Should you opt for securities lending?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Many brokers have an option to enable securities lending. When you do that, the broker can then lend your shares to other investors. And you then get some income from the securities lending.

Should you enable securities lending in your accounts? We answer this question in this article by going in details about this feature and its risks.

What is securities lending?

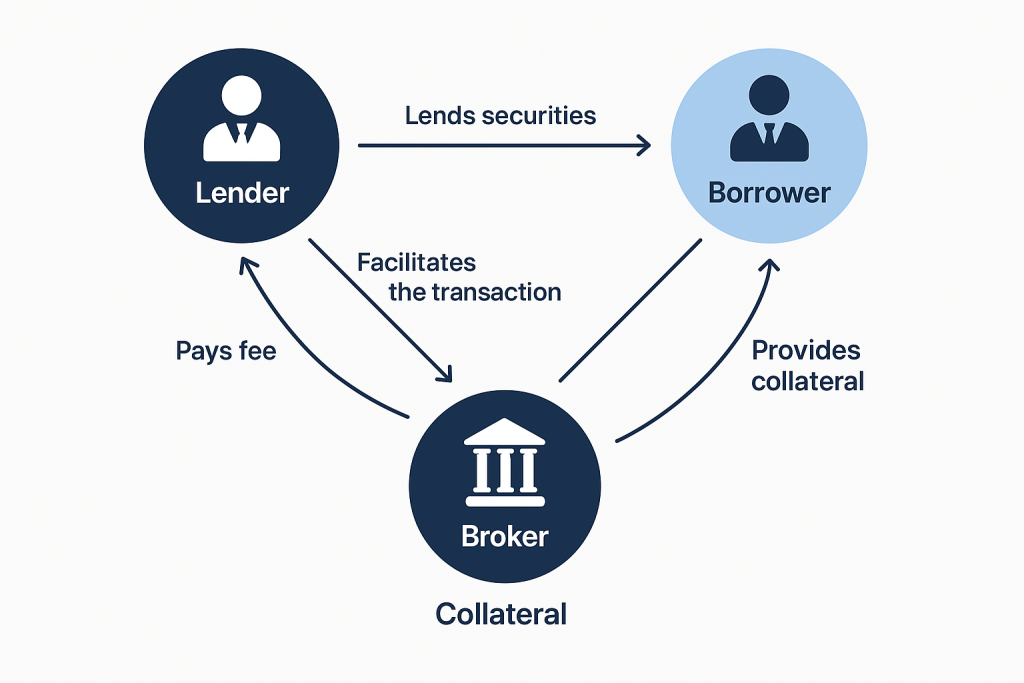

Securities lending means lending your shares to some other investors. But why would somebody borrow some shares?

Investors borrow shares to short a stock. When an investor wants to bet against a stock (betting the stock will go down in price), he sells a share he does not have and then buys it later. In this case, the investor intends to sell early at a higher price and buys back later at a lower price. But to sell a stock, you must have it. Therefore, the short seller must borrow shares. And if someone wants to borrow shares, someone must lend them. The broker acts as an intermediary here and will match borrowers and lenders.

And like all loans, there is an interest rate on this loan. So, the borrower will pay some interest to the broker. The interest rate is different for each security. And the broker can raise or lower the interest rate based on the market. These rates are based on demand and supply, on the state of the market and on the interest rate environment.

If you would like to know about the borrowing side of the story, I have an article about short selling. In the present article, we will consider the securities lending side.

Why Investors Participate in Securities Lending

So, we can start with the advantages of securities lending.

The only real advantage of securities lending is to generate extra passive income from your portfolio. If you are using a decent broker, the broker will share the profits from securities lending with you. Most brokers will share the profits (income minus lending costs) 50/50 between you and the broker. So you should receive a little less than half of the interest rate paid by the short seller.

The advantage of this income is that it is entirely passive, you have nothing to do. All is done by the broker and you only the income. Furthermore, while shares are lent, you are still getting dividends.

Key Risks Involved in Securities Lending

It is essential to talk about the risks of securities lending.

The main risk is that the counterparty (the borrower) defaults (counterparty risk). If that is the case, you will not get your shares back. It sounds dreadful, but it is not so bad because brokers ask for a collateral when lending securities. The collateral can be in cash or in securities. It usually covers at least 100% of the loaned securities. So, if the borrower defaults, you will get the collateral instead.

In theory, we should be fully safe with this collateral. However, there are still some collateral risks. If the shares you are lending go up in value, the collateral may not be enough anymore. If the collateral itself consists of shares, it could decline in value below the value of the loaned securities. Fortunately, brokers are keeping track of this and are revalidating the collateral value on a set frequency (the industry standard is daily). This is called marking-to-market, to make sure the collateral value meets the requirement of lending during the loan.

When the collateral is not enough when marked to market, the broker will require increased collateral. And if the borrower cannot meet the increased requirements, the broker will issue a margin call. If the borrower cannot restore the required margin quickly, he will default.

Since these events happen fairly quickly, you should not lose much money since the collateral value should not be too far off the value of your shares. But in the case of significant turmoil, you could lose everything that was lent.

So, in case of a counterparty default:

- You will get the collateral back

- In most cases, the collateral value should be close to the value of the shares you have lent

- In some cases, you could lose almost everything

The second main risk if the custodial risk. If your broker defaults while your shares are loaned out, getting back your shares after the bankruptcy may become more complex. Indeed, in this case, the ownership of the shares is different since they officially not yours, and you are officially lending them. During the bankruptcy proceedings, you should still be able to get them back, but it may take longer. Furthermore, it is important to note that if a broker defaults, the collateral will not be marked to market anymore. So, if the borrower defaults as well, then you may get very little back depending on the market.

Another kind of risk is the liquidity risk. While the shares are loaned out, the shares are less liquid. You can still them, but it may take time because they have to be recalled. Each lending agreement has a timeframe for that (a few trading days, generally). And it can get longer depending on the state of the market. So, you must be prepared to not be able to sell your shares instantly when you use securities lending.

In most cases, securities lending is safe. However, securities lending also incurs significant risks when markets are in turmoil. If the borrower or the broker were to default while your shares are loaned, you could lose a significant part of the value of those shares.

Other disadvantages to consider

In addition to the risks, there are other small disadvantages to securities lending.

One significant disadvantage about the securities lending income is that it is very difficult to predict. The income you will get will depend on your shares. Some shares and ETFs are lent more than others. And the demand for lending also depends on the market. There will be some periods where the stock market goes really well and the demand is low. Then, there are periods where the demand is high. Finally, even if demand is high, you have no guarantee that your shares will be lent. If the broker has too many shares to lend, yours may not be picked even when there is demand.

One disadvantage (at least for me) is that it can complicate your broker statements. When I tried it for a few months on Interactive Brokers a few years ago, it generated hundreds of lines in my activity statement. Since this is the statement I use for my taxes, I did not really like having multiple new pages (the tax office did not complain). But this is probably a slight disadvantage.

Another disadvantage of securities lending for some people is that you lose ownership of the shares while they are lent. One slight consequence is that you have no voting rights during the lending period. Another more major consequence is that you do not receive the dividends directly. Since you do not have the shares, the borrower will receive the dividends. But the borrower will have to compensate you fully with a substitute payment. In some countries, this may be an issue since they may be taxed differently. Fortunately, in Switzerland, this makes no difference since both kinds of payments are taxed as income.

Finally, one thing that is worth talking about is that by allowing securities lending, you allow people to bet against you. If you are holding shares for the long term, you are betting that the market will go up. But you then lend your shares to people that bet it will go down. This can be especially a moral issue if you are into ESG ETFs because you are betting on ESG but lending your shares to people that bet against ESG.

Securities lending for Swiss investors

We should also see how securities lending works with the main brokers for Swiss investors.

Interactive Brokers (our review) lets you enable securities lending and will give you half of the profits. Interactive Brokers calls this feature the Stock Yield Enhancement Program (SYEP). It is worth noting that you need a balance of more than 50,000 USD to enable this feature. The collateral requirements will depend on the currency (105% for CHF and 102% for USD for instance).

Saxo (our review) also lets you enable securities lending and gives you half of the profits. There is no minimum to enable this feature. There is a collateral requirement of 102% of the value of the security.

Swissquote (our review) started allowing securities lending in early 2024. Like Saxo, they share half of the profits with the lender, and there is a minimum. The collateral requirement is 105% of the security. It is worth noting that Swissquote will only lend shares to financial institutions, not to individual investors.

Finally, I would like to mention a different example: DEGIRO. In the past, DEGIRO would lend your shares by default, and you could not opt out of securities lending. This was later changed to an opt-in, but it is important to be careful about this.

Overall, the best brokers for Swiss investors handle securities lending in the same way. They share the profits with the lender, and they have relatively similar collateral requirements.

Securities lending and ETFs

There are two important points we can discuss regarding securities lending and ETFs.

First, ETFs can be lent exactly like stocks. If you have very broad ETFs, they are less likely to be lent out. So, with an ETF portfolio, you should not expect a lot of revenue. But since they are also less volatile, the risks are also lower.

The second point is the ETFs themselves are using securities lending. Large ETF providers like Vanguard and BlackRock themselves lend some shares of the ETFs to other investors (generally institutional traders). They do that to reduce the fees of the ETFs by sharing the income with the shareholders (and thus covering some fees). Some fund providers will also keep some profits to enrich the company itself.

Some fund providers are explicitly avoiding securities lending. Therefore, if you want to avoid securities lending entirely, you will need to select these providers. Unfortunately, this comes with a cost because some fees of the ETFs cannot be mitigated with income from lending. Therefore, if you would like to avoid securities lending, you will need to pay more in fees for your ETFs.

Expected returns from securities lending

If you want to get extra return, you may wonder how much can we get out from securities lending. Unfortunately, it is very difficult to answer this question.

For each of your security in your portfolio, there are two factors that will impact your income:

- The interest rate. As mentioned before, this will vary for each share, for each broker and vary over time as well based on demand and supply. Here are some very broad estimations for some categories:

- Low-demand: 0.1% to 0.5%

- Medium-demand: 0.5% to 3%

- High-demand: 5% to 20%

- Utilization rate: This defines how often your shares are lent out. You will only get something from securities lending when shares are lent out. Again, we can do some very basic estimations:

- Highly liquid stocks: Less than 10%

- Medium liquidity stocks: between 5% and 15%

- Special stocks: anywhere from 15% to 100%

As you can imagine, ETFs that are very broad will be less interesting than very specific ETFs. And shares that are very volatile (meme stocks are a great example) will be very profitable (and obviously much riskier).

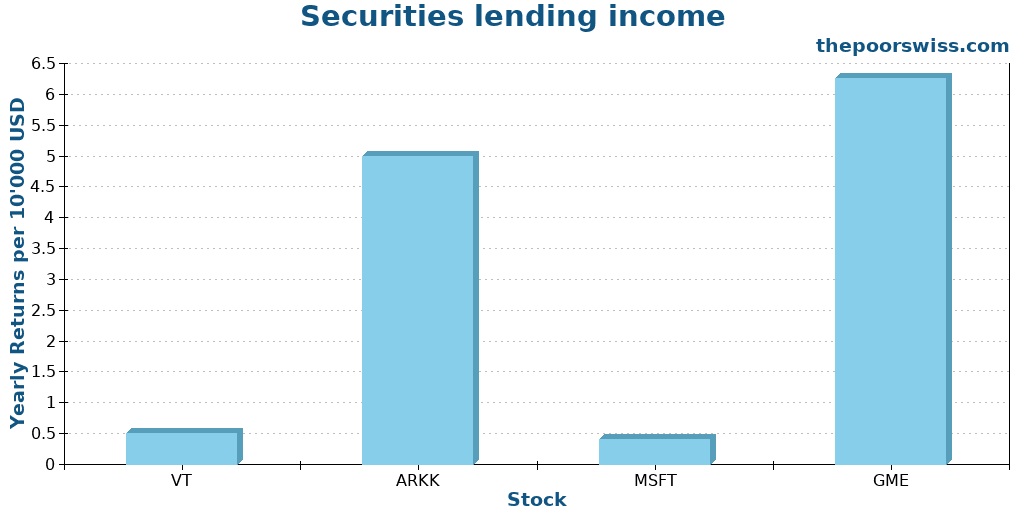

We can make some estimation based on past lending rates for a few ETFs and shares:

- Vanguard Total World ETF (VT). Assuming an interest rate of about 0.2% and a utilization of 5%, we could get a total return per year of 0.01%. If your broker shares half of the profits, you could get 0.5 USD per year for each 10’000 USD invested.

- ARK Innovation ETF (ARKK). We can assume an interest rate of 1% and utilization rate of 10%, giving us a total return of 0.1%. If you get 50% of the income, you would get 5 USD for each 10’000 USD in this ETF.

- Microsoft (MSFT). The lending rate is generally about 0.4% and the utilization rate at about 2%, with a total return of 0.008%. Assuming half of the profits go to the lender, the lender would get 0.4 USD per year for each 10’000 USD invested.

- GameStop (GME) during the short squeeze. This is an extreme example with an interest rate at around 20% and utilization rate close to 100%. You could get close to 20% per year, during the GameStop short squeeze. But of course, the prices of your securities would go up and down wildly, and trading was sometimes interrupted during this period. These days, you can get about 0.25% interest rate for 25% utilization rate.

Overall, if you stick to broad ETFs in your portfolio, you should not expect more than 0.1% per year in profits from securities lending. If you are some ETFs that are more specific to a sector, you may get slightly more returns. Shares of very stable companies like Microsoft are not very interesting either. Finally, if you have some more risky stocks, you could get higher returns.

Practical Recommendations for Investors

If you opt for securities lending after knowing all the risks and disadvantages, there are a few things you can do to make it smoother.

First, you should look at the details of the security lending program of your broker. You want to know to whom it will lend shares and how much of the profits it will pass to you. A general rule is also, of course, to only use a reputable broker (this always applies). And you should see the conditions for opting out.

Ideally, you should not lend out your entire portfolio. Some brokers allow you to select the share you want to lend. If your broker does not allow that, you could consider using multiple brokers and only opting for securities lending in one of them. Like that, you would limit the risks to a part of your portfolio and not to your entire portfolio (although the chance of your entire portfolio being loaned out is slim).

Finally, you should know that unless you have a portfolio full of heavily shorted stocks, you will not generate a lot of revenue.

Conclusion

Overall, should you opt for securities lending in your broker? Maybe.

Securities lending is not for everyone. It can generate some extra income, but it still adds extra risk to the portfolio. With a well-diversified portfolio of ETFs, both the upside and the downside are low. But if you own some shares that are often shorted, you may get higher income (at the cost of higher risk).

Typically, even a borrower default would not impact you too much because of collateral requirements. However, if the market is moving quickly (for either the loaned shares or the collateral), you may lose a significant part of the value of your shares. And you lose in liquidity since you may not be able to sell your shares exactly when you want.

Personally, over the years, I have tried securities lending on and off. The returns have always been very low, but it helps offsets the fees of the brokers. If you are investing for the long term, I would not say I particularly recommend securities lending. It adds a little risk and adds a little income, but it will not move the needle much in any direction. If you think it will make a major difference to your ETF portfolio, this will not be the case. But if you want to make a few more francs every year, try it out and see whether it suits you.

What about you? Do you use securities lending?

More reading

Saxo vs Swissquote 2026 – Which is the best Swiss broker?

The big broker battle. Saxo vs Swissquote: We compare the two leaders in Switzerland to see which one offers the best fees, safety, and features.

Interactive Brokers Review 2026: Pros & Cons

My honest and complete review of Interactive Brokers (IB), an excellent broker. Find out how good IB is and its pros and cons, and more.

Neon Invest Review 2026: Pros & Cons

Invest with Neon. Read our review of the Neon Invest feature. Are the low trading fees and selected ETFs enough for serious investors?

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste

Thanks for your article. Do you know if there would be any difference in the Withholding of cash-in-lieu you receive instead of the dividends? For US ETFs/Stocks we can claim it back but would cash-in-lieu not even get withheld? or at the same 15% rate if the borrower is resident in the US and maybe at higher (more detrimental) rate if borrower is in a place without tax treaty with the US?

Thanks

Hi Manuel

Excellent question. And yes, this can be an issue. I believe (not entirely sure) that in-lieu payments will not be considered as qualified dividends and will therefore be withheld at 30% withdrawal rate. Additionally, you may have a hard time getting it back through DA-1. So, with securities lending, you may lose 30% of the US dividends if that is right.

I will research this more and update the article accordingly.

“there is no maximum downside to what you can lose” and “In some cases, you could lose almost everything” is actually very different…

There is a maximum loss of 100% with lending (lender defaults and collateral is worth nothing, so you don’t get anything back). In shorting for instance, there is really no maximum loss, as you owe a share which could be several times the original investment.

Fair point, when you are lending, you can “only” lose what was lent but not more. I will fix this in the article, thanks!

Hi Baptist thank you very much for the comprehensive summary. If I may ask, do you know what are the tax implication of security lending? In particular:

1. How / where in the Steuererklärung one declares the interest rate from the loan?

2. Provided that we may not receive dividends directly, while I understand that the rate of the taxation is the same, does it make any difference in a way the securities are declared in the Steuererklärung? I.e., should one just “pretend” they owned the securities the entire time, declare them in DA-1 (if applicable), and thus implicitly request the return of the taxes paid in the US?

Thanks!

Hi Dominik

That’s a good question, and I am not entirely sure.

1) Last time I tried, I declared it under account interest (like a bank account) and it worked

2) I do not think it will make any difference in Switzerland in the way it is being declared. However, one case may be weirder. Some Swiss ETFs pay capital repayment instead of ordinary dividends and these capital repayments are tax-free. So, in theory, if you got a payment in lieu instead of a capital repayment, you may have to declare it extra, but I do not know exactly how.

Hi Baptist thanks for the post, very informative as usual. I started investing in IBKR because of you’re post, thanks.

How can I activate the security lending on IBKR if you don’t mind me asking.

Regards

Hi Chris,

Thanks :)

If you want to enable this feature, you can go into your account settings and click on “Stock Yield Enhancement Program”, this is how IBKR calls this feature.