How can you plan to die with zero?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

If you are planning an early retirement, you will have to choose a withdrawal method. Standard methods of withdrawal have a high probability of ending up with significantly more money than what you started with. Many people do not like it because it means they could have either spent more or retired with less.

So, can we adapt the withdrawal method to aim to die with zero? This idea was popularized by the book Die with Zero, by Bill Perkins. In this book, the author proposes a different approach to spending in retirement. And there are other methods that allow one to plan a retirement where we aim to deplete the capital at the end of retirement.

Die with Zero

Die with Zero is a popular book by Bill Perkins. The main idea of the book is to optimize spending for experiences. The idea is that when you are young, you can spend more because you are more active and you do more active experiences. As you age, your health declines, and so does your potential for activity. As a result, we should optimize our withdrawals for when we are early during retirement.

Note that I have not read the book, but I am interested in the withdrawal method and how to implement it, and especially how to validate whether it works. I have done many historical simulations in the past, and I will run more with the aim of trying to die with zero.

The issue with this book is that it is not very practical. The idea is mostly to spend more early and less late in your life. But how much is that? The author does not go too much into detail about how to implement it, but we can draw some withdrawal rules.

The basic idea is to withdraw each year our balance divided by the number of remaining years. So, if you have one million left and 10 years left, you can withdraw 100,000. Then, each year we adapt this amount based on a health factor that will decay over time. This idea leaves a lot of room for interpretation.

First, how do we define the health factor? There are many ways to do that, unfortunately. I propose to use a simple method in 3 phrases:

- For the first 40% of the retirement, we use a factor of 1.5 to maximize our spending on good health.

- For the next 40% of the retirement, we use a factor linearly decaying from 1.5 to 1.1

- For the last 20% of the retirement, we use a 1.0 factor

However, there are still two important things to adapt. First, if we only spend our balance divided by the number of years left, we may be left spending a few cents per year, which is not reasonable. Therefore, we need to add a floor to our spending (a minimum). This means one more parameter to spend.

Then, we also need to add a ceiling to our spending (a maximum). The point is that spending more has diminishing returns. Spending five times more does not make you five times happier. There is a limit to the experiences that money can bring us.

It is important to note that both the minimum and the maximum are quite personal. And they will also depend on wealth. If you have a very high wealth, you can afford a high ceiling to your spending.

If the withdrawal is above the ceiling, the author of the Die with Zero book recommends actually either giving that to charity or putting that in a special inheritance fund. But you could also keep that amount and increase your margin of safety in retirement.

With these parameters, we can now try to implement the die with zero withdrawal method and see how it compares with the standard withdrawal method of retirement.

Results with the Die with Zero method

As usual, I will use historical data from 1871 to 2025. I will use data from the US stock market, US bond market, and US inflation. In all cases, the portfolio is rebalanced yearly.

Since I want to compare it with the original withdrawal rate method, I will use a floor as a percentage of the initial value. For instance, if you start with one million, your 3% floor level of spending would be 30,000 USD per year. For the maximum spending, I will use three times the minimum. So, with a minimum of 4% spending, your maximum level of spending would be 12% spending. And both the minimum and maximum will be adjusted for inflation every month.

30 years of retirement

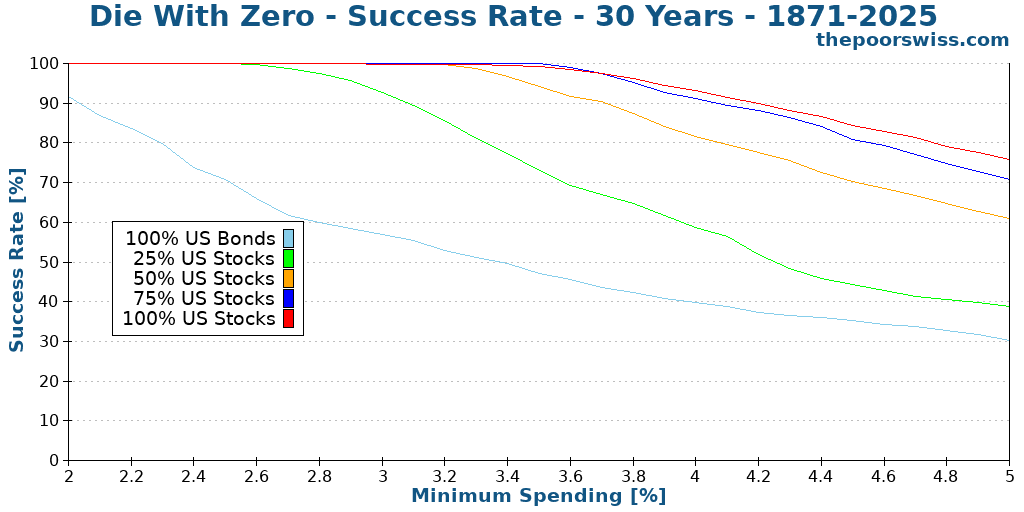

We can start with 30 years of retirement.

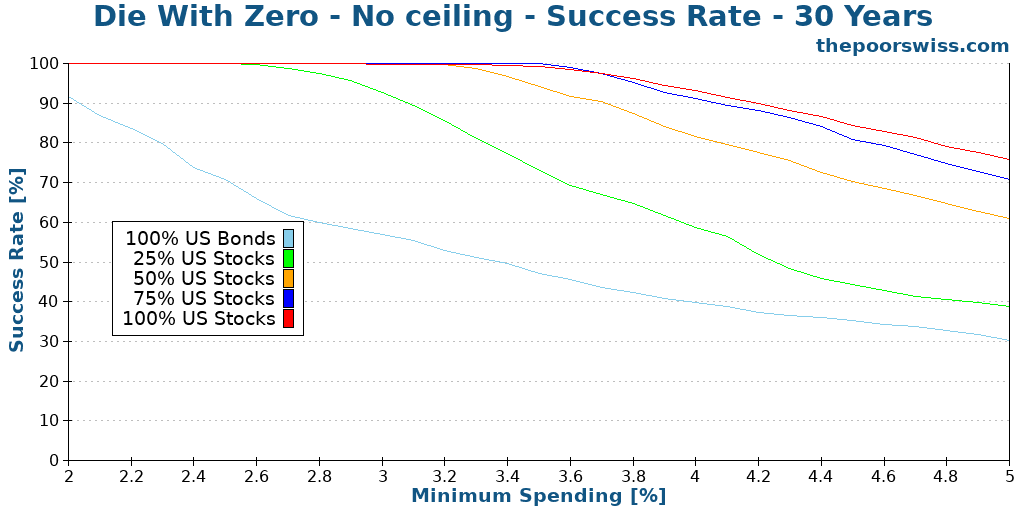

At first, I was expecting much better results than that. But then I realized that the goal is to run out of money, so it makes sense that these results are more risky. Indeed, to end up at zero at year 30, we aim to spend more money. However, this also means we are taking more risks, even at similar withdrawal rates.

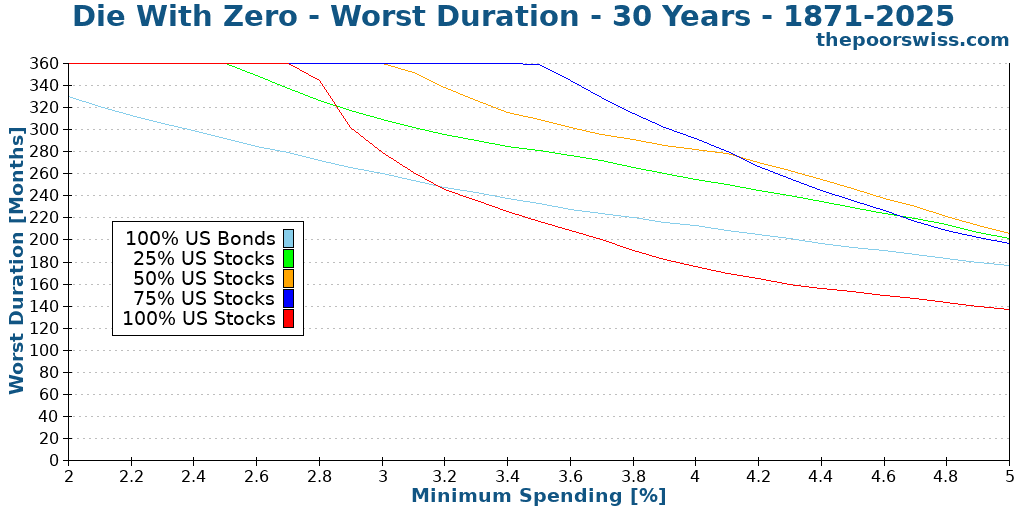

We can look at how quickly we run out of money with the worst duration in this same configuration:

Just like with the standard results of the Trinity Study, we can see how the 100% stocks approach can fail very early on, while bonds let us be safer. On the other hand, the success rate with more stocks is higher. It looks like it really helps to have an aggressive portfolio with this strategy.

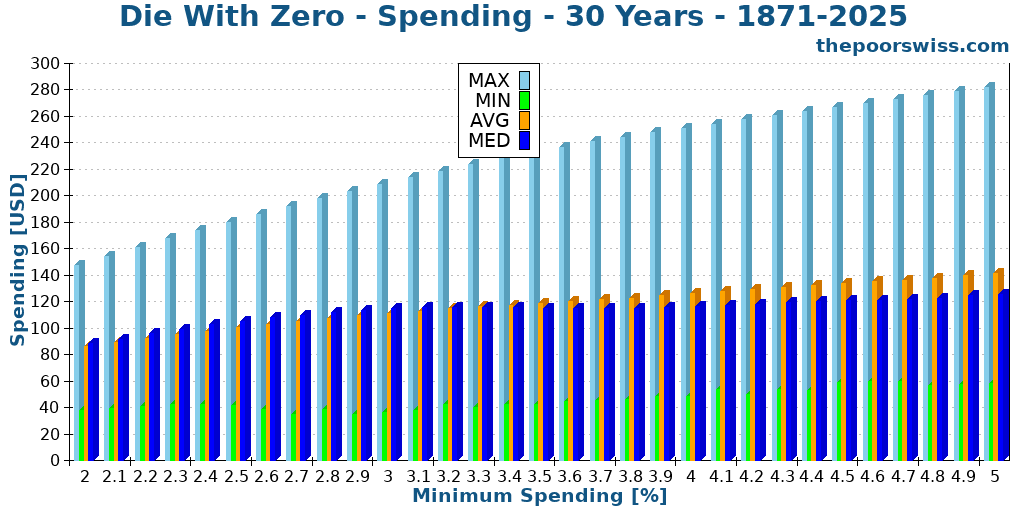

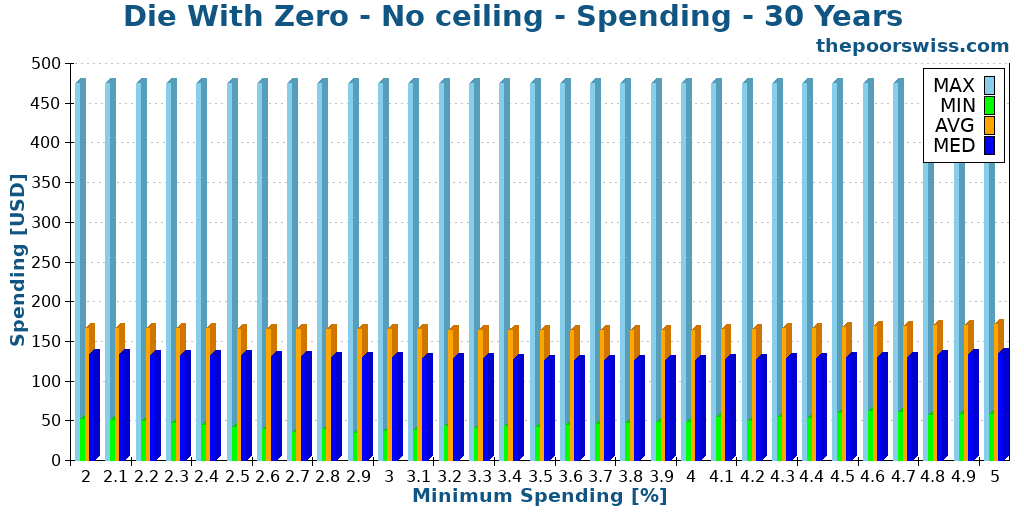

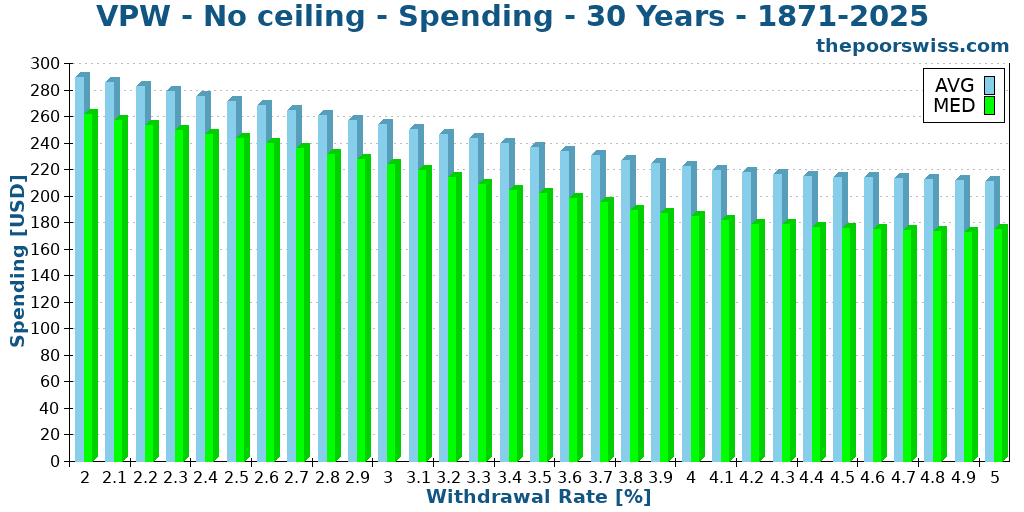

We can validate whether we are actually spending more with this withdrawal strategy. Here is the spending with this strategy and a portfolio of 100% stocks:

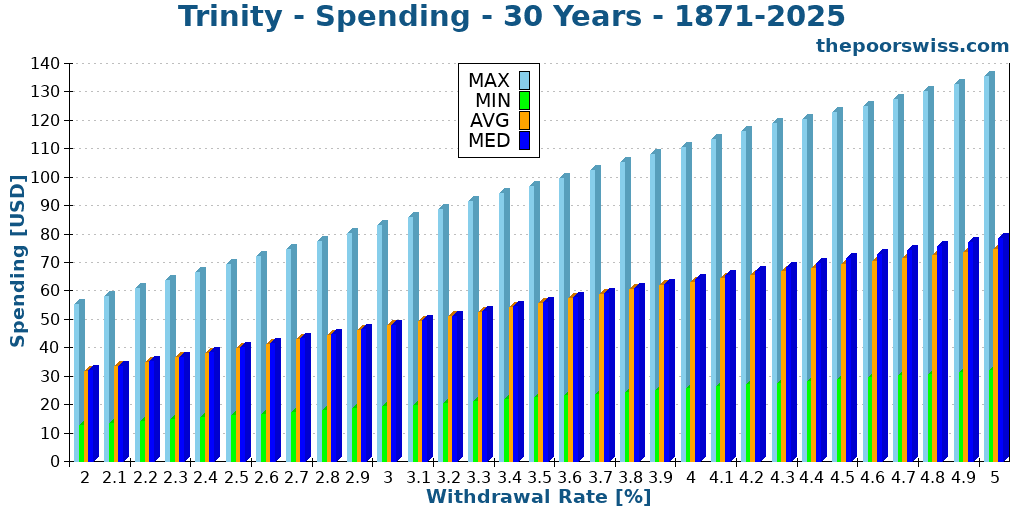

And for comparison, here is the spending with the standard Trinity study:

We can see that with the Die With Zero method, we can spend significantly more money. Overall, this comes down to the expense of a riskier withdrawal method.

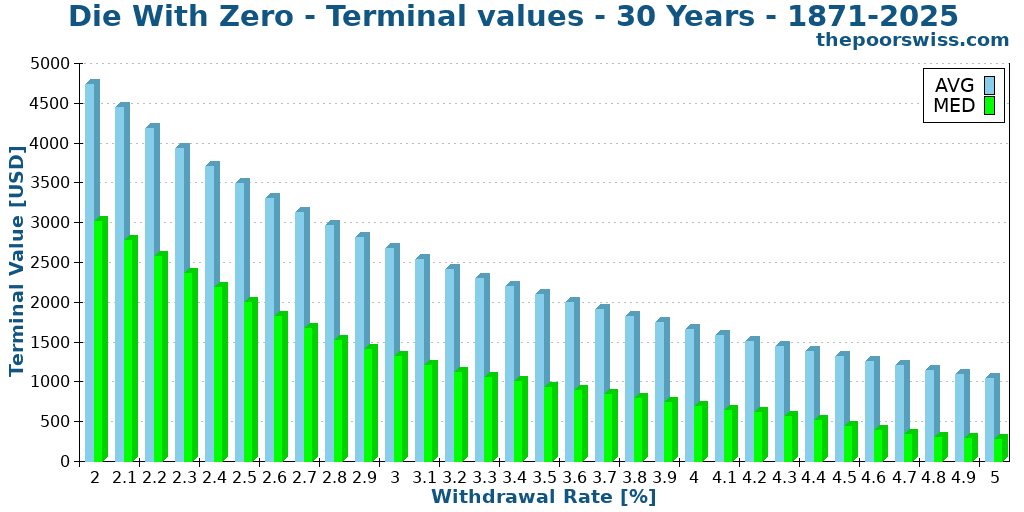

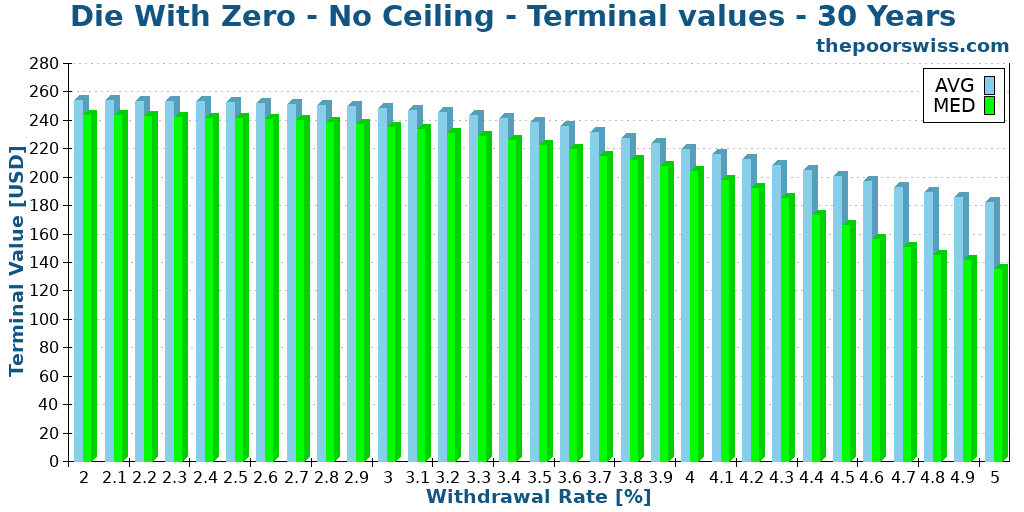

Since the goal of this method is to die with zero, we should look at the terminal values of the simulation. We will look at the average and median terminal values across all simulations.

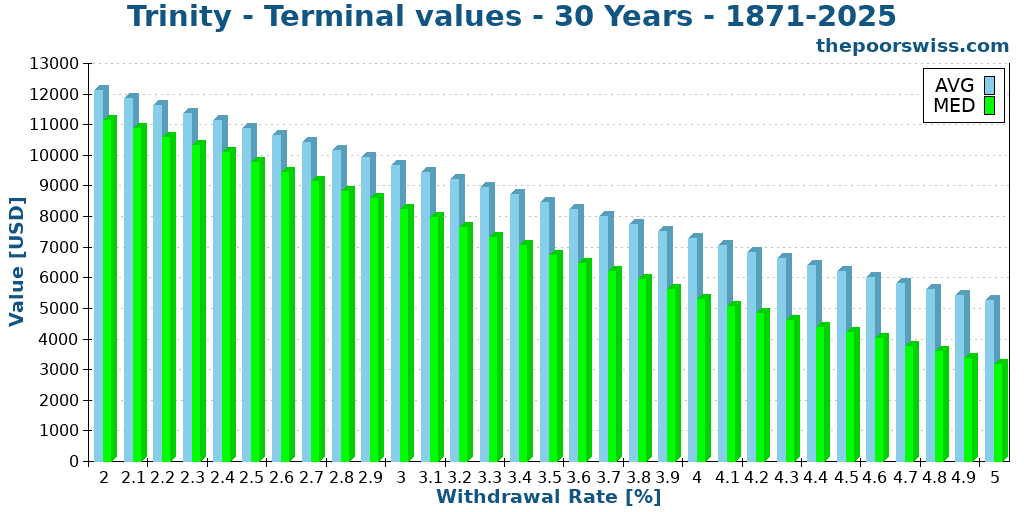

These are actually quite low already. We can look at the same graph for the Trinity Study as well:

We can clearly see that the terminal values are much lower, which is great and is expected. We could wonder why it is not closer to zero. This is actually because we have set a ceiling on the spending. In the next section, we increase maximum spending, so we can look at the terminal values there as well.

So, can you die with zero with this method? Yes. But you might also die earlier than you thought.

It is worth mentioning that you can reduce the minimum spending and increase the maximum spending, and you would still increase your chances of success. However, if you are using a lower minimum, you will need to accumulate more money to reach financial independence (and hence work more).

Increase ceiling

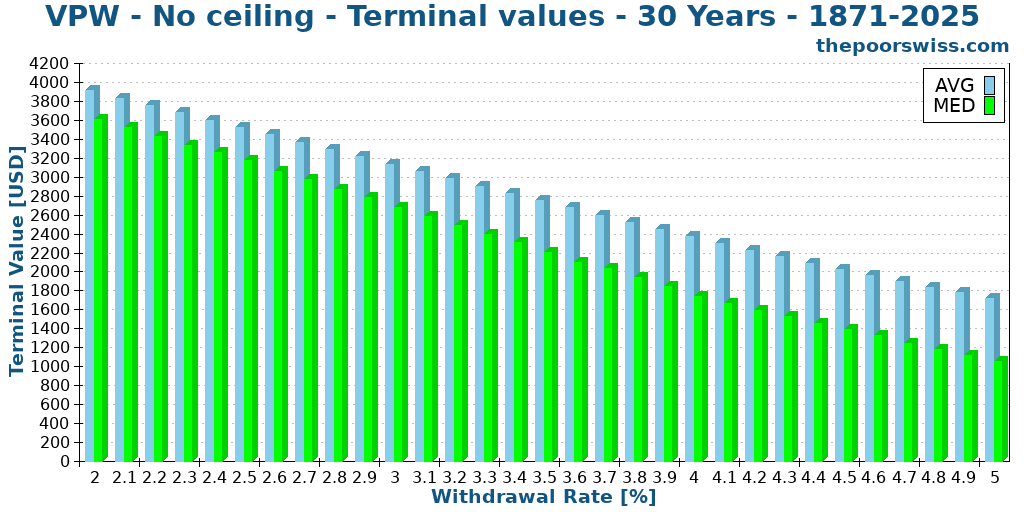

Currently, I have used a ceiling of 3 times the minimum. It is interesting to check what would happen without a ceiling.

In fact, very little changed with this parameter. This indicates that we can increase spending without reducing our chances of success. We can look at our spending again and see if that actually changed:

Here we can see something interesting. Since the upper limit is gone, only the lower limit has some influence. But since we generally spend more than this because of trying to deplete the portfolio, we can observe relatively stable spending regardless of the lower limit.

Again, we should look at the terminal values without the ceiling.

We can see that the average is very low, about 40 times lower than the standard withdrawal rate. Not reaching zero on average is fine; it still shows that we are very close, especially when we compare with the huge average terminal value of the Trinity study.

50 years of retirement

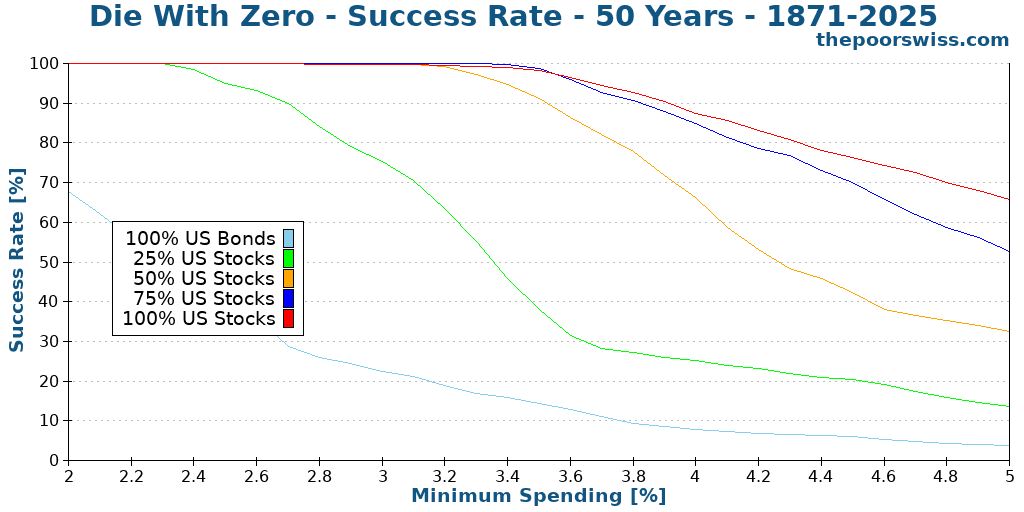

We can see if these results hold true for a retirement of 50 years. Again, here is the success rate of this method.

It is interesting that the results did not change much for portfolios with high allocations to stocks. This makes sense since the goal is to deplete the portfolio after the total retirement period. The difference with more years is less significant than for the standard withdrawal rule.

For 30 years of retirement, the chances of success were lower than the Trinity Study method, but with 50 years, they are comparable.

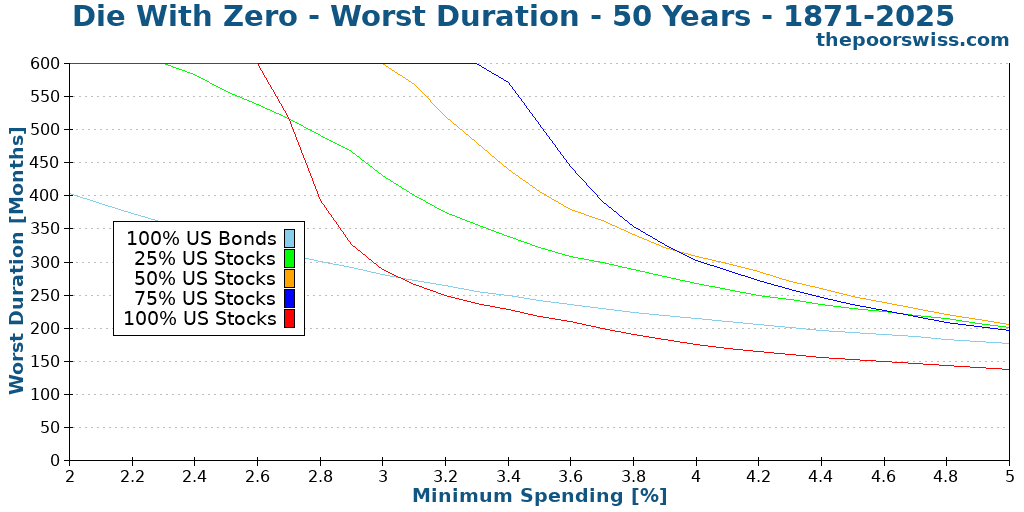

We can also look at the worst duration in this case.

Again, the results are not much different from the results for 30 years; they have slightly shifted to the left.

Summary of Die With Zero

Overall, the Die With Zero method is interesting. It allows you to spend more money than the standard withdrawal rule. However, it is riskier since we spend more. The book is not very specific on how to achieve it, and if we only use a simple 1/N withdrawal with a health factor, we could end up with very little money left to live on. Therefore, we need to add a level of minimum spending that is necessary. Once we do, it becomes comparable with the Trinity Study results, but with higher spending (and the spending is variable, based on health).

This method adds a little complexity compared to the standard withdrawal rule:

- You need to set a health factor based on your age

- You need to set your minimum level of spending

- You need to set your maximum level of spending (this is optional)

On the other hand, it achieves its goal well, which is to die with zero.

Variable Percentage Withdrawal (VPW)

Another strategy that aims at the same goal, to die with zero, is the Variable Percentage Withdrawal (VPW) strategy. Contrary to the Die With Zero method, the VPW method does not try to maximize spending early. It is more conservative in that sense.

This method has been developed on the Bogleheads forum. It is usually used with a table of percentages per year. The usual withdrawal tables are ending up at 100 years old. It means that it is done for living up to 100 years old. And the percentage varies each year, with the goal of increasing withdrawals over time.

If we are not using a table, we can use a formula to compute the VPW percentage. We have two parameters: r is the returns we expect every year, and n is the number of remaining years. And this would give us this formula:

=1 / ((1 – (1 + r) ^ n) / (r / (1 + r)))

In my simulations, I will use this formula for the percentage withdrawals. I will use 4.5% expected returns, which is more or less producing the same number as Bogleheads tables. However, I am going to use the same percentage across the board. In practice, this percentage should be different for each portfolio. It should be lower for portfolios heavy in bonds.

Again, we need to set up a minimum that is not too low, but this is less important for this method.

Results with the Variable Percentage Withdrawal method

I am going to use the same methodology as the Die with Zero method and treat the parameters in the same way.

30 years of retirement

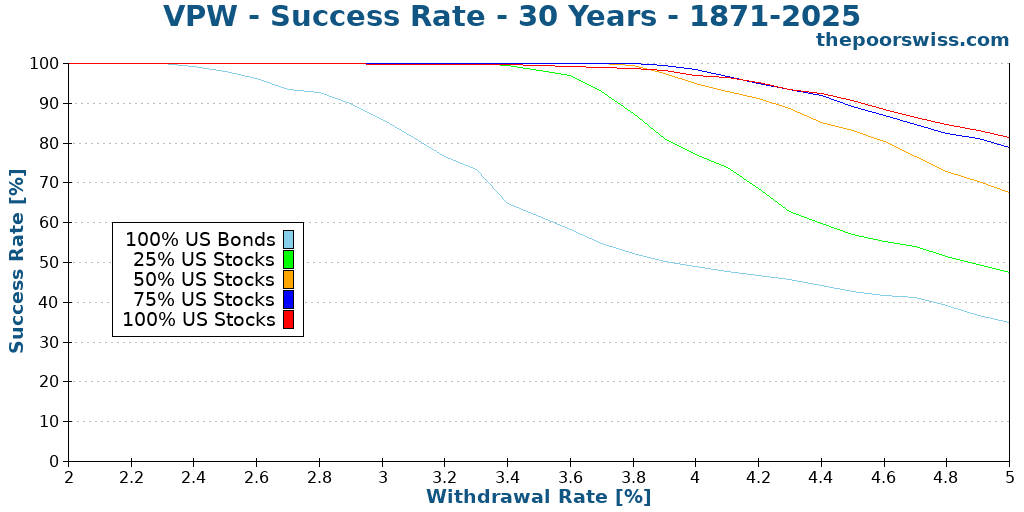

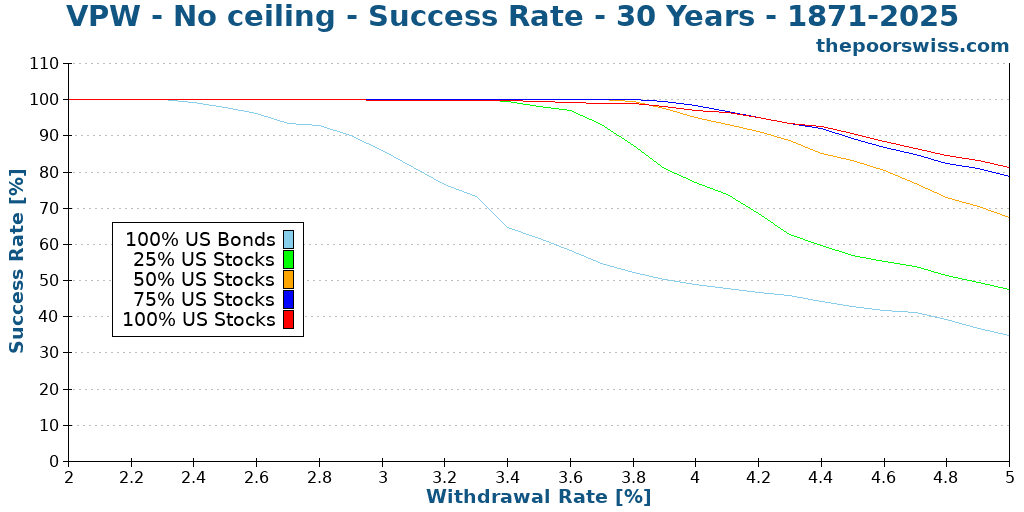

We can start again with 30 years of retirement and see our chance of success in retirement.

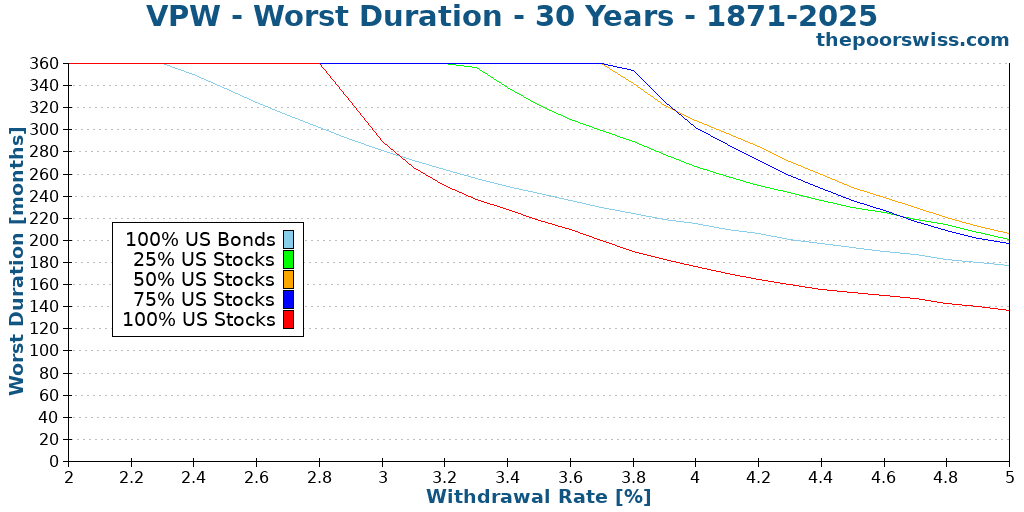

We can see that the chances of success are significantly higher than with the Die With Zero method. Interestingly, the results are very close to the Trinity results. We can also look at the worst duration:

Again, this is better than the method from Perkins, but this is also very close to the standard withdrawal rule. We should see if spending has increased.

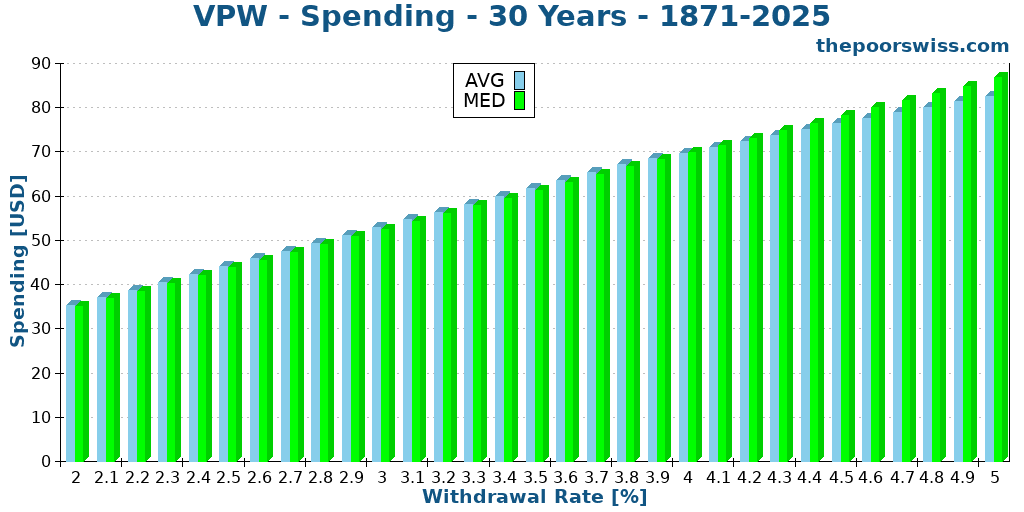

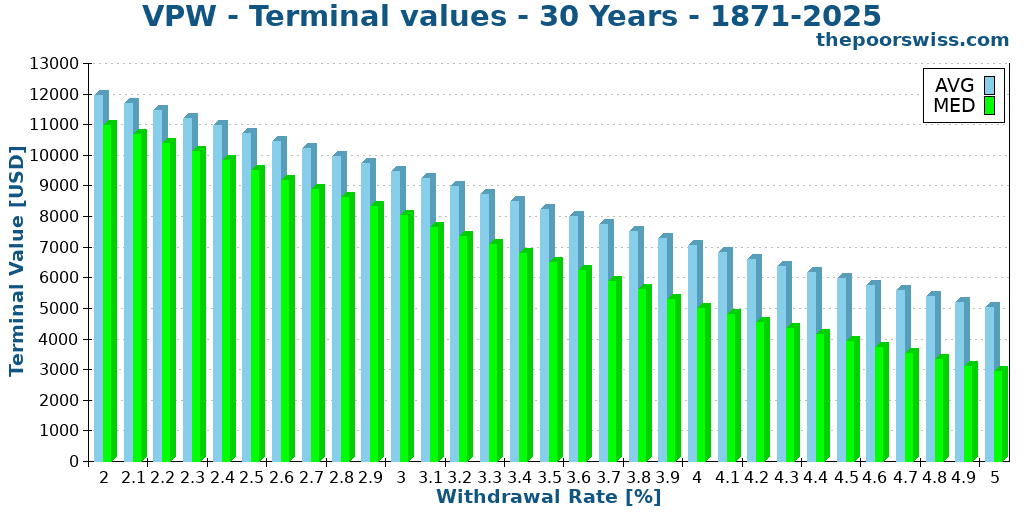

In fact, spending is higher than for the Trinity study, but not much higher. And we can confirm this by looking at the terminal values.

These values are barely lower than with the standard withdrawal rates. We need to remove our ceiling again to see how it works.

Increase ceiling

We can remove the ceiling instead of using 3 times the minimum as the maximum.

We can start by looking at the success rate again.

Again, similarly to the Die With Zero method, success rates almost did not move. And if we look at the worst duration, we can observe the same thing. Next, we should look at the spending, to see if it really increased.

Indeed, spending increased multiple times over the previous results.

As expected, we can see that the terminal values have gone down significantly.

50 years of retirement

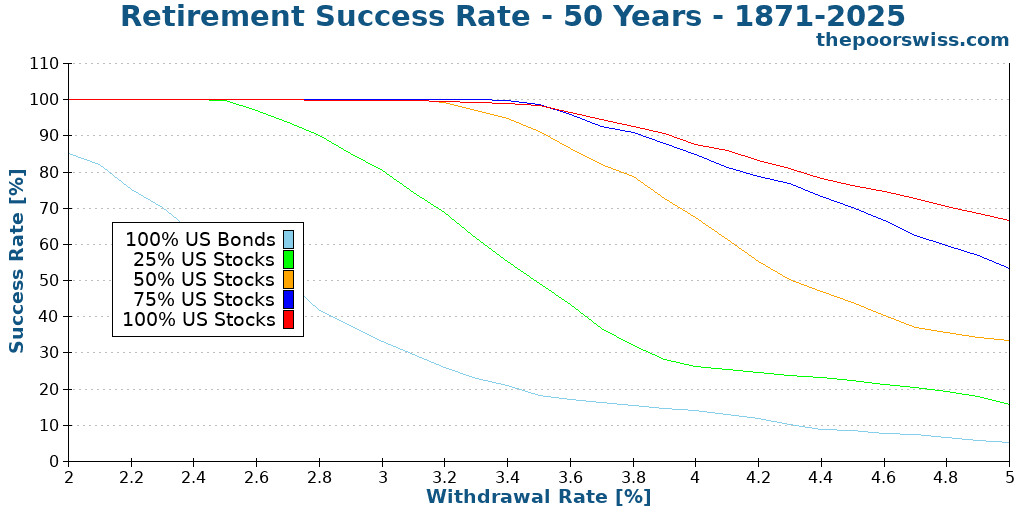

Finally, we can look at 50 years of retirement. And we can start with the success rate.

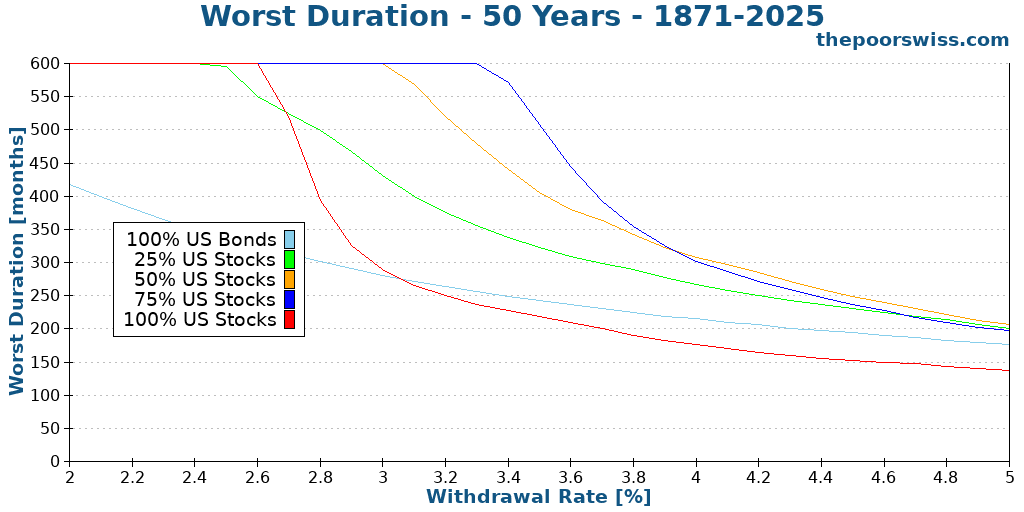

Again, we can observe a shift to the left since it is riskier to sustain 50 years with this method. However, the difference is not huge. We could still have success with a decent minimum spending. And for completeness, we can also look at the worst duration.

Again, the results are expected: a shift to the left, with shorter worst durations. But the results are still good for 50 years of retirement.

Summary of Variable Percentage Withdrawal

The Variable Percentage Withdrawal (VPW) strategy is quite elegant. It is simpler and better defined than the Die With Zero method from the book, in my opinion. It also shows a better success rate in my simulations. The only thing I do not like is it being based on a table of withdrawal percentages rather than on a formula.

As we have seen in our system, we do not really need to set a maximum spending level with this strategy. But setting a minimum level of spending is important for survival. If we did not have that, we could even have no parameters at all with this strategy, which is great.

What if you live one year longer?

Both methods are based on a model where you need to know when you will die. With Die With Zero, you will choose the age and most VPW percentage tables are based on a 100-year-old life expectancy.

So, what happens if you live to 101 years old? You have no money left with these methods.

For many people, this is fine because the likelihood of living to 101 years is extremely slim. But for some people, this is not acceptable.

One easy solution is to plan for more years. You can adapt both methods to plan for 120 years of longevity. However, we circle back to the main issue we are trying to solve. If we plan for a retirement until 120 years old and die at 85 years old, we will not nearly have died with zero.

Conclusion

The idea of dying with zero and enjoying life more is quite tempting. But this is quite risky in practice. We can spend more, but our success rate is lower, meaning we can run out of money significantly earlier than planned.

I am not convinced by the Die With Zero method. It is not sound enough for me. However, the Variable Percentage Withdrawal (VPW) method is quite elegant and seems to work well in practice. I understand people following up with this strategy.

However, with these methods, it is difficult to solve the issue of living one year longer than planned. You would need to rely on annuities for that, and it makes the methods again less elegant and less sound to me. Another issue is that it is great to die with zero, but you need to spend significantly more money than your basic threshold. So, in the end, you still have to accumulate as much money as with the standard withdrawal rates. But if you do not have a high spending habit, it will be difficult to spend more than planned.

Currently, I am not going to plan my retirement to die with zero. There are some issues with the standard withdrawal method for sure; we often end up with too much money. But I would rather increase my chances of success than decrease them. However, I want to look more into the VPW strategy in the future.

This method assumes that expenses decrease over time. However, there is one case where this can be the contrary: old-age care. If you need eldercare, you may have to increase your expenses because old-age care in Switzerland is expensive.

What about you? What do you think about these withdrawal methods?

More reading

The 6 Kinds of FIRE: Which One Are You?

Lean, Fat, or Barista FIRE? Discover the different types of Financial Independence and find out which FIRE style fits your life goals best.

How to Calculate your Financial Independence (FI) Ratio

How you can compute your ratio to Financial Independence (FI). How to use Safe Withdrawal Rate (SWR) to see how much you need to save.

Add some margin of safety to your FIRE plan

A good FIRE plan relies on historical data, so we need to protect it with some margin of safety! Here are some ways to achieve extra safety!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

I mean, as long as the AHV works, you will never be completely without money in Switzerland. That‘s at minimum 16k a year gross income. And if you do live one year more than planned, you can get EL. The last year when you‘re THAT old is usually not comfortable anymore anyway.

That’s a fair point, Barbara. In this case, you would need to take AHV into account. But getting EL is not necessarily what most people planning retirement expect :)

hmm, strange motivation, rather for lonely and greedy people, otherwise why not just living live and what is left goes to your heirs or to social causes.. didnt you think about this?

Hi beat

It’s not necessarily lonely, because with this strategy you could optimize your experiences without your spouse and children indeed. And I don’t think it’s really greedy since the goal is to spend, not save, no?

Hi Baptiste,

Thanks for providing this deep and insightful analysis and comparison – it’s very useful.

But I think you dismiss ‘Die with Zero’ too easily. Having just finished the book, I have a slightly different take away. Yes, the end result if things go ‘well’ is that the day you die, there will nothing left. You will have used it all up. But there several factors at play here. Chief amongst those is that your money should support your goals in life. Those will appear at different periods and need to be planned and financed. By doing this, you will be able to create memorable life experiences thoughout your life – not just after retirement. Perkins worries that too many of us spend too much time working too hard in jobs that they don’t really enjoy, getting to retirement, when it is already too late to enjoy some experiences and then leave a large legacy after they pass away. That legacy represents years of work and you can do some calculations to show how many days/months/years of work it takes to generate say CHF1000K of savings. so if for example you leave CHF500K when you die, that probably represents years of work. So you worked this time for nothing – you never used the money that took so long to save – which is a shame. Another point he makes is that, as you mentioned, not all experiences are available later in life because the opportunity has passed or your health has declined. E.g Your kids are only young once – what a shame if you spend those years earning money you will never use rather than creating highly memorable experiences with them. He also notes that using your money during your own life generates bonds. Instead of leaving a legacy to your kids , spend it with them during your life so that you can all enjoy that experience together. The average age of a recipient of a will in USA is around 60 years old. Most people have much less use for a large amount of money at 60 than they would at 25 or 30. So give the money during your lifetime not afterwards. I would also say that he worries that most people live on ‘auto pilot’ – they don’t think about these things until it’s too late. He wants people to plan a bit more what they want from life and then finance accordingly. He believes most people are too conservative in their planning and financing and are putting too much aside for events that are unlikely to happen. Most people dies within a couple of standard deviations of the actuarial tables. As long as you have some form of annuity that covers your basic subsistance costs in case you live to be very old, you can be more carefree but purposeful with your money earlier in your life.

However, I do agree that he does not give much investment advice – it’s more a philosophy to help you reduce your end of life regrets and to not be so scared that everything will go wrong.

I’ve certainly found it gives a pause for deeper thought and it is clearly a contrast to the FIRE philosophy of saving carefully and investing well until you have enough to be independent. It’s another approach.

Hi Nuticel

Thanks for sharing your thoughts on this strategy.

I have mostly taken an analytical approach to this strategy and not a “philosophical” one indeed.

I completely agree on spending money for experiences and on not working too long. However, for me, the book does not solve this issue. It proposes a “vague” spending strategy but it is not clear how that makes it any faster than a standard FIRE strategy.

For me, both the standard FIRE and these two methods will require more or less the same money to accumulate and therefore will retire more or less at the same time. What will change is that we can spend much more with these two strategies, which is great.

I wish we could retire earlier with a higher chance of success, but it does not seem to be the case in my testing.

>We can spend more, but our success rate is higher, meaning we can run out of money significantly earlier than planned.

Is our success rate really higher?

No :(

Will edit that crucial phrase.