Updated Trinity Study for 2026- More Withdrawal Rates!

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Would you like to know precisely which withdrawal rate is safe and will sustain your lifestyle for a long time?

You will find the answer in this article, with updated results from the Trinity Study! This study researched different withdrawal rates for retirement. Although the original research was not about early retirement, it is often referred to in the Financial Independence and Retire Early (FIRE) movement!

However, there are two caveats to the original study. First, they are only covering the period until 1995. And then, they are not covering more than thirty years of retirement. Thirty years is not enough for some people wanting to retire early.

Therefore, I reproduce the original study’s results with recent data all the way to 2025! And I extended the data back to 1871. This makes for much more data than the original study.

I have also considered periods as long as 50 years. It means many more withdrawal simulations than the original study.

In this article, you will find how I did it and all the results I have gathered from this data!

The Trinity Study

I have already talked at great length about the Trinity Study. It is an excellent research paper done by three professors from Trinity University.

Their research paper’s goal was to see which withdrawal rates people should use to sustain a particular lifestyle for up to 30 years. It is important to note that the original research was not about early retirement but official retirement.

It is important to emphasize that we are talking about sustaining a lifestyle (expenses), not capital. So, if you end up with 1 USD at the end of the retirement period, this is a success. If you want to sustain your capital in retirement, it is a different success criterion not treated by the original Trinity study.

They tested the success rates of withdrawal rates from 3% to 12%. Furthermore, they tested portfolios with between 0% and 100% stocks by jumps of 25%.

The authors also took inflation into account in the results. Indeed, it is interesting to compare the results with and without inflation. Finally, they also provided the terminal values of the portfolio.

I wrote a detailed article about the Trinity Study if you want more information.

The 4% Rule (of Thumb)

The Trinity Study is the source of the 4% Rule. This rule states that if you only withdraw 4% of your initial portfolio yearly, you can sustain your lifestyle for a very long period. And your withdrawal is adjusted for inflation every year.

Some people believe that the original study shows that this will sustain forever. But this is not what the original research was about. They only tested simulations for up to 30 years.

It is better to call it the 4% Rule of Thumb. Because if you plan to retire very early, you will probably need a lower withdrawal rate. Moreover, your withdrawal rate will depend on your portfolio and asset allocation to stocks and bonds.

Why did I do it again?

If the study is excellent, why did I want to redo it? I have several reasons for that.

First, I wanted to see how this worked with recent stock market returns. The original study was only covering years up to 1995. I wanted to have more recent data. I wanted to ensure the results were holding with more recent stock market behavior. So this simulation will cover returns until the end of 2025!

Secondly, the original study only covered up to thirty years of retirement. I wanted to ensure that the portfolio could sustain withdrawals for extended periods. For people retiring early, I think that 50 years is not unreasonable.

Finally, I have to admit that I like to write code. So it was cool to write code related to this blog. And being a big geek, now I can run many simulations with the data I want. Overall, it was a lot of fun preparing the data for this article.

Ultimately, I want to extend the Trinity Study to the European markets. It will be challenging to obtain the data. But I will try to find it for as many years as possible.

How I redid the Trinity Study

My simulation uses monthly withdrawals. Most people in retirement will withdraw money monthly. It is also possible to withdraw money at the end of the year instead. But I believe that it is not common.

I have calculated all the returns monthly. Doing that makes the results much more accurate than doing it yearly. And the monthly withdrawal is updated with inflation every month as well. Every possible starting month in the available data is tested.

For this simulation, I have not done any rebalancing. For more information, I have compared different rebalancing methodologies for retirement.

Withdrawals are based on the current allocation. For instance, if your base allocation to stocks is 60%, but your current allocation is 80%, 80% of the withdrawal will be taken from stocks. If you are interested, I have explored other techniques in other articles:

Based on this simulation, I collected the same results as the original study: success rates without inflation, success rates with inflation, and terminal values.

Success rates of the Trinity Study

I start the simulation with the entire data from 1871 to 2025.

In this simulation, success is when your portfolio does not run out of money before the end of the simulation. For instance, if we simulate for 20 years and end up with one dollar after 20 years, it is a success. This is a failure if the portfolio runs out of money before that (it could be in the first year or the nineteenth year).

So, the success rate is the percentage of the months that end up with success. The higher the success rate, the better the results are.

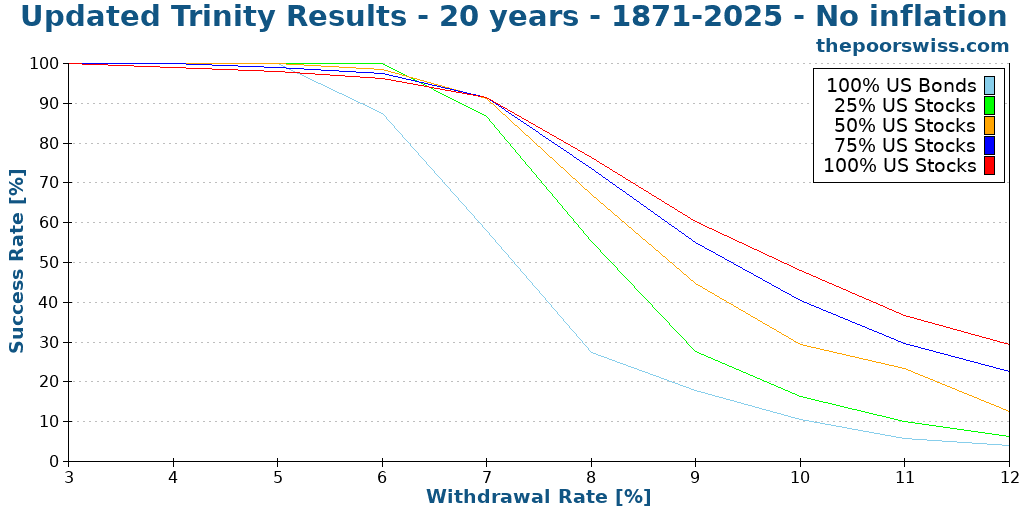

We will see what success rates we have when we ignore inflation. We start with 20 years since I do not think anybody will care about a ten-year-long simulation. I will begin at a 3% withdrawal rate and go up to 12%, increasing by 1% at a time.

We can see what we already expect:

- Increasing the withdrawal rate decreases the chances of success

- Any withdrawal rate higher than 8% does not make sense long-term, even without inflation.

- A small allocation of bonds can help with lower withdrawal rates

- Generally, a 100% stock portfolio will perform better than the other portfolios.

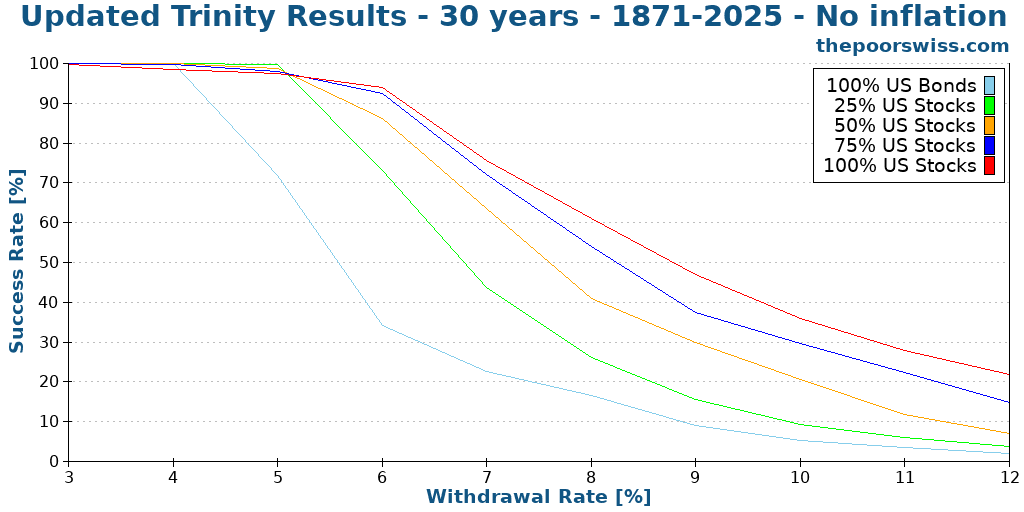

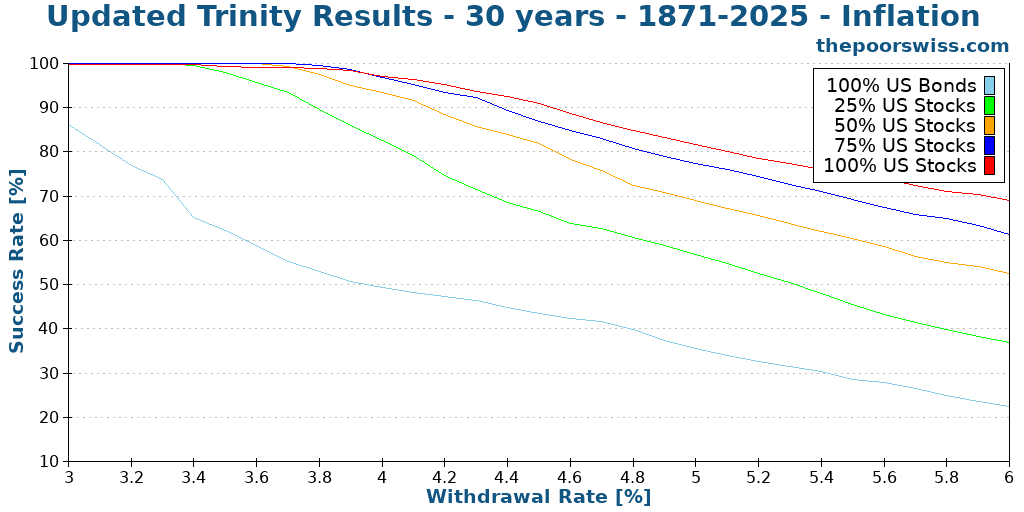

Here is what happens when we push the simulation to 30 years.

We can see that increasing the number of years decreases the likelihood of success. It is logical since you are more likely to run out of money.

With 30 years of retirement without inflation, a 6% withdrawal rate with a significant allocation to stocks still makes a lot of sense!

Taking inflation into account for retirement

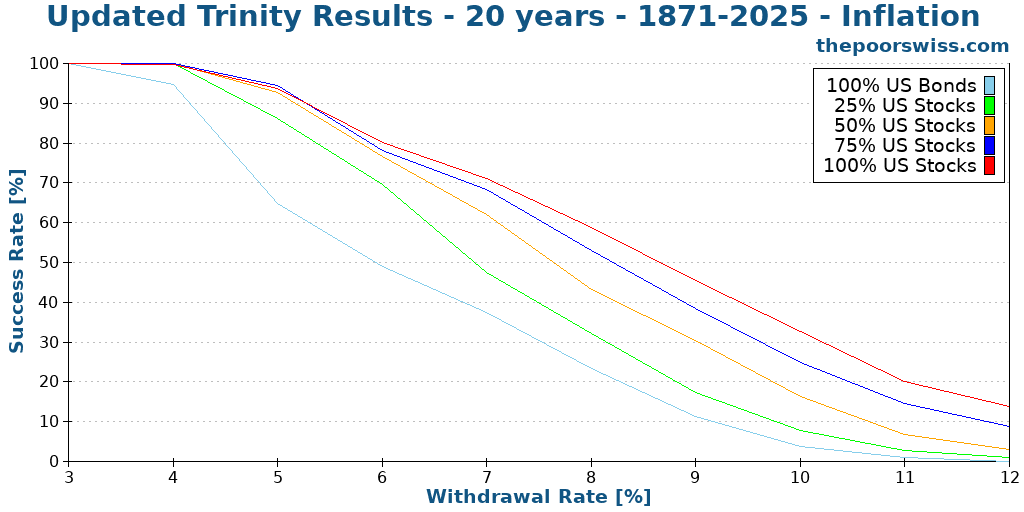

However, it is much better to consider inflation in our simulation! We start again with 20 years to compare the results:

As we can see, inflation causes a significant hit to our chances of success! Before inflation, an 8% withdrawal rate made some sense. Now 6% is the limit. And even 6% has a barely over 75% chance of success!

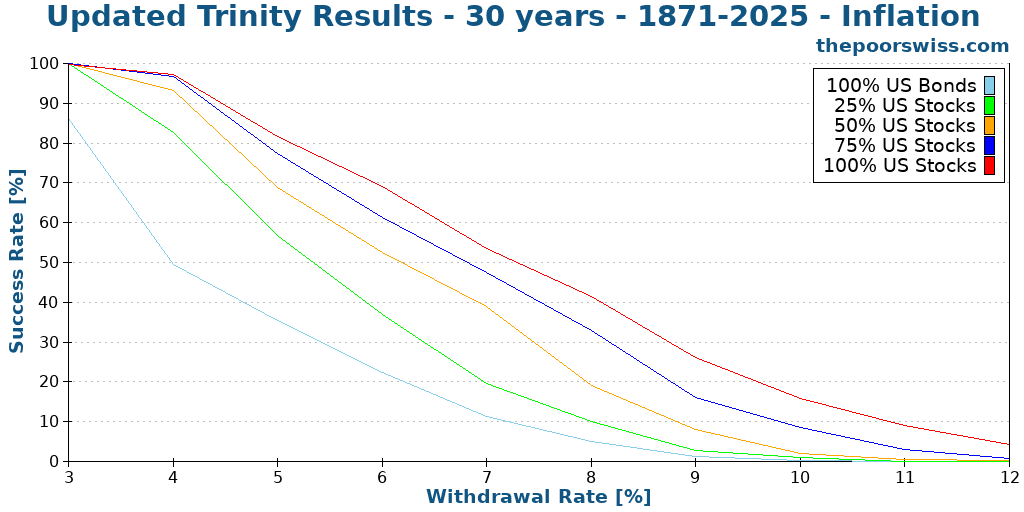

Here is what happens for 30 years of retirement.

We can now see that anything higher than a 6% withdrawal rate is hazardous, with a less than 75% chance to succeed even with 100% stocks.

More withdrawal rates

Since we see that reasonable withdrawal rates are in the range of 3% to 6%, we try more withdrawal rates. I have simulated increments of 0.1% of withdrawal rates.

With a large stock allocation, withdrawal rates between 3% and 4% are very safe. Some people would even dare use withdrawal rates of about 4.5%. But even a portfolio with 100% stocks has only an 85% chance of success after 30 years with 4.5%.

Longer retirement time

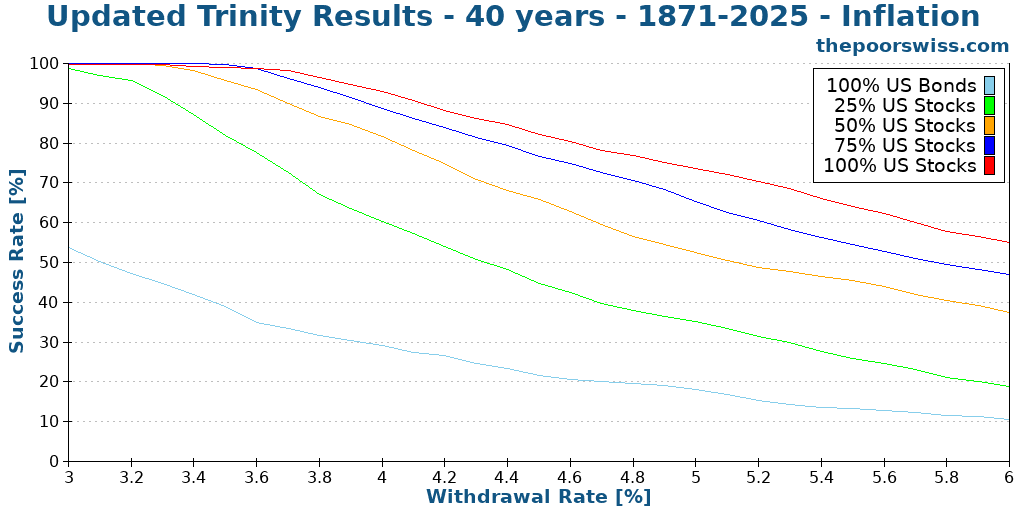

One of the caveats of the original study is that they stopped at 30 years. We run the same simulation again but with 40 years this time.

After 40 years, we are starting to see lower success rates, even for most people’s 4% withdrawal rate. Unless you have 100% of stocks, your success rate will be less than 90%.

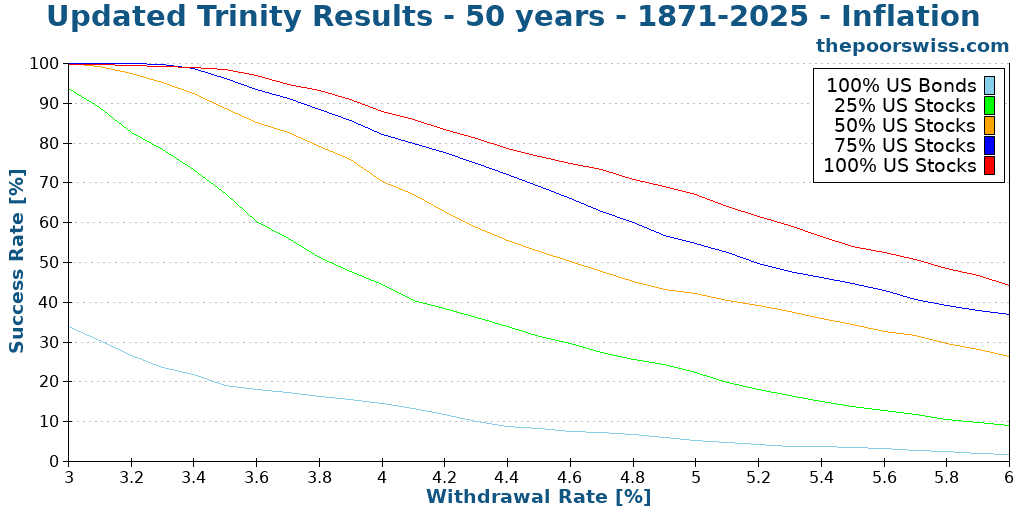

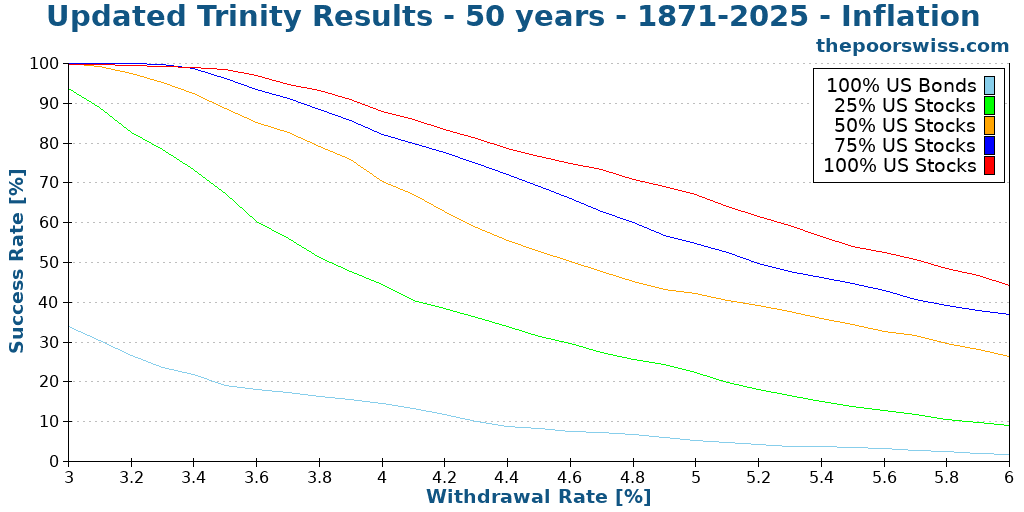

Here is what happens in 50 years.

As expected, we see lower success rates. But it is still not bad at all with reasonable withdrawal rates. A 100% allocation to stocks and a 3.5% withdrawal rate still have more than a 98% success rate. This is significantly more than I expected.

It shows that the study’s original conclusion can still hold for over 30 years. It is excellent news!

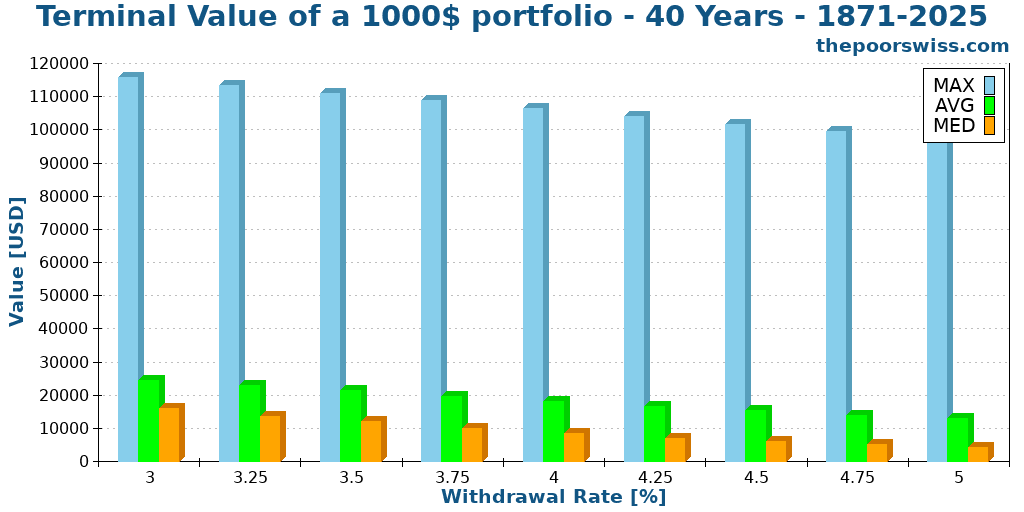

Updated Terminal Values

Another interesting thing from the study was that they also compared the terminal values of the different withdrawal rates and portfolios.

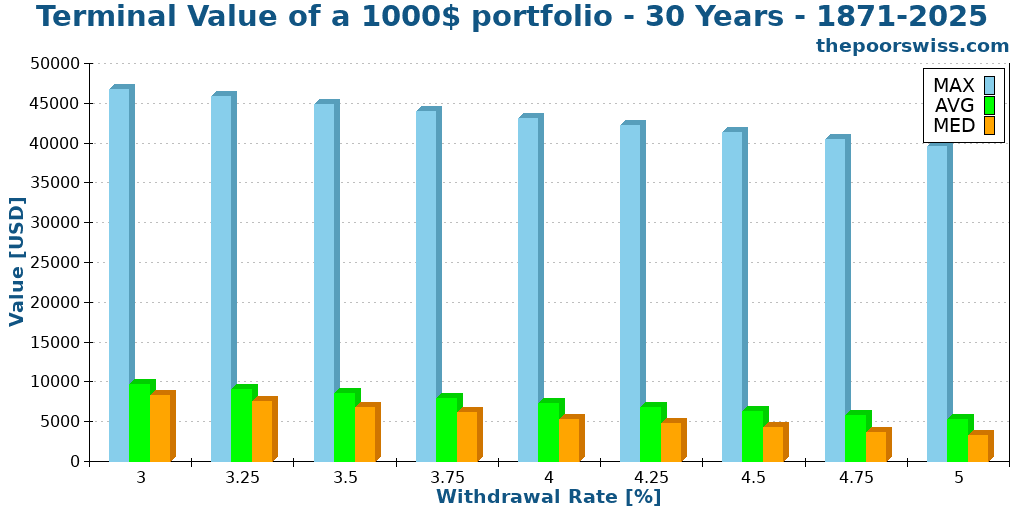

So we will see the terminal values of a 1000 USD portfolio after 30 years. I did the simulation for a portfolio of 100% stocks. For the sake of display, I have reduced the number of withdrawal rates.

I did not show the minimum values. Indeed, they are always zero. If the chance of failure exceeds zero, the minimum value will be zero.

However, the average and median values are quite remarkable. We will focus on the median since it is generally more representative than the average.

For a withdrawal rate of 3.5%, my current target, the median terminal value after 30 years, is about 6700 dollars! Not only did your portfolio sustain your lifestyle, but it also increased sixfold! Let me repeat this. After 30 years of doing nothing but withdrawing money, you have six times more money than when you started!

The maximum values do not mean a lot. But it is crazy to see that after 30 years, you could have about 30 times more money than when you started! And this is with a 3.5% withdrawal rate!

Here is what happens when we extend it to 40 years.

We can see that the results are comparable. However, all the values are significantly higher. The numbers are all about twice higher. On average, your retirement money will double during the ten additional years. So, even though you are not contributing more money and living from it, your portfolio will double in 10 years. How cool does that sound?

The success rate is not everything

There is something important with these measurements: the success rate does not tell the entire story. For instance, for you, which of these two scenarios is better?

- 98% to last 50 years, but a chance of running out after ten years

- 96% to last 50 years, but a chance of running out after 48 years

For me, the second scenario is better. You do not want to have a chance of failing after only ten years if you are planning for 50 years. But if it fails after 48 years, you have many years to make some adaptations.

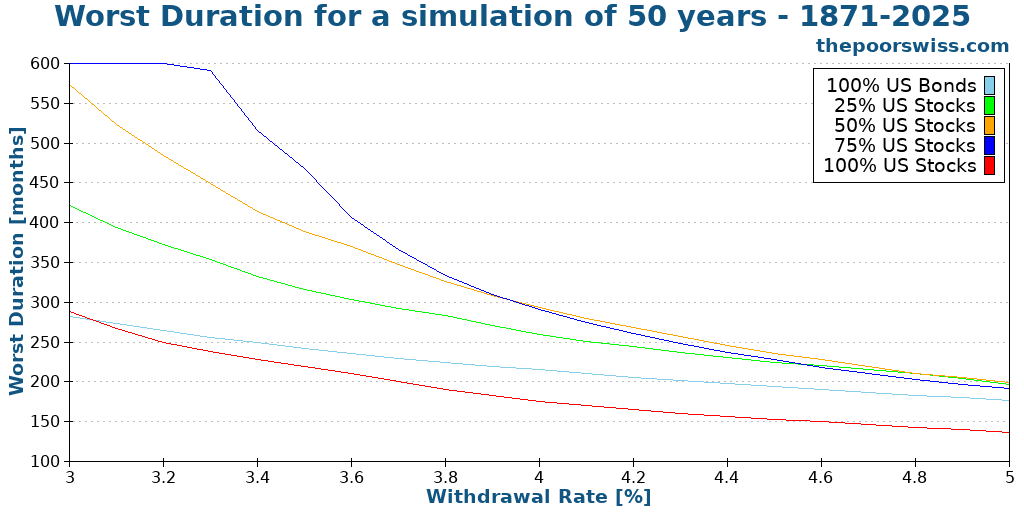

So, another essential metric is the worst duration of a scenario. This means after how many months, the first failure can happen.

For reference, here are the success rates of each portfolio for 50 years and different withdrawal rates:

And now, here are the worst durations for each of these portfolios:

If we only look at the first graph, the conclusion is that higher allocation to stocks is always better. But if we look at the second graph, 100% stocks is the worst one!

So what does this mean: you need a balance in your portfolio. Bonds will significantly reduce the chances of your portfolio failing too early. This does not mean that you should optimize for the highest worst duration either. Because if your highest duration is 40 years, but you have only a 50% chance of reaching 50 years, this is gambling, not planning.

So balance is essential. While stocks will increase your success, stocks are more subject to sequences of return risks.

How to implement the Trinity Study?

Now that we have noted that the results of the Trinity Study are encouraging and would let people retire early, how should we implement it?

Theoretically, the Trinity Study is based on a simple concept: you can retire based on a large principal by withdrawing with a fixed withdrawal rate.

However, in practice, this means you need to accumulate money, more than most people accumulate during their lifetime. And you need to accumulate this earlier than retirement age.

To accumulate this money is not easy, but it is also not complicated. First, you have to save money (as much as possible). For this, you will have to focus on your expenses and earnings.

Then, you will have to invest that money until you can retire. Once you have accumulated the proper amount through capital gains and savings, you will be financially free.

If you are interested, I have many articles on my blog about financial independence.

How did I do it?

You can find my code and my data on Github. Everything is available to share as much as possible!

I wrote the entire program in C++. I used this programming language because it is my favorite! And it is blazing fast! I have not especially optimized my code, and it takes less than a second to generate thousands of simulations.

If you are not a coder, I also have an online FIRE calculator to do most of the calculations presented here.

My U.S. and international data is based on the data made available by Big ERN in its Safe Withdrawal Rate series. It is a good dataset that has been tested several times already. Big ERN made all this available for free. I am thankful for his work! I have completed its data with the missing years using the same methodology.

If you want to use the graphs in this article, please cite this article as the source of the image!

Future of the series

It was fascinating to reproduce these results. And it was very insightful as well. I have learned many things from the results. It is great to see the confirmation that the original conclusions hold for more than 50 years.

And it also shows that my withdrawal rate (3.5%) is a safe bet. I may switch to 3.75% in the future. I will have to run more simulations. It is important to choose a proper safe withdrawal rate.

Talking of simulations, I have run a few more simulations with the same idea:

- Trinity Study Results with Swiss Stocks

- Withdrawal rates and low-yield bonds

- When should you rebalance your portfolio?

- Does the Trinity Study work in recent years?

- How often should you withdraw money?

- Can you retire early with Swiss stocks and bonds?

- The Trinity results with world stocks

- Equity glidepaths in retirement

Since I plan to make more articles like these with more simulations, I would like to get your perspective on this article! Please let me know what you think in the comments below! What should I improve?

What do you think of these results? Would you like me to run more simulations like this? Do you have ideas on what kind of simulations I should run next?

Conclusions

With all these results, we can have several important conclusions.

First, the paper’s original conclusions still hold even with much more data being considered. And it still stands accurate up to 2026! It is excellent since it shows that the 4% rule of thumb still works!

If you increase the simulation time to more than 30 years, a 4% withdrawal rate is no longer safe. With 50 years of retirement, you have a 90% chance of success with a 4% withdrawal rate at most. A withdrawal rate of around 3.5% would be safer for most people.

If you want real chances of success, you will need more than 50% of your portfolio allocated to stocks. The stocks allow us to fight inflation and cover the withdrawal rate year after year.

If you choose a reasonable withdrawal rate, you will likely have much more money than when you started! For instance, a 3.5% withdrawal rate over 30 years with 100% stocks would leave you about six times more money than when you started!

For information about the original study, read my detailed article about the Trinity Study. If you are extremely conservative, you will also be interested in learning how to choose a failsafe withdrawal rate.

If you want to start investing to become financially independent, you will be interested in my guide on how to get started in the stock market.

More reading

6 keys to avoid the pitfalls of financial independence

The dark side of FIRE. We discuss the potential pitfalls of pursuing Financial Independence, from burnout to social isolation, and how to avoid them.

The 6 Kinds of FIRE: Which One Are You?

Lean, Fat, or Barista FIRE? Discover the different types of Financial Independence and find out which FIRE style fits your life goals best.

The best and worst times to retire early

Timing is everything. We look at historical data to find the best and worst times to retire early and how market valuations predict success.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Thank you for your work, it is simply wonderful. I am from Israel, I am not a programmer and do not know how to run what you did on the Israeli market, is there a possibility that you are raising it in stocks? Although it makes sense that there are not many users who would benefit from it, the Israeli stock market is vibrant and rising well, and it may be worth it for other users to spread some of their holdings there. Thank you very much

Hi Moses

I am glad you enjoy my work.

The code is ready for any stock market. The problem is finding the data. I need historical monthly data for the stock market, and then any stock market can be included. If you know where to find this data, I could think of including it.

I would plan to only live on dividends. If I get between 3 and 4% that would be ideal. This way the assets stay untouched and go to the children. I guess this way you are safe. The only risk is that 3%+ would drop. What do you think?

Hi Zkaporius

You can live off dividends, but it means you need to accumulate more money. Getting 3% to 4% dividends is already difficult to get consistently while maintaining diversification.

Also, in Switzerland, this means you will pay more taxes than if you relied on a combination of both dividends and capital gains.

But yes, if you want to leave a larger legacy for children, it makes sense to use dividends or to at least reduce the withdrawal rate to keep the assets consistent.

I would have enough money, I guess. Problem is my investment until know was bad so I kept my money out of the market. I was thinking about getting those ETFs that deliver that percentage. Like e.g. VYMI. Around 3.5%.

In this case it would be quite simple. I wouldn’t touch the asset and live only from the dividend. Of course, the market might run up and down and the taxman would have his cut. What am I missing here?

Base your withdrawals on expected returns and deduct a safety margin to cover sequence of returns risk. Then you end up with the safe withdrawal rate that might be around 4%, or 3.x% if you want to play it safer.

It doesn’t make sense to invest in high dividend stocks only to life off dividends.

Consider 2 identical companies, one with 4% dividends, the other with 0% dividends but buying back stocks. With both companies you’d yield 4%, but with the first company you pay a lot of income taxes…

Amazing analysis.

What do you think about the accumulation phase of money?

Should you invest only in stocks and start buying bonds two or three years before retirement?

Thank you very much for your research!

Hi

Yes, I think it makes sense to start 100% in stocks for accumulating and then switch to some bonds once we are getting closer to retirement. This would be an inverted glidepath.

Then, I also think it makes sense to do a real glidepath to switch back to 100% after a few years of retirement to protect the early years with bonds and the later years with stocks.

What is the optimal portfolio mix that one should aim for while planning for the longest retirement (say 50 years) ?

It will depend on your risk capacity and on your withdrawal rate.

For me, it would be 100% stocks, but for some people, it would be 60% stocks only.

Thanks for the fantastic analysis. Would you include a simple rebalancing strategy into the mix at some point? I think it would make a big difference to some of the graphs.

Intuitively, the 75% stocks with yearly rebalancing might miss the max returns, but also extend the worst duration siginificantly.

Thanks, Duncan.

What do you mean by a simple rebalancing strategy?

I have considered multiple ones in another article: Should you rebalance your portfolio in retirement?

I saw the other article afterwards. It includes rebalancing but I read it as the expected case and not the worst case?

I think most people should indeed rebalance. Yearly rebalancing is enough, I think, because monthly creates too many transactions for me.

GREAT DATA!

I wonder how different the results will be if you assumed differential withdrawals during different markets – i.e. bonds in down markets and stocks (up to the point of replenishing the bond safety blanket) in up markets.

In a way similar to this simulation of the Buffet allocation of 90/10 – https://blog.iese.edu/jestrada/files/2016/03/Buffett-AA.pdf

In my mind, this should help with sequence of return risks by shielding stocks from withdrawals in down markets. Having the ability to withdraw from bonds only during a 3-4 year down market may help significantly extend the life of the portofolio and the mental sanity of the retiree (avoiding knee jerk reactions in down markets).

Somewhat different than straight up rebalancing which is agnostic of market status – and also different from glidepaths. Thoughts?

Thanks, Andre!

This should likely help indeed.

I think the results are likely similar to that of an equity glidepath: Equity Glidepaths in Retirement

The biggest risk is within the first decade. I do not think it’s necessary to replenish bonds because you don’t want to keep them long-term.

We can imagine many such strategies, but the problem is implementation. How do you define when to sell bonds, stocks and buy bonds back? You need a strong heuristic, and it’s difficult to know whether that heuristic will hold in the future.

Great analysis! Do you have an article about how currency exchange affects the withdrawal rate? At least since the year 2000, the US Dollar has lost quite some value vs Swiss franc. I guess that means a lower safe withdrawal rate.

Hi Edd

Yes, I did some simulations here: The 4% Rule for Swiss Stocks – Can you retire early?

Unfortunately, the historical data is not great because of how the USD was pegged to gold in the past.

But we can safely assume that a Swiss investor would need a lower withdrawal rate indeed.

Another vote here for using half TIPS and half (intermediate term) nominals for the bond holdings. A lot of investors split the difference.

Hi Ladder Up,

Thanks for sharing. I think TIPS makes a lot of sense for US investors indeed!