A Free FIRE Calculator – Find your chance of success

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

To choose a safe withdrawal rate, you need to know its chances of success. For that, you can use historical data from the stock market. Historical data helps you see the chance of success for each withdrawal rate. Today, I am making this easier for everybody with a free FIRE Calculator!

Recently, I have been playing a lot with withdrawal rate simulations. I am using a lot of data from the U.S. stock market to see which withdrawal rates are safe and which are not.

I have written a tool that can do the simulations for me. I have already released some results with this data.

In this article, I share a withdrawal rate calculator you can use to do the simulations yourself. And I also share the data and the tool I am using!

You can use this calculator to know which withdrawal rate you should be using. You can tailor the simulation to your situation.

FIRE Calculator

I recently wrote a simple tool to compute the historical success rate of withdrawals. I wanted to make this tool available to everybody!

So I wrote a FIRE calculator that can use the same data, and that is available to everyone. With it, you can discover your chances of succeeding in your retirement.

Without further ado, here is my FIRE Calculator

This calculator will simulate all possible retirement dates in the given years. And for each retirement starting date, the tool will check if the retirement will succeed or not. Success means that you still have some money left.

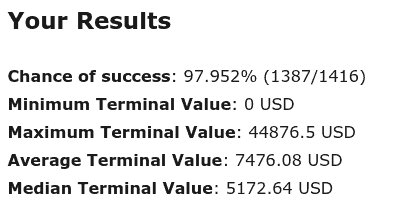

Here are some results generated by the FIRE calculator:

This calculator uses the same data I presented with my Updated Trinity Results for 2019. These are the stock market data for U.S. stocks and U.S. bonds from 1871 to 2018. It also uses U.S. inflation data for the same period.

How to use it?

Using the calculator is simple. I tried to make it as straightforward to use as possible.

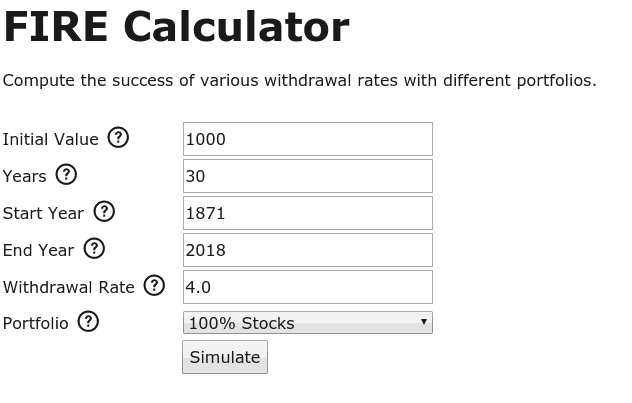

There are several things you can choose from to do a different simulation. First, you can configure the initial value of your portfolio. The initial value is how much money you have at the beginning of your retirement.

Then, you need to configure how many years you want to retire. If you plan to retire at 40 and think of living up to 90, you need your money to last 50 years. So you can input 50 in the Years field.

After this, you can configure the period for the simulation. By default, the simulation will use all the data. The data is from 1871 to 2018. If you want more recent years, you could configure from 1968 to 2018 for only 50 years of simulation. Remember that with a more extended period, there are more retirement dates.

Finally, you will have to select your portfolio. You can now choose the basic portfolio choices from 100% stocks to 100% bonds.

Once you have set your current situation, you can click on Simulate and get your results.

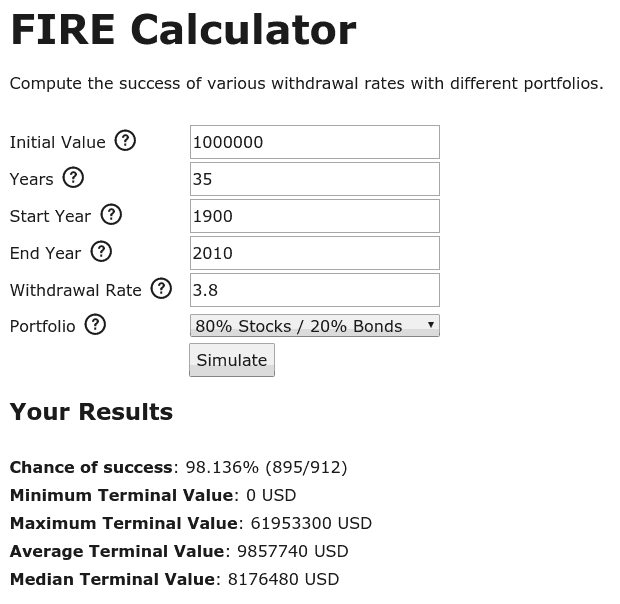

We can make an example:

- You plan to retire with one million USD (The Initial Value)

- You want your money to last for 35 years

- You want to simulate from 1900 to 2010 (Start Year and End Year)

- You want to withdraw 3.8% each year (Withdrawal Rate)

- You hold 80% in stocks and 20% in bonds

Here are the results of this simulation

As you can see, this scenario has a significant chance of success, more than 98%. This scenario is very safe. There are only 17 months between 1900 and 2010 where this scenario would have failed. In total, you have results for 912 start dates.

On average, you would end up with 9.8 million USD after this scenario. Be careful about the average value. The extremes often skew it. I would recommend you look at the median value. In that scenario, the median terminal value is still 8.1 million USD.

How does it work?

Now that you know how to use the FIRE Calculator, we can learn how the simulation works.

The calculator will try every possible starting month in the given period. From 1900 to 2000, there were 1080 months to start ten years of retirement. 1080 is 90 years times 12 months.

For each starting month, the simulation will start with the initial value. If your starting value is 1000 USD and you have an 80% stock portfolio, 800 USD will be in stocks and 200 USD in bonds.

The initial withdrawal is set based on the initial value. If your withdrawal rate is 4%, the withdrawal will be 40 USD for a 1000 USD initial value.

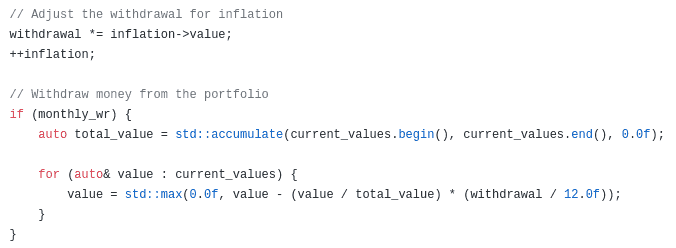

Then, the simulation will advance month after month. At the end of each month, the portfolio’s value is updated based on the historical returns of this month. For instance, the stocks could increase by 1%, and the bonds could increase by 0.2%.

After this, the calculator updates the withdrawal amount for inflation. For instance, the withdrawal could go up 0.5% if the prices increased during that month.

Finally, the withdrawal is removed from the value of the portfolio.

And this is repeated until the end of the simulation or until the portfolio value reaches 0.

It is successful when there is more than 0 USD at the end of the given period. Otherwise, the simulation is a failure.

The success rate is the percentage of successes in the total number of simulations.

What comes next?

I have many ideas to improve the calculator in the future. But I want to try to keep it simple so that everybody can use it easily.

I intend to add some income to the simulation. For instance, having a regular monthly income in retirement can help. Indeed, this will reduce the withdrawals you need each month. You may even invest during retirement.

I also intend to let the user choose the rebalancing technique. For instance, this could help you choose between monthly and yearly rebalancing.

Finally, I am also thinking of making it more flexible in the portfolio choice. For instance, you may want 90% in stocks and 10% in bonds.

If I add more options to the calculator, I will make a second, advanced version. That way, only people that want extra options will see them. Otherwise, I am afraid that the calculator will become complicated for people who do not need more features.

Safe Withdrawal Rate tool

The calculator uses a small simulation tool I wrote some time ago.

I wrote this tool to compute the results of withdrawal rates based on historical data. For instance, it can tell you how much chance of success you have if you use the 4% rule for 50 years with different portfolios.

I have used this tool to reproduce the results of the Trinity Study up to 2018. I was able to simulate success rates for thousands of withdrawal rates. The original study used old data. It was an excellent opportunity to see if their results hold for more recent years.

I also used this tool to compare different rebalancing techniques in retirement. It was great to see when you should rebalance your portfolio for the best chances of success.

I always wanted to share this tool with you to be transparent. I had to make some improvements before sharing them on this blog.

You can find the source code for this tool and the data on GitHub: thepoorswiss/swr-calculator

The repository contains information about how to use the code and the data. Keep in mind that this is a command-line tool, not a graphical tool. And I wrote it to generate data for my articles. I did not write it for general purposes. I may improve it for more use cases in the future.

Feel free to let me know if you find any issues with the code or have ideas on how to improve it.

I realize that this may not be interesting to most of you. For most people, the FIRE calculator on the website will be much more useful. And the web calculator uses this tool.

I hope people interested in the source code or the data find it useful. I am glad I get to share this data and code with you.

Conclusion

I hope you will find this new FIRE calculator useful for your retirement! It is essential to know how safe a withdrawal rate is before you choose. If you plan to become financially independent, you need to run simulations.

And it is essential to know that withdrawal rates are related to your portfolio. Based on how conservative your portfolio is, you can use different withdrawal rates.

I hope that this FIRE calculator will help people choose a withdrawal rate. They can then plan for their retirement.

I still have many ideas to improve this calculator. I will try not to make it too complicated. It should remain simple. It will have two versions, one simple version and one advanced version, for people wanting more flexibility.

To learn more about Financial Independence and Retire Early (FIRE), you can read about the Trinity Study.

If you have any suggestions for the FIRE calculator, I would like to hear them.

What do you think of this calculator?

More reading

Some extra income in retirement goes a long way

Planning to retire early and looking to increase your chances? Would income in retirement help your chances of success? We do the test!

What is a failsafe withdrawal rate?

Is any rate safe? We explore if a "failsafe" withdrawal rate exists for early retirement and how to protect your portfolio from total failure.

Grow Your Income or Spend Less to Reach FIRE in 2026?

Reach Financial Independence faster. Learn why growing your income is just as important as spending less and how to widen the gap to save more.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste!

Thanks for all your great guides!

The initial value would be the cash/2nd pillar/3rd pillar/value of stock bonds/real estate etc. Right?

Should we not also take somewhere into account the monthly pension from the 1st pillar?

I

Hi,

The initial value should be the sum of eveything you can withdraw, your FI net worth. I would not included real estate (at least not the primary residence) because it does not contribute to your withdrawals.

Currently, I have not factored in the monthly pension, but any income you will get will make it easier. The problem is that the 1st pillar won’t kick in directly if you are planning to retire early.

But I plan to add this feature in the feature.

thanks, I think that it would be a nice addition. Even 1500CHF per month, 18kCHF annually would make a big difference if somebody expects to get by with 40-50k per year. But as you said, they will only start coming after a certain age.

Thanks for the calculator. It showed 100% success for my situation-so it’s in agreement with every other calculator I’ve used. I’m a little on the cautious side. One small tweak- could you put commas or periods in the result numbers? I think it would make them easier to read! Good job on the calculator!

Hi She’s FIRE’d,

It’s good to be cautious :)

That’s a good idea! I really need to reformat the output :)

It’s on my list now!

Thanks!

It’s really cool, keep it up the great work with the blog!

Thanks Steve!

Great calc, well done!

i added a link to this on Mustachian Post:

https://forum.mustachianpost.com/t/fire-calculator/2761

Hope you don’t mind!

Hi Mr. Zack,

Thanks for the kind words!

Of course, I do not mind :)

Thanks for stopping by and for spreading the word!