How to sustain your capital in retirement?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

I have made many retirement simulations on this blog. Until now, all these simulations were successful if the capital was not entirely depleted. However, many people would like to sustain their capital in retirement.

So, is it possible to sustain our capital in retirement? And how much more careful do we need to be?

We will find out by running simulations where sustaining the capital becomes the success criteria!

Sustaining Capital

First, what does it mean to sustain capital? It means that during the period, our capital does not diminish.

We could have a strict rule that says the capital cannot fall below 100% of the initial value. But we can also be more flexible by having a rule allowing us to fall to a certain percentage. I would say that sustaining 90% of the capital is already great, especially if it lets us retire faster.

The Trinity Study defines success as having more than zero at the end of the retirement period. This means we can use significantly more money than if we try to sustain our capital.

Therefore, we can expect that sustaining capital results in a lower success rate. As such, it will likely need a lower withdrawal rate to compensate.

So, we will use simulations to see the difference it makes.

Simulations

Over time, I have made many simulations on this blog. These are historical simulations based on historical data from the stock market. For instance, I have updated the results of the Trinity Study to include recent years and longer retirement periods.

I have developed a tool that can quickly calculate many withdrawal simulations. This tool is available freely on GitHub with the data.

I will use historical data for the US stock market in this article, with the S&P 500 and the 10Y treasury bonds, from 1871 to 2024. This is the longest historical data available and is generally the reference for most Trinity Study simulations.

30 Year Retirements

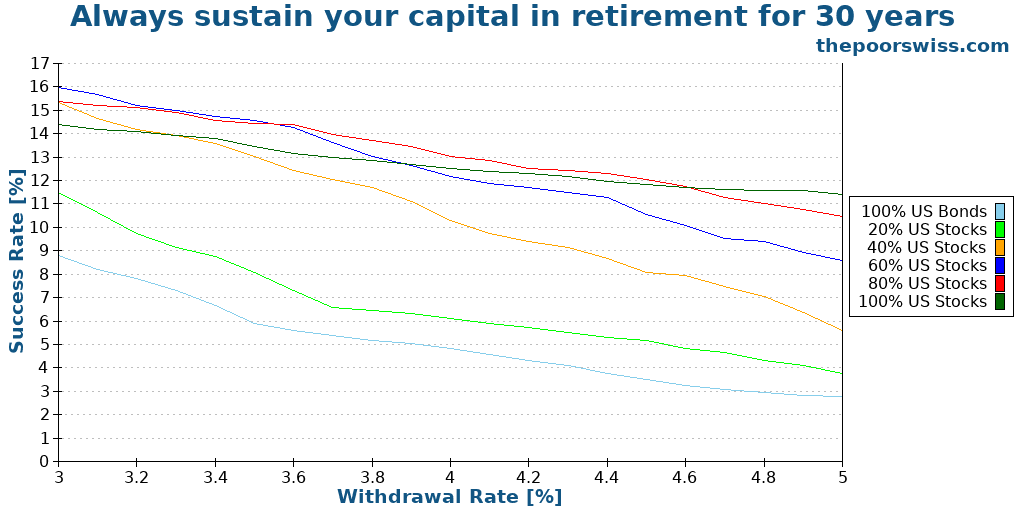

We start with a classical 30-year retirement period. First, we try with the strictest rule where the portfolio can never go below its initial value.

In this case, the results are bad since the rule is too strict. It is challenging to sustain 100% of the capital during the simulation. It puts a lot of stress on the early years that need positive returns.

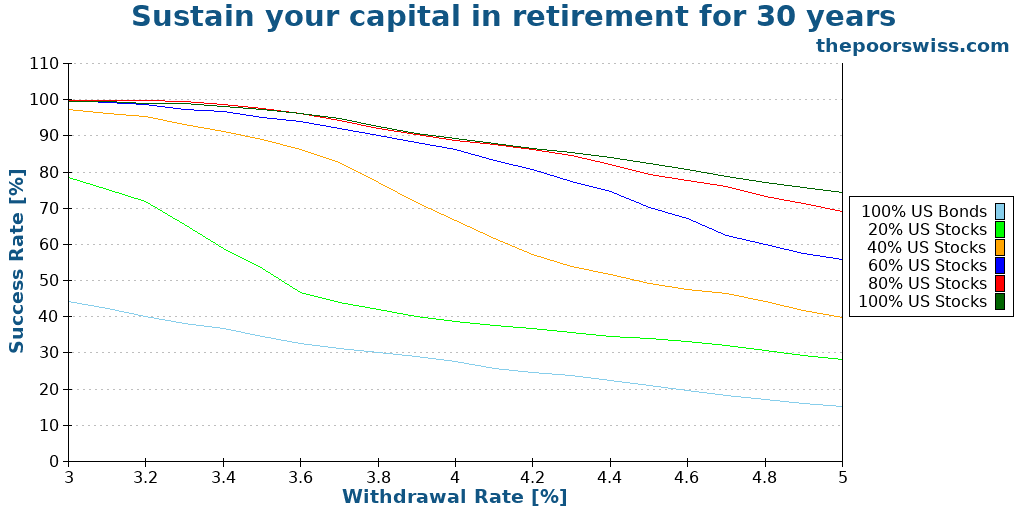

Therefore, we should adapt our rule. It is more interesting to have a success rate depending on sustaining the portfolio at the end of the period.

So, we will see how it works. This time, the portfolio must be 100% of the initial value at the end of the retirement period.

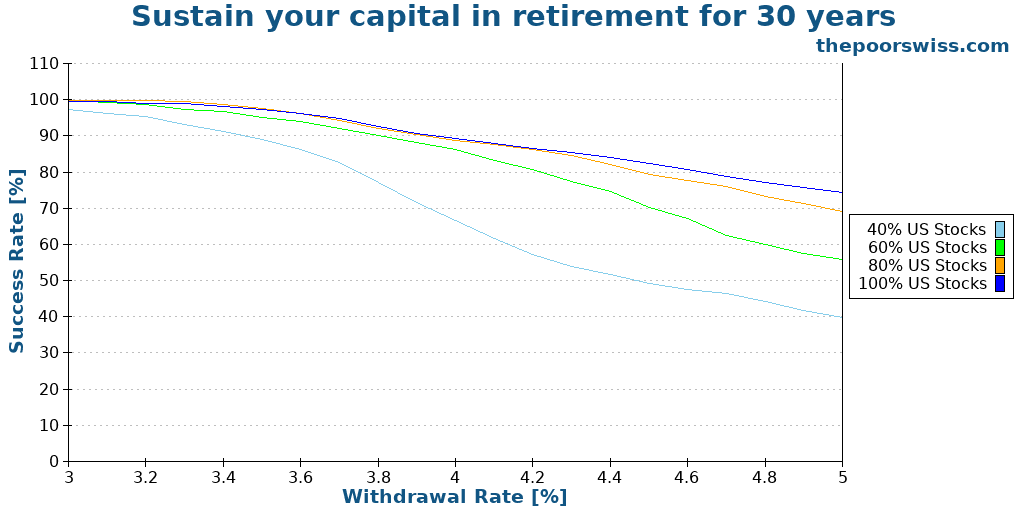

This time, the results are much better. Even at a 4% withdrawal rate, we get better than 85% success rates. We can remove the 100% and 80% bonds portfolios failing this test to see better.

The success rates are lower than with the standard retirement criteria. However, we can still observe relatively good results with a portfolio with at least 60% in stocks. However, the success rate decreases quickly once we go higher than a 4% withdrawal rate.

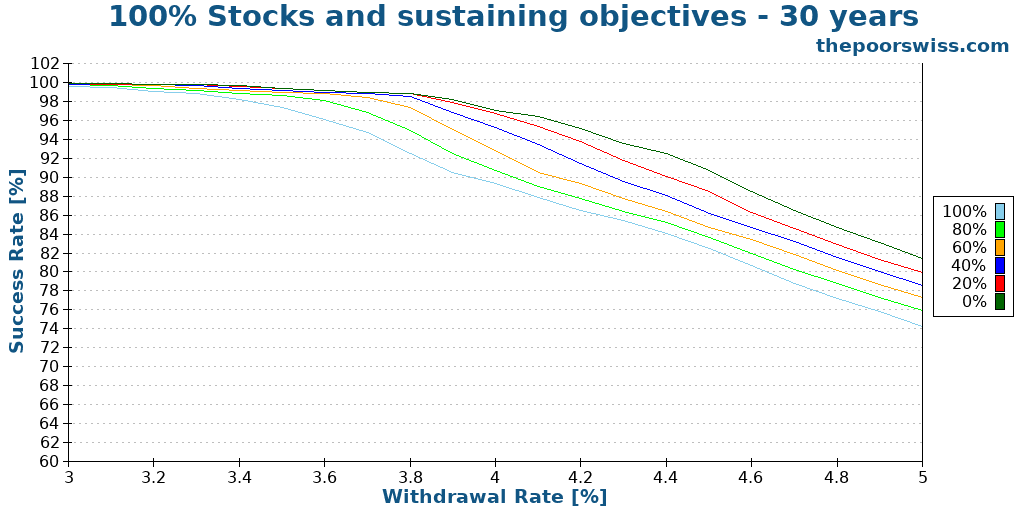

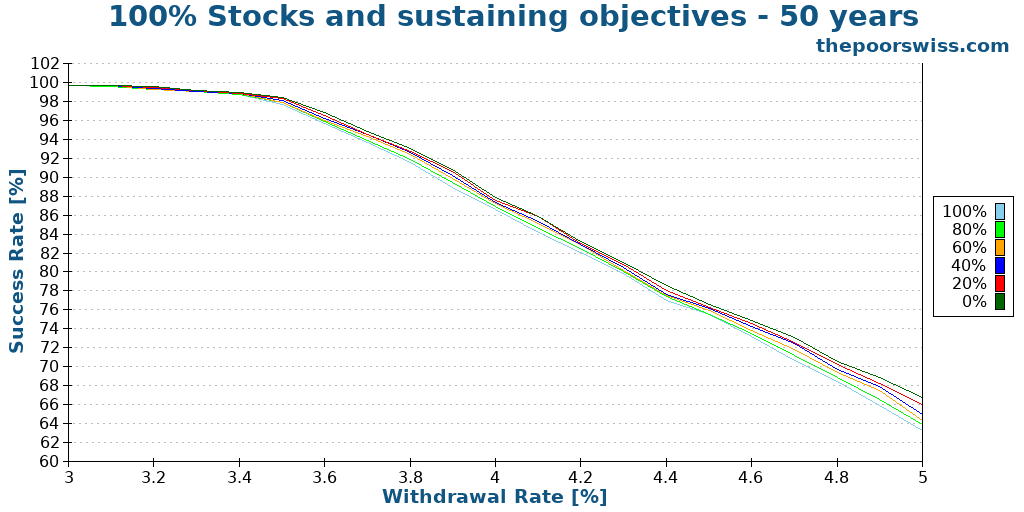

We can also see how a 100% stocks portfolio compares with different targets (0% is the standard Trinity Study criteria):

As should be expected, a higher capital-sustaining objective has a lower success rate. This is logical since we need to end up with more money.

Interestingly, the gap between the different objectives widens as the withdrawal rate increases. Indeed, with a 3.5% withdrawal rate, the difference between 0% and 100% is a 2% lower success rate. However, the gap is almost 8%, with a 4.0% withdrawal rate.

If you want to sustain your capital in retirement, you may want to plan for 80% capital sustaining instead of 100%. That way, you can gain a few percent of success rate.

Thirty years of retirement is relatively short if we consider early retirement. So, we will see what would happen with a longer retirement.

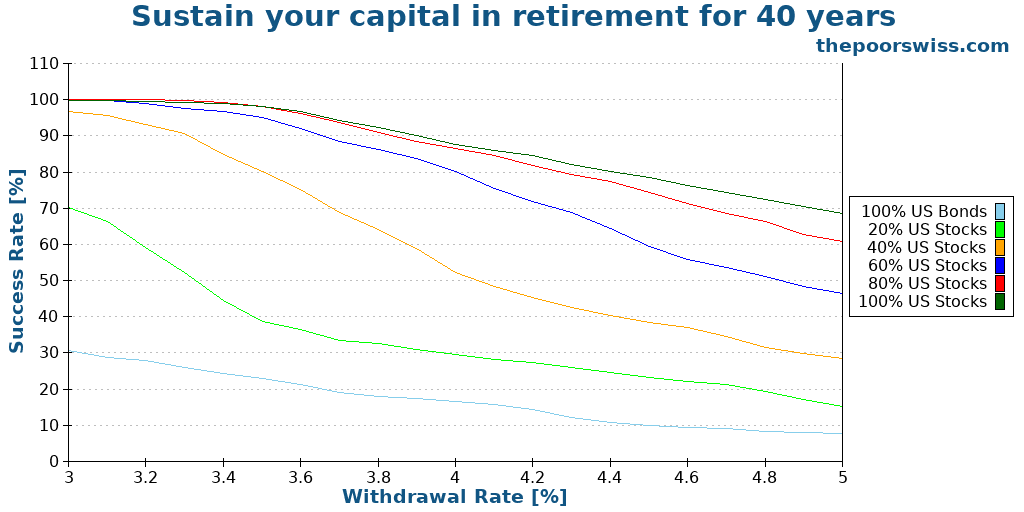

40 Year Retirements

We run the same simulation for 40-year periods.

When we increase the retirement period, bonds suffer more than stocks. The impact on portfolios with a high allocation to bonds is very significant, but the impact on portfolios with a high allocation to stocks is not too bad.

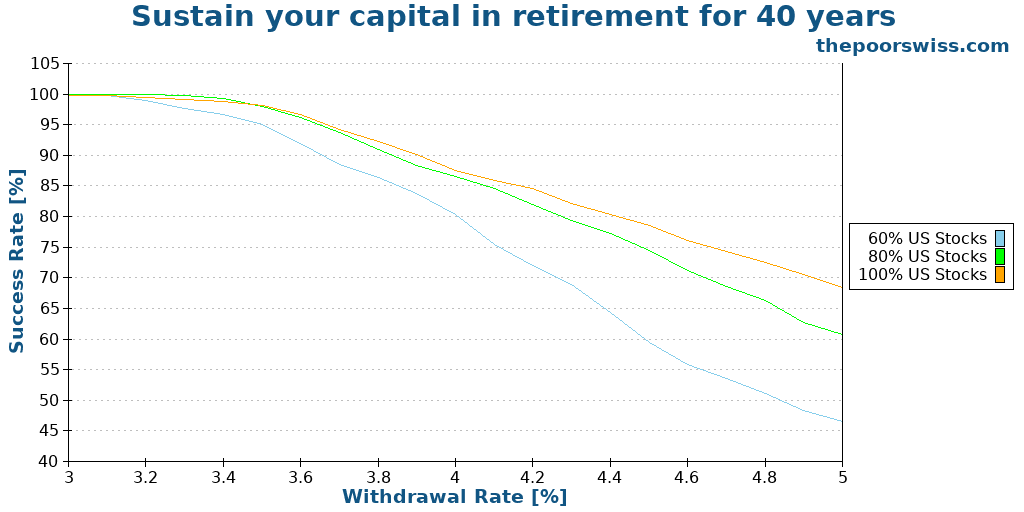

Again, we should remove some portfolios to see better what is happening.

Only three portfolios are generating decent results. And even among these portfolios, only two have more than an 80% chance of success with a 4% withdrawal rate. This means somebody wanting to sustain his capital in retirement would need a withdrawal rate below 4%, ideally around 3.5%.

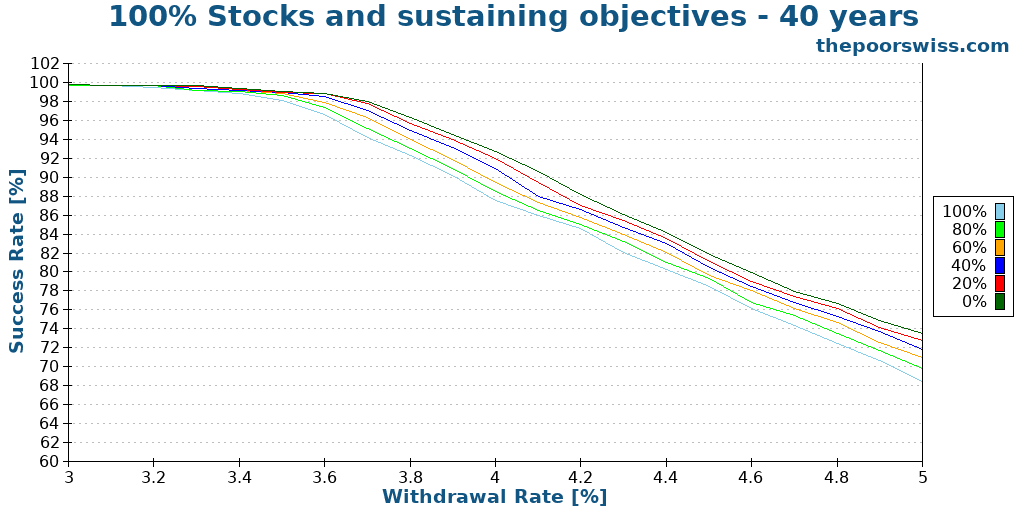

Again, we can see how it compares with different objectives for a 100% stock portfolio.

This result is very interesting. We can observe that the gaps between 0% and 100% have become narrower. In this case, the average gap is about 4%, with withdrawal rates higher than 3.50%. It means that over long retirement periods, sustaining your capital and not running out of money become closer.

Finally, we can also increase the retirement period to 50 years, which is good for most people.

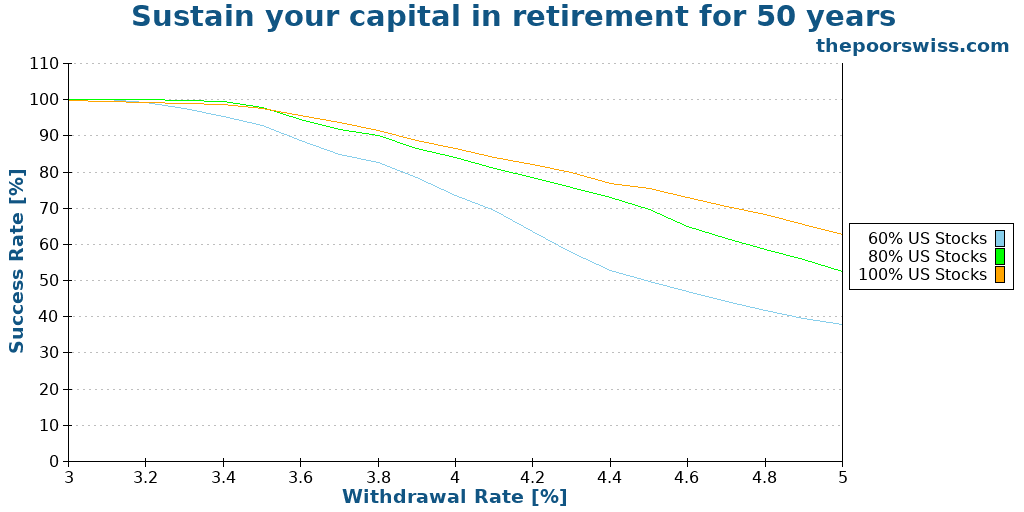

50 Year Retirements

Now, we run the same simulation for 50-year periods. I have directly removed the portfolios that would fail in this scenario.

As expected, the results are slightly worse than for 40 years. However, the three portfolios still do relatively well. If you have a 90% success rate criteria, you will need to use the following withdrawal rates:

- 3.80% for 100% of stocks

- 3.70% for 80% of stocks

- 3.50% for 60% of stocks

These withdrawal rates are still reasonable. This shows that sustaining your capital in retirement is possible and reasonable.

If we think about it a little more, it makes sense. Indeed, over a very long period, you need high returns to withdraw money consistently. And these returns will be significantly higher than your withdrawals in good times. And in bad times, you will have accumulated enough not to fall too low.

So, over a long period, sustaining your capital is not much more demanding than simply sustaining your withdrawals.

Finally, we can conclude with the final comparison of different objectives.

This picture is extremely interesting. It shows that over 50 years of retirement, we have almost the same chances of sustaining our capital as simply sustaining our withdrawals. The difference between 0% and 100% objectives is tiny unless you go for more than a 4.5% withdrawal rate. But such withdrawal rates are not reasonable with 50 years of retirement.

This means we have a high chance of significantly increasing our capital over 50 years. This is excellent news for people wanting to sustain their capital.

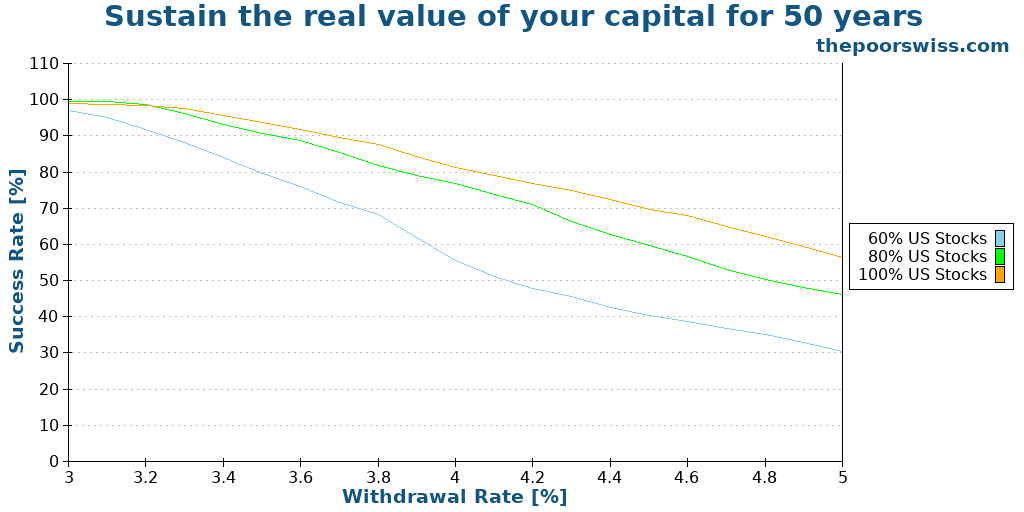

Sustain the real value of your capital

Until now, we have considered the initial value as the target. Inflation was considered for the withdrawals but not for the target value. So, if you start with a million, you will end up with a million in the case of success.

However, a million in 50 years is different from a million today. So, we can also take inflation into account for the target value. So, we would adjust our target every month with the monthly inflation.

We can see what would happen if we change this criterion:

As expected, the results are significantly worse. It makes sense since the target can increase considerably over time. We can see the scale of the differences. And as the withdrawal rate increases, the differences between sustaining the nominal and real value also increase.

If you want to sustain the real value of your portfolio, you will have to use a withdrawal rate lower than 3.50%. Therefore, this criteria requires to be very conservative.

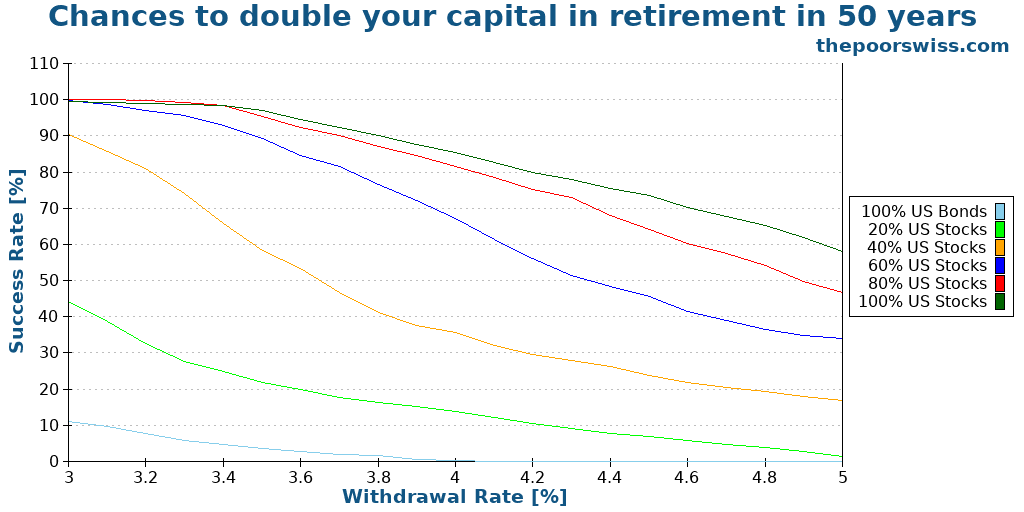

For fun: Can we increase our capital?

Since I had the tool ready, I figured it would be interesting to see whether we could double our money. Instead of aiming for 100% of the initial capital, we strive for 200%. It is simply a different objective.

We can observe two things in these results:

- Bonds are unlikely to double your money.

- Stocks are very likely to double your money.

I was surprised by these results. But this shows that over 50 years, in most cases, you have an excellent chance to double your money. It is not much more difficult to double your capital than to sustain it.

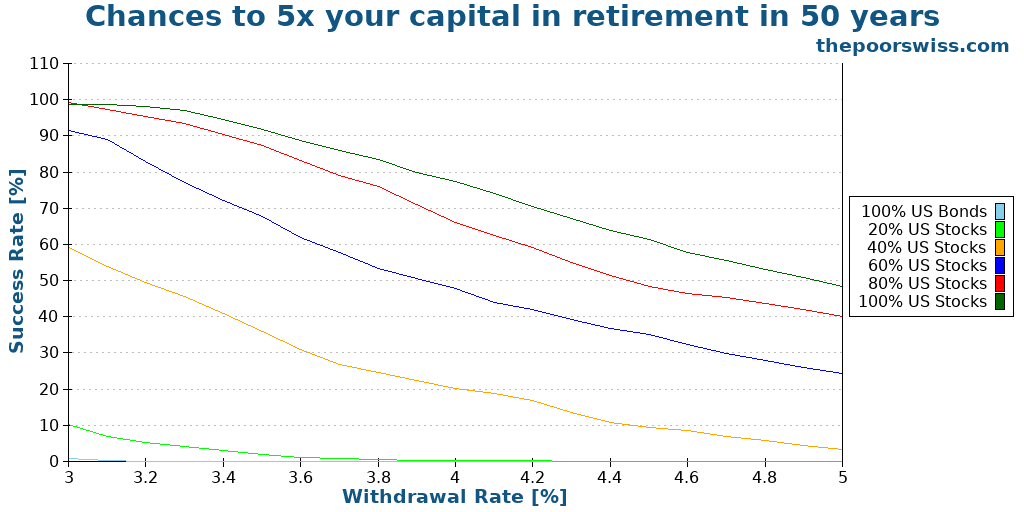

Here is what happens when trying to quintuple (5x) your capital.

This time, the success rates have taken a sizeable hit. Nevertheless, some of the results are not bad. At a 3.5% withdrawal rate, you still have over a 90% chance of multiplying your capital by 5.

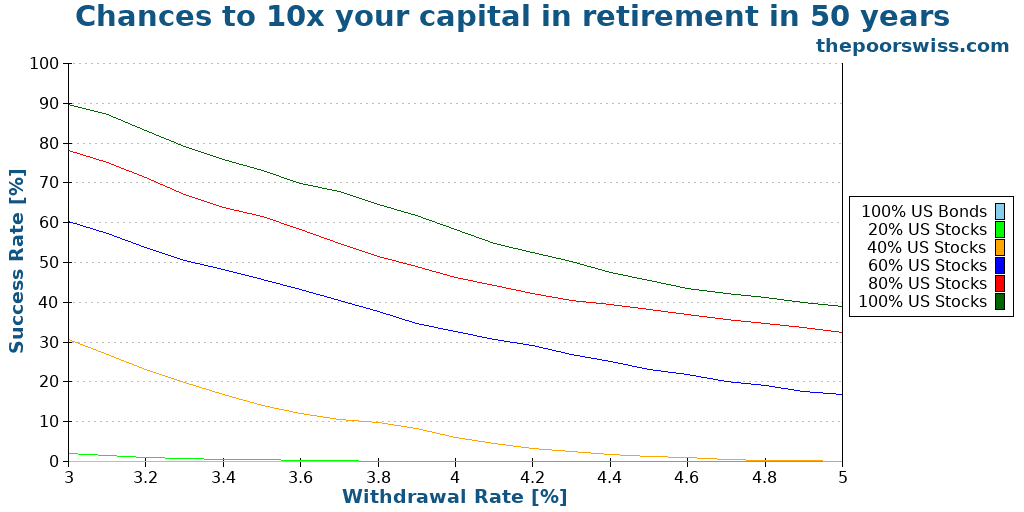

Finally, here is what it takes to multiply your money by 10.

Chances are now significantly lower. However, you still have an excellent chance to multiply your capital by 10 with a 100% stock portfolio. These impressive results show that these simulations’ average terminal values are incredibly high.

Why sustain capital?

Since sustaining capital rather than simply planning to have enough to live is harder, why would one want to do that?

There are several reasons for that. The first reason is that people often want to leave a legacy for their heirs. The goal is to create generational wealth. It is not a bad idea if you do not have many heirs, but if you have many, your wealth will be divided quickly and often lost after only a few generations. But if you want generational wealth, planning to sustain your capital is great.

Another reason is that planning to sustain your capital is safer than planning to sustain your withdrawals. With that strategy, you get significantly more margin of safety.

I do not think it is worth planning to sustain my capital. I do not believe my heirs will profit from this money, and I believe it is safe enough to play to sustain my withdrawals.

Conclusion

If you want to sustain your capital in retirement, there are a few essential points to know:

- Sustaining your capital in retirement is more challenging than not falling to zero. Nevertheless, achieving this with a slightly lower withdrawal rate is possible.

- If you want a reasonable success rate, you will need a consequent allocation to stocks.

- With a very low withdrawal rate, you will likely sustain your capital in retirement.

- With a low withdrawal rate, the chances that you will increase your capital are high.

Overall, if you plan for a long retirement (50 years, for instance) with a reasonable withdrawal rate, your chances of sustaining your capital are almost as high as those of only sustaining your withdrawals. This is good news for people wanting to sustain their capital.

Here, we tried to optimize for sustaining the capital. It is interesting to note that some people try to optimize their withdrawals to deplete the capital. The idea becomes to increase spending for experience and not let a large capital to heirs.

What do you think about these results? Do you want to sustain your capital in retirement?

More reading

The best and worst times to retire early

Timing is everything. We look at historical data to find the best and worst times to retire early and how market valuations predict success.

Can you withdraw 4% of your current portfolio?

In the Trinity Study, we withdraw based on the initial portfolio, what happens if we withdraw based on the value of the current portfolio?

6 keys to avoid the pitfalls of financial independence

The dark side of FIRE. We discuss the potential pitfalls of pursuing Financial Independence, from burnout to social isolation, and how to avoid them.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Maybe you should set up a Patreon :)

Hi John,

I tought about that, but I don’t think people want to pay a subscription and I don’t want to hide some of my content behind a paywall like too many content creators.

I may add a system to do a donation, because many readers asked me about that, but I did not find a good system for CHF.

Nano (XNO) are great for tips and donations. Love your blog!

Thanks, but I’d rather not get involved with any new digital currency yet :)

Hi! What is the compound annual growth rate of the S&P 500 used for this model? Online I’m seeing a CAGR for the SP 500 at 9.74% and for the 10y bond at 3.31%, with inflation of around 3% in the US.

Do you not think that using the historically extremely strong US stock market in your assumptions cause a distortion and way too optimistic model? A lot of academics consider the US outperformance to be mostly luck and survivorship bias and thus unlikely to repeat.

I am not using any compound value, but actual monthly from the S&P500 from the last 150 years.

It may be not be the same in the future, that’s definitely true. But we have no way of knowing that. And we have no better historical data.

Great post. Have you considered to include inflation into the mix?

You could buy a lot more with 1 million dollars 2 years ago than today. I imagine the compound impact of 20 years of inflation.

Hi ILS,

Inflation is taken into account. Each month, the withdrawal amout is adjusted for inflation.

But I could also take into account inflation for the final value, if that is what you mean. That would be interesting, but that would also make it significantly harder to sustain.

That is exactly what I meant. Trying to sustain the final value after inflation.

I assume that the main point of trying to sustain the capital during the retirment is to leave one heirs the gift of high financial independence ratio. For this, sustaining the capital value after inflation is the only meaningful way to look at it, in my personal opinion.

Yeah, that’s a good point. I will try to update the article later with the computations, but since that means updating the code as well, it may take a while before I get the time.

That’s a really great point. I would be also very interested to see trying to sustain the final value after inflation.

Hi Richard,

I have already updated the article with sustainging the final real of inflation :)

Really interesting simulations and findings! Thanks.

Thanks, I am glad you like them!