How to Calculate your Financial Independence (FI) Ratio

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

When you have a goal, it is always good to know your progress toward this goal. If you are trying to become Financially Independent, it will be essential for you to know how far away you are from your goal!

For this, you will need to know your Financial Independence (FI) Ratio. This ratio will tell you how close or how far you are from reaching your goal of being financially free!

Your FI ratio will tell you exactly where you are on your path to Financial Independence. In this article, we see precisely how to compute your net worth goal. And then how to calculate your progress toward your goal. It will help you know if you need to adjust your strategy to reach your goal on time.

Stay tuned if you want to know when you will be financially free!

Financial Independence

First, what is Financial Independence (FI)?

Financial Independence means you do not need to work to sustain your lifestyle. It is also sometimes called Financial Freedom. You are financially independent when you have enough money to maintain your lifestyle without working.

For this, your wealth must generate income. And this income must be higher than your expenses. The primary way to generate income from your net worth is to withdraw from it. In general, withdrawing means selling shares from the stock market and using the realized money. However, you must withdraw little enough to sustain your wealth for the longest time. Otherwise, you will end up with no money.

It is only one of the ways to reach Financial Independence, but this is the most standard way in the community. Some people prefer to focus on passive income. And some people focus entirely on real estate to become financially independent.

There are many reasons to become Financially Independent. It is currently very popular on the internet. Especially with the Financial Independence and Retire Early (FIRE) philosophy. The idea is to become Financially Independent as soon as possible and retire early. But you can also be Financially Independent and not retire. You can then choose to do precisely what you want with your life since it does not depend on your career income anymore.

First, we will assume you are following the withdrawing idea of Financial Independence. But I will also talk about the FI ratio in entirely passive income.

Your Withdrawal Rate

If you want to become financially independent by having a large enough net worth to sustain your expenses, you may have heard of the 4% rule.

This rule states that if you only withdraw 4% of your investment portfolio yearly, it should sustain you for at least 30 years. This percentage is your Withdrawal Rate (WR) or Safe Withdrawal Rate (SWR).

This rule assumes that you invest your portfolio in the stock market. Generally, the 4% rule assumes 75% stocks and 25% bonds. But the asset allocation is up to you. 4% is the recommended safe withdrawal rate. But some people choose to be more conservative (<4%) or more aggressive (>4%). I am more conservative, so my withdrawal rate is 3.5%.

Remember that the original 4% rule is based on 30 years of retirement. If you retire very early and plan for 50 years, it may not work in the same way. For this, you may have to reduce your withdrawal rate. You can take a look at my retirement calculator to help you.

To learn more about Withdrawal Rates and the 4% Rule, read about the Trinty Study Results!

Your Financial Independence Number

Now I got my withdrawal rate, how much do I need to be FI?

It is pretty straightforward. By dividing 100 by your withdrawal rate, you will have the number of years of expense you should save. For instance, for my withdrawal rate of 3.6%, I have to accumulate 27 (100 / 3.6) years of my annual costs.

If you think your expenses will go up or down in the future, you should also account for that. Indeed, you should use the number of expenses you plan for when you are financially independent. However, this amount is difficult to estimate. If your retirement is far in the future, you may take your current annual costs as a good estimation. It is what I am doing. Every year, I update my FI Number to reflect our current situation.

Your target net worth (your FI number) is 100/SWR times your planned annual expenses. If you have yearly spending of 100’000 USD and a withdrawal rate of 4%, you need to accumulate 2.5 million dollars to become Financially independent (=(100/4) * 100’000). If you spend 50’000 USD per year and plan to withdraw 3.5% every year, you will need to accumulate 1.4 million dollars (=(100/3.5)*50’000).

This target net worth is also called the Financial Independence Number or FI Number. I wrote an entire article to help you calculate your FI Number.

Your FI Ratio

Finally, how do I get my FI ratio?

You now have your target net worth (or FI number). That is the net worth at which you will reach Financial Independence. As soon as your net worth exceeds this number, you are financially independent!

For this, you will need to know your current net worth. As an example, you can see how I calculate my net worth. Your net worth is the value of all your assets minus your liabilities (debts). But you must be careful about some assets that can depreciate or are difficult to sell.

Your FI ratio is simply your current net worth divided by your target net worth. It could not be simpler!

If you have a target of 1 million CHF and you have 100’000 CHF, your FI ratio is 10% (100’000 / 1’000’000). Or if you have a target net worth of 1.4 million USD and have 200’0000 USD, your FI ratio is 14.28% (200’000 / 1’400’000).

As soon as your FI Ratio reaches 100%, you are financially free!

My Financial Independence Ratio

As an example, we can see how my situation is at the current time. I have calculated the results for my goal. I’ve also calculated how many years it will take to get there at the current pace. Here are my results:

| Withdrawal rate | 3.6% |

|---|---|

| Expected Annual Return | 5.0% |

| Years of expense | 27 |

| Running expenses | 93735 CHF |

| Monthly expenses | 7811.31 CHF |

| Target Net Worth | 2530865 CHF |

| Current Net Worth | 337653 CHF |

| Missing Net Worth | 2193211 CHF |

| Yearly income | 133200 CHF |

| Running Savings Rate | 44.25% |

| Yearly savings | 58946 CHF |

| FI Ratio | 15.39% |

| Months to FI | 216 |

| Years to FI | 18 |

| Date to FI | 2039-01-09 |

| Current Withdrawal Rate | 27.76% |

| Months of FI | 43.22 |

| Years of FI | 3.6 |

I have computed my expenses over the last 12 months (not counting this month). It gives me about 2.5 million CHF to save. So, at the time of this article, I am missing about 2.1 million CHF. If you compute the ratio of your net worth and the target net worth, it gives you your FI ratio. Mine is a meager 15.39%.

You can also estimate how many years you need to save this amount. I have computed my savings rate as the average of these twelve months. I am assuming a 5% annual rate of return, which is conservative. It gives me almost 18 years until I reach FI.

This result is not so bad since this will be before I am 50. And my primary goal is to become Financial Independent before I am 50. It seems I am on track to reach my goal! But things can change in the future, and I am aware of that.

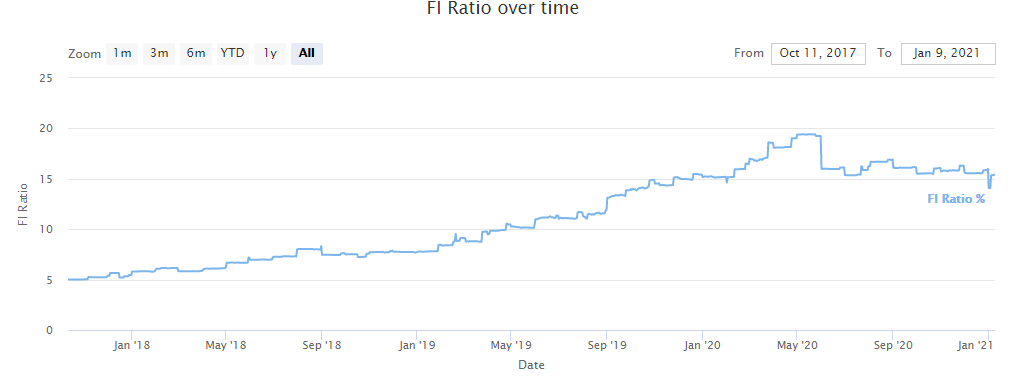

For reference, here is our FI Ratio since we started our journey to Financial Independence.

It does not look that great! But we are still working on improving it, and it should now start to grow over time.

Improvements for the calculation

My calculations are not entirely correct.

First, I am still working on increasing our savings rate. My current income is also higher than it was in most of the twelve last months. Finally, I am also working on improving my expenses. The last twelve months include some pretty bad months. So, hopefully, our future income should be higher, and our future expenses should be lower.

Another important thing is that your expenses in retirement will likely be different from now. For instance, you will pay fewer taxes in retirement than now. But it is quite likely that your health expenses will go up. It is challenging to compute the costs you must pay in retirement.

There is another thing that we have not taken into account. The second pillar and the third pillar can only be taken out at the retirement age. For now, I include them in my net worth. But this money will only be used once I reach the official retirement age.

Also, the first pillar will give you a retirement pension. If you want a really accurate calculation, you must integrate many more factors. It means that from retirement age, some of your retirement expenses will be covered by the first pillar. It would be the same in the United States with social security.

In every case, the FI Ratio remains an estimation. It can be a good estimation if you take care of all the details, but you never know what will happen.

Improving your FI Ratio

Of course, now that you have this metric, it is essential to improve your FI Ratio. You may want to become financially free faster than the current predictions.

Of course, you can increase your net worth to increase your FI ratio. But it is not trivial to improve it. And this is not something that will happen in one day unless you play into the lottery’s terrible odds.

The first thing you should do to improve your FI ratio is to reduce your FI Number. For this, you have to lower your expenses. All your yearly costs get multiplied by 100/SWR. If you plan on using the 4%, all your expenses are multiplied by 25. If you can cut your costs by 1000 USD per year, this is 25’000 USD that you do not need to save!

The second thing you can do to speed up your FI ratio is to improve your income. Increasing your income will not directly increase it. But it will grow faster over the years. Of course, this is only true if you do increase your expenses. Do not fall into the trap of Lifestyle Creep.

Another thing you can do to increase your FI Ratio is to use a larger withdrawal rate. Now, this is dangerous. The higher your withdrawal rate is, the more risks you deplete your net worth in case of a large downturn. But this would decrease your FI number significantly and increase your FI ratio. I would not do that unless I were aware of the risks.

Finally, by increasing your returns on your capital, you will also speed up your FI Ratio. To increase your profits, you generally can take on more risks. Once again, this is dangerous. And it is not easy to get a guaranteed return on income. But this would significantly increase the speed at which your net worth increases.

If you follow some of these ways, you will become Financially Independent faster!

If you want to know how many you need until you can retire, you only need to know your savings rate. You can use the savings rate to estimate how many years you have until retirement.

Notes

Keep in mind that all these numbers are only estimates. Your expenses could go up. Your salary could change. The stock market could crash. Your Financial Independence ratio and the estimated number of years left are useful numbers. But they are not definite.

For instance, I plan to have kids. This will increase my expenses. And my income will probably increase by the time I retire. It should not prevent you from calculating your FI ratio. You should just update your FI number at least once a year instead of using a fixed amount for too long.

Remember that the safe withdrawal rate rule has been created for the US market. You may have to adapt it to your country. And, if you plan to retire early (in your thirties, for instance), this rule will not cover you long enough. So take everything like this with a grain of salt. Every situation is different.

If you want to read more (much more) about safe withdrawal rates, you can read the Ultimate Guide to SWR, by Early Retirement Now. It is excellent.

Is a 100% FI Ratio enough?

By definition, when your FI Ratio reaches 100%, you are Financially Independent. In theory, this means you can quit your job.

In practice, you have to be careful about being exactly at a 100% FI Ratio.

First, if you retire from your job, you will have a lot of time. And filling your time may cost you money. You may visit more museums, for instance. Or you may travel more. It is difficult to estimate how much you will spend in retirement.

Secondly, you will have no margin of safety. This means that if something bad happens and costs you a lot of money, it could be bad. I am not talking about small emergencies but large ones. Your emergency fund should cover small emergencies.

Finally, at 100%, you are still subject to bad timing. If you retire at the peak of a bull market with a 100% FI Ratio, you are in a risky situation. The market may crash 40% the year after. And your portfolio is unlikely to recover from that. On the other hand, a 100% FI Ratio at the bottom of a bear market would be much better.

Since we cannot time the market, it is better to get some margin of safety with our FI Ratio. The exact goal would probably depend on people’s risk tolerance. For me, 110% would probably be fine.

The Passive FI Ratio

Now, what we have seen is the definition of Financial Independence that I use. But there is another definition of the FI Ratio used by some people.

Some people do not want to withdraw from their principal in retirement. That means they will focus on passive income. It can be an income from their principal, such as dividends or interests from a bank account. Some people focus, especially on P2P Lending. You can also include social security or other retirement benefits into your passive income.

For some people, this can also be income from a blog. However, that last one is not passive (contrary to what some people would like you to think)! But it sure can help you retire.

For these people, we can compute a Passive FI Ratio. It is simply the ratio between your passive income and current annual expenses. For instance, if you have a passive income of 10’000 CHF and yearly expenses of 40’000 CHF, your current Passive FI Ratio is 25%.

I do not focus on passive income. But I think this ratio is quite interesting. It is not necessary to aim for a Passive FI Ratio of 100%. Both ratios can play together. If you have a Passive FI Ratio of about 50%, this can reduce your FI Number consequently since you will need a smaller net worth. If you can get a guaranteed income of 1000 CHF per month in retirement, this will significantly reduce your yearly expenses!

For instance, one of the bloggers using Passive FI Ratio’s definition is Joe Udo at retireby40. He focuses a lot on his passive income.

FAQ

What is the FI Ratio?

This ratio tells how far you are from reaching Financial Independence (FI). It is a percentage of where you are compared to your goal.

How to compute your FI Ratio?

You can obtain your FI Ratio by dividing your current net worth by your FI Number.

Conclusion

Your Financial Independence (FI) Ratio will tell you exactly where you are on your road to FI.

The FI Ratio is a straightforward metric that can help you track your progress. It is a great metric that should probably be part of your financial metrics. But there are plenty of other personal finance metrics.

Even though it may not be vital, it is an interesting metric to follow. It will give you an overall idea of where you are in your quest for financial independence. If you graph it against time, you will also see if it grows faster over time or not.

In the future, I will follow the evolution of my FI Ratio. But for now, I will not pay too much attention to it. I will focus on decreasing my expenses and increasing my savings rate. I am not worried about the large number of estimated years before retirement. Indeed, I am just getting started on my journey. And I know I can reduce my spending and increase my income. It will help me reach FI faster.

If you liked this FI Ratio Metric, read about More Personal Finance Metrics.

By the way, you do not have to do the math yourself. You can use my Retirement Calculator.

What is your Financial Independence (FI) Ratio? What do you think of this metric?

More reading

How often should you withdraw money from your portfolio?

Withdrawal frequency. Should you withdraw monthly or yearly in retirement? We test different strategies to see which one minimizes risk and cash drag.

Why do so many software engineers choose FIRE?

Tech and FIRE. Explore why so many programmers and software engineers are drawn to the Financial Independence, Retire Early movement.

What is a failsafe withdrawal rate?

Is any rate safe? We explore if a "failsafe" withdrawal rate exists for early retirement and how to protect your portfolio from total failure.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi – a couple of questions: 1) is the Running Savings Rate a net (post-tax) or gross (pre-tax); 2) do you include bonus in the calculation or not? and 3) how do you calculate Yearly savings? Shouldn’t it be 39,465 (133,200 – 93,735)?

Hi Z

1) It’s post-tax

2) Yes, it’s included in the running income

3) Good question. I had to look at the code because it’s weird. I am computing the yearly savings based on the running income and running savings rate. But since the running savings rate is an average, it does not produce income – expenses for savings. This choice is highly debatable, and I think now that the running savings in my app should be the total savings rate over those 12 months rather than the average, which is more skewed.

Hi Baptiste,

Does your SWR consider a retirement now or in 18 years? Or, in other words, would you feel comfortable enough to FIRE if you would reach your target Net Worth today?

I ask because I do this a little bit differently (I am probably over complicating it), but I consider an increasing SWR, i.e. if I retire now I would be more conservative (e.g. 3% SWR) than in 18 years (e.g 3.6% SWR).

I am also thinking that in early retirement I cannot immediately tap into my retirement accounts (and that cashing them out will be taxed, even if at a lower rate). How do you account for that?

Hi

Oh, that’s a good point. I currently consider my SWR to be safe by retiring at 50 and living at most 50 extra years (being optimistic).

If I were retiring today, I would redo my simulations to make sure my portfolios can sustain at least 60 years and I would likely be slightly more conservative.

For the taxes on retirement accounts, I plan to account for them in the final years with a percent tax (like accounting for only 95% of their value). Keeping them until retirement does not bother me since the bulk of my FI net worth will be in my portfolio.

Thanks for your response! That makes sense.

I agree once the time comes close more calculations are needed before pulling the trigger, including whether the non-retirement accounts are sufficient to bridge the gap until retirement age, but unfortunately we are still a long way from it :-)

Did you consider that if you become FIRE then you will be considered as a professional investor because your income will be only from the stock exchange (dividends, capital gains, interests etc.) and there will be an extra tax?

Because of this, Switzerland is not the best country to get FIRE.

Hi THomas

I did consider that but I don’t think this will be the case. One part of my income will be from dividends, so I should be good to have enough income to not draw too much from stocks and be potentially classified as professional investor.

I talk about this here:

* The truth about Capital Gains and Taxes in Switzerland

* Distributing Funds vs Accumulating Funds: Which is better?