Investing Fees could cost you your early retirement!

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

When you are investing, you want to minimize your investing fees. It is something most people already realize. But what most people do not realize is how expensive fees can be in the long term.

In this article, we see precisely how much investing fees are hurting you! Not only will we see that they are more expensive than they seem. We will also see that investing fees have a significant impact on your retirement!

And of course, we cover different kinds of fees there are (there are more than you think!). Finally, I will give you a few pointers on how to reduce all these fees.

Types of investing fees

When you are investing, there are many different types of investing fees. It is essential to know about them to avoid them.

Of course, there are some fees that you cannot avoid. But you can still minimize them. And some fees are more important than others so you will need to consider them first.

Management Fees

The most important investing fee is the management fee.

Management fees are something you will pay every year on the stock market funds you are investing in. In funds, this is called the Total Expense Ratio (TER).

The reason this fee is very important is that it is set in % of your invested money. It means that you will lose some percentage of your money year after year. The more money you have, the more fees you will pay!

While there are some mutual funds and ETFs with 0% TER, it is still very rare. Therefore, you cannot entirely avoid this tax. But you can minimize it.

Unfortunately, there are some considerable discrepancies between funds and ETFs. For instance, my primary ETF is Vanguard Total World (VT), with a TER of 0.08%. If you take the PostFinance Fonds Global A that invests similarly, it has a TER of 0.80%. This ETF is ten times more expensive!

And you can find even more expensive funds. For instance, another similar fund, the Raiffeisen Global Invest Equity A, with 1.32% TER! And the UBS Vitainvest 100 World U is coming at 1.61% TER! This ETF is 20 times more expensive than VT!

By choosing the fund with the lowest TER, you can divide your management fee by twenty! It is a lot of money!

We can take a simple example. If you have 100’000 CHF invested in this fund, VT will cost you 80 CHF per year. But with UBS, you will lose 1610 CHF per year! And this is only for one year. The long-term costs are much higher, as we will see shortly. We will see in the next section that this could mean the difference between early and late retirement.

So, you need to minimize management fees! And you need to check these fees. When you choose a fund, a financial service, or a broker, you need to read well about all the fees they may have. Sometimes, they are not transparent, and some fees are hidden. You want to do your research correctly.

Issuance and redemption fees

There is another fee you must be very careful about, issuance and redemption fees!

An issuance fee is a fee that is paid when you buy shares of a mutual fund (or another investment). And a redemption fee is a fee that is paid when you sell shares of a mutual fund (or another investment).

These two fees are generally expressed in percentages. For instance, if you have an issuance fee of 0.2% and a redemption fee of 0.3%, you will pay 2 CHF to buy 1000 CHF of shares and pay 3 CHF to sell 1000 CHF of shares.

Many believe these fees are less critical since they are only paid once. This fee indeed has less impact than the management fees. However, they can have a significant impact.

What is essential to know is that there are many funds without any issuance and redemption fees! It means that you can avoid this fee entirely! So, there is no reason to pay an issuance and redemption fee.

Secondly, even a 0.1% fee will weigh you down long-term. If you invest 10’000 CHF right now and you directly lose 10 CHF, this means your investment is in negative territory directly. And the issuance fee will also take a cut of your returns. If you sell after ten years and double your investments, you do not want to give away even 0.2% of this!

The great news is: if you invest in ETFs, there are no such things as redemption and issuance fees! And some good mutual funds like Vanguard do not have such fees either.

So, you should only choose ETFs or mutual funds with no issuance and redemption fee. And when you are presented with an investment, make sure to check these fees.

In 2023, there is no reason to pay issuance and redemption fees

Transaction fees

When you invest in the stock market, you must use a broker. And broker will introduce a new set of fees: the transaction fees.

Every time you do a transaction on the stock market, you will pay some fees. You will generally pay the same transaction costs when you buy and sell.

The differences between brokers can be huge. You can easily find brokers ten times more expensive than others when you invest. For instance, buying 100 shares of Novartis will cost you 5 CHF with Interactive Brokers and 40 CHF with Migros.

And on the U.S. Stock market, the difference is much more significant. Buying 100 shares of Microsoft will cost you 0.36 USD with Interactive Brokers and 80 USD with Swissquote! Swissquote is 200 times more expensive for this trade!

If you invest monthly, like me, these fees can quickly add up to several hundred CHF per year. So, you need to be careful.

Custody fees

Sometimes, some brokers will make you pay custody fees. And more likely, some financial services will also make you pay a custody fee.

There are two kinds of custody fees:

- The custody fees with a fixed amount. While you want to minimize them, they are not so bad unless you are starting up.

- The custody fees with a percentage. These fees are the same as management fees and should be minimized or avoided.

When you choose a broker, you want to avoid custody fees in percentage. If there is a maximum per year or quarter, it is not that bad. But without a maximum, you can pay a lot of your fees. For instance, Migros Bank has a custody fee of 0.23% per year without a maximum. I would never invest with a broker with a percent-based custody fee and no maximum. The problem is that most people will not even verify this!

When you choose a financial service like a robo-advisor, you want to select the cheapest one for your needs. These services always have a custody fee. You will not be able to avoid it. But you need to find the one with the lowest fee that fits your needs.

So make sure you are avoiding brokers with custody fees and choosing financial services with low custody fees.

Never invest with a broker with a percent-based custody fee and no maximum

Taxes

Now, in some countries, you must pay taxes on your portfolio. They are not directly investing fees. But they will have the same effect. Two kinds of taxes could be important here.

The first important tax is a wealth tax. This kind of tax is based on a percentage of your net wealth. So, the wealth tax has the same effect as a management fee except that you will pay it in cash, and it will not be removed from your portfolio. And Switzerland has a wealth tax, so you need not forget that.

The other important tax is the dividend tax. Since the dividends are a percentage of your net worth, any tax on dividends will also be a percentage of your net worth! Once again, this acts in the same way as a management fee. For instance, if you pay 10% taxes on your 2% dividends, this is a 0.2% tax over your entire portfolio. A 0.2% tax is very significant, as we will see shortly.

The long-term cost of investing fees

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

Now that we have seen the different fees, we can take a look at the long-term impact of the investing fees.

You may think a few hundred in fees here and there is not so bad. But over the long term, it can make a very significant difference. And you need to be aware of that to motivate you to minimize these fees.

For this, we will make a few simple simulations with different management fees. If you have a custody fee in % of your net worth (robo-advisors, for instance), you can treat it as a management fee. It is important to consider everything together.

I will not make simulations with transaction fees and issuance fees because there are too many factors going on. But it will still make a significant difference in the long term! Unless you invest with a stupidly expensive broker, transaction costs do not matter much in the long term.

And the impact of redemption fees is pretty easy to understand. If you have a redemption fee of 0.3%, you must increase your net worth by 0.31% to be financially independent. When looking at a 2 million net worth, this is an extra 6200 CHF that you need! But this is not nearly as bad as a 0.3% management fee!

For each period, I will do two simulations. For the first one, I will simply take a 5% yearly return for the simulation. These are somehow reasonable returns to expect.

And in a second time, I will compute the historical chances of successful retirement with different investing fees. For this, I use the 4% Rule. If you do not know about this, I encourage you to read my article about Trinity Study results. In this article, you will find the details of my simulations.

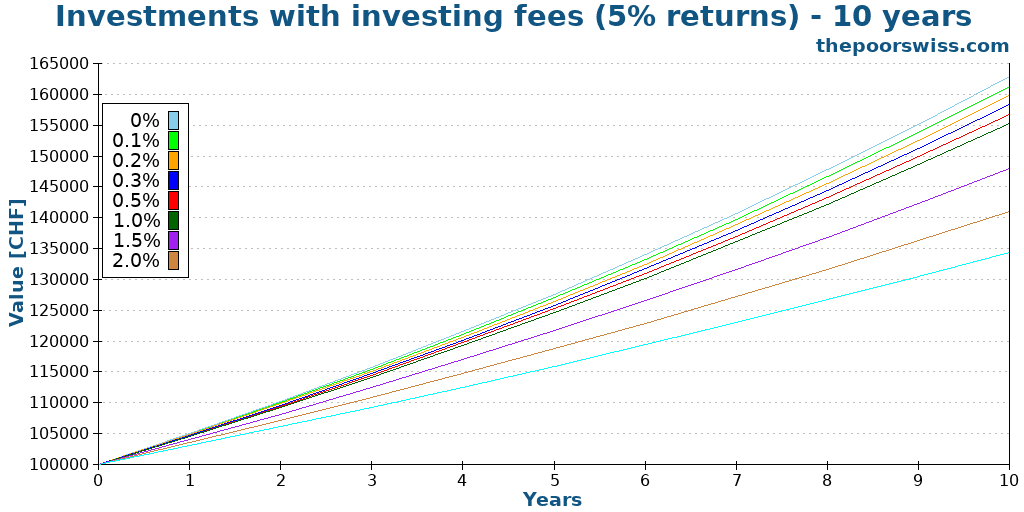

Impact over 10 years

We start with the impact of fees over ten years. Ten years is a short time for investing.

Here is the evolution of a portfolio starting at 100’000 CHF from 0 to 10 years with different levels of fees.

There is one thing crucial to understand in this graph: the impact of fees becomes greater and greater as more years go by. Most people do not realize this. All the fees you pay do not compound! So, all the fees that you can avoid will compound year after year. Compounding makes a very significant difference.

Most people think they will pay the same amount of fee every year. But if the portfolio gets bigger, so do the fees. So fees also compound if your portfolio compounds! And you lose more money to fees than only the fees you pay. There is also the lost opportunity of having these fees compound into your portfolio.

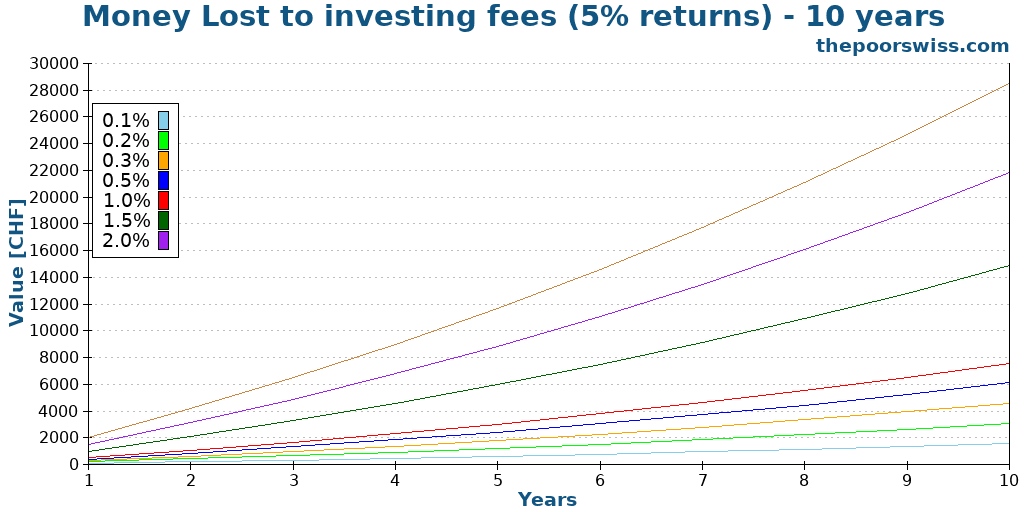

Here is how much money you will lose with fees:

With a 100’000 CHF portfolio, you can lose more than 28’000 CHF over ten years to investing fees. 28’000 CHF is a huge amount! A 2.0% fee is very high, but it is not impossible. There are mutual funds out there with such a fee. Do you want to lose 28’000 CHF?

Even a 1.0% fee per year will cost you 14’000 CHF! If you can reduce to a 0.5% fee, you will save more than 7’000 CHF! And this is only for ten years and only for a 100’000 CHF portfolio!

Even over ten years, we can see that investing fees matter! You cannot ignore fees when you are investing in the long term! You need to think of investing fees like you are thinking of bills.

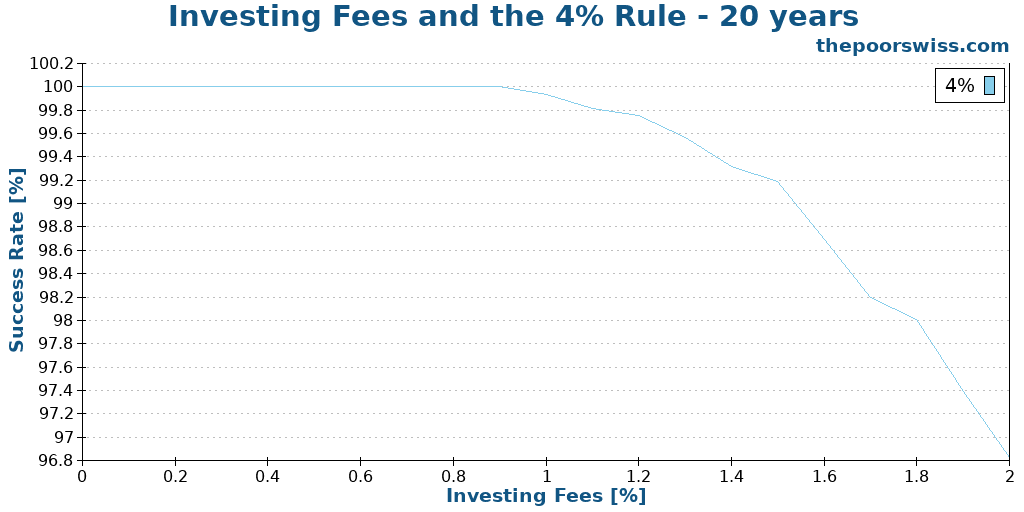

The analysis of retirement success rate for ten years is not very interesting. Indeed, even with 2% fees, you still have a 100% chance of success, so we keep that for 20 years.

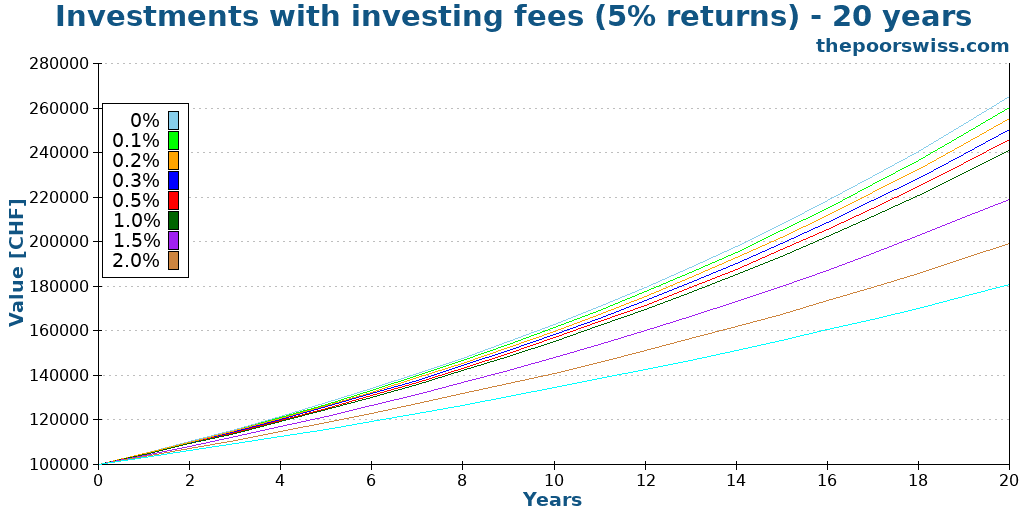

Impact over 20 years

Ideally, you want to invest a long time. So, here is what happens with these investing fees over 20 years.

Over 20 years, the differences between investing fees are much more significant. As your money grows longer, you lose even more to fees. The fees you lose the first year will not compound for the next 19 years. And as your portfolio grows, the fees you are paying are growing higher and higher as well.

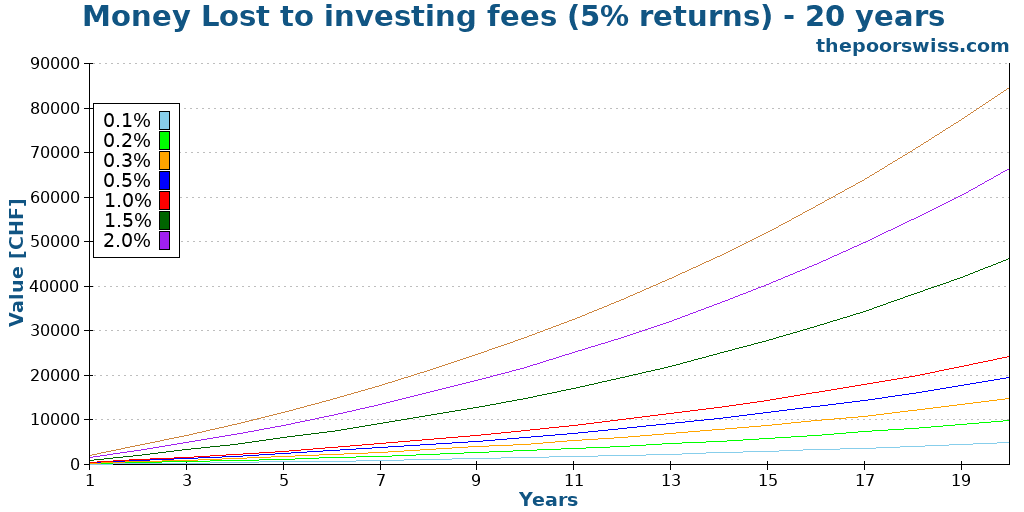

So, here is exactly how much we are losing to fees:

As you can see, the amount lost to fees is pretty impressive over 20 years! If you pay a 2.0% fee each year, you will have lost 80’000 CHF. I am sure you can think of better things to do with 80’000 CHF than giving it away!

Over 20 years, the difference between 0.2% and 1.0% fee is already more than 36’000! You do not want to pay anything more than a 1.0% fee!

If you plan to retire early using the 4% rule (or any other withdrawal rate), you may be interested in knowing how much investing fees could impact your chances of a successful retirement (not running out of money).

I did the simulation for an 80% U.S. stock portfolio and a 4% withdrawal rate. I am using U.S. inflation here as a reference. Here are the results with different levels of investing fees:

Interestingly, investing fees will not have a substantial effect on your chances of success. However, a 2.0% fee will reduce your chances by 5%. A 95% chance of success is still a good result. But we must keep in mind that this is only for 20 years. Twenty years is still a short retirement by any means.

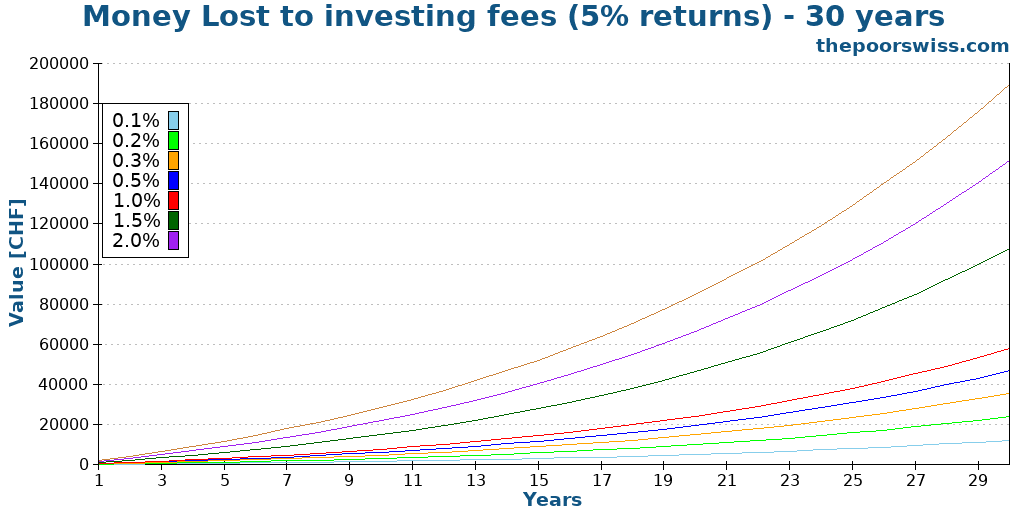

Impact over 30 years

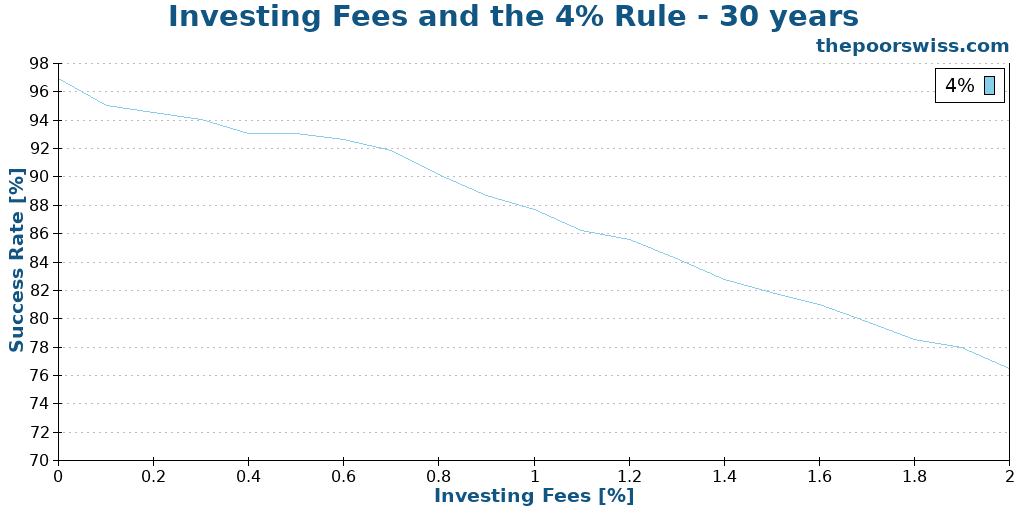

Then, we look at the impact of investing fees over 30 years. 30 years is a period that is already more reasonable for early retirement.

Here is directly how much money we lose to fees:

After 30 years, a 2.0% fee could cost you almost 200’000 CHF! These amounts are getting extremely significant. It is more money than most people ever save.

By going from a 1.0% fee to a 0.2% fee, you can save over 80’000 CHF! We are talking about a huge amount of money that can make a significant difference! If you had a portfolio of 1’000’000 to start with, you would get a difference of 800’000 CHF after 30 years!

It is very interesting to note that after 30 years, the lost compounding value is higher than the fees paid. And this gets even more true for a higher number of years!

We can check our retirement simulation again for 30 years.

This time the impact of investing fees is significant! A 1.0% fee will cost you more than a 10% chance of success. And a 2.0% fee will cost you more than 20% chances!

If you pay a 1.0% fee or more, you will likely have to use a lower withdrawal rate than 4.0%. When you are planning for the future, it is essential to take this into account. Reducing your chances of success by 10% is already very dangerous. Some people can plan for a 90% chance of success. But many fewer people can accept an 80% chance of success.

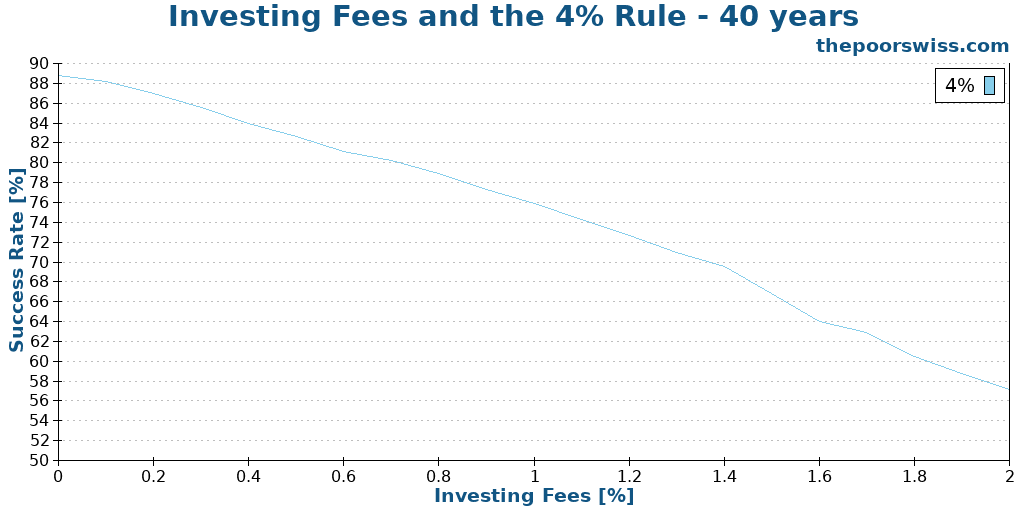

Impact on 40 years of retirement

We will repeat our retirement simulation for 40 years now. I will not repeat the first experiment since, by now, you should have seen the significant impact of these investing fees.

Over 40 years, investing fees have a devastating impact! Even a 1.0% fee reduces your chances of success to less than 80%! It means that with such a fee, the 4% rule fails! And with 2.0%, your chances of success are even below 60%.

If you are investing in ETFs yourself, it is likely that your investment fees are significantly lower than 1.0%. But even a 0.2% fee diminishes your chance of success by 2.5%. So going from a 0.5% fee to a 0.2% fee will increase your chances of success by 4%. If you are investing with an expensive robo-advisor, you will have to take this into account if you plan for early retirement.

We can conclude two things at this point:

- Investing fees have a significant impact on your chances of success in retirement if you follow the 4% rule.

- Over a long retirement period, even a small change in fee can have a significant impact.

How to reduce investing fees

We have now seen that investing fees have a significant impact in the long term. So, here are a few practical things we can do to reduce them.

Only use ETFs with low TER

The first thing you should do is invest only in cheap ETFs and mutual funds.

If you are in Switzerland, like us, you want to choose only Exchange Traded Funds. Indeed, there are no good mutual funds available in Switzerland. If you are in another country with access to good mutual funds like the ones from Vanguard, you can also consider them!

When you choose ETFs (or mutual funds), you want to focus on those with a very low Total Expense Ratio (TER). The TER is the management fee per year of the funds. And this will be removed from your net worth year after year. Doing so is the most important thing you can do to reduce your investing fees.

These days, there is never any reason to pay more than 0.4% TER for a fund. And ideally, you want to focus on ETFs with significantly less than that.

Now, the TER should not be the only factor you use to compare ETFs, but it is an important one. I have a guide on choosing Exchange Traded Funds if you need additional information.

Use the best broker

Transaction costs are less important than management because they do not represent a portion of your assets.

But this does not mean they are not important either. If every time you invest something, you lose 50 CHF. It is not ideal. And you need to remember that you will also pay transaction costs when you sell your assets.

You especially want to avoid all significant fees proportional to the amount invested. But generally, with good brokers, these are so small they almost are not significant.

When you choose a broker, you need to avoid choosing one with a percentage custody fee. Fortunately, there are plenty of good brokers without such fees, so you will never have to pay for it.

But there are other factors at play here. For instance, if you are using a Swiss broker, you will pay up to 0.15% stamp tax duty on each buy and sell operations. This fee is not as bad as a management fee. But this is still something that you want to avoid.

You do not have all the research yourself. I have an article on the best brokers for Swiss investors.

Use the best third pillar

Another place where you will have to pay investing fees is in your third pillar. And again, you want to minimize these fees.

The first thing you want in a third pillar is to invest it in stocks. Most people do not invest the money in their third pillar. But there are now several good third pillars with a large amount invested into stocks.

To choose between these few good third pillar providers, you need to look at their fees. You will not find something as cheap as a Vanguard ETF. But you can now find third pillars with a 0.5% fee or less, which is reasonable compared to other alternatives.

If you do not know where to start, read my article about the best third pillar in Switzerland.

Use the cheapest robo-advisor

If you are not investing by yourself, you will probably want to use a robo-advisor. For this, you will pay a management fee each year.

The price of a robo-advisor is not the only criterion you should use. However, it is an essential one. As we saw before, the difference in returns is quite significant.

So make sure you are choosing a robo-advisor with reasonable fees. I have talked about several robo-advisors in Switzerland. They are not cheap by any means. But there are some more reasonable than others.

Optimize your taxes

We have also seen that taxes can weigh heavily on your fees. There are a few things we can do to reduce this part of the fees.

If you want to reduce your wealth tax, the only thing you can do is move to another state. There are some very significant differences in taxes between the different states. For more information, you can read my post about Geo-Arbitrage in Switzerland. Of course, this is only doable if you are not too attached to your place or live near a border.

There are two ways to reduce your dividend taxes. First, you need to invest in efficient ETFs. Currently, the best ETFs for Swiss investors are U.S. ETFs. It is because you can reclaim 15% of the dividends withheld in the United States.

Secondly, you can avoid investing in companies with high dividend yields and focus on growth. If you want to be diversified, it is impossible to avoid all dividends. But you can avoid investing in funds focused on dividends.

Conclusion

By now, you should understand that investing fees are essential. You cannot ignore investing fees if you are serious about investing!

In the long term, even a 0.1% extra investing fee will cost you much money. And extreme fees also diminish your chances of retiring early. Reducing your investing fees should be a priority!

If you realize this, you also need to minimize fees as much as possible to get the most out of your investments. There is no point in investing if most of your earnings go to your bank, broker, or advisor.

One problem with investing fees is that people do not pay them as bills. If people received a 10’000 CHF bill for a 1.0% fee on a one-million portfolio, they would be more eager to optimize it. But investing fees are vicious in that they are almost invisible. So people tend to forget about them.

If you are investing directly by yourself with a broker, the most important thing you should do is invest in ETFs that have a low Total Expense Ratio (TER). Then, you also need to minimize your transaction costs by choosing an affordable broker.

If you are not investing by yourself and you prefer robo-advisors, you need to make sure you are using the cheapest one that fits your needs. You will pay more in fees than when DIY investing. But investing with a robo-advisor is much better than not investing at all!

If you do not know where to start, you can start by looking at the best ETF portfolio for Swiss investors.

Did you realize investing fees were so important? Do you know how much in fees you are paying?

More reading

The Three-Fund Portfolio Makes Investing Simple – 3 funds are enough

A Three-Fund Portfolio is a very simple, yet very efffective, way to invest. It is especially suited for beginners who do not know in what to invest.

Swiss Stamp Tax Duty – All you need to know

Avoid extra fees. Learn what the Swiss Stamp Tax Duty is, how much it costs, and how to choose a broker that helps you avoid paying it.

How to Choose a Stock Market Index for 2026

S&P 500 or MSCI World? Learn how to choose the best stock market index for your strategy and diversify your investments effectively.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

A good alternative to Interactive Brokers is Saxobank IF you open an account booked in DENMARK to avoid Swiss Stamp Duty (completely legal). I would not recommend anyone who is trying to minimize costs to have an investment account booked in Switzerland.

Hi Anton

Interesting, I never thought about using another Saxo entity. Can you deposit CHF for free in this case?

This would be closer to IB indeed if you can save on the stamp duty.

Thanks for sharing!

The best way to reduce FX spreads in my opinion is to transfer CHF to Interactive Brokers, then to actual separate FX trades (buy USD.CHF, min 25k in each trade to get the interbank rate and dilute the USD 2 commission), then use the USD cash from those trades to buy US(D) ETFs.

AVOID buying ETFs if you don’t already have enough cash in the right currency since Interactive Brokers will then automatically do an FX trade in the background with much higher fees than a direct FX trade.

Hi Anton

I would say it depends on how much you are converting. If you convert less than 6500, an automatic conversion will be cheaper.

But you are right, that if you can convert more than 25k at a time, this will be very efficient. However, for most people, this means a long time to accumulate. I think it’s better to lose a little on currency conversion and invest more frequently rather than wait too long.

Hi there,

Could advise on Forex risk snd hedging costs. Up till now I have only invested in Swiss stocks directly to avoid forex and fund managing fees. The euro/ chf has gone ftom 1.0/1.20 to strengthen to 1.0/0.92 in ten years. Some experts are predicting the demise of the USD as the worlds reserve currency. What do you think?

Hi Graham

As a Swiss investor, when we buy equities in foreign currencies, we must expect that we will not have the same returns in CHF than people have in USD. So, we are paying the price of having a very strong currency. Historically, this was compensated by higher stock returns outside of Switzerland.

In the short-term, currency hedging is a very good tool. But I do not believe it is worth it in the long term.

Should you use currency hedging in your portfolio?

Thanks for all your analyses! I’ve been looking at the fees with VZ (I use them for my 3rd pillar and am wondering if they are an interesting alternative to Swissquote for investments). I’m not sure how to interpret them and therefore if they might be better!

https://www.vermoegenszentrum.ch/fr/operations-bancaires/modeles-de-frais

If you ever feel inspired to add VZ to your analyses/comparisons, I’d be very interested to read them!

Hi Stephanie,

Are you wondering about the fees for the 3a or for the brokerage services? For the 3a, they are not very interesting at 0.83%. I will soon have an article on the 3a.

For the brokerage services, I did not study them in detail, but at first sight, they do not look appealing. The all-in-one system would come to at least 1750 CHF in fee per year, which is bad and the standard system would come at 39 CHF per transaction and multiple recurring fees which is not great at all.

of course the question on the fees is already well andwered.

however as to sound customer and even non-customer information material VZ is outstanding. you can opt for their free newsletter (email or print) as well many extra topics material.

they very much recommend ETF investing, f ex, more than any other mainstream bank/advizor.

try it !

best wishes

FrankieS

It’s a good point. They do indeed recommend good investing practices, but then they directly point to their services which are far from the best.

I was wondering about the brokerage!

Will keep my eyes peeled for your article on the 3a, didn’t think it was a bad deal 🤔

I am REALLY picky when it comes to TER.

My current IBKR portfolio TER is 0.0458% (48% VTI @ 0.03, 28% VXUS @ 0.07, 10% GOVT @ 0.05, 10% SCHP @ 0.04, and 4% SCHH @ 0.07). About 46 bucks every 100k is pretty reasonable IMHO.

I have also selected Finpension funds with the lowest issuance and redemption fees I could find, while avoiding as much hedging as possible:

83% Swisscanto IPF I Index Equity Fund World ex CH NT CHF

7% Swisscanto Index Equity Fund Switzerland Total (I) NT CHF

5% CSIF III Real Estate World ex CH – Pension Fund ZB

4% Swisscanto Index Commodity Fund hedged CHF NTH CHF (the least worst of commodity funds)

If only Finpension slashed their TER by half I would be very happy. :)

Forgot to mention I also turned off rebalancing in my Finpension portfolios. No need for that when every new contribution more or less rebalances the overall portfolio and I get rid of redemption/issuance fees from moving from one fund to another.

It’s all a matter of scale. Vanguard can have a TER of 0.07 because they manage trillions. It’s not possible with Finpension that managers a few billion in a country like Switzerland. They have to make money, they are not a charity and they are already among the cheapest. I am quite happy about their fees.

Don’t forget to consider VTI from Vanguard. (if you want to invest in US Stocks) TER = 0.03%.

True, using a good ETF is very important!

As a novice investor, I created some finpension 3a strategies with hugely overlapping instruments like:

CSIF (CH) III Equity US Blue – Pension Fund ZB

CSIF (CH) III Equity World ex CH Blue – Pension Fund Plus ZB

CSIF (CH) III Equity World ex CH Blue – Pension Fund Plus ZBH

Portfolio performs well, but do you think there is a significant drawback in fees when using overlapping funds?

Also, in the finpension, they often mention that TER is 0%, but there is an annual administration fee for example 0.39%. Is it at the end the same thing as TER of 0.39%?

Hi giovere

If you are a novice, I am not sure you should really do your own portfolios.

That being said, your portfolio is not too bad, but you should simplify it. The US fund gives you a bias towards US, which may make sense if you want to do that.

The other two funds give you a lot of international diversification. One of them is hedged to CHF while the other is not. This could allow you to configure amout of hedging you want.

It would probably be simpler to either use either only the second or only the third fund.

TER is generally only related to funds. But yes, for the customers, what matters is total charge, so TER + management fees. 0.39% is what matters to us.

An often hidden/overlooked but very significant

problem are currency switch fees,

f ex when I buy U.S.-domiciled ETFs investing part of my

CHF-salary via a CH-broker. Would be ‘wiser’ to transfer CHF-funds via Wise (or other) into the USD-account of the CH-broker.

bye,

FrankieS

Hi Frankie

Yes, this fee is essential. Swiss brokers are horrendous for currency conversion. A 0.95% fee for instance, will cost a lot when withdrawing from the portfolio.