Is Interactive Brokers safe for Swiss investors?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

I have been using Interactive Brokers for many years now. But many Swiss investors are wondering whether Interactive Brokers is really safe for their money, especially considering the fact that it is not a Swiss broker.

So, in this article, we are going to investigate whether Interactive Brokers is safe. We look at the financial shape of the broker, how it manages its money, and how it protects assets and accounts. This helps paint a picture of Interactive Brokers safety.

Interactive Brokers for Swiss investors

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Before delving into whether Interactive Brokers is safe, we should look at the different Interactive Brokers entities.

Interactive Brokers has entities in many countries. As Swiss investors, we deal with Interactive Brokers (U.K.) Ltd. This entity is affiliated with Interactive Brokers LLC, which is the main US entity. Residents in the European Union are generally using different entities, such as the ones in Ireland or Liechtenstein. This is an important difference because as Swiss investors, we get an advantage by using IB UK, such as being able to use US ETFs and benefit from SIPC protection. European customers do not get this custody by IB LLC.

The Interactive Brokers UK entity is regulated by the Financial Conduct Authority (FCA) in the UK. In the US, they are regulated by the Financial Industry Regulatory Authority (FINRA). So, Swiss investors may fall under both regulations. In Europe, entities are regulated differently. For instance, Interactive Brokers Ireland is regulated by the Central Bank of Ireland.

We are discussing a standard investor in stocks here. This distinction is critical because not all assets from the UK entity are custodied in the US entity. For instance, CFDs would not be custodied in the US.

Now, we have enough context to delve into the safety of Interactive Brokers.

Interactive Brokers is financially safe

When considering the safety of a broker, it is critical to consider its financial status. A good broker will be profitable and have a long-term history. So, we can look at key financial figures of Interactive Brokers.

As of June 2025, Interactive Brokers has 18.5 billion USD in assets. These are the assets of the firm itself, not the clients. So, they have a significant amount of equity. It is worth mentioning that they hold 12 billion more than they are required by regulations.

In 2024, Interactive Brokers reported more than 3.5 billion USD in pretax profit. This high profitability is a good sign for the future of the company.

We can easily say that Interactive Brokers is in excellent shape financially. The fact that they are profitable despite having low fees is an excellent sign. Often, some brokers do not have a profitable business model and end up closing after some time. If we care about our assets being safe, we should care about how long a broker will last.

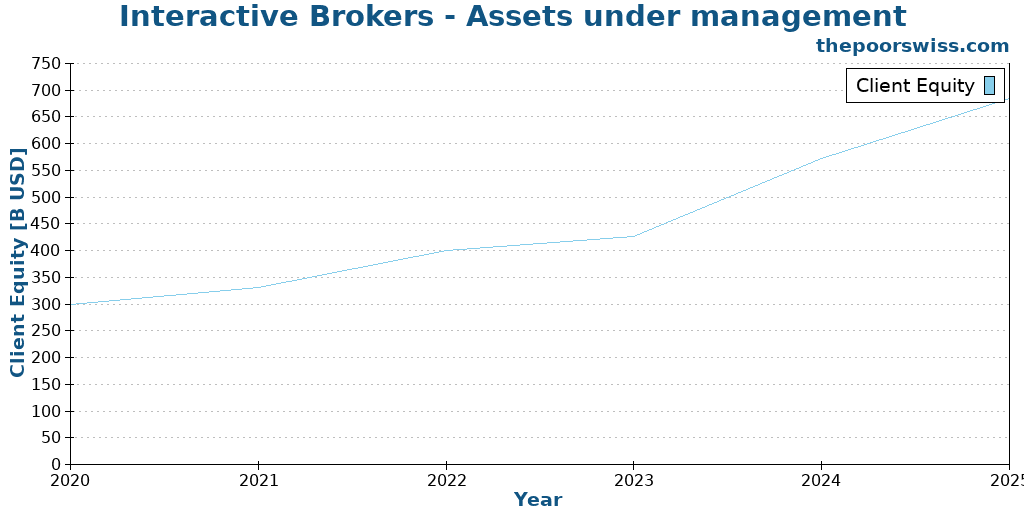

Interactive Brokers manages a lot of money

We can also look at how much money Interactive Brokers is managing.

As of August 1st, 2025, IBKR was managing about 685 billion USD in client assets. This is a very significant amount. And the good news is that this amount is still increasing, showing potential for growth.

At the same time, they had about 3.3 million customers. Again, this shows the popularity of Interactive Brokers.

Overall, Interactive Brokers has a solid user base and is trusted by many investors. It does not prove they are safe, but it proves they are trusted by many and able to handle many customers.

Interactive Brokers is a conservative broker

It is also important to check what a broker does with its money and that of its investors.

In that case, Interactive Brokers is a very conservative broker. They invest the cash of their investors in very short-term investments (government securities of only a few months). Additionally, Interactive Brokers does not hold any assets such as CDOs, MBS, or CDS (all instruments leading to the 2008 financial crisis).

IBKR only provides margin loans, which are secured by securities. They also have strict margin requirements. All their investments are marked to market daily to avoid unnecessary risks.

The company itself has no long-term debt.

Overall, compared to other brokers, Interactive Brokers appears to be very conservative. A conservative broker is much safer for our assets.

Interactive Brokers is not a bank

Contrary to many brokers, Interactive Brokers is not a bank. In terms of safety, this is actually an advantage.

Indeed, since IB is not a bank, they cannot do unsecured long-term loans. This is good because it means they have less leverage and as a result, less risk.

Another advantage is that they are free to use banks for their customers. And in fact, IBKR is using multiple banks to store cash. This means risk is reduced by not relying on a single bank.

One issue with some brokers that are also banks is that they allow arbitrary outgoing wire transfers. Normally, a broker will only allow accounts in your name for incoming and outgoing transfers.

Finally, since they are not a bank, they do not have products of their own. Banks could be incentivized into selling their products. But this is not the case with Interactive Brokers, which does not have their own products.

Overall, the fact that Interactive Brokers is not a bank is actually an advantage for the safety of our assets!

Interactive Brokers has a long history

Having a broker with a long history is generally a good sign that the broker is safe and stable and should be around for a while.

Interactive Brokers was founded in 1978, almost 50 years ago. It originally was market maker. Brokerage operations started in 1993. Since its founding, it has been growing quickly and has accumulated multiple millions of customers all over the globe. It indicates that they have global experience, dealing with many countries and regulations.

Another good sign is that the founder is still in the company and is still the chairman. Indeed, Thomas Peterffy founded the company and acted as CEO until he stepped down at 75 years old in 2019. Currently, he is still chairman of the board.

Of course, no history is perfect. During these years, Interactive Brokers has been fined a few times by regulators. For instance, they had a technical issue with negative pricing of futures. They were also fined a few times for free-riding (transactions without sufficient capital, related to cash settlement) and naked short selling (short-selling an asset without first borrowing it).

The fact that Interactive Brokers lived through many financial crises is a great sign. That and its great financial shape are good signs of longevity and safety for the future.

Interactive Brokers protects assets

How a broker protects assets is mostly defined by regulations. But some brokers decide to go further. So, we can see how Interactive Brokers protects customer assets.

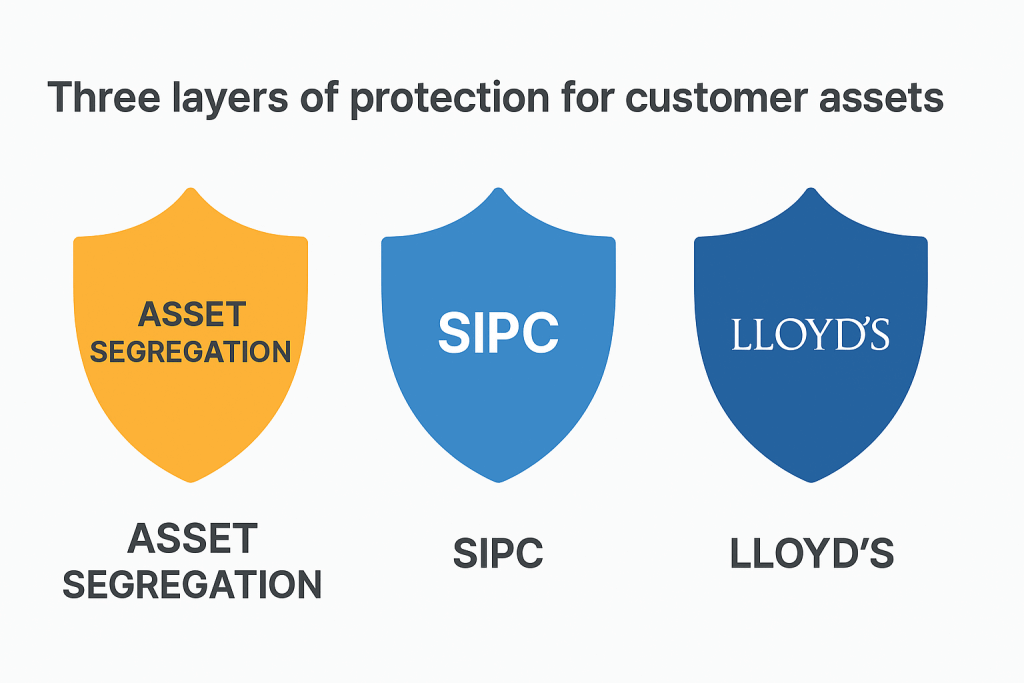

In the US, brokers must segregate assets. Segregation means that the broker assets must not be held together with the customer assets. In the US, this is done through the use of omnibus accounts. These accounts are accounts where the assets of multiple customers are held along with a ledger keeping track of everything. This is also what Interactive Brokers is doing.

Being a US broker, Interactive Brokers gets SIPC protection for customer assets. I must mention that I am talking here about Swiss investors. Indeed, Swiss investors will deal with Interactive Brokers UK, which will custody some assets with Interactive Brokers LLC (the US entity). This is not the case for other Interactive Brokers European entities.

SIPC is protection for up to 500’000 USD per customer, with a maximum of 250’000 USD in cash. This will protect customers in case of bankruptcy. Normally, the stocks should be protected by segregation, but SIPC would also protect stocks in case they were mismanaged and missing after the bankruptcy.

It is worth noting that SIPC has a global pool of money available; it is not unlimited (exactly like the Swiss deposit protection insurance). Currently, SIPC has about 5 billion USD at its disposal. It can also borrow about 2.5 billion USD from the Treasury. Overall, it means that SIPC has a global protection worth about 7.5 billion USD.

Additionally, Interactive Brokers has extra insurance from Lloyds to cover the funds that would not be covered by SIPC, for up to 30 million USD per customer, with a total cap of 150 million USD. There is a cash limit of 900’000 USD per customer. This is great for people with high net worth.

Overall, Interactive Brokers protects investor assets really well and keeps them safe. The three levels of protection are very effective.

Interactive Brokers protects accounts

These days, technical security is essential. It is essential to secure your account so that nobody else can access it. And the minimum is to enforce a second factor of authentication.

IBKR forces all accounts to have a second factor of authentication. There are two options:

- A digital second factor, with either the IBKR Mobile application or a standard TOTP authenticator app (Yubico, Google Authenticator, Proton, …).

- A physical security device (called Digital Security Card+) for accounts with a balance greater than one million USD.

Overall, Interactive Brokers is doing an impressive job at protecting user accounts and is technically safe.

Since we are talking about security, I should remind people that the biggest security vulnerability is generally human error. So be careful with your accounts and take online security seriously.

Interactive Brokers is not a Swiss broker

Obviously, Interactive Brokers is not a Swiss broker; it is a US broker, so it obeys different regulations. However, this does not mean it is less safe than a Swiss broker.

There are two main differences in regulations between a Swiss broker and a US broker.

- They both have to segregate investor assets from their assets, but they do it in different ways. In Switzerland, brokers are required to open a custody account for each of their customers. In the US, brokers use omnibus accounts, which are accounts holding the assets of many investors together.

- They both have some level of protection. In Switzerland, cash is protected by the Swiss deposit insurance for up to 100’000 CHF in case of bankruptcy. We have seen that Interactive Brokers has SIPC protection for up to 500’000 USD. SIPC includes stocks that are not protected in Switzerland. But in practice, this should not happen since the stock protection would only happen if some stocks were to be missing in a bankruptcy.

We have also seen that Interactive Brokers has insurance for extra-SIPC assets, which is not common. I am not aware of any Swiss broker doing such a thing.

Overall, assets with Interactive Brokers are as safe as with a Swiss broker. In case of bankruptcy, our cash is even better protected at IB than at a Swiss broker.

Conclusion

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Overall, Interactive Brokers does a great job at protecting the assets of its customers. It is also financially very stable, which is great for long-term continuity and stability. Since it is a conservative broker with a long history, this gives us confidence.

The conclusion is simple for me: Interactive Brokers is a safe broker for Swiss investors. I plan to keep the main part of my portfolio, with US ETFs, at this broker until retirement.

If you would like to learn more about Interactive Brokers, you can read our Interactive Brokers review. You can also look at how IB compares with Swiss brokers.

What about you? What do you think about Interactive Brokers?

More reading

E-tax statements now available for Interactive Brokers

Thanks to Datalevel AG, e-tax statements are now available for Interactive Brokers, removing one of its few disadvantages against Swiss brokers.

How To Buy an ETF on DEGIRO

Start investing today. Follow our step-by-step guide on how to buy your first ETF on DEGIRO and build your portfolio with low fees.

Saxo vs Interactive Brokers 2026

Local or Global? Saxo Bank vs Interactive Brokers: We compare fees, currency conversion, and safety to help you pick the best broker.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Is it an issue that my IBKR account has been assigned to the US entity?

Support recently confirmed this to me. In the account details I am clearly listed as a Swiss citizen, but I am a bit unsure whether the entity assignment could cause problems at some point in the future. What do you think?

I don’t think it’s a big issue. I remember one of my readers mentioning he chose IBKR US for better access to crypto a while back, and it seemed to be working.

Do you have access to a CH IBAN when you do a deposit? I would think that could be the main limitation. If you have access to that, you will likely have access to everything else you need.