EU ETFs with a buy and hold strategy, as I don’t have the capacity, the experience and the nerves for active trading. Everything seems to be pointing in the direction of US ETFs, but my big dilemma, that doesn’t seem to come up very often is the USD-CHF (and low key also the EUR-CHF) exchange ratio. The CHF getting stronger is a pure loss, if I am looking top spend later in CHF. To my beginner mind the upsides of tax efficiency and lower TER with US ETFs seem miniscule when compared to the potential loss, which necessary occurs if CHF continues to get stronger. Or is the US market outperforming ours so much, that even if we lose like 10% (HUGE number) on strong CHF after investing for years into US ETFs, we still are better off than if we invested in CHF all along? I guess diversification if also a key thing, but I am kind of mortified by looking at the USD-CHF and EUR-CHF graphs.. A dollar is worth half as much as it did 30 years ago..

Ok, a short unprofesisonal research tells me that during its lifetime VT and VWRL more-or-less quadruppled, while CHSPI only gained 50%. I guess higher dividends in CH also makes the math more complex than just pitting 400% (plus all the little upsides, minus the loss due to strong CHF) against 50%..

How should one think about this topic?

Hi Peter,

Congratulations to decide to start investing.

I do believe that we are better off in the long term with non-hedged instruments than with hedged instruments. That being said, if it helps you sleep at night, you can use CHF-hedged instruments. But beware that you really need hedged CHF funds to fight the curency risk; funds traded in CHF do not reduce the risks.

As for your last point, normally most graphs will include dividends. Over 10 years, CHSPI had an 84% performance per year, or 6.29% annualized, which is really not too bad.

Thank you for these insights, Baptiste, very helpful.

Could you clarify a few things further, please?

1. What do you mean by “And moreover, we can reclaim the 15% left on our tax declaration”? Are you saying that the US ETFs have 15% withholding tax and you can get that back through the DA-1 form, essentially paying 0% withholding tax?

2. “But when we use an ETF in Europe, the dividends will be withheld before reaching the fund.” I thought that you said above that the US ETFs also have a 15% withholding tax?

3. You say: “For instance, if you invest in an ETF from Ireland with Coca-Cola shares, you will lose 15% of these dividends directly. But if these dividends are paid to a US fund, there is no loss!” What do you mean by ‘loss’ in these two sentences? Can you please explain better?

4. What are the tax implications of holding a US-domiciled ETF that consists of US and non-US stocks (e.g. 55/45% split) over this ETF being domiciled in IE? (If you are a Swiss resident investing with IBKR.)

Many thanks in advance for further clarity on these.

Hi Igi,

1) Exactly that.

2) Yes, they both have it. But if it’s not a US fund, the money is lost before reaching Ireland. In the case of US fund, you hold it directly, therefore you can reclaim it.

3) If Coca Cola pays 100 USD dividend, you will receive 85 USD in both cases. Otherwise, you can reclaim 15 USD from your taxes if you have a US ETF.

4) The efficiency will be better for the 55% US part.

Thank you for this article!

What about currency exchange? I earn in CHF and spend in CHF. If I want to set up a savings plan or invest in stages, additional fees for the currency exchange are charged each time (IBKR minimum of USD 2 per currency exchange).

For a staged investment, I can convert the entire amount into USD at once. This saves me exchange fees, but I lose money due to the USD/CHF exchange rate (especially these days). The currency exchange would then no longer be staged, only the investment itself.

What do you recommend for savings plans and what do you recommend for staged investments?

Best regards

Hi Dario

Actually, with IBKR, you can convert for less than 2 USD if you do an automated conversions. This is cheaper than 2 USD if you convert less than 6500 USD. This should be automatically used if you use their recurrinv investments: Automate your investments with Interactive Brokers in 2025

IB does not really have a savings plan but recurring orders which allow you to do more or less the same.

I always invest all I have at once and do one currency conversion.

Thank you very much for your reply. I’ll try automated conversions.

US-domiciled ETFs are attractive, but many overlook the risk of up to 40% US estate tax on all US assets above $60,000 for non-resident aliens if they die. Swiss-domiciled investors benefit from the US-Switzerland estate tax treaty, which allows a much higher exemption (up to $14M) determined by the share of US assets in your global estate, typically shielding most investors from this risk, though a complex IRS filing process is still required.

Very important: if you later change your domicile to a country without a US estate tax treaty (such as most EU countries), you lose this protection and revert to the standard $60,000 exemption, with 40% estate tax due on any excess.

What’s the solution? To permanently avoid this mortal issue, consider Ireland-domiciled ETFs – UCITS, which do not carry US estate tax exposure for non-US residents, regardless of future changes in residency.

Hi Nik

It’s true that it can create some filing process. However, if you are below the exemption, the process is not too difficult. I have described it in another article: Should Swiss investors worry about the US Estate Tax in 2025?

But of course, if you want to limit the complexity to the minimum, you can choose to avoid US ETFs entirely.

Great article, thanks. Suggest you extend it wrt double taxation applied to US domiciled ETFs in case of Non-US stocks. This is a disadvantage for ETFs primarily consisting of Non-US assets like VGK, VWO and others.

Yes, you can reclaim the US withholding tax with DA-1 to break even. But only if you declare enough taxable income at the same time. And that is not usually the case with FIRE. With low income Irish ETFs are better for Non-US assets for this aspect.

Hi Capmac,

Yes, it’s true that US ETFs are best for US stocks, not necessarily for other. But since they make up much of the world, they are great for world ETF. But I should that clearer, good point.

Basically you loose 15% of dividends with low income.

It begs the question if it is better to separate out US stock/assets from the rest in a dedicated ETF, and not use world ETFs either. In case of low income that is. World ETFs still hold 35% assets not in the US. Also gives you more freedom to change the ratio of investments between USA and ROW.

I think it is not worth the extra complexity, but this may depend on each case.

Hi Baptiste,

This blog post was very insightful, especially how Swiss investors can benefit. Thank you!

How do you think the new Swiss “revenge tax” will influence the situation? Especially the VT total world ETF? Maybe the topic deserves its own blog post?

Hi Martin

By revenge tag, Are you talking about section 899 of the big beautiful bill? I have opened the discussion about that on the forums: Should we worry about section 899 of The Big Beautiful Bill?

Or are you talking about revenge from Switzerland? In this case, I have not heard aobut it.

Yes, I was taking about the section 899 of the big beautiful bill. Thanks for the forum link.

You mention IE ETFs, what does IE stand for?

Ireland :)

Dear Baptiste,

First of all congratulations for this great website, it has served me a lot to better understand Switzerland.

You mention that US based ETF are financially better than their equivalents based in Ireland. However if I compare an accumulating ETF based in Ireland (VUSA with a TER of 0.07) with VOO distributing ETF based in USA I get a slightly better result for VUSA (around 0.3 % on a yearly basis) despite the higher TER.

Based on this I would also recommend to check the accumulating Irish ETF’s if I don’t need the periodic dividends payment.

Do you agree ?

Hi Ricardo

No, I do not agree :)

This comparison does not take into account the dividends you can get back by filing a DA-1 form. With VOO, you will get back 15% of US dividends on your tax declaration. But with a IE ETF, these 15% are lost.

Hi Baptiste,

Correct ! From the US tax perspective there is an advantage with VOO, but what about from the Swiss perspective ? Isn’t there and advantage for the accumulative ETF as there is no tax due to the fact that there are no dividends ?

No :) In Switzerland, we are taxed the same way whether an ETF is accumulating or distributing.

I am using IE based etfs and I don’t get taxed on dividends

If you are in Switzerland, you should declare the dividends on your tax declaration and then you should be taxed on it.

And the fund itself is going to be taxed 15% at source for all US dividends.

Dear Paptiste

Need your help regarding investing in a Europe ETF.

Is it more Taxi efficient to invest in VGK (US domizil, USD) or some fund in Ireland in Euro? Mist important for me is to get the maximum back from dividend tax.

I Wonder if US ETFs are only favorable if the stocks are in US…

Thank you!

Hi Susanne,

US ETFs should be preferred for US stocks and World Stocks (because they contain US stocks). But on the other hand, they have no advantage for European stocks.

So, in your case, you can get an Ireland fund in Euro and you should be fine. But you would also be fine with a US fund in USD if you prefer.