Save taxes with staggered withdrawals in 2026

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Most cantons use a progressive tax system for taxing retirement withdrawals. These withdrawals are coming from the second and third pillars.

This progressive tax system makes it more interesting to stagger your withdrawal over multiple years to save on taxes. This technique is called staggered withdrawals.

I want to discuss this in detail in this article and how you can use staggered withdrawals to save taxes on your second and third pillars.

Withdrawal taxes

When you withdraw your retirement assets, you must pay a tax on this withdrawal. This applies to assets from the second and third pillars.

These taxes are based on the amount you are withdrawing. As usual in Switzerland, you will pay taxes at three levels:

- The canton

- The municipality

- The country

For this, most cantons use a progressive tax system. Such a system means you pay a lower percentage for smaller amounts than larger ones.

The country (federal taxes) also has a progressive tax system, with the percentage increasing with the amounts. The municipality is a percentage of the cantonal taxes. So, if the cantonal tax is progressive, the municipality tax will also be progressive.

Here is the example of the canton of Fribourg:

- 1% for the first 50’000 CHF

- 2% for the next 50’000 CHF

- 3% for the next 50’000 CHF

- 4% for the next 50’000 CHF

- 5% for any amount higher

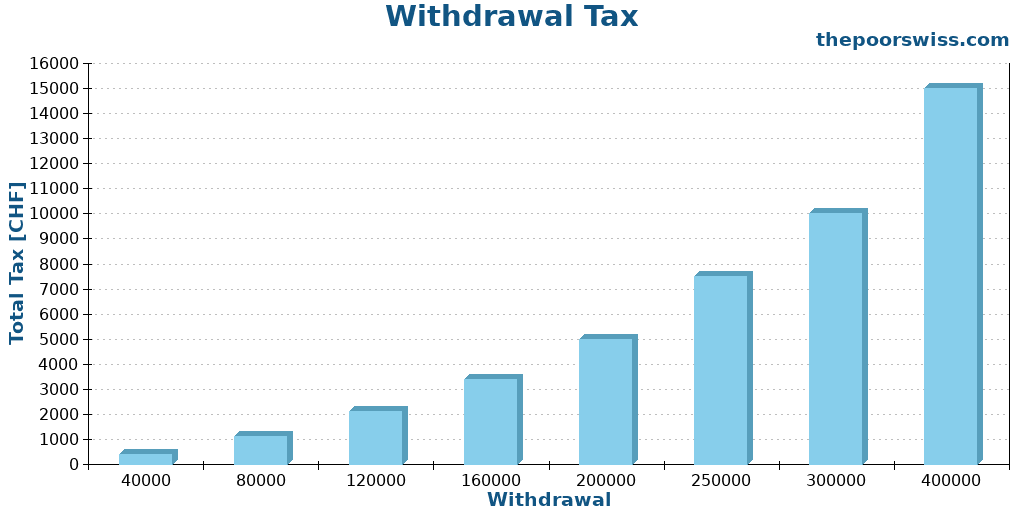

With this system, we can run a few examples:

- If you withdraw 40’000 CHF, you will pay 400 CHF.

- If you withdraw 80’000 CHF, you will pay 1100 CHF.

- If you withdraw 120’000 CHF, you will pay 2100 CHF.

- If you withdraw 160’000 CHF, you will pay 3400 CHF.

Here are more examples in a graph:

So, we can see that this is not a linear system. What is very important to realize is that withdrawing multiple times small amounts is cheaper than withdrawing a large amount. If you withdraw 4 times 40’000 CHF, you will pay 1600 CHF in taxes. But if you withdraw 160’000 CHF at once, you will pay 3400 CHF. This is more than double!

Since the amounts are calculated yearly, you will need to stagger your withdrawals over multiple years.

Some cantons are worse, and some cantons are better than Fribourg. Since this can vary for each canton and municipality, I cannot show all results here. However, since the federal tax is progressive, it will always be important to stagger your withdrawals.

Staggered withdrawals

So, now that we know that we need to withdraw over multiple years, how can we achieve it? First, we need to see the rules for withdrawing the second and third pillars.

For the second pillar, if you have a pension fund, you must withdraw it at retirement age. If you have a vested benefits account, you can withdraw it up to 5 years before retirement and up to 5 years after. Up to 2030, you do not need proof of employment to withdraw after retirement. However, since 2030, you will need proof of employment.

We can withdraw our third pillar five years before the official retirement age. And we can postpone the withdrawal up to five years after the official retirement age. However, postponing the third pillar withdrawal requires proof of employment. This means that we will need to postpone retirement as well.

So, in a perfect world, you could spread your withdrawal over 11 years. However, this requires working after the retirement age since you need proof of employment. Therefore, in most cases, we should consider that most people can stagger their withdrawals over 6 years.

Theoretically, you could also use advance withdrawal before buying a house or starting a company. However, this is not applicable in most cases. Regardless, this could be another way of staggering withdrawals.

So, let’s see how we can increase the number of withdrawals for the second and third pillars.

Get five third pillars

Unfortunately, you cannot do a partial withdrawal of a third pillar. You must withdraw an account all at once. So, you need multiple accounts if you want to stagger your withdrawals.

Fortunately, you can open multiple accounts. You should open five third pillar accounts. You may wonder why five since we can generally spread over 6 years. The reason is that most people also have a pension fund or a vested benefits account to withdraw, taking a year.

If you are married, taxes will be computed together. If you are the same age, you will have to withdraw following the same pattern. But if you have some age difference, this means you will be able to withdraw over more years. So, make sure you take that into account. In 2032, we will switch to individual taxation, so they will not be added together.

A good thing about this system is that you can open multiple accounts with the same provider. A good third pillar provider will allow you to create up to five accounts. If you need a good third pillar, you can look at the best third pillar for Switzerland.

And unfortunately, you cannot split a third pillar account. So, this is something you must plan.

Get two vested benefits accounts

If you are employed until your withdrawal, you must withdraw from your pension fund at once (unless you have two employers and two pension funds, but this is rare).

However, if you are not employed, you could have several vested benefits accounts. For this, when leaving your pension fund, you could ask them to send the money to two different vested benefits foundations. It is important that you need two different foundations. You cannot have multiple accounts with the same foundation.

However, some providers have two foundations. So, you can have two accounts at the same provider if it has two foundations. If you do not know where to start, look at the best vested benefits account.

Once again, you cannot split a vested benefits account, so you must plan.

How much can you save?

While you could, in theory, split your withdrawals up to 11 years, most people will only achieve up to 6 years since most people will work until the reference retirement age and will not be able to postpone withdrawals since they will not be employed.

So, in theory, you could split up your withdrawals in equal chunks of 1/6 of the total. However, this ignores that most people will have significantly more in their second pillar than in their third pillar. Since the contribution percentage increases over time, the contributions to the second pillar will quickly outpace the contribution to the third.

On average, we can imagine that most people will have double the money in their second than in their third pillar. This is an average, of course, but it makes sense.

So, if you have 200’000 CHF in your second pillar and 100’000 CHF in your third pillar, you will still have to do a single 200’000 CHF withdrawal and five 20’000 CHF smaller withdrawals. This will still result in very nice tax savings, but significantly less than if you could split the second pillar.

In that case, you would pay 5600 CHF in cantonal taxes instead of 10’000 CHF. This is a very good improvement in favor of staggered withdrawals.

If you split your second pillar withdrawals, you could optimize it further by withdrawing four times 25’000 CHF and twice 100’000 CHF. With that extra step, you would only pay 3’250 CHF in cantonal taxes. In this case, staggering your withdrawals divides your taxes by three.

From that, we can draw a few conclusions:

- Staggering your withdrawals is very effective!

- In practice, most people will only be able to split their withdrawals over six years.

- The strategy becomes more and more effective the more money you have.

- Splitting vested benefits can be very effective if you can achieve that.

Is it legal?

One question you may ask yourselves is whether this is legal. Currently, it is legal, but there are some limitations.

Many people feel this is tax evasion and want to pass new laws to limit it. Already, with the OASI 21 reform, staggered vested benefits are more difficult than before.

Also, some cantons are stricter than others. For instance, the canton of Vaud only allows staggering for 3 years, and the canton of Neuchatel only allows 2. After these points, they will consider this tax evasion.

We will likely see stronger regulations to avoid this in the future. However, we should not stop trying to have 5 third pillars and, ideally, two vested benefits accounts. Since this is currently possible, we should still try to do it. And even if it is not possible in the future, you can always withdraw multiple accounts per year to abide by the law.

The important point is that since you cannot split them later, it is important to be prepared. You never know in which canton you will retire. So it is better to be prepared. Having multiple accounts is never an issue. Staggering over too many years can be an issue in some cantons.

Conclusion

Staggering your retirement withdrawals can save you a significant amount of taxes. However, you must plan for it since you cannot split a third pillar or a vested benefits account. Therefore, you should always consider this when managing your retirement assets.

I recommend anybody open five third pillar accounts and try to balance them over time. You can simply send the money into the account with the lowest amount over time, which will be more or less balanced.

If you have the opportunity, it is also a good idea to split your pension fund into two vested benefits accounts before the official retirement age. But I realize this is an optimization that is only doable for people retiring before the reference retirement age and able to live without these funds for some years.

I plan to reach ten third pillar accounts (5 for me and 5 for my wife) by the age of retirement, more or less balanced. If my plan to retire early works, I will split my pension fund into two vested benefits accounts. Then, we will spread all these accounts for 6 years.

What about you? Are you planning to stagger your withdrawals?

More reading

What is a 1e pension plan (pillar 1e)?

The 1e advantage. Learn about 1e pension plans for high earners in Switzerland, which allow you to choose your own investment strategy.

Interview of Marc Pittet Author of Free by 40, in Switzerland

Marc Pittet is the author of the future book Free by 40, in Switzerland. Today he is answering my questions about the book.

Free by 40 in Switzerland – Book Review

Free By 40 in Switzerland is a book by Marc Pittet about Financial Independence, in Switzerland: Learn to spend less, earn more and invest!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Great article as usual.

I am not sure about the mechanics of opening 2 different vested benefit accounts in 2 different foundations.

For simplicity: I have 100k in PensionKasse “PK”.

When losing my job, I want to move 50k to Vested Benefit foundation “A”, and 50k to “B”.

How can I instruct my current PensionKasse to make split payments? They only have formularies for “full transfer”…

(I am checking with them in parallel, but maybe you already know more on this practical aspects)

It was my case as well. I had so many questions, and the old fashioned pension kasse only had a form for full transfer.

At the end of the day, everything went really smooth and happened in a couple of days.

I just wrote on the form “transfer 20% to VB1 and the rest 80% to VB2”.

FYI, both the mandatory and extra mandatory part keep the same % in the transfer. Meaning if e.g. you have 25% of your current pension as mandatory, the 20 and 80% part, will each have 25% of mandatory and 75% of extra mandatory.

Not sure if you can instruct otherwise, but I have memories that the “old-fashioned” pension kasse said also the mandatory and non-mandatory part can be decided… I was just not interested.

Another info: depending on the receiving vested benefit account, it took a week or so, to show the split of mandatory and extra mandatory correctly on the app. The other VB account I chose instead was showing it already after 1 business day.

Hi M.

That’s a good question. You don’t necessarily have to follow their templates, you can write your own letter. You could also edit the letter to add the mention that you want to split

Otherwise, you can contact them and find a solution with them.

Hi Baptiste,

Thanks again for your articles.

I am planning to leave Switzerland (to Italy) in about 3-5 years, and possibly try to early retire.

If laws and regulations don‘t change, I plan to withdraw my accounts over 10-15 years, starting with my 2x Accounts 3a (over 3-4 years), then moving on to my 2x VBAs, withdrawing the extra mandatory part from each, over 4-6 years, and then the mandatory part from each, later on, when I will be close to, or already in my retirement age.

Meanwhile I hope my accounts will grow since they are fully invested in stocks, and I might enjoy compound growth with no capital gain.

I hope this plan will work, although I know many variables are involved. I will have backup plans ready in case.

Anyone sees any problem with this plan?

Thanks

Alan

Hi Alan, people here tend to obsess over staggered withdrawal tax savings. But each withdrawal is a hassle. Filling out forms, obtaining documents in foreign countries, mailing them to Swiss providers, waiting for approvals, paying high fees. Doing this every year for 15 years sounds like a nightmare. It may be easier to withdraw all at once, just pay the higher tax and be done with it.

I would not retire to Italy because of the bureaucracy and capital gains tax. If you have significant capital, better choose a country without capital gains tax, such as Cyprus, Malta, Slovakia or Dubai. Keeping a Swiss residence while spending most of the year abroad may also be a good option.

In any case, with a Schengen passport, you are free to spend spring and autumn in Italy, winter in Spain, summer up north. You can live in nice places for months at a time without entering difficult bureaucracies and creating tax obligations.

Hi Alan

On paper, your plan sounds good.

But I am not sure you will be able to withdraw separately the mandatory and extra-mandatory part. You should make sure your pension fund allows that. And I would be surprised if this was possible with VBAs.

If you have the VBAs with the same provider, I would also not be surprised if they force you to withdraw both accounts if you announce you are leaving Switzerland definitely. So you may be limited by your providers.

Hi Baptiste, I am confused why you say “I am not sure you will be able to withdraw separately the mandatory and extra-mandatory part.”. Everywhere (I guess including your blog) it is mentioned that upon emigration you can at the very least withdraw your extra-mandatory part, hence I do not see reasons why they would not allow you that… while keeping the mandatory part until retirement age. I will check with VIAC and Finpension, but, is there any reason I missed you state it would be difficult to withdraw separately?

Thanks again for your content!

A pension fund has the information about both.

But, if you have already transferred your assets to a vested benefits, I am not sure if it’s possible to then withdraw only a part, I think the vested benefits provider may not even know the split, but I may be wrong here.

My thinking is that it’s not a choice to split both and withdraw at separate time. If you leave Switzerland definitely, there are some countries where you can withdraw everything and others where you will be limited to the extra-mandatory part.