Saxo vs Interactive Brokers 2026

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Saxo Bank has greatly improved its offer this last year. And while Interactive Brokers is my current and favorite broker, it may be interesting to compare it against Saxo Bank now.

So, it is time to compare Saxo vs Interactive Brokers in detail. I will examine and compare their fees, features, and usability. And we will also look at the user reviews for these two brokers.

|

Cheapest Swiss Broker

|

The best broker

|

Saxo

Saxo is a broker from Denmark, from 1992. They have an entity in Switzerland, licensed by FINMA. So, while they are technically a foreign broker, they work exactly like a Swiss broker and follow the same rules. Therefore, I consider Saxo to be a Swiss broker.

Saxo has more than a million customers worldwide, but it is unknown how many customers they have in Switzerland.

In 2024, Saxo slashed their fees, becoming competitive with other Swiss brokers. At this point, it is the cheapest Swiss broker, so definitely interesting to compare it against alternatives.

Interactive Brokers

Interactive Brokers is a US broker, from 1978, with multiple entities in Europe. In Switzerland, we are using the UK entity.

IB is a publicly traded company (helps with transparency)j and quite profitable (helps with sustainability). They currently have well over two million customers worldwide.

They have been known to have great fees for Swiss investors. And they provide access to many instruments in many stock exchanges.

Features

First, you need a broker that has all the features you need. If your broker does not fit your investing requirements, you must find another one. Therefore, we must compare the features of Saxo vs Interactive Brokers.

However, many brokers have many more features than we require. This does not improve them necessarily. We only care about the features we require. As simple passive investors, we use only a few features.

First, we can look at stock exchanges. In this case, both Saxo and Interactive Brokers provide us with access to the main stock exchanges. We have access to the major Swiss, European, and United States exchanges. These stock exchanges are all we need to build a great portfolio. Of course, they provide access to many more stock exchanges, but if we do not need them, we do not have to worry about them.

As for instruments, both brokers will provide us with access to ETFs, stocks, and bonds. Again, this is more than enough for simple investors, and both brokers provide access to further instruments such as futures and options.

Both brokers allow us to trade with US ETFs, the most efficient ETFs for Swiss investors. It is important because not doing that would be a significant disadvantage for one broker.

You can get interest on cash and margin loans at both brokers. Only Interactive Brokers offers fractional shares, but this is probably not something very essential for most people.

It is worth mentioning that Saxo provides e-tax statements, while Interactive Brokers does not. Many people like to use these statements to save time when filling out their taxes.

Overall, when comparing Saxo vs Interactive Brokers, both brokers have more than enough features to invest in the stock market.

Fees

It is critical to compare the fees for investing with brokers. Indeed, if we have the same portfolio on two brokers, the fees are what will differentiate our total returns. So, we will look at the fees of Saxo vs Interactive Brokers, in detail.

One disadvantage of IB is that its fee structure is more complex than Saxo. IB has two different fee structures (tiered and fixed) and two different fees for the currency conversions (manual and automated). For stocks, I will use the tiered pricing, which is generally better. And I will detail both for currency conversions.

We can start with the fixed fees. Both brokers have no custody fees or management fees. This is great.

For transactions, we must consider the fact that Saxo is a Swiss broker. As such, it will incur some Swiss stamp duty. Other than that, Saxo pricing is simple. Here are a few examples for standard stock exchanges:

- SIX Swiss Stock Exchange: 0.08% (minimum of 3 CHF)

- Euronext Paris: 0.08% (minimum of 2 EUR)

- NYSE: 0.08% (minimum of 1 USD)

On the other hand, the IB system is very complicated. I will not detail it here, but you can read more in my article about IB Fixed and Tiered pricing schemes.

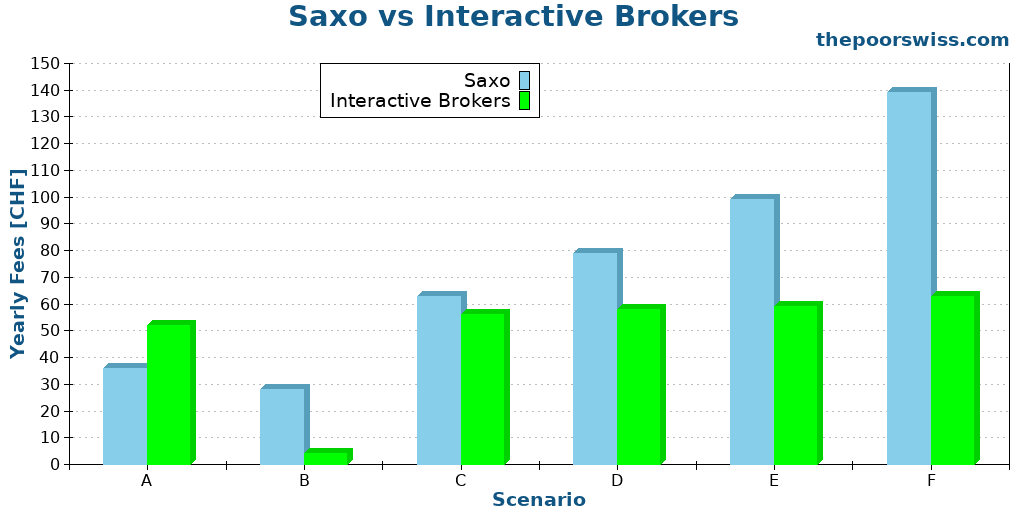

To compare Saxo vs Interactive Brokers, I took different scenarios and ran them through our broker comparison tool and got the results for the total fees of each broker. I have defined six scenarios:

- A: 1000 CHF in portfolio, 100 CHF in monthly investment, and 0% world allocation.

- B: 1000 CHF in portfolio, 100 CHF in monthly investment, and 100% world allocation.

- C: 1000 CHF in portfolio, 100 CHF in monthly investment, and 80% world allocation.

- D: 10000 CHF in portfolio, 500 CHF in monthly investment, and 80% world allocation.

- E: 50000 CHF in portfolio, 1000 CHF in monthly investment, and 80% world allocation.

- F: 100000 CHF in portfolio, 2000 CHF in monthly investment, and 80% world allocation.

For small scenarios, Saxo compares well to Interactive Brokers. Then, it starts to become pricier. Then, the stamp duty starts to weigh on the balance (but Saxo cannot do anything about that). The currency conversions are also much higher for Saxo than for IB. If you only invest in a Swiss ETF, Saxo will do very well.

We can also look at currency conversion fees in detail. Saxo has a 0.25% currency conversion fee. A manual conversion on IB costs 2 USD (or 0.002% if you convert more than 100k). An automated conversion costs 0.03% without a minimum. Here are a few examples of conversions:

- 100 USD

- 0.25 USD at Saxo

- 2 USD for a manual conversion at IB

- 0.03 USD for an automation conversion

- 500 USD

- 1.25 USD at Saxo

- 2 USD for a manual conversion at IB

- 0.15 USD for an automation conversion

- 1000 USD

- 2.5 USD at Saxo

- 2 USD for a manual conversion at IB

- 0.30 USD for an automation conversion

- 10000 USD

- 25 USD at Saxo

- 2 USD for a manual conversion at IB

- 3 USD for an automatic conversion at IB

Overall, as long as you are using the cheapest way to convert, Interactive Brokers can be much cheaper than Saxo to convert. That being said, Saxo is quite fair at currency conversion, when we compare it with other Swiss brokers.

Overall, when comparing Saxo vs Interactive Brokers, while Saxo is very fairly priced, Interactive Brokers is still significantly cheaper.

Safety

We also compare the safety of holding investments at Saxo vs Interactive Brokers.

Both brokers are well established and are in a good financial situation, with many customers (both have beyond one million customers). This makes them less likely to fail.

The technical security of both brokers is good. I have not heard of any major breach in either of these brokers. They both have support for a second factor of authentication (2FA). I would personally not use a broker that does not have a second factor. This is a crucial step in improving the security of your online accounts. Interactive Brokers goes one step further in forcing 2FA for all users.

Both brokers are regulated. In Switzerland, Saxo is regulated by FINMA, like all other Swiss brokers. As a result, 100,000 CHF of cash will be insured in case of bankruptcy. IBKR has SIPC protection, protecting up to 500,000 USD (250,000 USD of cash protection). So, unless you keep a lot of cash, you should not have to worry about it.

In both cases, assets are segregated, so your shares are not in their accounts. This is done slightly differently by both brokers. In Switzerland, Saxo does full segregation, with one account for each customer. And IB uses so-called omnibus accounts, which are accounts for multiple customers. In practice, it should not make a difference.

Overall, as for safety and security, both Saxo and Interactive Brokers are safe.

Reputation

Finally, we can look at the reputation of Saxo vs Interactive Brokers.

Even though it is far from perfect, I usually use Trustpilot as a source of reviews. Saxo gets a 3.7 out of 5 for the reviews on the whole group and 4.2 for the reviews on the Switzerland entity. So, based on that only, Saxo is slightly better than IB. On the other hand, IB only gets a 3.3 out of 5.

In both cases, the most negative point is about the customer service. On the positive side, we find some good reviews about IB fees and some good reviews about Saxo being easy to use. And we also find some contradicting reviews because some people truly enjoy both customer service. This is often the case because people generally do reviews either when they are really happy or really angry.

If we look at their apps, on the Google Play Store, IBKR gets a 4.8 score while Saxo gets a 3.9. On the Apple App Store, Interactive Brokers gets a 4.5 and Saxo a 4.6. Overall, it looks like apps from Interactive Brokers fare slightly better.

From what I am hearing in Switzerland, Interactive Brokers has a better reputation than Saxo. But Saxo is becoming quite popular since they changed their fees in 2024.

Overall, regarding the reputation of Saxo vs Interactive Brokers, I would say that both brokers have a decent reputation.

Saxo vs Interactive Brokers Summary

We can make a summary of Saxo vs Interactive Brokers:

|

Cheapest Swiss Broker

|

The best broker

|

|

Primary Rating:

4.5

|

Primary Rating:

5.0

|

|

Extremely affordable

|

Extremely affordable

|

|

Pros:

|

Pros:

|

|

Cons:

|

Cons:

|

|

: (Swiss residents using my link get 200 CHF in trading credits) |

: |

- Good execution

- Good range of investing instruments

- Swiss broker

- Easy to use

- No custody fees

- Not the cheapest currency conversions

(Swiss residents using my link get 200 CHF in trading credits)

- Good execution

- Wide range of investing instruments

- Very low currency conversion fees

- No custody fees

- Not always easy to use

We can draw a few conclusions for Saxo vs Interactive Brokers:

- Interactive Brokers is cheaper in most cases

- Saxo can be cheaper for small portfolios

- Interactive Brokers is a foreign broker

- Saxo is a Swiss broker

- Both brokers have all the instruments we need

- Both brokers are really good options

Conclusion

Overall, Saxo and Interactive Brokers are great brokers for Swiss investors. Interactive Brokers remains the cheapest broker available for us. But Saxo is closer than I would have thought. For some people, the fact that Saxo has a Swiss entity regulated by FINMA is an advantage.

Overall, the choice of Saxo vs Interactive Brokers boils down to a simple point: Are you open to a foreign broker?

- If you are, Interactive Brokers can save you a significant amount of money in fees.

- If you are not, Saxo is an excellent choice that is very affordable.

I am currently using Interactive Brokers as my main broker. And I am using Saxo as my secondary broker, for diversification. I have a good experience with both brokers.

For more information on these two brokers, read my reviews:

What about you? Which broker do you prefer?

More reading

How to buy an ETF from IBKR Mobile

Trade on the go. A step-by-step tutorial on how to buy an ETF using the Interactive Brokers (IBKR) mobile application.

Neon Invest Review 2026: Pros & Cons

Invest with Neon. Read our review of the Neon Invest feature. Are the low trading fees and selected ETFs enough for serious investors?

How does cash settle with Interactive Brokers?

Where is my money? Learn how cash settlement works at Interactive Brokers (T+2) and why you cannot withdraw your funds immediately after selling.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste! Thank you for the comparison. What would be interesting is to also add to the table a “Saxo Autoinvest” column, as that one is somewhat cheeper than the base case. Alternatively, would you mind please sharing your code so I can run that simulation? Thanks! :-)

Hi,

That’s a good point, I will mention it in a future update! Thanks for the idea.

You can use my comparison tool here (it does include AutoInvest as savings plan): https://thepoorswiss.com/broker-comparison-tool/

Hi Baptiste,

Your blog is very informative. While I am not a swiss, rather a resident of UAE and an Indian national, I received a message on IBKR “Form 1042S for tax year 2024 is now available”. And while trying to figure out what does it mean for me, I stumbled upon your blog. Could you please let me know if possible, if it has any implication for me?

Hi Zafar,

This form is only for the US, you can ignore it unless you have to file a tax return with the IRS.

You will receive it every year.

It’s great that Saxo now allows US ETFs.

To reduce broker risk, and continue to benefit from IBKR lower prices, I was thinking of transferring part of my VT shares to Saxo, while continue to use IBKR for trading. Do you know what is the cost at both ends for a position transfer? Or where can I find it?

Hi,

I think it should be free in this case:

* Saxo charges nothing for inbound transfers (Saxo Security Transfer)

* IB charges nothing for ACATS transfers which I believe would be involved here (IB Other Fees)

That’s great! Thanks!

Hi Poor Basler,

I am planning to do the same.

Where you able to successfully transfer securities from IB to SAXO?

Any pitfalls or bad surprises encountered along the process?

Thanks,

Guido from Basel ;)

It was very easy and it was all done within a week or so. You do need to start the process at both ends and they require some information from each other but I could find all I needed in the help articles in the websites.

Thanks for sharing, this is good to know!

Hi!

Big fan :)

So to understand correctly would it make then sense to have Saxo as our broker for Swiss ETFs and IB for non Swiss (world allocation) ETFs ?

Also in saxo they do the tax declaration for free. Is IB doing the same? If not is it very complicated and expensive ?

Hi Aline

If you want two brokers, it makes a lot of sense to have Saxo for a CH ETF and IB for US ETFs, yes.

Saxo does not do the tax declaration for free, it costs 100 CHF, unfortunately. You can probably do it manually as well and avoid paying but their reports are pretty bad.

IB is free but does not provide an e-tax statement. So, you have to generate an activity statement and enter everything manually into your tax declaration (which is perfectly fine unless you trade regularly).

Hi ! Thank you so much for your answer. It’s not per se that I want two brokers but the best strategy at lowest fees. So I understand then that having SAXO for Swiss ETFs and IB for non Swiss ones would be the best strategy in terms of lowest fees? Thanks again !

If you don’t want two brokers, only use IB. The difference in fees between IB and Saxo for CH ETFs is not that significant.

But if you want the optimal, then yes for small to medium amounts, Saxo is cheaper. But IB can be cheaper for large amounts.

Are you sure that IB doesn’t provide tax statements? I literally just got this email today. :-)

Dear IBKR Client,

Form 1042S for tax year 2024 is now available for account ****. To view your tax form, please log in to your account and select the Performance & Reports > Tax Documents menu or click the following link:

gdcdyn.interactivebrokers.com/sso/Login?forwardTo=2

For more information on our tax reporting, visit the Tax Information and Reporting page of our website or contact Client Service.

Sincerely,

Interactive Brokers

Interactive Brokers (U.K.) Limited is regulated by the Financial Conduct Authority

It’s a tax statement for the US, it’s not really useful for us :)

IB provides annual activity statement that works for Switzerland but cannot be imported (e-tax) directly.

Hi Baptiste,

I’ve taken another look at this topic today and compared SB and IB regarding security aspects. Here’s a summary of my findings:

1. Security at SB:

• Cash Protection: Cash balances are insured up to CHF 100,000.

• Securities Account: Securities are held separately under the Street Name (in the name of SB). In the event of bankruptcy, these securities do not form part of the bankruptcy estate, meaning the client has a claim to all (unlimited) of their securities, except for options.

• Custody Fees: Clients can choose whether their securities can be lent out:

• Yes: No custody fees are charged.

• No: Custody fees of CHF 120 per year apply.

2. Security at IB:

• Cash Protection: Cash balances are insured up to USD 250,000 by SIPC.

• Securities Account: Securities are also held under the Street Name (in the name of IB). However, in the event of IB’s bankruptcy, SIPC insurance covers securities up to a maximum of USD 500,000 (including USD 250,000 for cash).

• Securities Lending: Clients at IB do not have a choice; securities may be lent out if possible, backed by collateral.

• Bankruptcy Estate: From what I’ve read, all securities exceeding the SIPC limit are included in the bankruptcy estate. This means that if a client has, for example, CHF 1M invested in ETFs and IB goes bankrupt, the client would receive a maximum of USD 500,000 under SIPC protection.

Question:

Do you understand it the same way? Or would you agree with these points?

Thank you in advance for your feedback!

Best regards,

FD

Hi FD

Only two points I do not 100% agree:

1) Normally, at SB, the custody at not held under the street name but under the customer’s name. I think that’s a regulation of FINMA and that all Swiss brokers must follow. However, this does not change your conclusion which menas that the client has a claim to all the assets and they will not be part of the estate.

2) At IB, securities are indeed held under street name in omnibus account. Each of these accounts has many owners. But these accounts protected by SIPA regulation, so they should be considered segregated in a bankruptcy. So, they will not be part of the bankruptcy estate either.

Other than that, your analysis seems fair!

Hello, I thought it was not possible to invest in US ETFs directly from Swiss brokers due to KID/KIID requirement. But based on your description, I can buy VT on Saxo. Is that true?

Hi TG

Yes, you can buy US ETFs on Saxo and Swissquote (maybe other Swiss brokers as well). Brokers are allowed to execute trades on these ETFs, but not explicitly advertise them. If they were to advertise them, they would be forced to have a KID and in that case, they would not be able to advertise US ETFs.

Thanks for this article!

Do you know the best report to run in interactive Brokers in order to show the Swiss government your portfolio worth for the taxes? It’s tricky to find a report that shows the exact end of year value as well as the total dividends.

Hi Chaz

I do a full annual activity statement, as described here: How to file your taxes with Swiss and foreign securities in 2024

Hello!

I am new to your blog but I am interested in investing and in third pillar pension plans.

For now I am on B permit and i am not sure if it still makes sense to open one so I thought to wait with the 3a account at Finpension but I saw that they offer investment options as well.

Do you have any thought on Finpension’s product or would still recommend to do with IB?

Thanks

Hi Kitti

If you do not fill a tax return, you should not fill up your 3a because it only makes sense with tax benefits.

You should wait until you fill a tax return.

Finpension Invest is great (my review) and I even compared it to IB: Can Robo-advisors be cheaper than brokers?

Hello, I have held managed portfolios with Saxobank (Saxo Select-Brown Advisory ESG), which I just learned today will be discontinued. The charges were high @1.65% p.a., minimum deposit of USD 30,000 but I was getting good returns (around 17% p.a.). Can you suggest any other bank which provides managed portfolios in USD or currency hedged. I already have accounts with True Wealth and IB for ETFs. Unfortunately I dont have the expertise to invest directly in stocks nd my experience with UBS has not been great. Thank you

Hi,

I did not know they were offering this. Maybe Alpian has something if you do not mind something a bit more expensive than average.

Thanks. I just read your review on Alpian. I’ll research it. It sounds aligned with my needs. UBS really pushes their own funds and try charges are pretty high.

Thanks for the great comparison!

Saxobank has recently announced that they wave all custody fees, if customers enable securities lending on their portfolio. Additionally, the interest gains from security lending are shared 50/50 between SB and the customer, thus, generating potential additional revenue for customers.

Thus, even for larger portfolios, fees should be very comparable to IB. What are your thoughts about this?

Link: https://www.home.saxo/en-ch/accounts/securities-lending

Hi Maxime,

Indeed, waiving the custody fees makes it more interesting against IB. The potential income does not make a difference because you can also lend your shares at IB for 50/50 split.

Then, the holding fees will be the same. But the transaction fees at IB will still remain lower for large operations than Saxo.

Hi Baptiste,

Many thanks for all this useful information. Two questions:

1) Might assets at IB owned by a US person resident in Switzerland face any additional risks, given the political situation in the US?

2) Will Saxo work with US persons resident in Switzerland? If so, might Saxo be a better option?

Thanks!

Hi Michael

1) Currently, no. But who knows what the future holds for the US with Trump being so unpredictable? But in the worst case, even assets at a Swiss broker could be subject to some further stupid rules.

2) Unfortunately, Saxo will not accept US citizens. You would have to renounce your citizenship for that :(