First Pillar: All you need to know to retire in Switzerland

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

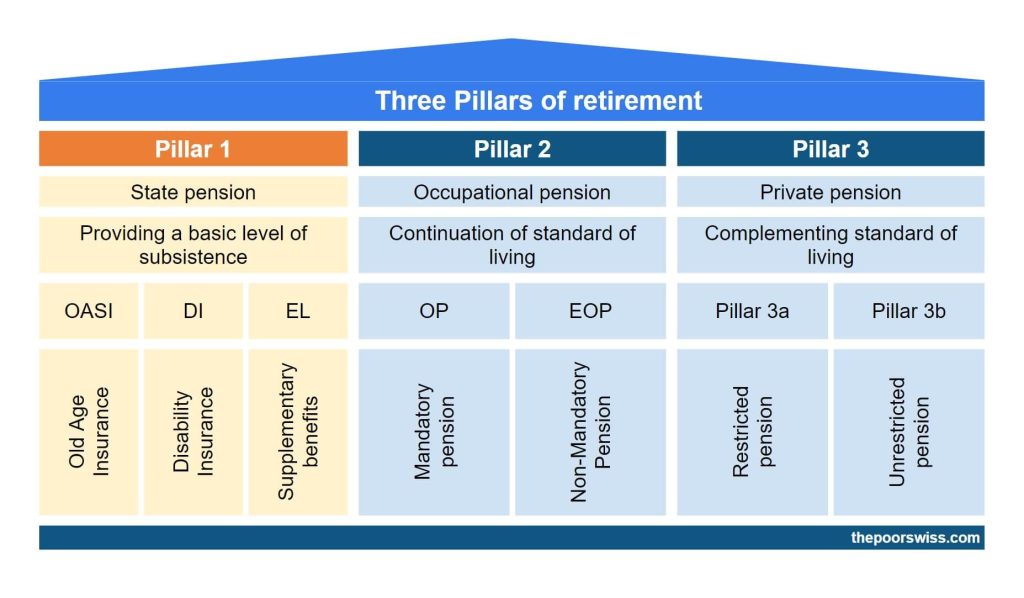

The retirement system of Switzerland is a system with three pillars. Each pillar is paid differently and will cover different needs. The first pillar is the state pension.

If you are working in Switzerland, it is essential to know these three pillars. Even if you do not plan to retire in Switzerland, understanding how they work will help you plan your retirement.

This article discusses the first pillar in detail. It should contain everything you need to know about the first pillar to retire in Switzerland.

I use the French acronyms in this article. But the figure at the top of this article has the acronyms in English as well.

Introduction to The three pillars

Here are the three pillars of retirement in Switzerland:

- The first pillar (state pension). This first pillar will grant a pension to every Swiss employee after retirement. It is a state pension between 1175 CHF and 2350 CHF per month if you have worked every year since you were 20. Each employee in Switzerland finances this pillar.

- The second pillar (occupational pension). The second pillar will grant a pension to every Swiss retired employee. You will only receive money from this pension if you work and have an annual salary of more than 21150 CHF (currently). You will pay for this pillar with a deduction of your salary each month.

- The third pillar (private pension). The third pillar is a personal saving system. While the first two pillars are mandatory, the third pillar is optional. You can only save a certain amount each year into the third pillar. The essential part is that the third pillar has tax advantages.

Every pillar will improve your quality of life after retirement. The first pillar is only there to cover your basic needs. With the first pillar, the second pillar should cover from 75% to 80% (on average) of your last salary. And the third pillar, which is optional, should help you cover the missing part of the second pillar.

The first pillar

The first pillar is a state pension.

Every Swiss person registered with this global insurance will receive this pension. The Assurance-Vieillesse et Survivants (AVS) insurance is what makes the first pillar. This insurance covers the basic needs of every person in Switzerland after retirement.

This pension is paid by every Swiss employee (and independent people) after 17 years old through a deduction from their salary.

You pay for the AVS insurance and two other insurances: the insurance for invalids (AI) and when you serve in the army (APG). Each month, 8.7% of your raw salary goes to the AVS, 1.4% to the AI insurance, and 0.45% to the APG insurance, for a total of 10.55%.

Employees pay half of the full contribution, and the employer pays the other half. Therefore, you should see a deduction of 5.275% each month for these three insurances together.

These contributions can change every year. For instance, in 2020, the contribution for AVS insurance (the first pillar) increased from 8.4% to 8.7%.

For completeness’ sake, we also need to talk about Unemployment Insurance. It is not directly related to the retirement system. But you will also pay for it monthly. You will also pay 1.1% of your salary for it. If you get more than 148,200 CHF per year, you will pay 0.5% of the part higher than this number. This insurance will cover the needs, for some time, of people who lose their jobs and cannot find a new one.

Unemployed people also have to pay this fee. People who do not have a salary have to pay the minimum fee of 478 CHF per year, starting from their 20-year birthday. An exception is if their spouse pays at least twice the minimum fee (956 CHF) per year. For instance, I have enough salary that my wife does not have to pay AVS.

If you have a significant net worth, the minimum fee will increase. For instance, with a one million net worth, you must pay 2054.60 CHF (as of 2020) as a minimum each year. There are exceptions if paying this fee would reduce your living standards too much. You can use this calculator to see how much the tax is for unemployed people.

How much will I get from the first pillar?

The full pension is a minimum of 1260 CHF per month, up to a maximum of 2520 CHF per month. How much you get depends on several factors:

- How much income you got during your working life.

- The number of years you have contributed to the first pillar.

- Contributions for caring for children or relatives.

First, the amount of your salary determines the amount of the full pension. The minimum pension is up to a salary of 14,100 CHF per year. To reach the maximum pension, you must have an average annual salary of 88,200 CHF. You can see in the previous image how that scales. Between those two milestones, the full pension scales linearly.

The second factor is how many years you paid the AVS insurance. To get the full pension, a man should pay for 44 years and a woman for 43. If you have missing years, you will receive a pension prorated for the years you have paid the insurance.

The third factor is when you care for children below the age of 16 or care for relatives. During the years when you are in this situation, you cannot have contribution gaps. Even if you did not pay during this time because you had no income, it would not count as a gap in your contributions.

The first pillar and marriage

Importantly, a married couple cannot receive two full pensions, only 150% of a full pension (3525 CHF per month).

Fortunately, the minimum is still 200% of the minimum pension (2350 CHF monthly). It is unfair to married couples with both a large income. But some things are unfair to married couples in Switzerland (taxes, for instance).

This first pillar of pension also covers the case of widowed people. If the dead spouse were eligible for a pension, the surviving spouse would receive this pension.

Several things need to be considered in the case of divorce. First, each spouse will get a pension based on half the combined income during the marriage. The care contribution credits are also divided in half. If one of the divorced spouses dies without retirement, the other spouse will get 80% of the deceased pension.

The first pillar and early retirement

The first pillar only covers official retirement, at 65 for both men and women.

If you want to retire earlier, you can ask for a pension one or two years in advance. However, this means you will get a reduced pension of 6.8% per year of advance. You can also take it later, as seen in the next section.

If you want to retire earlier than two years before the official retirement age, you will only be eligible for the pension when you reach retirement age. Before that, you must rely on your net worth to cover your expenses.

Official calculator

If you want an official estimation, there is a cool official tool for estimating your pension.

Remember that this is only an estimation, not an official number. But in my experience, it seems pretty accurate. It can compute the results based on your income and marital status.

If you have not worked in Switzerland your entire life, you can enter your income for each year and get a good picture of what you will get based on the holes in contributions.

The first pillar and leaving Switzerland

If you leave Switzerland, you will usually still be entitled to the pension. So, once you reach retirement age, you will receive your pension.

If you are a Swiss citizen, or a citizen of the European Union (or of an EFTA member) or a citizen of a country with which Switzerland has a social security agreement, then you will receive a pension abroad.

On the other hand, if you are a citizen of a country with which Switzerland has not concluded a social security agreement, then you will not receive a pension when leaving Switzerland. Under some conditions, if you are a citizen of Australia, Brazil, China, India, Philippines, South Korea, Tunisia or Uruguay, you may also not be entitled to a pension.

If you lose the right to the first pillar pension while abroad, you are generally entitled to reimbursements of your first pillar contributions. The amount reimbursed may reach at most 8.7% of your total gross income. It means you can get back both your contributions (at most 4.35%) and your employer’s (at most 4.35%).

As of September 2024, here are the countries with a social security agreement with Switzerland:

- All member states of the European Union and EFTA

- Albania

- Australia

- Bosnia and Herzegovina

- Brazil

- Canada/Quebec

- Chile

- China Tunisia

- India

- Israel

- Japan

- Kosovo

- Montenegro

- North Macedonia

- Philippines

- San Marino

- Serbia

- South Korea

- Tunisia

- Türkiye

- United Kingdom

- United States

- Uruguay

In any case, it is mandatory to announce that you are leaving the country.

Optimize your first pillar

You cannot do much to optimize your pension from the first pillar. Since it is mandatory, you are already paying for it.

It is essential to avoid any years when you do not pay the AVS insurance. All these years will significantly reduce the amount you will receive. If you go to a foreign country for a long time, you should continue to pay the minimum each year to avoid penalties.

Even living abroad after retirement, you should receive your pension. But the country where you retire should have a social security agreement with Switzerland.

When you are studying, you should also pay the minimum to avoid any missing years. If you missed a year of contribution, you could pay for it in the next five years. After five years, you cannot compensate for it anymore.

If you are moving to Switzerland, you will not be able to fill your gaps, unfortunately. These gaps can be filled if you are in Switzerland and then living abroad for a few years, for instance.

If you want to increase your pension, the biggest thing you can do is increase your salary. Although it may not be evident, you should probably try to increase your income regardless of the pension.

There is one other thing you can do to increase your pension. You can delay your first pillar pension. If you delay the pension by one year, you will get a pension increase by 5.2%. It increases to 10.8% for two years, 17.1% for three years, 24% for four years, and 31.5% after five years (maximum delay). It is a gamble on your life expectancy. If you expect to live until 100 years old and can afford to delay the pension, you should delay it by five years.

Accounting

I do not account for the first pillar in my net worth. There are several reasons for this.

- You do not only pay this insurance for yourself. It is global social insurance. The people with more salary will pay more for people with a smaller salary.

- Then, since I plan to retire in Switzerland, I will never touch the capital, only the pension.

- I am not entirely confident it will still exist once I reach the official retirement age.

However, I should account for this in my computation of my Financial Independence (FI) ratio. Since it is a guaranteed pension after retirement age, you will need less money stashed for your needs. But it is a bit weird to account for it, and I still have not done it. Indeed, it is only starting at the official retirement age. And your retirement may begin early.

Another argument for not accounting for the first pillar is that it may not be solvent once I reach retirement age. It is a somewhat pessimistic point of view. But the population is rapidly aging, and Swiss couples have fewer and fewer children. I prefer to ignore it for now in my strategy, and I will rethink it when I am closer to retirement. If you are optimistic about it or close to retirement, you should account for the first pillar in your retirement strategy.

FAQ

What is the first pillar in Switzerland?

The first pillar of retirement in Switzerland is a state pension. Every person in Switzerland is eligible for this state pension.

How much will I receive from the first pillar?

This will depend on your salary. The minimum is 1175 CHF per month, and the maximum is 2350 CHF per month. The minimum is up to a salary of 14’100 CHF per year, and the maximum is 84’600 CHF per year.

How can I optimize my first pillar?

You cannot do much to optimize for your first pillar. You need to make sure you pay for it every year. Having holes in your contribution will lower the money you receive.

Conclusion

The first pillar is the first part of the Swiss retirement system. It should cover the basic needs of every retired Swiss person. Employees pay it from their salary, and unemployed people pay a minimal amount each year. The pension is quite low (2350 CHF per month at most).

Most people cannot live only on this pension after retirement. The other two pillars are here to complete your needs during retirement.

Next, I cover the second pillar, which is an occupational pension that should make up a significant part of your retirement income.

What about you? Do you have any tips regarding the first pillar? Do you have any questions about the first pillar?

More reading

Second Pillar: All you need to know to retire in Switzerland

Maximize your Second Pillar (LPP). Discover how occupational pensions work in Switzerland and how to optimize your contributions for a better retirement.

Should you take a pension or a lump sum from your second pillar in Switzerland?

The big decision. Annuity or Capital? We analyze whether you should take your Second Pillar as a monthly pension or a lump sum cash withdrawal.

Third Pillar: All you need to know to retire in Switzerland

Save on taxes today. Learn everything about the Third Pillar (3a) in Switzerland and how to choose the best account to grow your retirement savings.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Title: Keeping AHV Contributions While Working Abroad (4 Years in China) – Possible and How Much?

Hi everyone,

I’m Swiss and have a question about AHV contributions when living abroad.

My situation:

– Swiss citizen

– Worked in Switzerland for the last 7 years

– Salary was high enough to count for the maximum AHV contribution each year

– Planning to move to China for 4 years (will work there, no income in Switzerland)

Then I will likely move back to Switzerland and continue working here

I read on this forum that if you leave Switzerland and live abroad for a few years, it may be possible to continue contributing to AHV so you don’t lose any contribution years. That’s exactly what I want to do so my future 1st pillar pension is not reduced.

My questions:

1. Can I continue contributing to AHV while living/working in China so that these 4 years still count as full contribution years?

2. If yes, how much would I need to pay per year to maintain the “maximum contribution level”?

– Is there a formula or way to calculate the amount?

– Does it depend on my past salary in Switzerland, my salary in China, or some other parameters?

– Or is it simply a fixed amount for voluntary AHV contributions abroad?

3. How does the payment work in practice?

– Do I need to register before leaving Switzerland?

– Do I pay directly to a Swiss AHV account each year?

My goal is to make sure I don’t lose anything from my AHV pension because of these 4 years abroad.

If anyone has experience with voluntary AHV contributions outside the EU/EFTA (especially China), I’d really appreciate your tips!

Thanks!

Hi,

Next time, this kind of long-form question would be better suited for the forum.

Normally, you can pay back contributions in the last 5 years when you come back to Switzerland. But I don’t think you can continue paying while you are abroad. I would recommend asking your local AHV office to be sure.

But I do not know about the details of the payment (i.e. how much you will pay after 4 years).

Hi Baptiste – thanks a lot for all the info you wrote. They are all super useful. I already implement your suggestion on investment :) I have a question, when I do not get any income at all (not employed and no property being rented out) and solely depends on using my assets until I reach retirement age, how much AHV do I have to still pay until retirement age?

I read everyone is obliged to pay in AHV until retirement age. Thks a million!!!!

Hi Rosie

You are welcome, I am glad this is useful.

If you do not have any income, you will pay AHV based on your wealth. This ranges from 530 CHF per year (below 350k) to 26’500 per year if you have 8.950m. If you have a wealth of 1 million, you will pay 2014 CHF per year. You can check the table here (page 6): https://www.ahv-iv.ch/p/2.03.f

ps. I should add that my salary was around CHF 230K per annum.

Thanks for all your work on this web site, very helpful! Here is a question about a different angle on “optimizing” AVS payouts. Assume that I’m seven years older than my wife, who is still working in Switzerland. We’ve been working in Switzerland for 22 years. I’m 65 and have “delayed” (“ajourné”) taking my AVS. I was thinking of delaying until I’m 70 to take AVS. However, I was wondering whether if when my wife retires, assume in five years, that our overall payout from AVS would be reduced. So the question is, should I continue to delay payments from AVS for four more years to take advantage of the increased payout, or start taking it now to maximize lifetime payout, assuming both myself and my wife live to say 90? Her salary is around CHF 160K right now. Thank you for any insight!

Hi CT,

I am not entirely sure I understand it entirely. Why would it be reduced when you wife retires? It’s true that for married couples, the maximum pension is only 150% of the total, is that what you are talking about? If you are delaying to increase the pension, I don’t know how exactly this will be computed.

It’s a difficult decision to delay it because it depends on your life expectancy. If you have great health and good family history, it may be worth it financially. But I am not sure most people would do it.

Thanks! What I meant by “reduced” is that the total monthly payout would be “capped” at 1.5 times my payout. So the question is whether I should collect now for four years so that when we add hers and we’re capped, my waiting four more years doesn’t help us…. Hope that makes more sense. I guess I can make a simulation with the actual figures. So far, I feel pretty healthy :-) At least you helped me think through the issues!

Indeed, if you both get a full pension, delaying the pension is less interesting for both of you since it only applies to 75% of the full pension. I never thought of that before.