How many years until you can retire?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

If you plan to retire early, it is important to know when you can retire. We have already covered a lot of simple math about financial independence. But we have not yet covered how to know how long it will take you to retire (or to become financially independent).

In this article, we cover the simple math behind financial independence and find out how long you will need before you can retire early!

And since we are on the subject, we also see how you can retire earlier!

How to retire early?

We review first how you can retire early. You will be able to retire when you are financially independent.

Retiring at the standard retirement age, you can rely on your country’s social security system. But when you are retiring early, most countries will not help you. In this case, you need to rely on your net worth to cover your expenses.

You could accumulate the cash for each of the years you plan to be retired. If you want to retire at 40, you could plan for 50 years of retirement. So, you need to accumulate 50 years of expenses.

Unfortunately, there are two important issues with this simple approach. First, it requires you to accumulate a considerable amount of cash. And second, with inflation, your net worth is unlikely to sustain you for as long as you planned.

There is a better alternative: retire early with your investments. This strategy is at the heart of the Financial Independence and Retire Early (FIRE) movement. And it is based on The Trinity Study.

The idea is simple: by withdrawing only 4% of your principal every year and investing everything in the stock market, you should be able to sustain your portfolio for a very long period.

Following the 4% rule, you must accumulate 25 times your yearly expenses. This total is called your FI Number. Once you reach your FI number, you can retire.

That math behind retirement

So, now that we know how to retire, how can we know when we can retire? The math is the same if you want to know how many years you have until you are financially independent.

With that, we can compute the years you will need based on the compound interest formula.

The number of years is LOG((R*FIN/Savings)+1)/LOG(1+R) where:

- R is your yearly returns on investments

- FIN is your FI Number

- Savings is your yearly savings

Now, we can simplify this. Your FI Number and your Savings are highly correlated, and we can simplify this only to have your savings rate (SR). So, the number of years is LOG(((1/WR)*R*((1/SR)-1))+1)/LOG(1+R), where we add:

- WR as your withdrawal rate

- SR as your savings rate

There is something powerful here! Your income and expenses are not very important. What is essential is your savings rate! A person with a 50’000 CHF yearly salary and a savings rate of 50% will be able to retire at the same as a person with a 100’000 CHF salary and the same savings rate!

This formula shows the importance of your savings rate! If you want to retire earlier, you must optimize your savings rate. Do not worry too much about the math. You do not need to work it out yourself. I am here for that!

You will find many examples in this article. And if you want more, I have created a Years To Retirement Calculator, for you!

How many years to retirement?

But enough with the math, we start with two assumptions:

- Your yearly returns on investment are 5%

- Your withdrawal rate is 4%

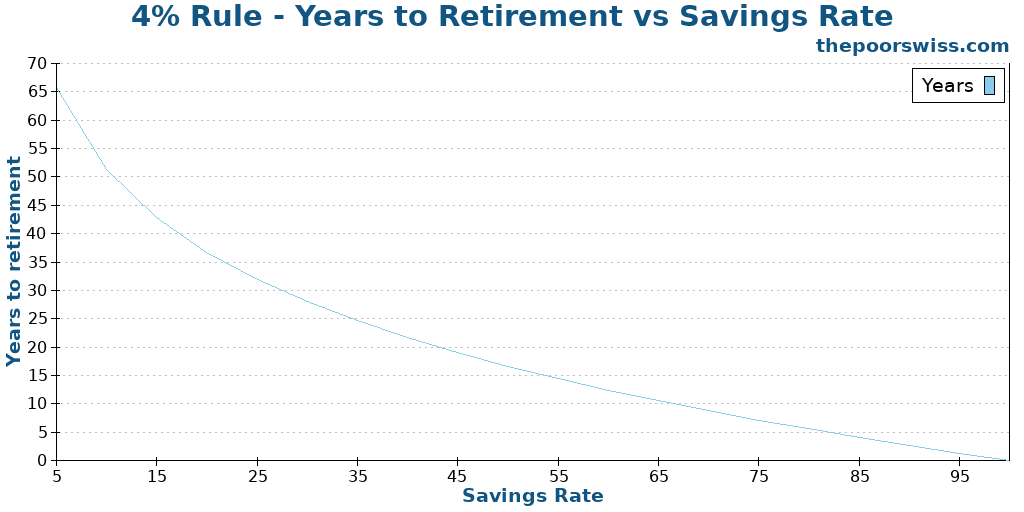

Based on these assumptions and our formula, we can draw the following graph:

We can see from this graph that increasing your savings can make a huge difference in when you can retire. If you can increase your savings rate by 10%, you could save many years.

You can use this graph in two ways:

- You can find how long you need to retire with your current savings rate.

- You can find how much savings rate you need to retire when you want.

Here are some number of years to retirement for some savings rate:

| Savings Rate | Years To Retirement |

|---|---|

| 10% | 51.35 |

| 20% | 36.72 |

| 30% | 27.98 |

| 40% | 21.64 |

| 50% | 16.62 |

| 60% | 12.42 |

| 70% | 8.79 |

| 80% | 5.57 |

| 90% | 2.67 |

| 100% | 0.00 |

If you save 20% of your income, you will need 36 years to retire. But if you increase your savings rate by 10%, you will only need 27 years! By saving 10% more of your income, you are saving nine years.

The higher your savings rate is, the fewer years you need to retire. But it does not mean that it is not worth improving. If you save 50% of your income, you will need 16 years to retire. If you push to a 60% savings rate, you only need 12 years. By doing so, you are saving 25% of your time for retirement.

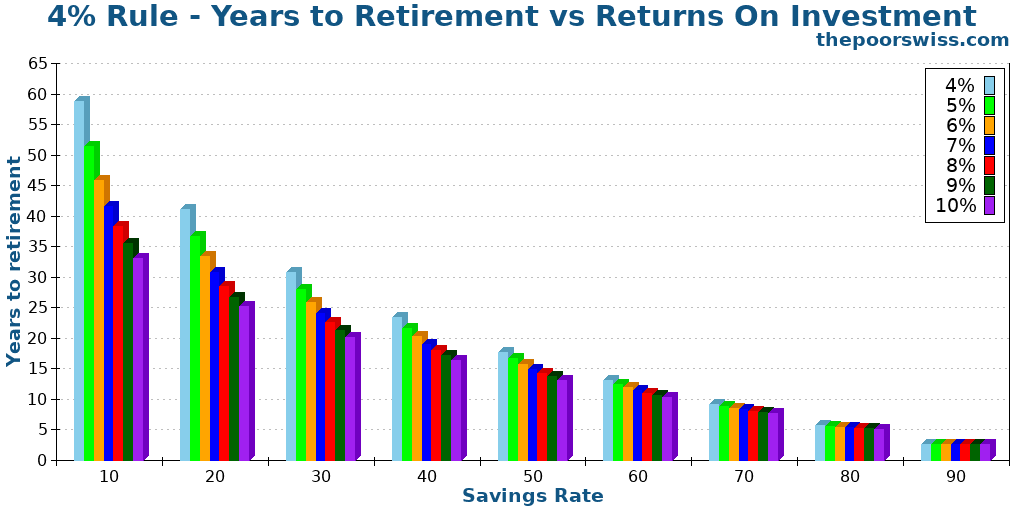

Retire earlier – More returns

Now, ideally, everybody would want to retire earlier. The first way for that is to increase the returns on your investment.

Here is the same kind of graph but with different yearly returns after inflation:

For low savings rates, increasing the annual returns makes a very significant difference. You can easily retire many years earlier.

Now, the problem is getting consistent returns. Getting more than 5% returns after inflation on average is not easy. Depending on the stock market you invest in, you may get 7% returns after inflation. But you are very unlikely to get 12%. That is unless you take a large amount of risk.

In general, you should only take the appropriate risk for your situation. Not everybody needs or wants the same amount of risk. To retire earlier, I would be cautious about taking too many risks.

You need to find an investment portfolio that suits your ability to take risks and keep at it. Even though it will reduce the number of years you need, you should avoid taking more risks just for that reason.

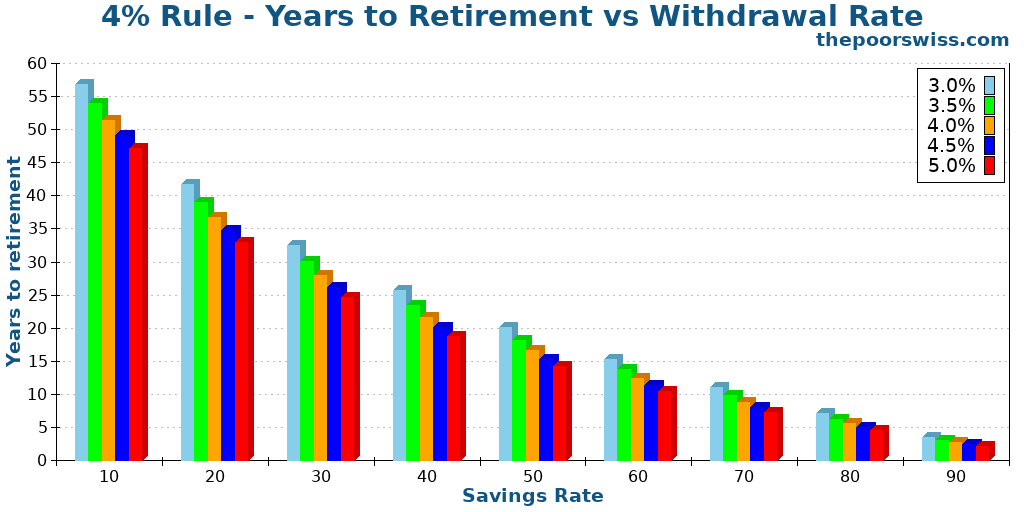

Retire earlier – Higher withdrawal rate

Another way to retire earlier is to increase your withdrawal rate. By being able to withdraw more money every year, you need to accumulate less money. Now, this is more of an exercise because, in practice, anything higher than 4% is unlikely to last for very long periods.

So, here is what happens with different withdrawal rates (again, assuming 5% yearly returns):

Your withdrawal rate will make a significant difference in how many years you need to work before retiring.

For instance, at a 20% savings rate, there is an eight years difference between a 3% withdrawal rate and a 5% withdrawal rate. At a 50% savings rate, there is a six years difference. This difference is significant.

Now, as I said, this is a thought exercise more than practical advice. Indeed, the risk difference between a 3% withdrawal rate and a 5% is enormous. A 3% withdrawal rate is very conservative. But a 5% withdrawal rate is hazardous. Except for short periods, a 5% withdrawal rate is unlikely to work.

Nevertheless, it is essential to realize the impact of withdrawal rates on the number of years before you can retire.

For more information on withdrawal rates, you should check out the recent results from the Trinity Study.

Retire earlier – Better savings rate

The first two ways to retire earlier were to take on more risks. But you can also retire earlier by increasing your savings rate. This fact should be clear from the first graph already.

Now, we can see some more practical advice to reduce the years to your retirement. For this, you will have to increase your savings.

There are two ways to increase your savings rate:

- Reduce your expenses

- Increase your income

The first, reducing your expenses, is more potent. Indeed, reducing your expenses has a double effect: increasing your monthly savings and reducing your target FI Number. But reducing your expenses has a limit. You cannot practically cut down your costs to zero, especially in a country like Switzerland.

While it is less effective mathematically, increasing your income is also very potent. And it has higher limits than reducing your expenses. If you grow your income a lot, with your own business, for instance, it could become straightforward to retire early.

And obviously, you can also work on the two fronts and do both. For more information, I have an article about whether you should reduce your expenses or increase your income.

Savings Rate – Reduce your expenses

The easier way to increase your savings rate and hence reduce the years to your retirement is to reduce your expenses.

Here are some examples of how to cut your budget:

- Cook more at home and avoid eating out.

- Cut down unnecessary recurring expenses like newspaper subscriptions you do not read or TV subscriptions you do not use.

- Buy your food in a cheaper shop.

- Review all your insurance coverage for optimization.

- Cut your investing and banking fees.

- Cut down on your travel.

For example, we assume you are spending 75,000 per year on an income of 100,000 per year. Over a year, you are spending 5000 CHF on eating out. If you stop eating out, you will save 30% instead of 25%. By doing so, you will be able to retire four years earlier.

Of course, you do not have to stop eating out, but you could cut it in half and save two years. Ultimately, it is always a balance between how much you want something and how much you want to retire early.

There are many ways to reduce your expenses. You can get creative and cut down a lot of them. Some people even start living in a trailer to reduce their living and travel expenses.

Savings Rate – Increase your income

The second way to increase your savings rate is to increase your income. Doing so will also reduce the number of years to retirement.

Here are some ways to increase your income:

- Work hard to get a raise or a promotion.

- Invest in real estate.

- Invest in dividend stocks.

- Start a side hustle.

We can make another example, assuming you are spending 75,000 CHF per year on an income of 100,000 CHF. Now, we also assume you can generate 10,000 CHF extra per year and you are not spending this new income. Your savings rate will increase from 25% to 31.8%. With this change, you are now five years closer to retirement.

Again, you have to be careful about not pushing yourself too much. If you have to work 80 hours a week to generate more income, you will probably not enjoy your time before retirement. So, once again, it is a matter of balance.

When you increase your income, you have to be careful about not spending too much of that raise.

Calculator

To make it easy for you, we wrote a calculator that can compute how long you have until you are financially free.

Conclusion

By now, you should realize the importance of your savings rate if you want to retire early. Your savings rate is more important than your income or your expenses. And it is the same thing if you would like to become financially independent.

We can directly see this fact in the different experiments for this article. As long as you increase your savings rate, you will reduce the years to retirement. We can simplify the formula for the years to retirement to base it on the savings rate only.

The best way to retire earlier is to improve your savings rate. For this, you can either reduce your expenses or increase your income. In practice, you should try to do both. Many people neglect income and focus only on reducing expenses. But both fronts are essential.

But do not forget to enjoy your time before retirement. Too many people only focus on the goal of retiring early and are living a miserable life on the path to financial independence. Being FI will not entirely change your life.

As you can see, the math is relatively simple. Retiring early is simple, but is not easy at all. It takes a lot of dedication and work to reach financial independence.

To read more about financial independence, you can read about the multiple reasons to become Financially Independent.

When do you plan to retire?

More reading

Should you contribute to your third pillar in 2026?

Save taxes now. Learn why you should maximize your Third Pillar contributions every year and how it boosts your retirement savings.

The Trap of Life Insurance Third Pillar

Avoid this mistake. Learn why mixing life insurance with your Third Pillar is usually a bad idea and costs you thousands in fees.

What is the Substitute Occupational Benefit Institution?

Lost pension? Learn what the Substitute Occupational Benefit Institution is, why your money might be there, and how to move it to a better fund.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

How do you explain your graph: if you save 100% of your income you can retire right away? When you need 25 times your income?

Hi Matt,

Yes, if you save 100% of your income, you can retire now, which is logical, no?

You need 25 times your annual expensees (not income) if you use a 4% withdrawal rate, but I am not sure I get your second question right.

Confused me at first too, I presume the 100% savings rate implicitly means you spent 0% of that, so the equation assumes you survived on 0 Chf that year and projects that forward.

Yes, if you can save everything (100%), you are not spending anything and so you can retire anytime :)

Your calculator doez something wrong in my opinion.

When the witdrawel goes up he gives that the years to retire goes down

Its the other way round

No, it does not :) This is entirely expected.

If you increase your withdrawal rate, it means you increase how much of your capital you can withdraw every year. That means you need less total capital to match your expenses. And as a result, you need fewer years to get that capital.

Hi. So I am prepared to start my FI journey when I get back to the states (I’m currently deployed). I am doing the most reading that I can in my downtime, but I have one glaring question. How to I get my money once I reach FI? Assuming I want to keep a 3%-4% withdrawal rate, I haven’t any posts that say, “Ok you’ve made it, here’s how to keep going forward.”

Hi Zach,

That’s a good point, I should write about what I plan to do once I am actually there.

I have one article about withdrawing in retirement that could be useful. That basically says that you should withdraw as rarely as possible.

Other than that, using dividends first make sense to avoid withdrawals.

Thank you, I’ll give it a read!

Hi,

great article but before I start do rebuild everything with my favorite spreadsheet tool I ask you if you can offer us a template to calculate those numbers?

Thx :)

Hi Simon,

I am afraid I do not have a spreadsheet ready to do these calculations.

I am planning to add a calculator to the website to compute this, but I have not yet done it.

Thanks for stopping by!