Vested benefits accounts: All you need to know!

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Vested benefits accounts play an essential role in the retirement system of Switzerland. You can transfer your pension fund money to a vested benefits account when you are unemployed.

You then keep your vested benefits until your retirement or until you work again.

These accounts are not well known, and there are many interesting things to learn about them. So, this article will go in-depth into everything you should know about vested benefits.

What is a vested benefits account?

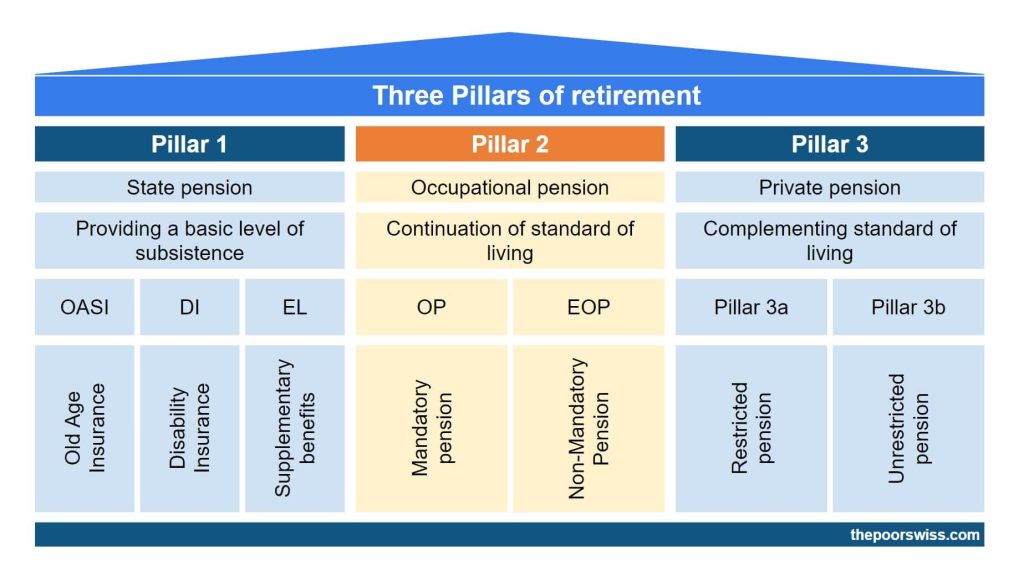

A vested benefits account is a particular account where you can keep your pension fund money when you are not working. It is part of the second pillar system.

When you are working, you are enrolled in a pension fund. But if you leave your company and do not join another, you will not be part of a pension fund. In that case, you must move your pension fund capital to a vested benefits account.

An exception to that is that if you are becoming unemployed, you could choose to still contribute yourself to the pension fund. In this case, you would generally go to the Substitute Occupational Benefit Institution. But this is a rare case.

This also applies if you move out of the pension fund system while still working, for instance, if you are moving abroad.

Just like a third pillar account must belong to a third pillar foundation, a vested benefits account belongs to a vested benefits foundation. These foundations are heavily regulated and must follow strict rules.

While not everybody can profit from vested benefits, they remain an important part of the retirement system. This article will cover everything there is to know about vested benefits.

Vested benefits and retirement

The usual way to use vested benefits is at retirement. It makes sense since it is part of the second pillar.

You can withdraw your vested benefits at retirement age or up to five years before normal retirement.

Furthermore, it is currently possible to delay the withdrawal up to five years after retirement. However, this will not be possible after January 2024 unless you are still working.

With the second pillar, you can usually choose between a pension and a lump sum. However, you cannot draw a pension from a vested benefits account. You will need to withdraw the capital as a lump sum.

A few vested benefits foundations allow you to draw a pension, but this is extremely rare.

We must note that you cannot partially withdraw vested benefits accounts. At retirement, you have to withdraw it entirely.

Optimize for taxes

There is one thing hardly any people know: you can have two vested benefits accounts. Two accounts allow you to optimize your taxes when withdrawing from them.

You will pay a withdrawal tax when you withdraw your vested benefits. This tax is lower than the taxes you have saved using the second pillar, but it is not negligible either. Therefore, it is essential to try to optimize these taxes.

Withdrawal taxes are using a progressive system. This means you will pay a different tax rate on each tranche of your withdrawal. For instance, a progressive tax system may look like this (entirely made up for the example):

- 2% on the first 10’000 CHF

- 3% on the next 20’000 CHF

- 4% on the next 20 ‘000 CHF

- 5% on the rest

So, if you withdraw 60’000 CHF, you will pay 2100 CHF in taxes. So, higher amounts are taxed at higher rates.

Imagine you can withdraw 30’000 CHF the first year and 30’000 CHF the second. In that case, you will pay 1600 CHF in taxes. You have saved 500 CHF on your taxes, more than 25%!

Therefore, you should always try to have two vested benefits accounts. When you leave a pension fund, you can tell them to split your second pillar and send it to two vested benefits accounts.

It is also important to note that you cannot have two accounts with the same foundation. You need to have accounts with different vested benefits foundations.

Vested benefits and employment

As discussed before, you use a vested benefits account when you are not part of a pension fund, namely unemployed.

But it is important to know that when you are employed again in Switzerland, you must transfer your vested benefits to a pension fund. This is a rule of the retirement system.

Many people will say it is a grey area because pension funds cannot verify your vested benefits assets. And indeed, many people do not transfer their retirement benefits when working again. But this is against the rules. Therefore, I would not recommend doing it. I recommend following the rule and transferring your vested benefits to a pension fund.

Vested benefits and death

In the event of death, the vested benefits go to the beneficiaries. The foundation determines the beneficiaries based on four different groups.

In most cases, the vested benefits will go to the members of the first group: the surviving spouse or partner, the surviving divorced spouse or partner (under some conditions), and dependent children.

If there is nobody in the first group, this will go down to group 2, group 3, and then group 4. If all the groups are empty, the vested benefits will return to the state.

In most cases, you will not have to do anything, but if you are living with an unregistered life partner, you should declare it to the foundation to ensure they can inherit (if you wish to).

If you want to learn all the details, read my article about retirement benefits and death.

Vested benefits and divorce

Finally, we cover the event of divorce.

If you get divorced or your registered same-sex partnership is dissolved, each spouse or partner is entitled to half of the vested benefits of the other party earned during the period of marriage or partnership. This is done regardless of your marital property regime.

Only the part earned during the official relationship will be shared, not the entire sum. And both parties will see their earned vested benefits cut in half and transferred to the other person.

If only one person worked, this could significantly reduce their retirement benefits. This is one reason divorce makes couples much poorer.

Withdraw vested benefits without retiring

There are several other ways to withdraw your vested benefits without retiring.

The most used way is to use your vested benefits assets to finance a mortgage. You can use your retirement benefits to cover 10% of the property value.

You can also use your vested benefits to pay off an existing mortgage. This is not something really interesting, but that is an option nonetheless.

If you become self-employed, you can use your vested benefits to start your own company.

Finally, if you leave Switzerland permanently, you can get some or all of your assets. If you leave for a country outside the EU/EFTA countries, you can withdraw the entire vested benefits. If you leave for a country part of the EU/EFTA, you will only be able to withdraw the extra-mandatory benefits.

The Substitute Occupational Benefit Institution

Many people have vested benefits assets in the Substitute Occupational Benefit Institution and may not even know it.

Indeed, many people forget to transfer their second pillar benefits when they switch employers or stop working. In that case, pension funds must transfer the assets automatically to the Substitute Occupational Benefit Institution.

How to choose vested benefits accounts?

When transferring your pension fund money to a vested benefits account, you must choose a vested benefits account. And as with every financial service, there are many options out there. And unfortunately, many of these options are pretty bad. So, how do we choose vested benefits accounts?

If you are close to withdrawing the money, your choice is simple. You only need to find a provider that allows you to keep the money in cash and charges as low fees (ideally zero) as possible.

However, if you are not close to retirement, you want to look for a provider that lets you invest your money.

There are several critical criteria for choosing a vested benefits provider.

First, you must look at the fees. You do not want to lose your hard-earned money in fees to a greedy banking institution. They usually charge a management fee as a percentage of your assets. This can eat your returns very quickly. And be careful that many companies are not transparent, and you have to look hard to find the total fees, not only the first fees they present.

Then, you need to look at the investment strategy of the company. You should prefer companies that offer passive funds. Ideally, you want to be able to invest as much as possible in stocks.

Finally, you should look at the domicile of the vested benefits foundation. This domicile is essential if you withdraw your vested benefits while abroad. Indeed, if you are abroad, the domicile of the foundation will determine which canton will tax you. And there are some major differences in withdrawal taxes between Swiss cantons.

You can also look at other small things like:

- Customization of portfolio

- Foreign exposure limits

- Sustainability options

The best vested benefits account

Finpension Vested Benefits is the best account in Switzerland.

Use the FEYKV5 code to get 25 CHF in your account!

- Invest 99% in stocks

Currently, the best vested benefits provider is Finpension. This service offers many advantages:

- You can invest up to 99% in stocks

- You only pay a 0.49% yearly fee (the lowest available!)

- Finpension is only using passive funds

- You can customize your portfolio in detail

- You can heavily invest in foreign currency instruments (without hedging)

- Excellent tax domicile for withdrawing abroad

- They have two foundations, ideal for splitting your assets

Finpension is significantly better than other alternatives if you want to invest aggressively. If I had to use a vested benefits account, I would use finpension.

You can read my review of Finpension vested benefits if you want further information.

However, keep in mind that if you look for a short term vested benefits account, Finpension may not be the best. Indeed, for the long-term, you want to invest it aggressively. But in the short term, you want to be more careful. In general, for the short term, you will want a good interest rate on cash and avoid exit fees.

Conclusion

There are many important notions regarding vested benefits. If you are serious about the retirement system of Switzerland, you should learn about this critical subject too.

Choosing a good account is essential if you use vested benefits. Currently, finpension is the best option for aggressive investors.

If you would like to learn more about the second pillar and vested benefits, you should read our article about what you should do with your second pillar when you stop working.

What about you? Are you using a vested benefits account? Did I miss anything about these accounts?

More reading

Free by 40 in Switzerland – Book Review

Free By 40 in Switzerland is a book by Marc Pittet about Financial Independence, in Switzerland: Learn to spend less, earn more and invest!

Your retirement benefits after your death

Your retirement benefits are important for your retirement, but do you know what happens if you die before? Lets' find out!

From Early Retiree to Investment Coach: An interview with Charlene Cong

Charlene Cong retired early in Switzerland and started an investment coach career. Learn from her story and profit from her advice.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hello Baptiste, thank you for the interesting topics.

I have questions regarding having one vested account (been unemployed) and getting divorced. In this case, can I split the amount I receive from my ex-partner into 2 new vested accounts? Having 3 vested accounts as total?

I am also not understanding the benefits of splitting into 2 vested accounts while being unemployed, if we need to return both to the new pension fund starting to work for a new employer? Maybe only benefits when becoming a self-employed?

Hi Stacy

I think you should be able to split in this case, yes.

If you are unemployed, it’s indeed only interesting if you are not working again. However, one could be in a situation without finding a job again. In this case, it can make sense to preemptively split since we can’t do it later.

Hello Baptiste,

I red somewhere, that only mandatory part of vested benefits can be transferred to a new employers pension fund. Is that correct? Thank you.

Hi Isa

I don’t think that’s correct. You are supposed to transfer the entire amount to your new employer.

Hi Baptiste,

Thank you for your helpful article. I am not sure I fully understand at which point I should split the funds from the 2nd pillar into two vested benefits accounts. Should this be done right prior to retirement with the last pension fund?

I still have years to retirement and am between jobs at the moment. My pillar 2a funds are still with the pension fund of my previous employer for 6 months. I assume it does not make sense to split them into two vested benefit accounts, if I have to roll them into a pension fund of a new employer in the foreseeable future, right? Or, am I missing something?

Hi Heln

Splitting should be done when you know you will not work again (so not possible for everybody).

If you are going to work again and transfer the vested benefits anyway to a new employer, splitting is not interesting.

I have an article where I detail multiple cases: Your second pillar when you stop working in Switzerland

Hi Baptiste, thank you for the blog.

I would like to clear my understanding. I left my job last month. For someone, who is planning to start a new job in 2-3 months, I don’t think it makes sense to move the money to a vested benefits account. Am I correct?

AXA (they held my pillar 2) informed me that they will hold my funds for 6 months before moving it into their “the Substitute Occupational Benefit Institution” as required by law.

Worst case scenario, if I don’t get a job in a timely manner, I can move the funds into a vested benefits account in the 5th or 6th month.

Am I missing something crucial?

Regards

Hi Anshuk

You are not missing anything. For 2-3 months, it does not matter. You could move it but you should definitely not invest it.

You are correct, in the worst case, you can then move it to another vested benefits (or even keep it temporarily in the substitute foundation).

Hello – great post! Thank you!

I recently came across Liberty, based in Canton Schwyz. They seem to have an even lower cost basis.

See here for the cost schedule:

https://www.liberty.ch/asset/e10223c1-0e49-4d61-9501-4a3164fa5aa6/libfz_reglement_kosten_en.pdf.

And see here for their investment options, we seems to include a very large list of basic low cost ETFs.

https://www.compare-invest.ch/en/2nd-pillar-investment-solutions/self-management-investment-solutions/multi-fund-invest/list/investment/list/pid///245.html

Does anyone have any experience here? The cost and service offering appears better than FinPension

Thanks for your feedback!

Hi Anant

I don’t think they are cheaper, but they have decent pricing indeed. Looking into the cost schedule, it would cost 0.45% per year for the index fund solution. On top of that, you would pay the product costs and at least the stamp duty (and potentially VAT, which is unclear on their cost schedule). Without knowing the portfolio, the products are difficult to estimate. Looking at your list, we can probably assume 0.2% at least, so a total cost of 0.60% which is quite decent but not the best.

Other than that, I have no experience with them.

Hi!

You mention that using the funds for paying a mortgage is not very interesting. Would you mind perhaps expanding a bit on this opinion & rationale?

Thanks for the insights!

Hi Laura

Sure, I should have explained that better. If you have great vested benefits like finpension, you are getting nice returns. So it does not make much sense to withdraw money to put that into a mortgage because what you will gain is the interest rate of the loan which is generally significantly lower than the returns on a good vested benefits.

If you have a banking vested benefits, it may make more sense, but you also have to keep in mind that you are reducing what you will have in retirement.

Hi Baptiste, Thanks for this useful article. I currently have 2 vested benefits accounts as you recommend spread equally between 2 different foundations. At least one of them has been charging very high fees (TER1.15%) and the performance has been poor. ButI will most likely retire in 2 years or so.

What would you advise? Stick with the pain for 2 more years or find a cheaper fund? Any particular funds you would suggest at the moment? Thanks

Hi Nuticel,

Good question. Since you are retiring in two years, an option would be to simply convert it in cash, if you can in this foundation. That way, you will not have to pay any more fees in the next two years. And since you have to liquidate anyway in 2 years, it is a short-term investment now.

The other solution would be to move to another foundation like Finpension Vested Benefits. However, this is not ideal with your time-frame.

Hi Baptiste, your blog is so helpful, thanks. I have a question regarding vested accounts to park my pension when between jobs. As I intend to park the money for a shorter period than the recommended for the investing option, I’m looking at Clientis Bank offering 1.5% and freeMe offering 1%, both without fees and reasonable early withdrawal conditions. Are these good options in your opinion or am I missing something? Thanks so much for the feedback!

Hi Cecilia

I do not know any of them in detail. I had heard of Clientis before. They are a group of 14 banks, founded in 2002 already and look legit. FreeME looks much more recent and I had never heard of it. Apparently, an online account by the Glarner Kantonalbank. They both look safe, but I have no real opinion of either.

Hello, can you contribute “extra” funds into a vested benefits accounts the same way you can with a company-linked 2nd pillar account? Thanks.

No, you can only do voluntary contributions to a pension fund.