Should you rebalance your portfolio in retirement?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Many people want to know whether they should rebalance their portfolios. This is an excellent question, and it becomes essential once in retirement.

Rebalancing is selling the shares that have overperformed and then buying the stocks that underperformed. The idea is to keep your portfolio allocation at the same level.

People disagree on whether you should rebalance in retirement or not. People do not even agree on that during the accumulation phase. So we will cover this subject as well.

And since I now have a lot of data about the stock market, I figured it would be great to use. So, I simulate whether it has historically been better to rebalance.

The data in this article is based on more than 3.2 million simulations of withdrawal rates! So, without further ado, delve into rebalancing!

Rebalance a portfolio

When you choose your investment portfolio, you decide on a particular allocation to each of the instruments in your portfolio. For instance, you could have 40% of bonds and 60% of stocks. It is a popular portfolio in the United States.

But, during a bull market, the stocks will probably outperform the bonds. So, after one year, your effective allocation may become 65% of stocks instead of 60%.

Rebalance your portfolio is setting your stock allocation to 60% again. For this, you will sell stocks to buy bonds. Once it is done, you are back with a 60%/40% portfolio.

The same can happen during a bear market, where you can sell bonds to buy more stocks. And if you have different asset classes, for instance, small and large companies, you may also have to rebalance both.

When to rebalance

There are two main ways of seeing rebalancing:

- Perioding rebalancing: You rebalance each given period.

- Threshold rebalancing: You rebalance when your portfolio is too imbalanced.

Most people rebalance their portfolios either monthly or yearly. Monthly rebalancing makes little sense because the stock market is very volatile. Quarterly and yearly are the two rebalancing schedule that makes the most sense. We have to keep in mind that rebalancing is not free. You will need to pay for both operations.

But in practice, you could rebalance at any time. Some funds are rebalancing their assets daily.

On the other hand, you could also decide to rebalance once it is too much imbalanced for you. So you need to decide when you start to rebalance. For instance, you could choose not to rebalance a portfolio at 61%/39%. It is good to set a threshold, after which you will start rebalancing.

And, of course, you can also opt for a hybrid of these two techniques. For example, some people will rebalance every quarter, but only if it is more than 2% out of balance.

Advantages of rebalancing

The apparent advantage of rebalancing is that your asset allocation stays the same over time. If you base your asset allocation on your risk tolerance, then the risks of your portfolio remain aligned with your risk tolerance. This stable allocation is essential for some people.

If you have several kinds of stocks in your portfolio, rebalancing can also help the diversity in your portfolio. For instance, you could allocate 40% of your portfolio to Swiss stocks and 60% to U.S. stocks. If the U.S. Stocks do very well, you may end up with 80% U.S. stocks instead of 60%. You just lost diversification in your portfolio.

Some people also argue that rebalancing can improve the performance of your portfolio. You are automatically selling high to buy low. On paper, this makes a lot of sense. We will see later what this means in practice.

Disadvantages of rebalancing

One of the problems of rebalancing is that it is more costly than doing nothing. You will pay a fee to sell your shares. And you will pay a fee to repurchase the other shares. If you use a good broker, it is not a lot, of course. But if you often rebalance, for instance, once a month, this could significantly increase the yearly costs of your portfolio.

Another simple disadvantage is that it is more complicated. Doing nothing is simpler.

By rebalancing your portfolio, you are selling the shares that are doing well and buying shares that are not doing well. Unfortunately, you may miss out on the good shares doing even better.

Rebalance during the accumulation phase?

Before considering rebalancing during retirement, we should discuss rebalancing during the accumulation phase. This is the phase where you often invest in the stock market, and you do not withdraw money from it.

There are two ways to ensure a balanced portfolio during the accumulation phase:

- Rebalancing by selling and buying shares to go back to a better balance.

- Invest more to balance your portfolio.

I do not think it is necessary to rebalance a portfolio during the accumulation phase. It should be enough to buy the shares that are too low in allocation. I am buying shares every month. And I am always choosing the shares that need the most buying.

It is cheaper to do it without actually rebalancing. But at some point, if there is too much imbalance, an actual rebalancing may be necessary. That is if you want to have your portfolio well balanced.

It makes sense to keep a balanced portfolio during the accumulation phase. But, I do not think it is as crucial as during retirement. And I think that using your regular investments will be enough for rebalancing.

Rebalance in retirement?

Now we get to the main point: Should you rebalance in retirement?

First, during retirement, you probably cannot balance by using investments. Even if you have some passive income, you will probably save much less than during the accumulation phase. Therefore, either you rebalance by buying and selling, or you do not rebalance.

You also have the choice of whether you want periodic or threshold rebalancing. These are the same choices as during the accumulation phase.

The pros and cons are the same as we saw before. Now, we will see what would have happened with and without rebalancing in the past.

Periodic rebalancing

We start our first simulation to see how periodic rebalancing is doing.

We will use the same data I used for the Updated Trinity Results. Our simulation will include the period from 1871 to 2024 (included). I will plot the success rate with different withdrawal rates.

I compare three different setups:

- No rebalancing

- Monthly rebalancing with a 0.005% fee per rebalancing

- Yearly rebalancing with a 0.01% fee per rebalancing

Next, we see whether we should rebalance for different portfolios.

We will not do the test for a 100% stock portfolio. Indeed, there is no rebalancing necessary. It is another advantage of a full stock portfolio.

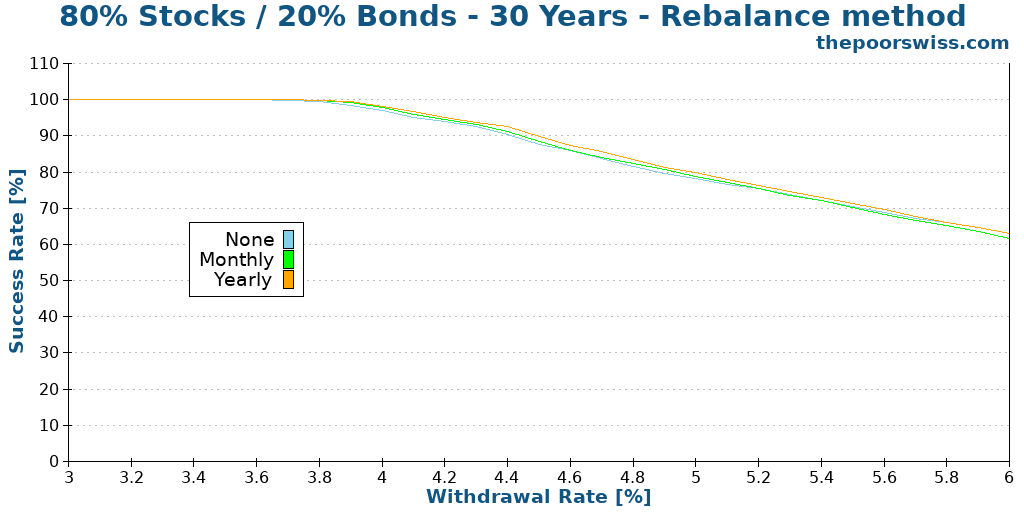

80% Stocks / 20% Bonds

Here are the historical results for a portfolio with 80% Stocks and 20% Bonds for 30 years:

As you can see, there is very little difference between the different rebalancing options. We can still observe two things.

First, yearly rebalancing is always better than monthly rebalancing! For low withdrawal rates, annual rebalancing is the best option. Then, no rebalance becomes better for higher withdrawal rates.

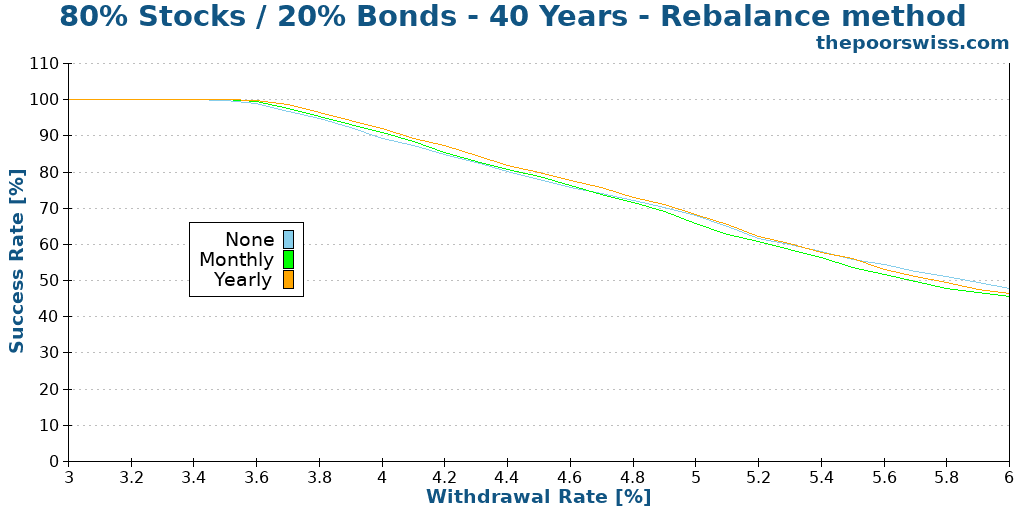

Here is what happens with a 40 years horizon:

With a longer time, no rebalancing starts to outperform yearly rebalancing. However, we are in a zone where the success rate is low.

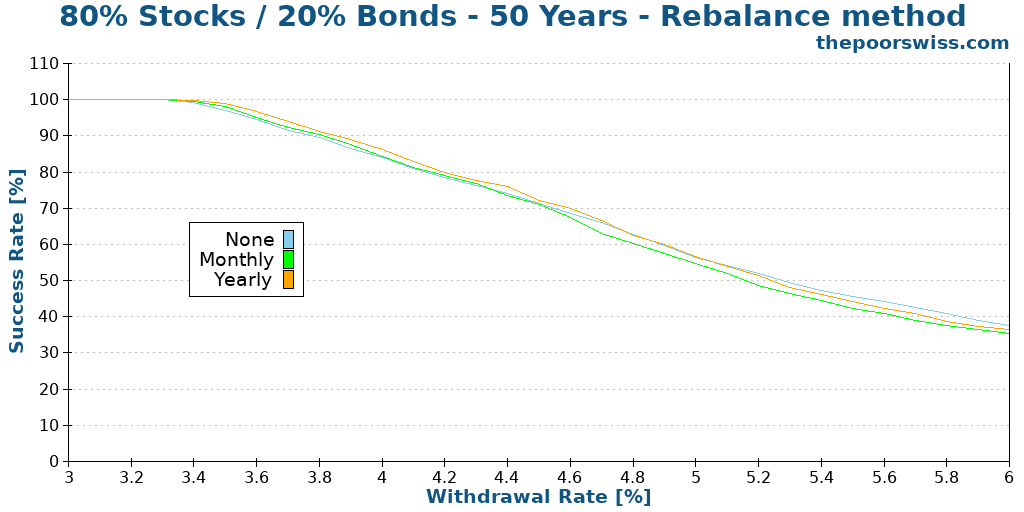

With 50 years, we get the following results:

This time, No rebalancing starts to outperform yearly rebalancing from about a 4.7% withdrawal rate.

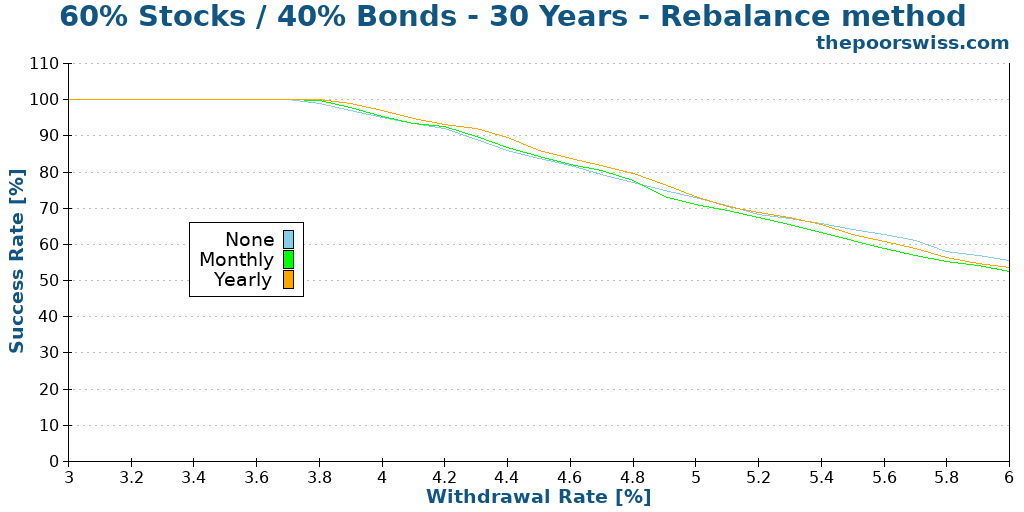

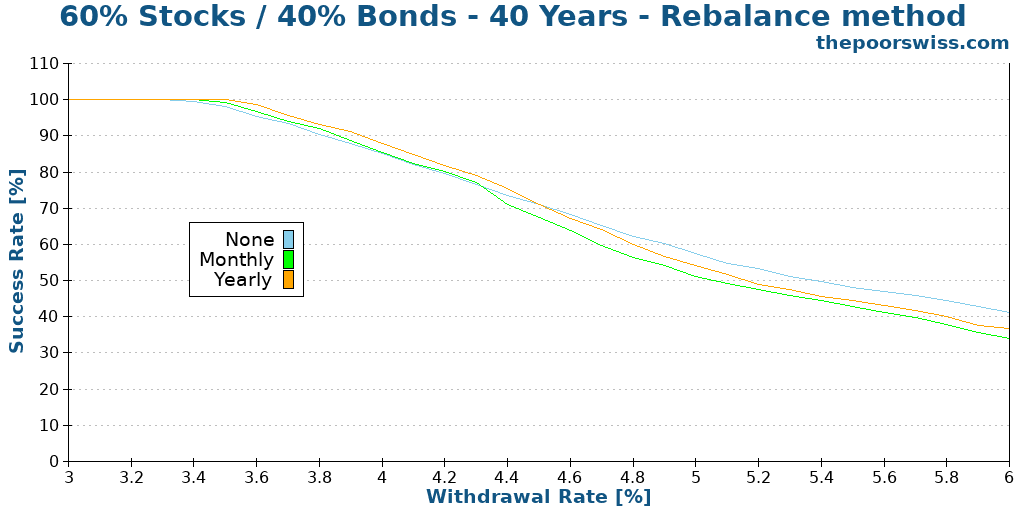

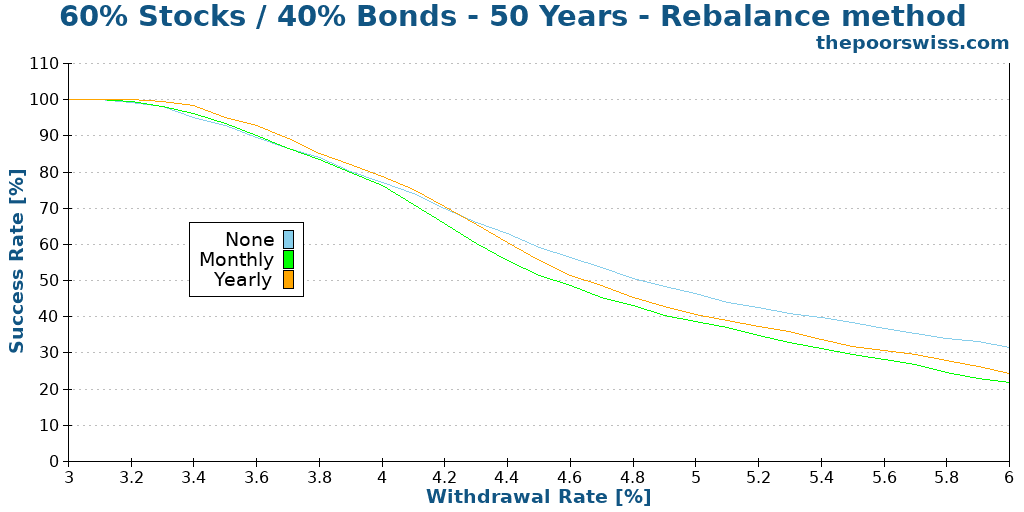

60% Stocks / 40% Bonds

We can also try the popular portfolio with 60 percent in stocks and 40 percent in bonds. It is a portfolio that many people use.

Once again, we start with 30 years of retirement:

There is more margin for imbalance in this portfolio. So the effects of rebalancing are higher than in the first case. We can see that below 5% withdrawal rate, it is better to rebalance yearly. However, after this limit, you should probably not do any rebalancing.

With 40 years, the effects of rebalancing are more important. After a 4.4% withdrawal rate, you should avoid rebalancing. And below that, the effects are also more important.

Finally, with a 50 years retirement horizon, the effects of no rebalancing are significant. Below a 4% withdrawal rate, not rebalancing could cost you a few percent chance of success.

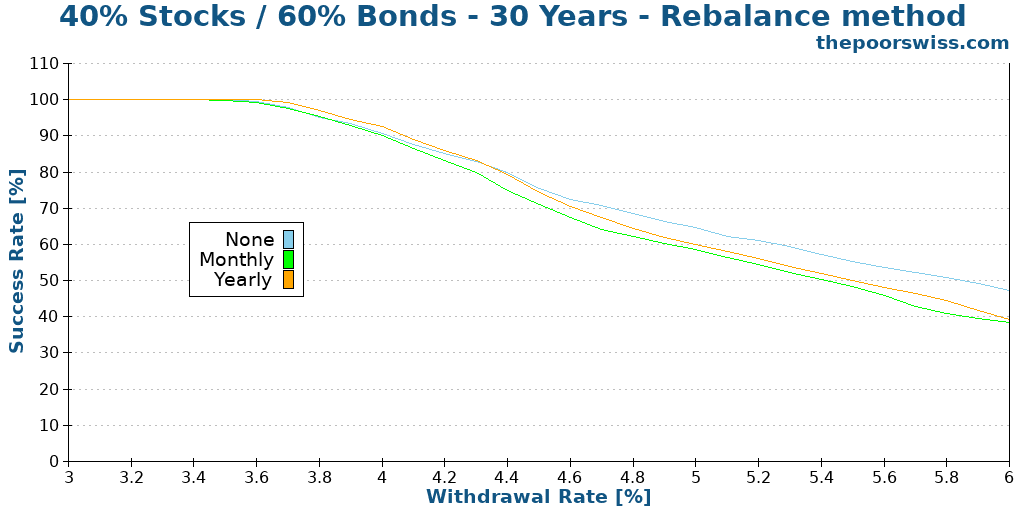

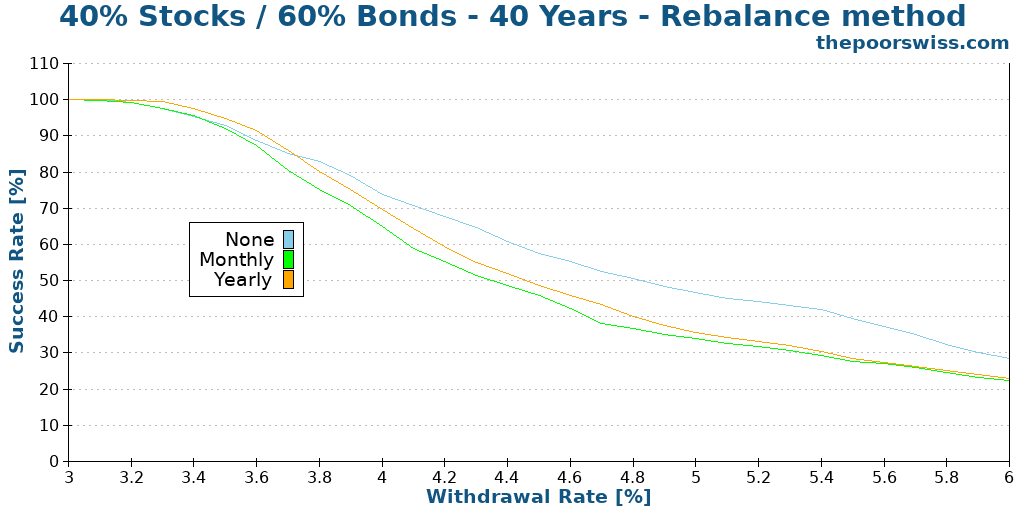

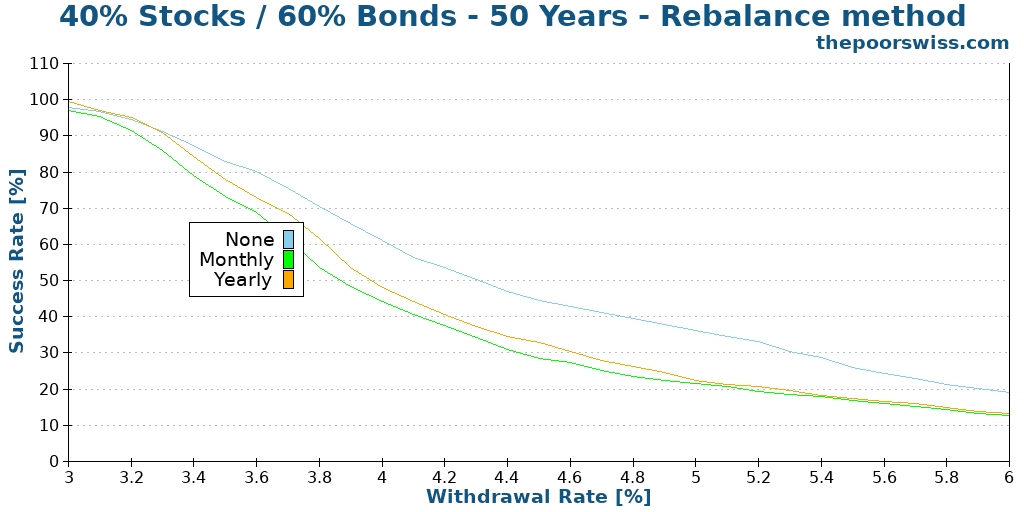

40% Stocks / 60% Bonds

The last portfolio we will test is a portfolio with 40 percent of stocks and 60 percent of bonds. It is also a typical conservative retirement portfolio for many people.

We can observe the same thing as before, with the interest of rebalancing decreasing as you increase the withdrawal rate.

Once we go to 40 years of retirement, it becomes better not to rebalance quickly.

Finally, after 50 years, you should not rebalance. However, this is not a great portfolio to plan for 50 years of retirement. Your chances are going lower very quickly.

Periodic rebalancing – Conclusion

We can make a small intermediary conclusion already for periodic rebalancing.

One thing is fascinating: yearly rebalancing was always at least as good as monthly rebalancing! So, historically, it was better to rebalance only once a year instead of once a month. It will not make a huge difference. But it can give one or two more percent chances of success. And this is always good to take. Moreover, it is also simpler!

Also, the smaller allocation to stocks you have, the more difference rebalancing can make. And the longer the retirement, the higher the difference as well.

The last conclusion we can make is that if you plan on a high withdrawal rate, you are probably better off not rebalancing at all. It makes sense. Since the stock returns are historically higher, it is better to let them run their course.

Threshold Rebalancing

Now, we can also compare these results with threshold rebalancing. Generally, people using this technique will rebalance each month if the imbalance exceeds a certain threshold.

Ideally, you should rebalance as soon as the imbalance appears. But this means you need to monitor your portfolio regularly. Monitoring your portfolio is highly inconvenient. And I hope nobody does that manually. It is what some computers do with automated trading. But monthly is more than enough for threshold rebalancing.

For instance, if your standard allocation to stocks is 60%, but your current allocation is 63%, you have a 3% imbalance. If your threshold is 2%, you will rebalance. If your threshold is 5%, you will wait.

I test several different thresholds:

- 1% (this is almost the same as monthly rebalancing)

- 2%

- 5%

- 10%

- 25%

- 50% (this is almost the same as never rebalancing)

Once again, we will measure the chance of success for different portfolios with these different thresholds.

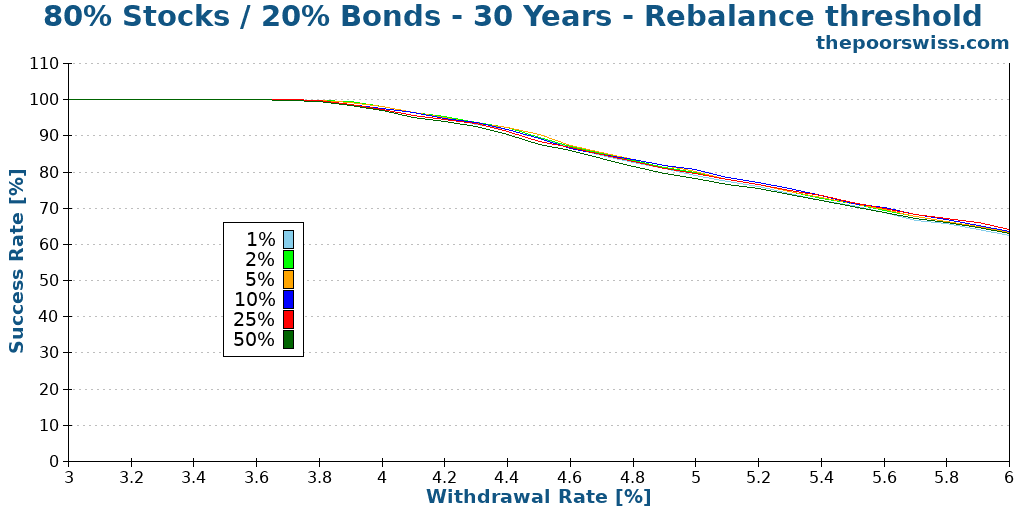

80% Stocks / 20% Bonds

We start with our portfolio, with 80% allocated to stocks. Here is what it looks like with 30 years of retirement:

As expected, there is not much difference in this case. There is not much opportunity for rebalancing. We can still see interesting behavior. The higher the withdrawal rate, the higher the threshold you can use.

Overall, in this case, the best threshold is about 10% if you use more than a 4% withdrawal rate.

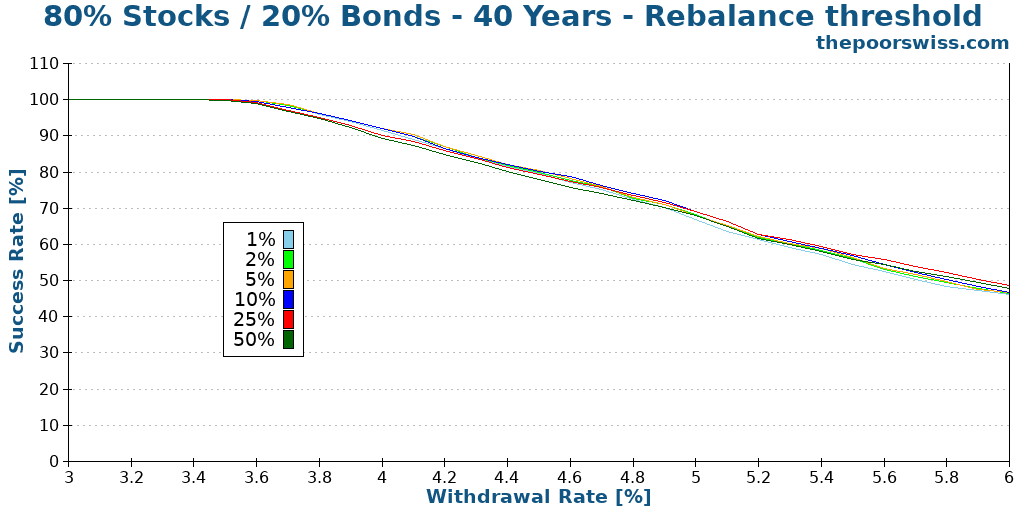

Here are the results for 40 years:

There is slightly more impact on rebalancing on your chances of success. It is interesting to note that neither 1% nor 50% is the best choice here. It means that monthly rebalancing (same as 1%) is easily outperformed by other thresholding. Below a 5% withdrawal rate, 10% is the best threshold. After 5%, 25% becomes the best threshold.

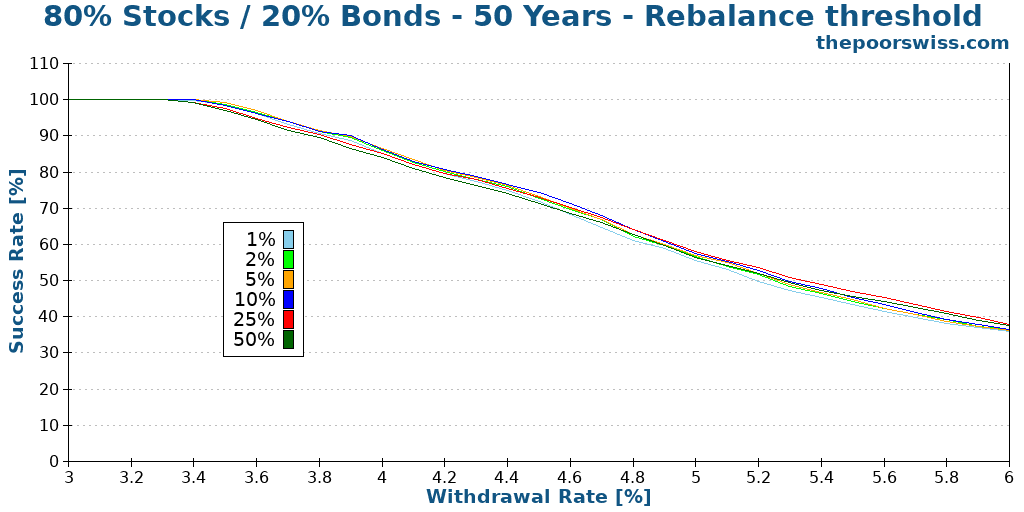

Again, we can check if this holds for 50 years:

Once again, as we increase the retirement time, there are more differences between the strategies. We have the same result: below 5% withdrawal rate, a threshold of 10% is best, and a 25% threshold becomes better after that.

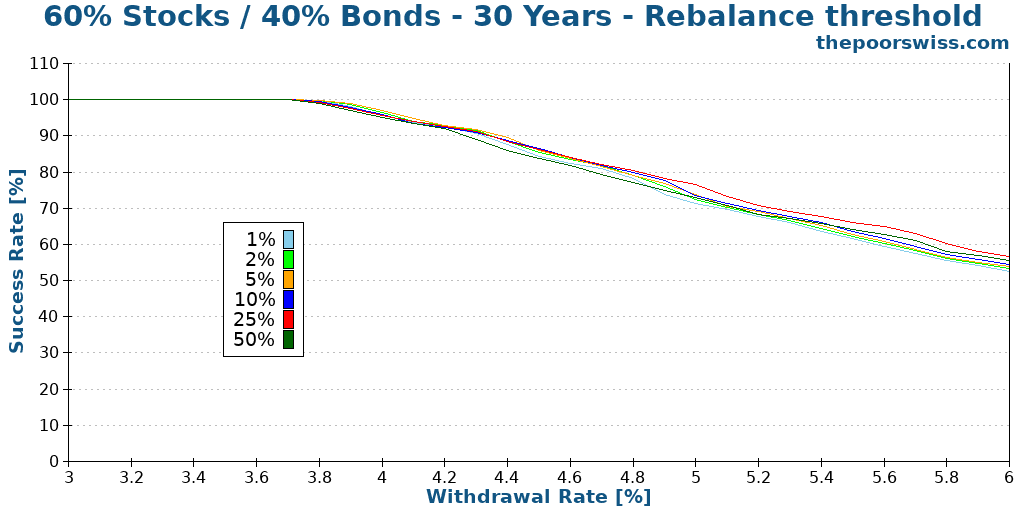

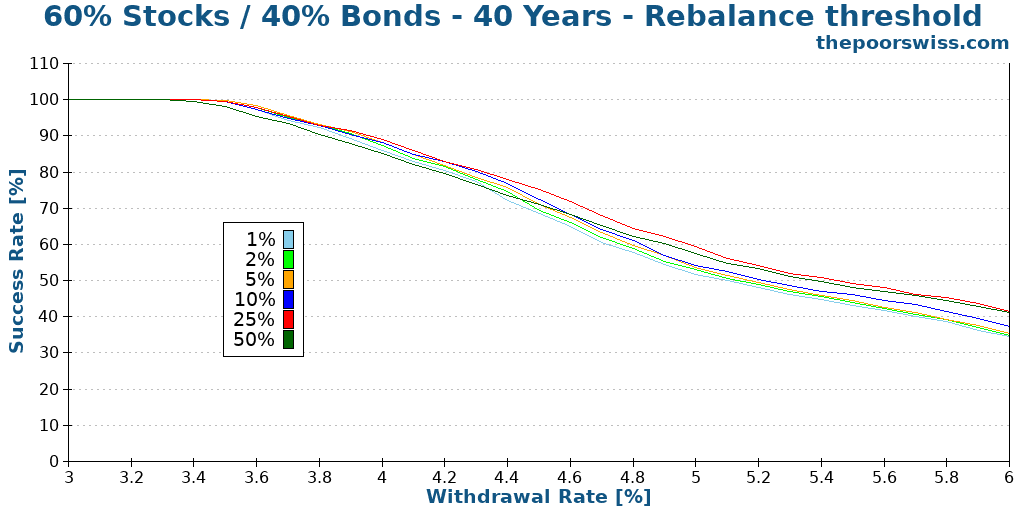

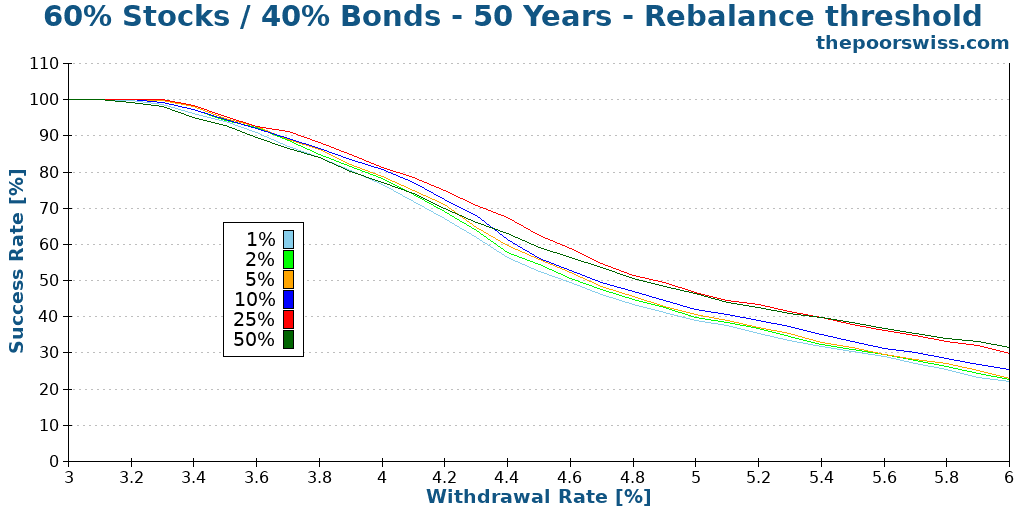

60% Stocks / 40% Bonds

We continue with the popular portfolio, with 60% allocated to stocks. We saw before that this portfolio had more opportunities for rebalancing. So, we will see what threshold rebalancing does for it.

First, with 30 years of retirement:

We can observe more differences between the different thresholds of rebalancing. Once again, the worst rebalancing thresholds are 1% and 50%. 10% and 25% are once again excellent.

These results are interesting. 25% is almost always the best threshold here. Only below 3.5% is it better to have a smaller threshold. And we can also see that the differences between the thresholds are getting more significant.

Finally, with 50 years in front of you:

In this scenario, you should always opt for a 25% rebalance threshold. Even for low withdrawal rates, this will be the best option.

It is very interesting because I never saw this discussed before for this portfolio. And many people use this portfolio. It can make a difference in several percent chances of success compared to yearly or monthly rebalancing.

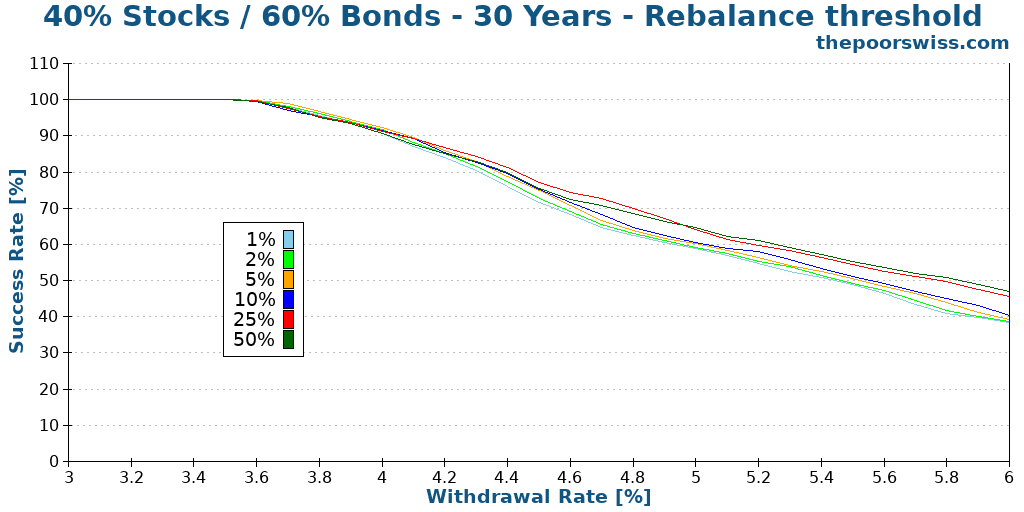

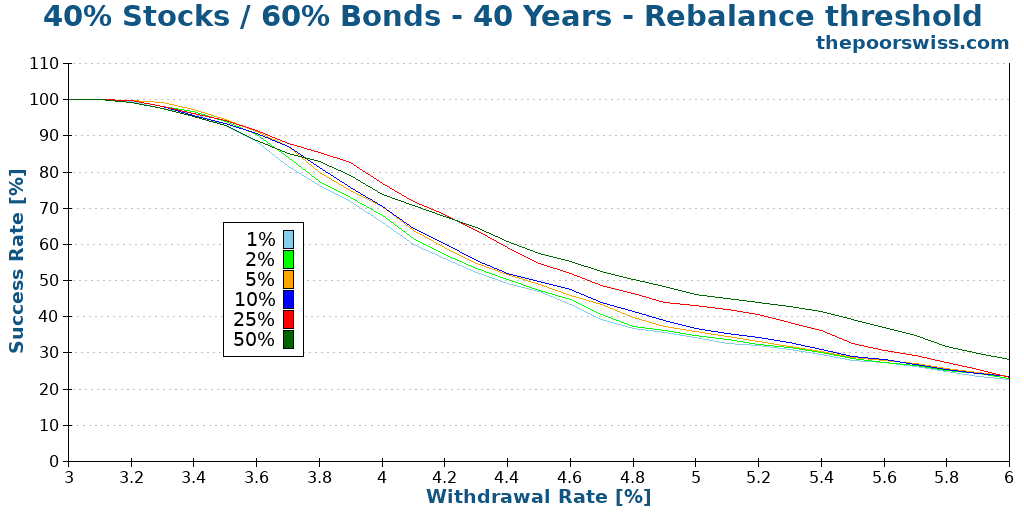

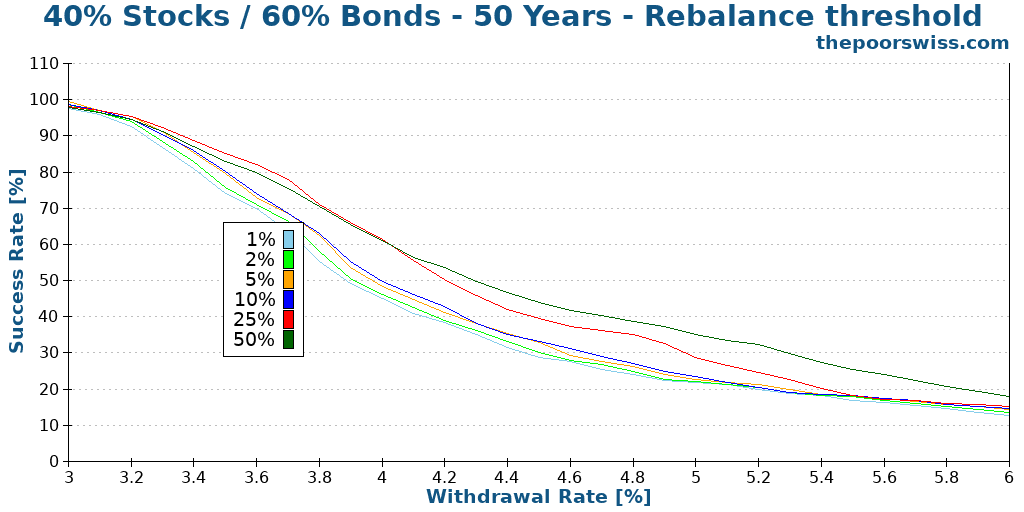

40% Stocks / 60% Bonds

Finally, we try again with our more conservative portfolio.

This case is quite interesting. Below a 4% withdrawal rate, you are best off with a 5% threshold. From 4% to 5%, you should use 25%, and after 5%, you should not rebalance at all (50%).

Does the same stands true for 40 years?

The difference between the thresholds is even more impressive. But the chances of success are also getting quite slim. Until a 4.3% withdrawal rate, 25% is a good option, but you should use 50% or not rebalance after this.

And finally, we see what happens with 50 years of simulation:

We can observe almost the same thing. Until a 4.1% withdrawal rate, you can use a 25% rebalancing threshold. After this, you should forego rebalancing. But in this scenario, even with a 4% withdrawal rate, you will likely run out of money before 50 years.

Threshold Rebalancing – Conclusion

There are several interesting conclusions we can get from these simulations. I was not expecting so much difference between the different thresholds.

First, rebalancing monthly with only a 1% threshold is generally the worst strategy. You should use a higher threshold. 5% and 10% work well on average for low withdrawal rates. Once you start considering longer retirement, 25% is becoming very interesting.

Generally, the higher your withdrawal rate, the higher the threshold you should use to rebalance your portfolio. This correlation makes sense since you want high returns to compensate for large withdrawals. So, you want your stocks to grow more.

Finally, another thing that makes sense: a portfolio with a smaller allocation to stocks will have more impact from rebalancing. This increased impact is because the stocks will have more opportunities to get off balance.

Conclusion

There are several important conclusions we can draw from these results. And it is even more exciting because there are few simulations like that.

On average, yearly rebalancing is better than monthly rebalancing. It is significant since a lot of people are planning to rebalance monthly. Historically, you have a slightly better chance of success by rebalancing once a year.

Also, the longer your retirement, the more critical it becomes to choose the correct rebalancing method. For example, if you plan for 50 years of retirement with the 60/40 portfolio, you should probably only rebalance when your portfolio is 25% off balance.

With a larger withdrawal rate, the best action is to rebalance once your portfolio is imbalanced by 25%. Even not rebalancing is better than monthly and yearly rebalancing.

If you have a very long retirement plan and use a conservative portfolio, you will be better off not rebalancing or rebalancing only when a large imbalance is present. It is logical since having a very conservative portfolio will reduce your returns. So letting the stocks go out of balance will increase your profits. As such, this will increase your chances of success.

Overall, it was very interesting to compare these rebalance strategies. I would not have expected such differences between them. I hope you will find these results are interesting as I did!

In the future, I also want to try to see if these conclusions hold between assets that are less different. For instance, in my portfolio, I have about 20% of Swiss stocks. Should I rebalance my stocks in retirement? I will do the simulation once I have more data.

Another thing I want to try is if we can use the withdrawals to rebalance the portfolio. This would be the same thing we do during the accumulation phase but with negative numbers. Instead of investing more in the underperforming asset, we sell more of the overperforming asset.

If you have not read it already, I encourage you to learn about the Updated Results of the Trinity Study for 2019. And you can compare them with the original Trinity Study results.

If you are interested in the simulation code, you can read my article about the FIRE Calculator.

What do you think of these results? What is your strategy for rebalancing in retirement?

More reading

Grow Your Income or Spend Less to Reach FIRE in 2026?

Reach Financial Independence faster. Learn why growing your income is just as important as spending less and how to widen the gap to save more.

9 Things that are Wrong With FIRE

Is FIRE perfect? We discuss the common criticisms and downsides of the Financial Independence, Retire Early movement.

7 Best Blogs on FIRE

There are more and more blogs about Financial Independence and Retire Early (FIRE), so which ones should you read? Here are my favorites!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Good breakdown of why rebalancing still matters in retirement. It’s easy to overlook but makes a difference long term.

Hello Baptiste,

So I did track down this article after you mentioned it on the fire calculator page. The results I shared there differ a little because using your cool service as a base, I score rebalancing options not on swr success but on terminal value average (and also terminal value median). So this explains why I saw “yearly” as better most times.

Thanks

Hi Joseph,

Thanks for sharing. It is definitely interesting (and not unexpected) that you get different result based on the terminal values.

Be careful that the terminal values can get a little crazy.

What shall I say, you did it again, yet another incredibly helpful article :)! Many people write about the rebalancing conundrum and give some half-baked tips, but you actually go about solving the problem in a very practical and thorough way.

One thing gets me confused though: In terms of worst portfolio duration, wouldn’t NOT rebalancing affect your downside risk, resulting in worse portfolio durations?

Example: Your bond allocation becomes lower than it should compated to your allocation target. Normally, now you would rebalance, but you don’t. Than you get hit by a crash & multi-year bear market.

HI Tim,

Thanks for your kind words.

Regarding the worst duration, it depends on what is the risk :) If the risk is running out of money because of low stocks, then, rebalancing would hurt worst duration. But in general, the risk for worst duration is lack of bonds. So it is possible that the worst duration would be better with rebalancing. But I have not gotten worst duration results with this simulation. If I update this article, I will have to do it.

Excellent, thanks again for your valuable contributions!

Thank you for your article. It gave me new perspectives for re-balancing. I’m currently in the accumulation phase, 20 years from retirement. I found one of my accounts to be very imbalanced, mostly bonds. It’s too much to rebalance through deposits so I’m going to rebalance them via buy/sell and this article gave me confidence that this is the right decision.

Hi Nira,

I am glad it gave you food for thought!

Indeed, if it’s too much out of balance, you could still buy/sell

Rebalancing reduces volatility assuming stocks/bonds at 60%/40%. However, it should lower returns.

That sums it up nicely :)

Very interesting analysis. A comment or two:

1) When adding or withdrawing funds, that presents an opportunity to move towards your target allocations. It may reduce the need to actually rebalance.

2) I adopted an approach in this link

https://www.michaeljamesonmoney.com/2020/04/portfolio-rebalancing-based-on-expected.html

The basic concept is to consider trading costs as well as bid/ask spreads to determine when it makes financial sense to rebalance and identifies which assets are farthest from target – not necessary to bring all assets back to target if no financial benefit. It also includes a factor which you can adjust to increase or decrease the “triggers”.

I used this when markets dropped in March 2020 and I ended up selling a portion of my small bond allocation and moving to equities – very profitable move.

Hi Bob,

1) Completely understand, this is what I am doing during the accumulation. And this could be done during the retirement phase as well. However, it there is too much of an imbalance, this won’t work well.

2) That sounds interesting, but I still prefer never to sell unless I need the money :) But well done for your profits!

Returning to point 1) (When adding or withdrawing funds, it presents an opportunity to move toward your target allocations. This may reduce the need to actually rebalance.) When you make monthly withdrawals, it makes sense to sell the asset that is overweighted, right? Even if you can’t fully achieve the target allocations and still need to rebalance the portfolio in the long term. It is getting complicated when you try to follow a 4 assets strategy….

You got it exactly right. And indeed, the more assets you have, the more complicated it may become.

Hi Mr TPS

Thanks for all of your articles, they’ve made a real difference for me and even those that aren’t directly relevant are always an interesting read!

I read the article above after reading a couple on the Trinity Study, and those seemed to show that historically the higher the percentage equity allocation, the better the outlook because equities were nearly always outperforming bonds over longer periods of time.

Do you think the calculations for rebalancing are effectively saying the same thing? If you had waited longer for rebalancing, the equity portion would have been at a higher level (because historically it went up more quickly), therefore on average the Trinity Study data will always say “take longer to rebalance”, or in the extreme don’t rebalance – just move to a higher equity allocation?

Hi Andrew,

Thanks for your kind words :) This is what keeps me going :)

That’s a very good point. And yes, I am pretty sure they say the same. By not rebalancing, you are increasing your allocation to stock over time and increasing your returns.

You are also increasing volatility. But for the extremely long-term, this volatility is not a huge deal.

Thanks for pointing that out!

Do you see common elements in your failing simulations at 4%? How could a retiree realize they were on a track to fail? How could a retiree make course corrections if they recognized their portfolio being on a failing track? Would dropping to 3.5% for a number of years put them back on a track to succeed?

Hi J,

The common elements would be a series of bad months, especially early on during retirement.

There are a few things you can do. You need to make sure your retirement amounts are not significantly higher than your planned withdrawal rates. You can try to reduce your withdrawals when they are reaching the planned level. But of course, there are limits to flexibility. If you get a special cash cushion to handle these cases, this could also help.

I hope that helps!

It does, thank you for this very informative post! Exciting what you can show with your code!

Amazingly interesting. Thank you so much for your work on this and the Updated Trinity Study.

Two things comes to mind:

1. The main selling point of robot advisors (or whatever you call it…) is that they automatically maintain your allocation strategy by rebalance continuously. I assume this means daily or weekly…

But this goes against your conclusions and also the idea to “let the winners keep winning”. Right?

2. We’re now in a low-interest environment so what is the point of having bonds when they do not return much?

Your results show that having bonds actually decrease the success rate.

I understand bonds are there to reduce the risk, in order to sleep better etc. Also, it can give an element of currency speculation if you buy bonds in foreign currencies.

Myself I keep a diverse portfolio (stocks, bonds, gold + silver) and I try to maintain an accurate balance in order to “buy cheap and sell expensive”…

But I am more and more doubting to purpose of the bonds. Just seems like there is more downside than upside in the long term.

Hi Kalle,

I am glad you liked it :)

1. That’s a good point. And I would agree with you that if you do not want to rebalance, a robo-advisor would even be even less interesting than it is. I really do not think they are going to rebalance daily, it’s just too expensive. I would say that they are doing it monthly or weekly.

If you have only two assets like stocks and bonds, it’s easy to rebalance. And looking at my results, not really interesting. However, for more assets, let’s say you have a Swiss allocation and a U.S. allocation, it may still be interesting. I have only run the calculation for stocks and bonds. The results may be different for different asset classes.

2. That’s a great question. As you said, bonds have never been here for returns, they have been here for stability. They should reduce the volatility of your portfolio.

In the context of Europe where bonds are negative, I would say there are really no points in investing in bonds unless you want to speculate on interest rates.

I also have doubts about bonds. If you have a long-term investment in front of you, I do not think bonds will do a lot for you. I do not have any bonds on my portfolio for instance.

How is your portfolio doing?

Thanks for stopping by!

Hi Mr TPS.

Thanks for your reply. My portfolio is doing quite well, thanks. It’s perhaps a bit on the conservative side considering I’m below 40 years old… But I’m able to sleep at night so my risk level is probably in the right range. :)

I have about 25% treasuries and bonds in my portfolio. However, I find it difficult to have a good diversification between different currencies and different types (government, corporate etc). I miss a good product for this.

I know many prefer to have their treasury/bond investments in their local currency (or hedged to the local currency) but I think this is a mistake in the longer term and I think this is basically currency speculation.

Currencies fluctuate but the products we consume are increasingly global so if your local currency takes a plunge before it’s time to retire then you may struggle…

A good global stocks fund take care of this automatically but I don’t know of any equivalent bond fund.

So, you are lucky to stay with 100% stocks (and also lucky to be Swiss). It’s definately a luxury to have a clear long-term investment strateg that can tolerate 100% exposure to stocks.

Good luck with your investments and please do keep up the good work with your articles!

Hi Kalle,

Thanks for sharing all this!

I completely agree with you on personal allocation. If you can sleep at night, it’s a great portfolio for you. Some people definitely have an allocation that is too high for them and they worry about it.

It’s true that there is also a risk in your local currency. But if you know exactly where you want to retire, I would agree that it’s still less of a risk than an international currency. Now, if you plan to retire in Venezuela, you are better off with some bonds in USD, that’s sure. But in the end, it will be different for each situation.

Thanks for stopping by and good luck with your investments as well!