The best and worst times to retire early

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Historically, there have been some good times and some bad times to retire early. But what were the best and worst times to retire? I went over my dataset to find out.

But this is only history. What can we do to avoid these times? And what can we do if we retire during a bad time to retire? We will answer these questions in this article.

Best times to retire early

We can start on a positive note. What are the best times to retire?

We can use our historical stock data going back to 1871 to find out. We can rank the times to retire based on the amount of money left at the end of retirement. And then, we can keep only the best 10% out of these.

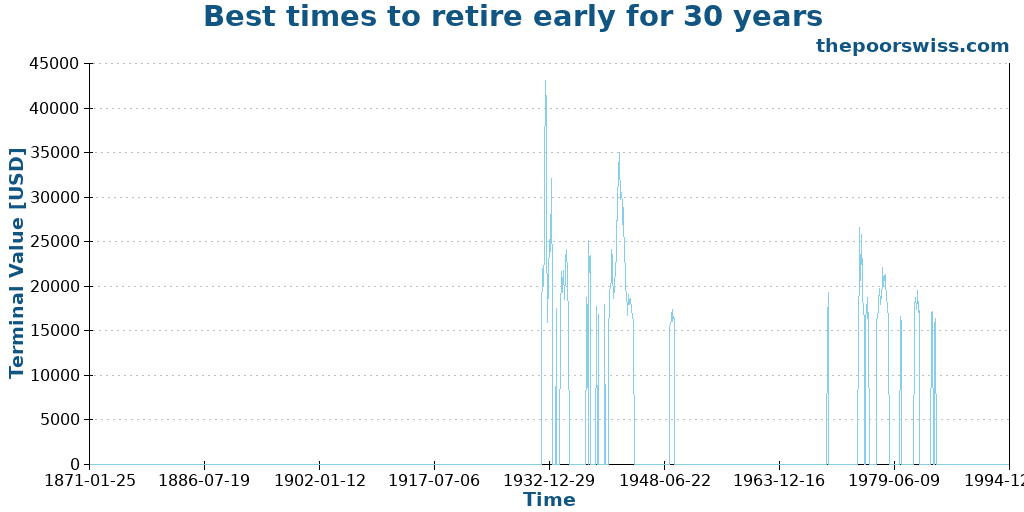

We can first start to look at the best times to retire for 30 years. I will use a 100% US stocks portfolio, US inflation, and a 4% withdrawal rate in this case.

As we can see, there is a concentration of success in the same regions. We can also see that despite using data from 1871 to 2024, all the best times to retire are within the 1930 to 1980 region.

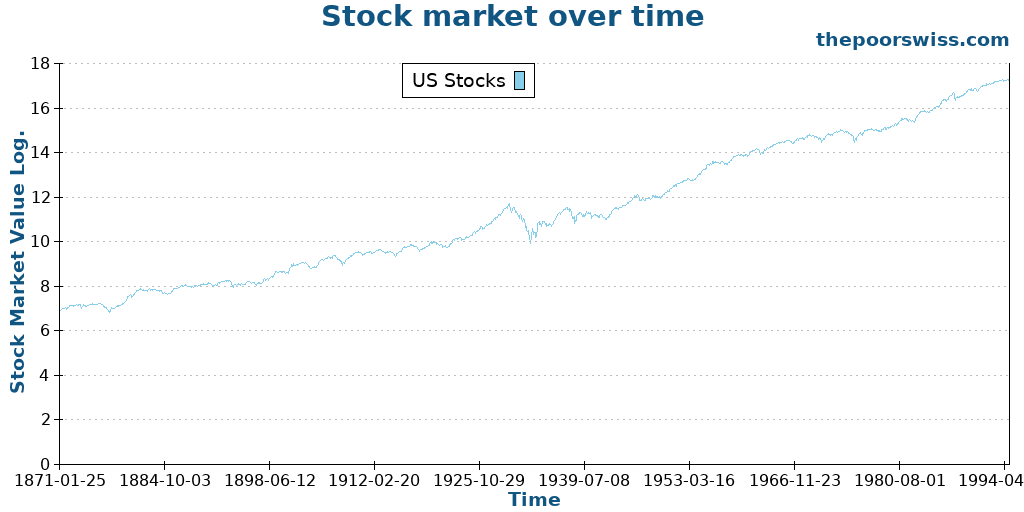

We can try to see if this correlates with anything on the stock market. For that, we show the stock market performance over time for US stocks. To see better, we use a logarithmic scale.

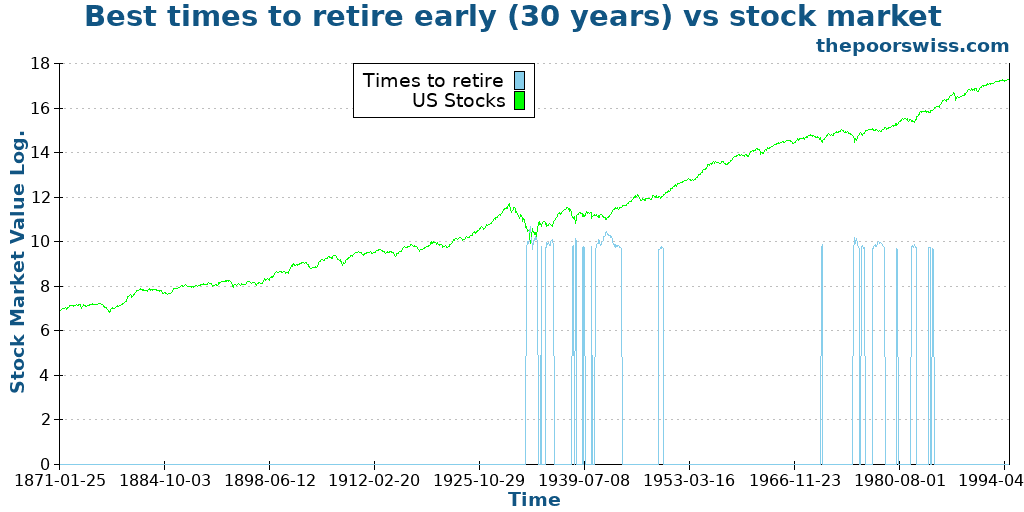

Unfortunately, it is difficult to see well on this graph. So, we should try instead to put both series on the same graph. We now use logarithmic scales for both series so that we can match them together.

On this graph, the results are clearer. We can see that the best times to retire correlate to the worst times in the market. It means it is better to retire early when the market is bad than when the market is good.

When we think a little about it, it makes a lot of sense. Indeed, when the market is bad, we have a higher chance for the market to go higher and therefore push our net worth in the right direction. And when the market is good, we have a higher chance for the market to drop and therefore push us in the wrong direction.

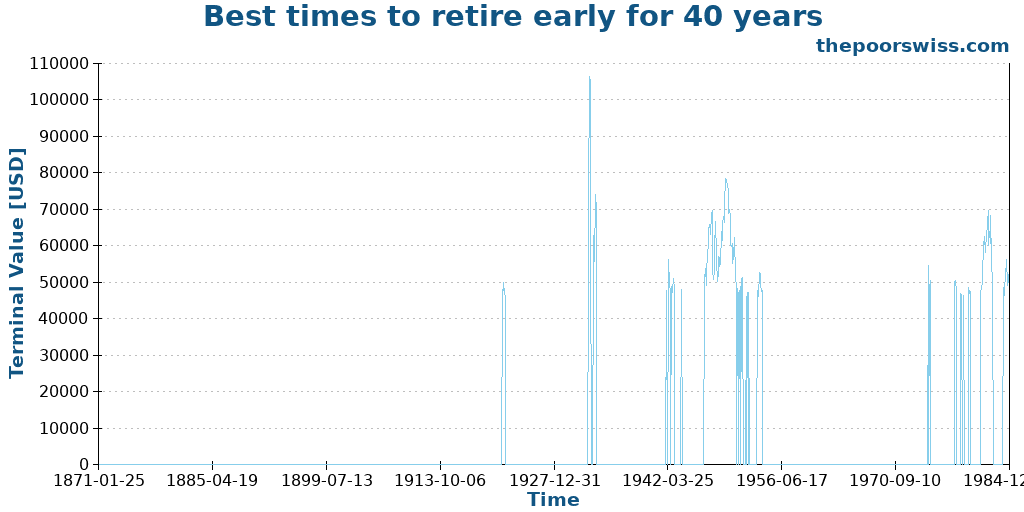

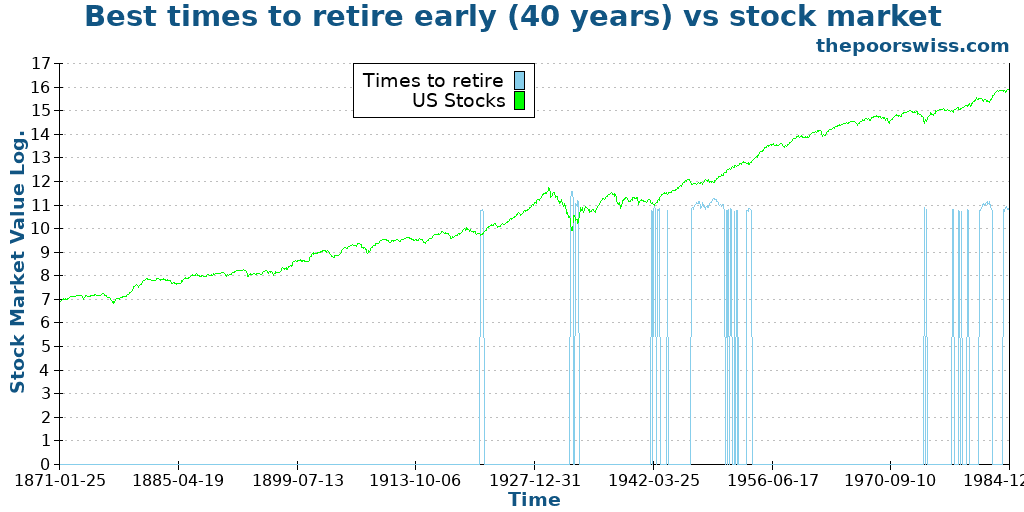

We can check if the same conclusion holds for 40 years of retirement.

It interesting to note that the outcomes are much less concentrated and are more spread around, which is nice. We can see some correlation with the best times to retire early for 30 years as well.

Again, we can put that on the same graph as the stock market to see if we can draw some conclusions.

Once more, the conclusion is similar: it is best to retire when the market is doing poorly.

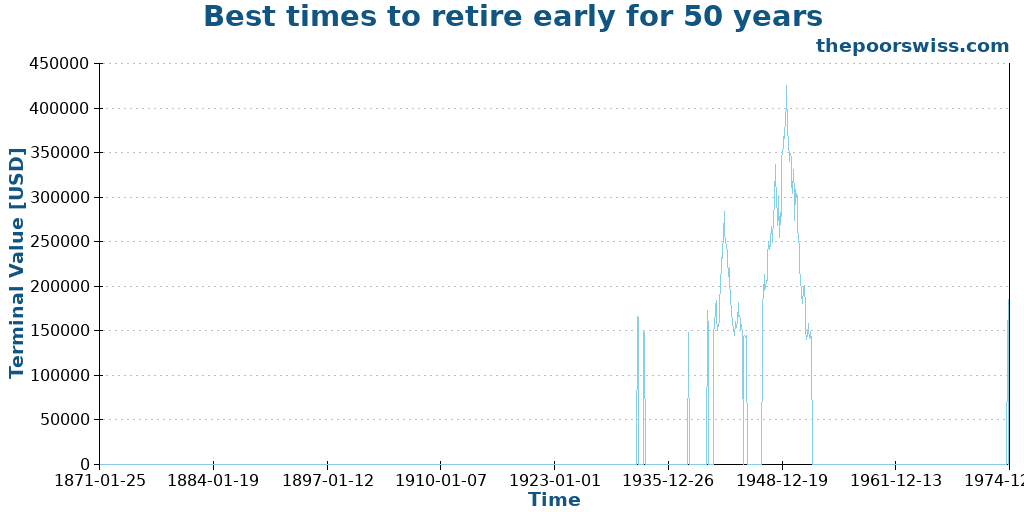

For the sake of completeness, we can do 50 years of retirement as well and see what the best times to retire early are here.

I was expecting more spreading of the outcomes in this case, but this is not the case. One reason is also that there are fewer starting times for 50 years since we do not have historical data past 2025. So, it turns out the best times to retire early for 50 years are very concentrated.

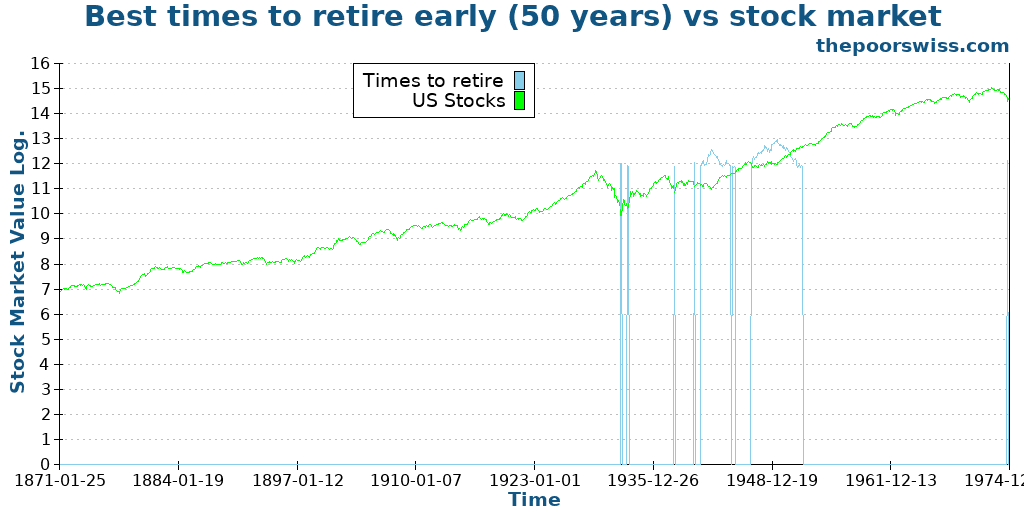

Again, we can see the correlation with the stock market.

It appears that the correlation is less important in this case. We can still see that the best times to retire early are on the drops or plateaus of the stock market. But some of the best periods are also at the beginning of a sharp rise in stock market prices.

So, we have learned that the best times to retire are when the market is doing poorly. This makes sense since at this time our FI net worth will be based on poor stock market valuations. And there is a higher likelihood for the market to go up once we are at a low point in the stock market.

Worst times to retire early

Now, we can run the reverse experiment: what are the worst times to retire early?

Again, we will use our historical stock data from 1871 to 2025. We know the worst times are when we run out of money. So we can try to plot the 10% worst terminal values, which will be mostly zeroes. However, plotting zeros is not ideal. So, instead, I will plot the failures as a large number so that we can visualize the graphs the same as for the best times to retire early.

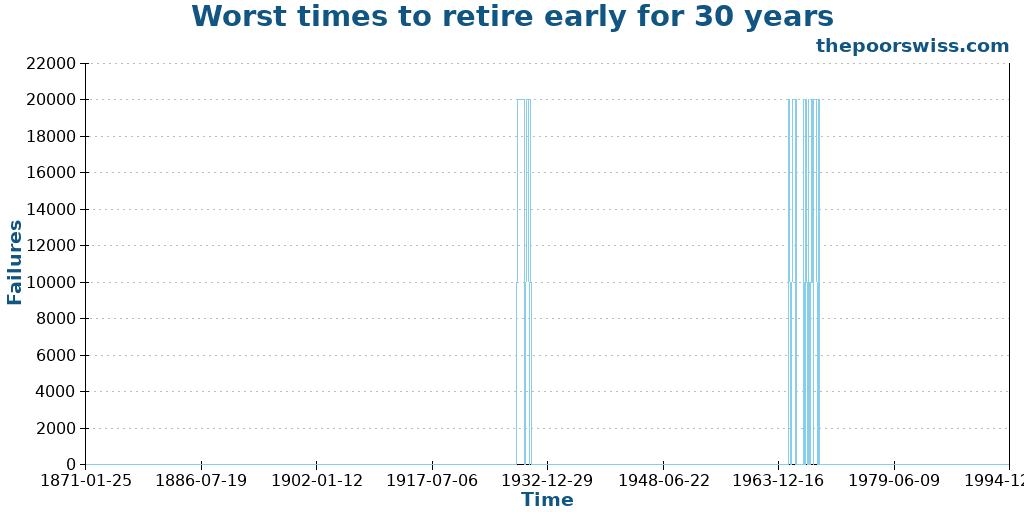

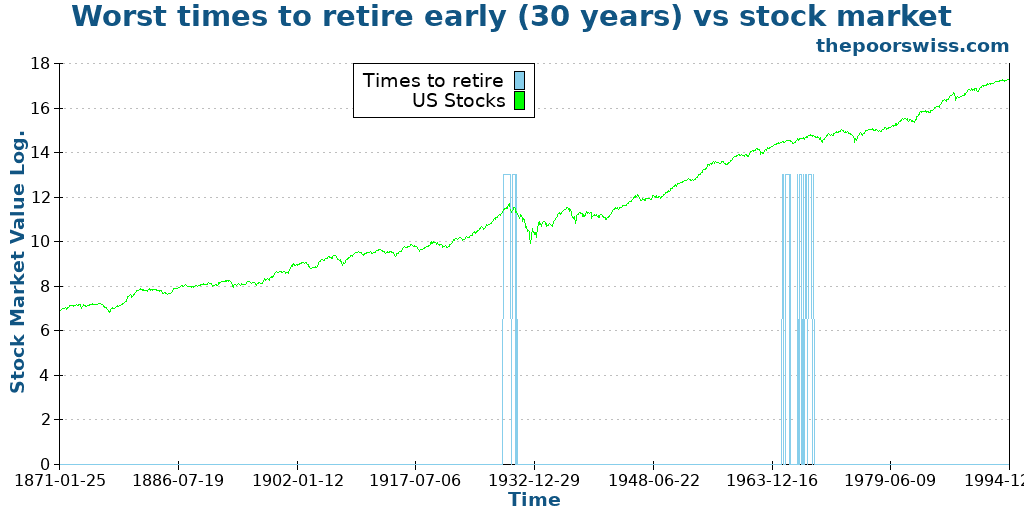

Again, we start with 30 years of retirement.

The data is a bit more concentrated than I expected, but there are also not many failures in the data. We can see a some serious concentrations into two groups. We should now try to understand what makes these periods special.

And for that, we will try to get a correlation with the stock market.

The correlation is quite interesting. We can see that the worst times to retire are when the stock market is very high and about to drop. This makes sense because this is the worst possible scenario. If you just retired and your portfolio drops sharply and still have to withdraw money, you are in for a tough time. This is a bad sequence of returns risk.

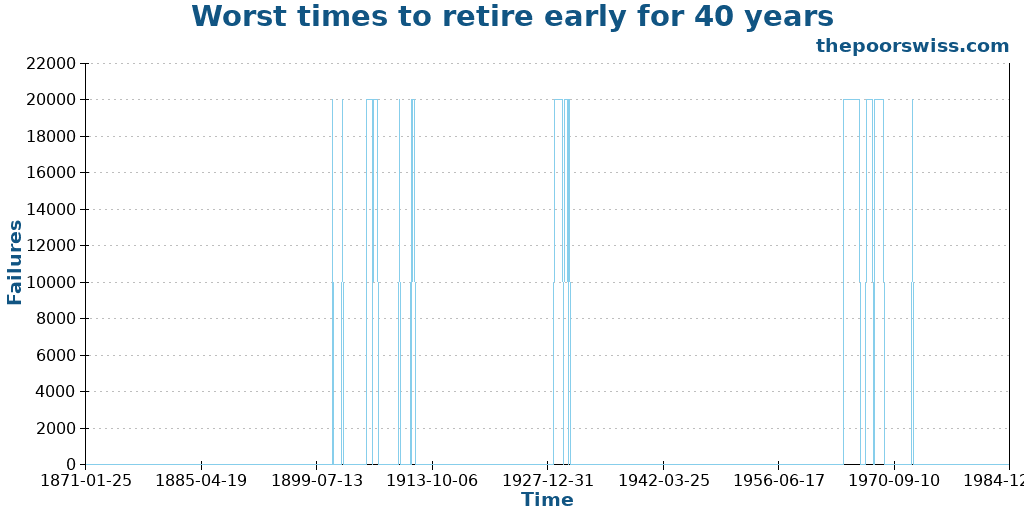

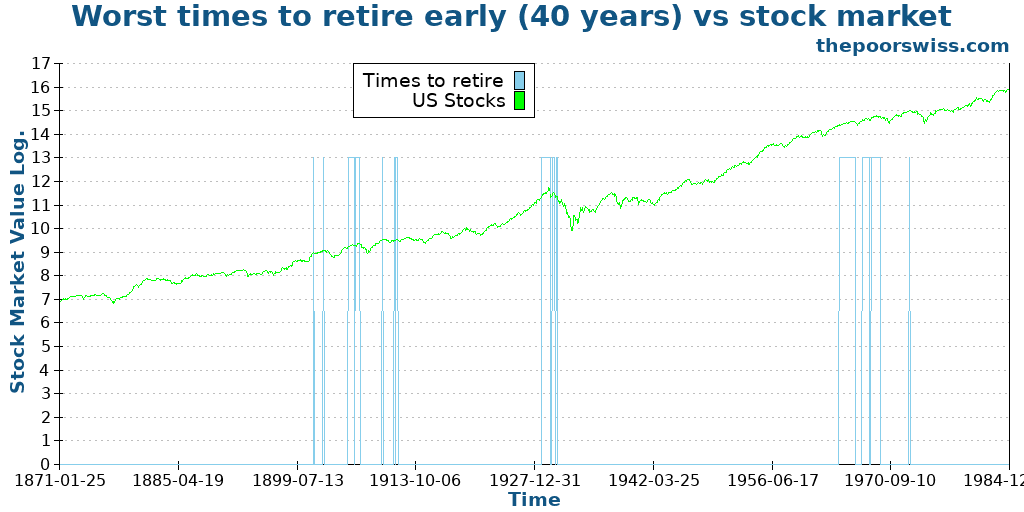

We can see if the same is also true for 40 years of retirement.

We can observe that there is more spreading of the outcomes in this case. But we need to correlate this data with the stock market to see if we can draw any conclusions.

Indeed, there are some interesting conclusions. As before, we have most of the failures happening at the top of the market (or near). But we can also observe some failures before a plateau. If the stock market is not moving higher, our chances of a successful retirement are rather low since we will exhaust our money too early.

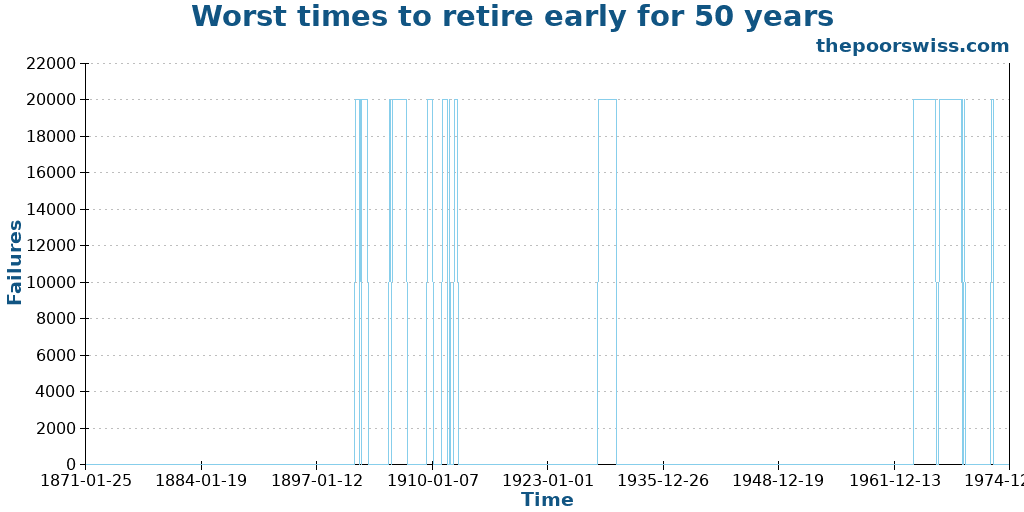

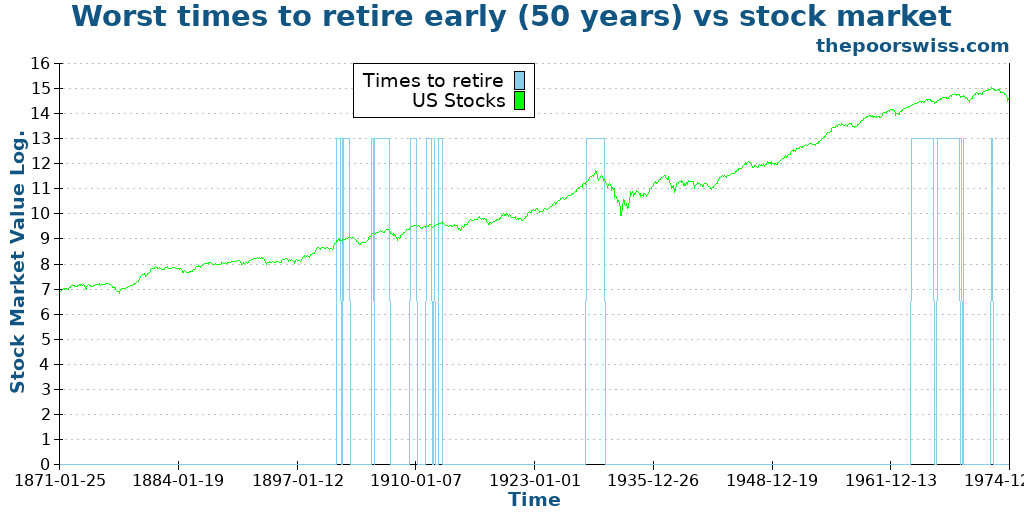

We can continue for 50 years to see if anything changes.

At first sight, it appears that these failures are quite similar to the one for 40 years. So, let’s quickly correlate that with the stock market.

And indeed, the conclusions remain the same. The worst times to retire early are either at the top of a peak or before a plateau.

Therefore, after looking at all this data, we should be careful about retiring early when the stock market is at the top of a perceived stock market high. Of course, it is very challenging to know where we are in the stock market cycle.

Conclusion

So, can we draw some useful conclusions from this data? Yes.

First, it is much better to retire at the bottom of the bottom of the stock market than at the top. The reason is that we look for future returns, which are lower when the stock market is already high. So, if the stock market is near its peak, we have a lower chance of success than if the stock market is near its bottom.

But do we know where we are in the stock market cycle? No. However, we can make some educated guesses. If we just saw a large decline in the stock market, we can expect to be near the bottom and have more chance of success. On the other hand, if the stock market has been doing well for years, we can expect our chances of success to be lower.

If we know this, we can adapt our margin of safety. For instance, we can assume we need a higher margin of safety after multiple years of stock market returns. On the other hand, we probably do not need that much if we have enough to retire when the stock market just dropped 30%.

Of course, these are just heuristics. We do not know where the market is headed in the future. But it still helps to know what are the best and worst times to retire early.

What about you? What do you think about these results?

More reading

How to sustain your capital in retirement?

Never run out of money. Learn strategies to sustain your capital indefinitely during retirement, even with market crashes and inflation.

7 Best Blogs on FIRE

There are more and more blogs about Financial Independence and Retire Early (FIRE), so which ones should you read? Here are my favorites!

Not All Assets are Created Equal – Introducing the FI Net Worth

What counts for FIRE? Learn why your "FI Net Worth" is different from your total net worth and which assets you should exclude from your calculations.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste,

Very interesting analysis, as always. Thank you.

One potentially dangerous aspect worth mentioning is that one is most likely to reach 100% FI when the stock market has done well for a while. Unfortunately, this is also the most dangerous time to actually act on it, based on your analysis.

Another solution, rather than just reducing the withdrawal rate, could be to use 5 or 10 year averages for the FI calculation. Trading time for safety. The best solution, IMHO, is finding a job you like and continuing to do it ideally without financial pressure.

Hi Joerg

That’s a very good point. It’s easy to increase worth in a bull market, but that’s not necessarily when you want to retire (or maybe at 110% instead).

I think it makes sense to trade some time for safety. It’s important to retire safely, as long as we don’t overdo it (at the risk of never retire).

Nice analysis, but you forgot one variable in the formula: inflation.

That explains why in the late 60ies and in the 70ies it was bad to retire: because of a long period of high inflation in the 70ies, and not because of really bad stock market.

If you redo your calculations using inlation-adjusted returns, you’ll get a much clearer picture.

Hi Marco

As mentioned in the article, I am using inflation in my calculation; everything has been done using inflation-adjusted withdrawals, like I always do.