Updated Trinity Study for 2026- More Withdrawal Rates!

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Would you like to know precisely which withdrawal rate is safe and will sustain your lifestyle for a long time?

You will find the answer in this article, with updated results from the Trinity Study! This study researched different withdrawal rates for retirement. Although the original research was not about early retirement, it is often referred to in the Financial Independence and Retire Early (FIRE) movement!

However, there are two caveats to the original study. First, they are only covering the period until 1995. And then, they are not covering more than thirty years of retirement. Thirty years is not enough for some people wanting to retire early.

Therefore, I reproduce the original study’s results with recent data all the way to 2025! And I extended the data back to 1871. This makes for much more data than the original study.

I have also considered periods as long as 50 years. It means many more withdrawal simulations than the original study.

In this article, you will find how I did it and all the results I have gathered from this data!

The Trinity Study

I have already talked at great length about the Trinity Study. It is an excellent research paper done by three professors from Trinity University.

Their research paper’s goal was to see which withdrawal rates people should use to sustain a particular lifestyle for up to 30 years. It is important to note that the original research was not about early retirement but official retirement.

It is important to emphasize that we are talking about sustaining a lifestyle (expenses), not capital. So, if you end up with 1 USD at the end of the retirement period, this is a success. If you want to sustain your capital in retirement, it is a different success criterion not treated by the original Trinity study.

They tested the success rates of withdrawal rates from 3% to 12%. Furthermore, they tested portfolios with between 0% and 100% stocks by jumps of 25%.

The authors also took inflation into account in the results. Indeed, it is interesting to compare the results with and without inflation. Finally, they also provided the terminal values of the portfolio.

I wrote a detailed article about the Trinity Study if you want more information.

The 4% Rule (of Thumb)

The Trinity Study is the source of the 4% Rule. This rule states that if you only withdraw 4% of your initial portfolio yearly, you can sustain your lifestyle for a very long period. And your withdrawal is adjusted for inflation every year.

Some people believe that the original study shows that this will sustain forever. But this is not what the original research was about. They only tested simulations for up to 30 years.

It is better to call it the 4% Rule of Thumb. Because if you plan to retire very early, you will probably need a lower withdrawal rate. Moreover, your withdrawal rate will depend on your portfolio and asset allocation to stocks and bonds.

Why did I do it again?

If the study is excellent, why did I want to redo it? I have several reasons for that.

First, I wanted to see how this worked with recent stock market returns. The original study was only covering years up to 1995. I wanted to have more recent data. I wanted to ensure the results were holding with more recent stock market behavior. So this simulation will cover returns until the end of 2025!

Secondly, the original study only covered up to thirty years of retirement. I wanted to ensure that the portfolio could sustain withdrawals for extended periods. For people retiring early, I think that 50 years is not unreasonable.

Finally, I have to admit that I like to write code. So it was cool to write code related to this blog. And being a big geek, now I can run many simulations with the data I want. Overall, it was a lot of fun preparing the data for this article.

Ultimately, I want to extend the Trinity Study to the European markets. It will be challenging to obtain the data. But I will try to find it for as many years as possible.

How I redid the Trinity Study

My simulation uses monthly withdrawals. Most people in retirement will withdraw money monthly. It is also possible to withdraw money at the end of the year instead. But I believe that it is not common.

I have calculated all the returns monthly. Doing that makes the results much more accurate than doing it yearly. And the monthly withdrawal is updated with inflation every month as well. Every possible starting month in the available data is tested.

For this simulation, I have not done any rebalancing. For more information, I have compared different rebalancing methodologies for retirement.

Withdrawals are based on the current allocation. For instance, if your base allocation to stocks is 60%, but your current allocation is 80%, 80% of the withdrawal will be taken from stocks. If you are interested, I have explored other techniques in other articles:

Based on this simulation, I collected the same results as the original study: success rates without inflation, success rates with inflation, and terminal values.

Success rates of the Trinity Study

I start the simulation with the entire data from 1871 to 2025.

In this simulation, success is when your portfolio does not run out of money before the end of the simulation. For instance, if we simulate for 20 years and end up with one dollar after 20 years, it is a success. This is a failure if the portfolio runs out of money before that (it could be in the first year or the nineteenth year).

So, the success rate is the percentage of the months that end up with success. The higher the success rate, the better the results are.

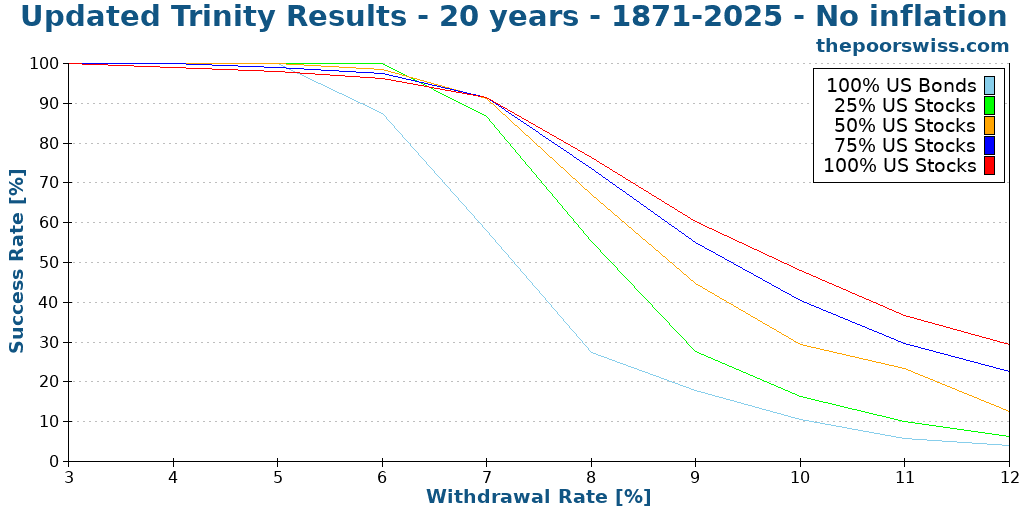

We will see what success rates we have when we ignore inflation. We start with 20 years since I do not think anybody will care about a ten-year-long simulation. I will begin at a 3% withdrawal rate and go up to 12%, increasing by 1% at a time.

We can see what we already expect:

- Increasing the withdrawal rate decreases the chances of success

- Any withdrawal rate higher than 8% does not make sense long-term, even without inflation.

- A small allocation of bonds can help with lower withdrawal rates

- Generally, a 100% stock portfolio will perform better than the other portfolios.

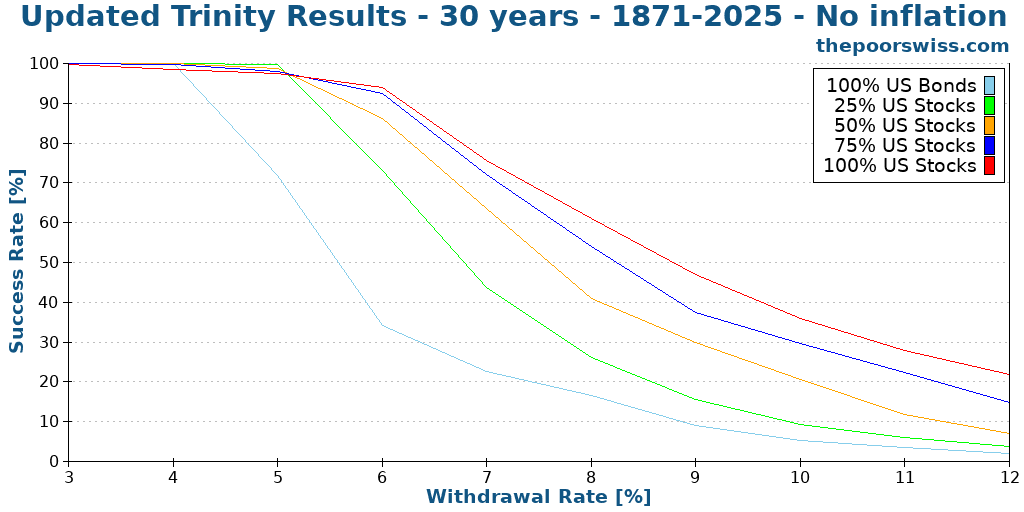

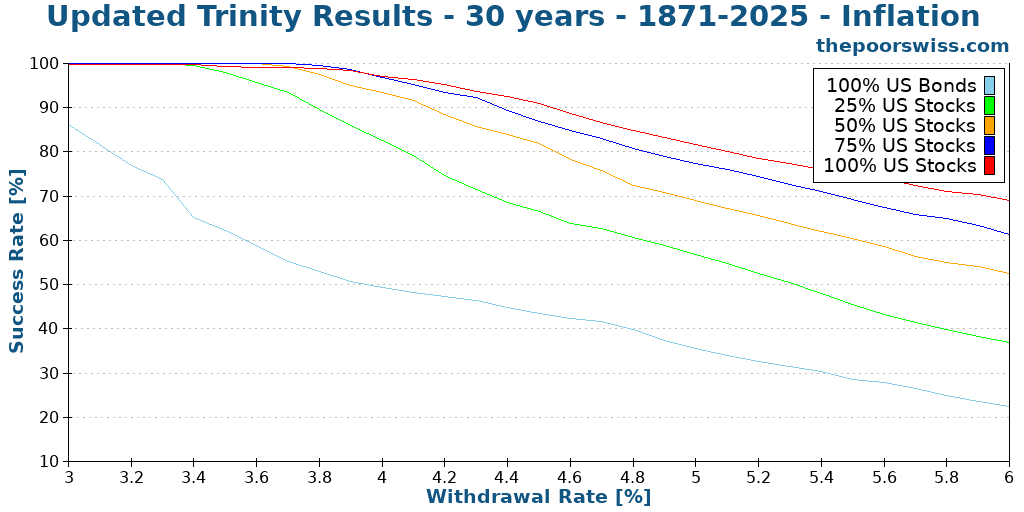

Here is what happens when we push the simulation to 30 years.

We can see that increasing the number of years decreases the likelihood of success. It is logical since you are more likely to run out of money.

With 30 years of retirement without inflation, a 6% withdrawal rate with a significant allocation to stocks still makes a lot of sense!

Taking inflation into account for retirement

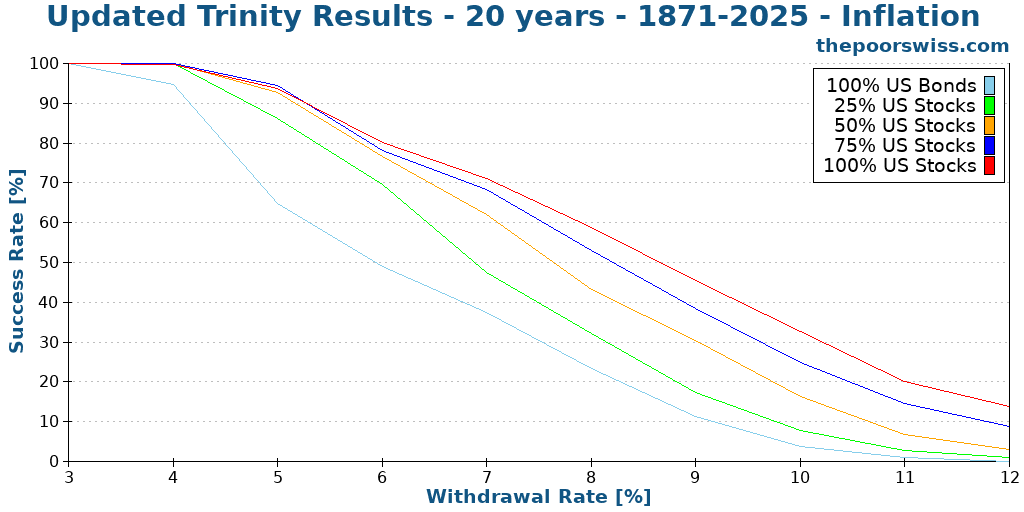

However, it is much better to consider inflation in our simulation! We start again with 20 years to compare the results:

As we can see, inflation causes a significant hit to our chances of success! Before inflation, an 8% withdrawal rate made some sense. Now 6% is the limit. And even 6% has a barely over 75% chance of success!

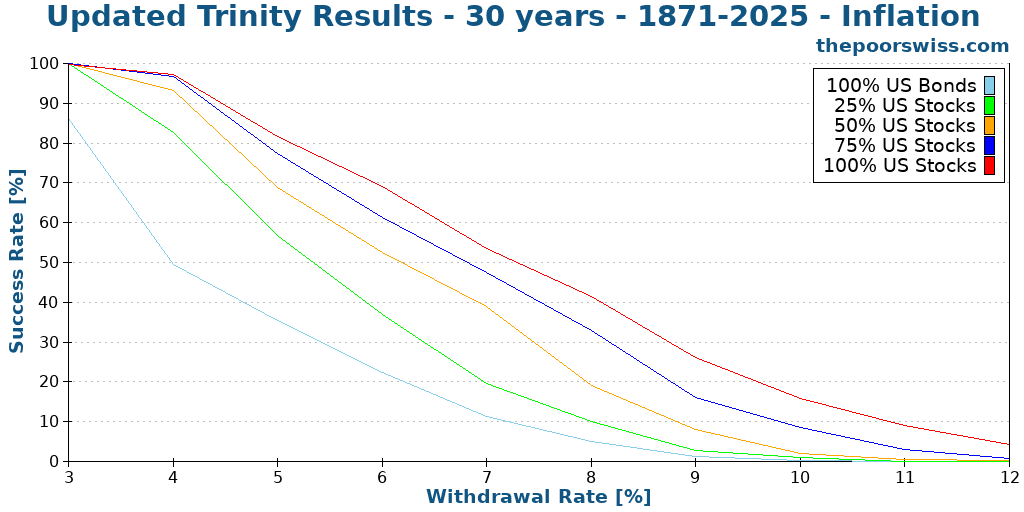

Here is what happens for 30 years of retirement.

We can now see that anything higher than a 6% withdrawal rate is hazardous, with a less than 75% chance to succeed even with 100% stocks.

More withdrawal rates

Since we see that reasonable withdrawal rates are in the range of 3% to 6%, we try more withdrawal rates. I have simulated increments of 0.1% of withdrawal rates.

With a large stock allocation, withdrawal rates between 3% and 4% are very safe. Some people would even dare use withdrawal rates of about 4.5%. But even a portfolio with 100% stocks has only an 85% chance of success after 30 years with 4.5%.

Longer retirement time

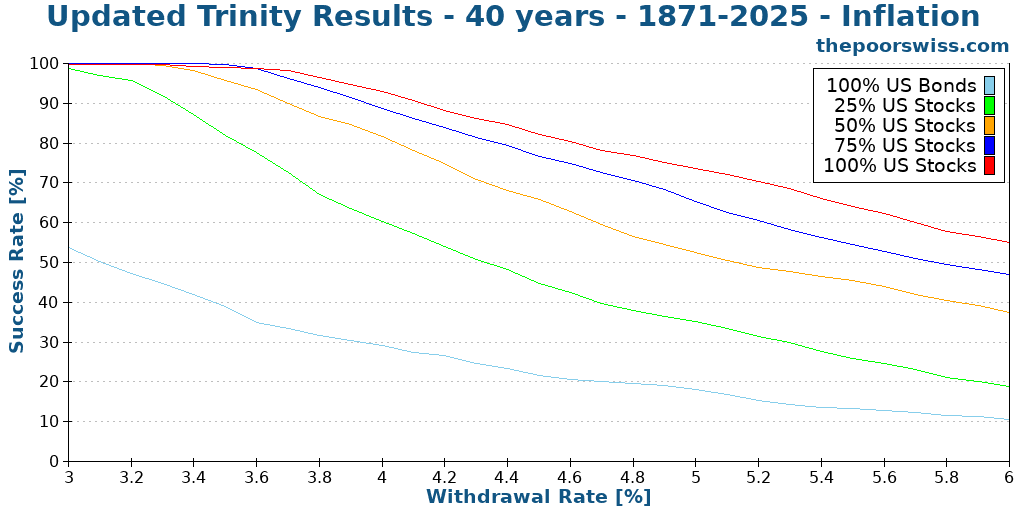

One of the caveats of the original study is that they stopped at 30 years. We run the same simulation again but with 40 years this time.

After 40 years, we are starting to see lower success rates, even for most people’s 4% withdrawal rate. Unless you have 100% of stocks, your success rate will be less than 90%.

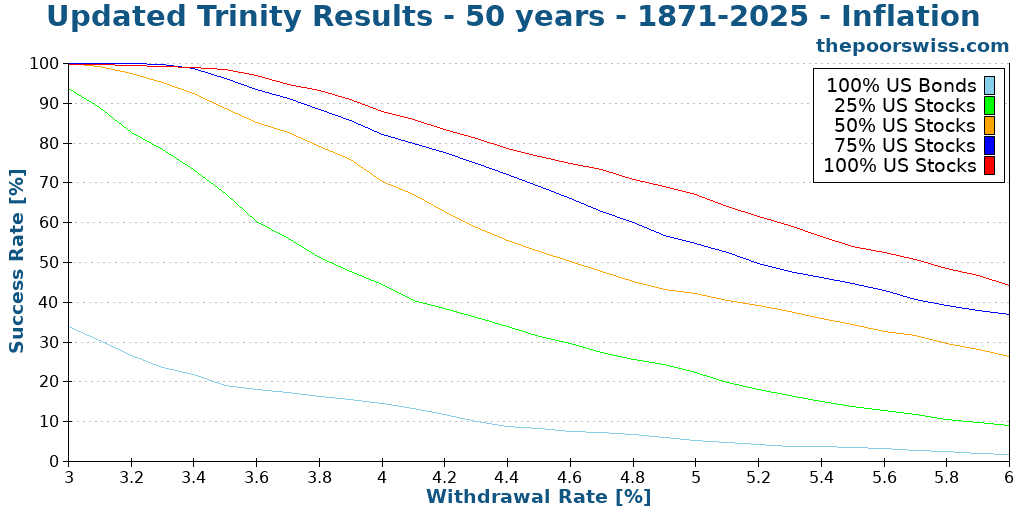

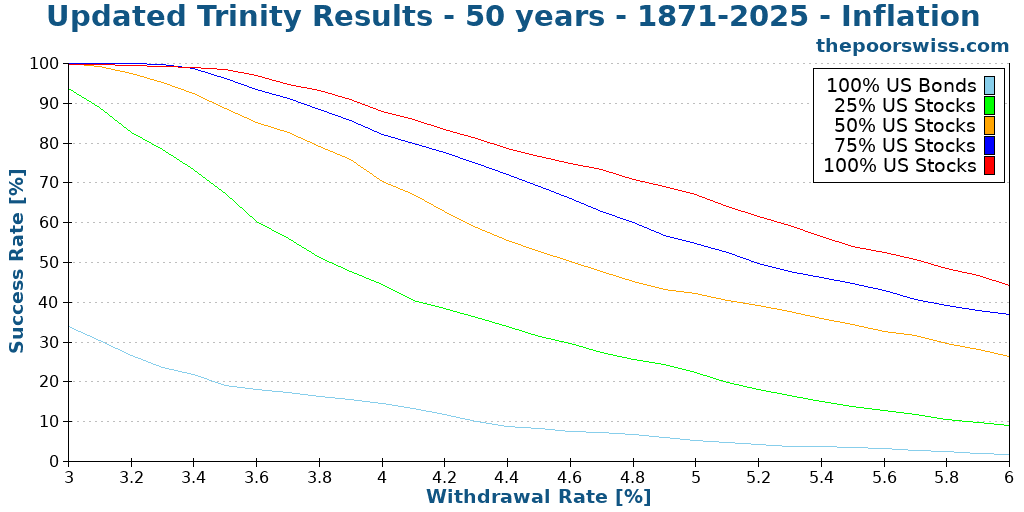

Here is what happens in 50 years.

As expected, we see lower success rates. But it is still not bad at all with reasonable withdrawal rates. A 100% allocation to stocks and a 3.5% withdrawal rate still have more than a 98% success rate. This is significantly more than I expected.

It shows that the study’s original conclusion can still hold for over 30 years. It is excellent news!

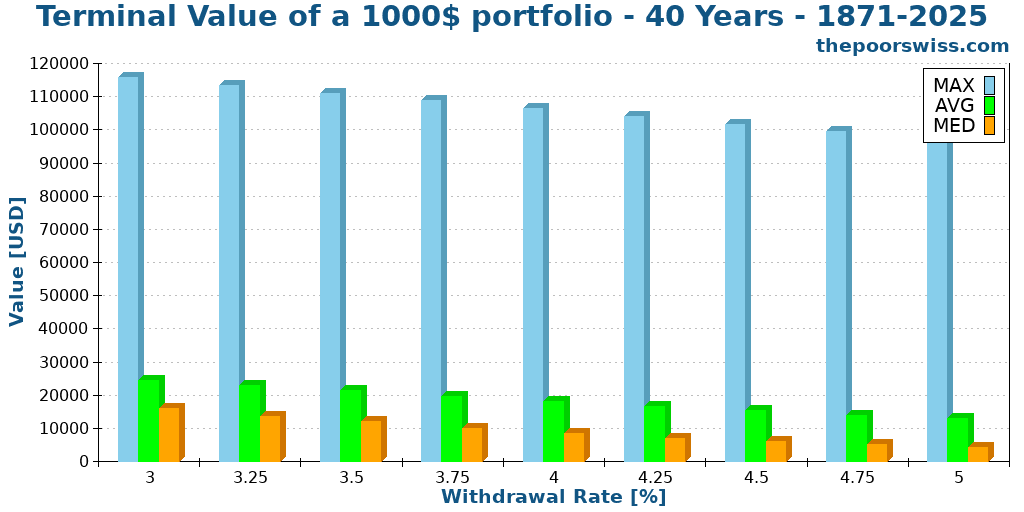

Updated Terminal Values

Another interesting thing from the study was that they also compared the terminal values of the different withdrawal rates and portfolios.

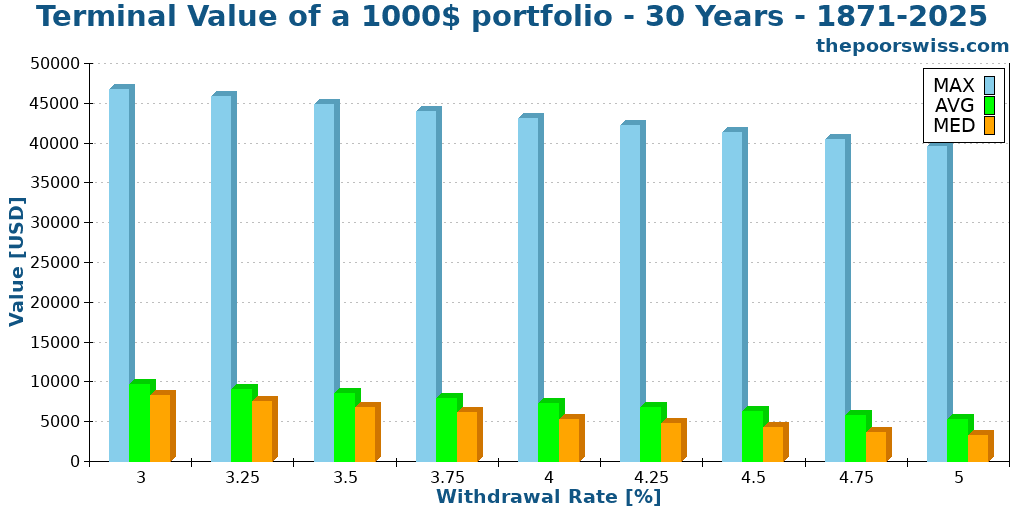

So we will see the terminal values of a 1000 USD portfolio after 30 years. I did the simulation for a portfolio of 100% stocks. For the sake of display, I have reduced the number of withdrawal rates.

I did not show the minimum values. Indeed, they are always zero. If the chance of failure exceeds zero, the minimum value will be zero.

However, the average and median values are quite remarkable. We will focus on the median since it is generally more representative than the average.

For a withdrawal rate of 3.5%, my current target, the median terminal value after 30 years, is about 6700 dollars! Not only did your portfolio sustain your lifestyle, but it also increased sixfold! Let me repeat this. After 30 years of doing nothing but withdrawing money, you have six times more money than when you started!

The maximum values do not mean a lot. But it is crazy to see that after 30 years, you could have about 30 times more money than when you started! And this is with a 3.5% withdrawal rate!

Here is what happens when we extend it to 40 years.

We can see that the results are comparable. However, all the values are significantly higher. The numbers are all about twice higher. On average, your retirement money will double during the ten additional years. So, even though you are not contributing more money and living from it, your portfolio will double in 10 years. How cool does that sound?

The success rate is not everything

There is something important with these measurements: the success rate does not tell the entire story. For instance, for you, which of these two scenarios is better?

- 98% to last 50 years, but a chance of running out after ten years

- 96% to last 50 years, but a chance of running out after 48 years

For me, the second scenario is better. You do not want to have a chance of failing after only ten years if you are planning for 50 years. But if it fails after 48 years, you have many years to make some adaptations.

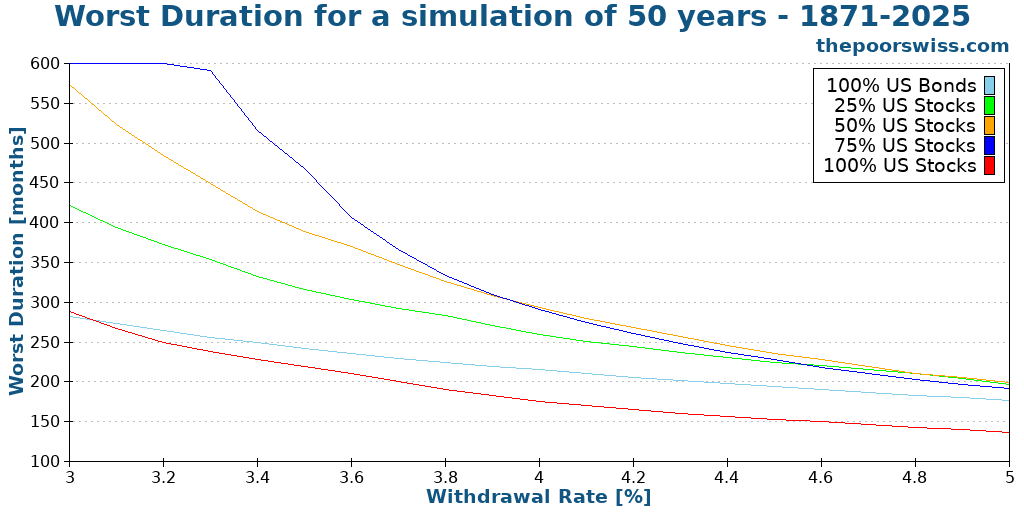

So, another essential metric is the worst duration of a scenario. This means after how many months, the first failure can happen.

For reference, here are the success rates of each portfolio for 50 years and different withdrawal rates:

And now, here are the worst durations for each of these portfolios:

If we only look at the first graph, the conclusion is that higher allocation to stocks is always better. But if we look at the second graph, 100% stocks is the worst one!

So what does this mean: you need a balance in your portfolio. Bonds will significantly reduce the chances of your portfolio failing too early. This does not mean that you should optimize for the highest worst duration either. Because if your highest duration is 40 years, but you have only a 50% chance of reaching 50 years, this is gambling, not planning.

So balance is essential. While stocks will increase your success, stocks are more subject to sequences of return risks.

How to implement the Trinity Study?

Now that we have noted that the results of the Trinity Study are encouraging and would let people retire early, how should we implement it?

Theoretically, the Trinity Study is based on a simple concept: you can retire based on a large principal by withdrawing with a fixed withdrawal rate.

However, in practice, this means you need to accumulate money, more than most people accumulate during their lifetime. And you need to accumulate this earlier than retirement age.

To accumulate this money is not easy, but it is also not complicated. First, you have to save money (as much as possible). For this, you will have to focus on your expenses and earnings.

Then, you will have to invest that money until you can retire. Once you have accumulated the proper amount through capital gains and savings, you will be financially free.

If you are interested, I have many articles on my blog about financial independence.

How did I do it?

You can find my code and my data on Github. Everything is available to share as much as possible!

I wrote the entire program in C++. I used this programming language because it is my favorite! And it is blazing fast! I have not especially optimized my code, and it takes less than a second to generate thousands of simulations.

If you are not a coder, I also have an online FIRE calculator to do most of the calculations presented here.

My U.S. and international data is based on the data made available by Big ERN in its Safe Withdrawal Rate series. It is a good dataset that has been tested several times already. Big ERN made all this available for free. I am thankful for his work! I have completed its data with the missing years using the same methodology.

If you want to use the graphs in this article, please cite this article as the source of the image!

Future of the series

It was fascinating to reproduce these results. And it was very insightful as well. I have learned many things from the results. It is great to see the confirmation that the original conclusions hold for more than 50 years.

And it also shows that my withdrawal rate (3.5%) is a safe bet. I may switch to 3.75% in the future. I will have to run more simulations. It is important to choose a proper safe withdrawal rate.

Talking of simulations, I have run a few more simulations with the same idea:

- Trinity Study Results with Swiss Stocks

- Withdrawal rates and low-yield bonds

- When should you rebalance your portfolio?

- Does the Trinity Study work in recent years?

- How often should you withdraw money?

- Can you retire early with Swiss stocks and bonds?

- The Trinity results with world stocks

- Equity glidepaths in retirement

Since I plan to make more articles like these with more simulations, I would like to get your perspective on this article! Please let me know what you think in the comments below! What should I improve?

What do you think of these results? Would you like me to run more simulations like this? Do you have ideas on what kind of simulations I should run next?

Conclusions

With all these results, we can have several important conclusions.

First, the paper’s original conclusions still hold even with much more data being considered. And it still stands accurate up to 2026! It is excellent since it shows that the 4% rule of thumb still works!

If you increase the simulation time to more than 30 years, a 4% withdrawal rate is no longer safe. With 50 years of retirement, you have a 90% chance of success with a 4% withdrawal rate at most. A withdrawal rate of around 3.5% would be safer for most people.

If you want real chances of success, you will need more than 50% of your portfolio allocated to stocks. The stocks allow us to fight inflation and cover the withdrawal rate year after year.

If you choose a reasonable withdrawal rate, you will likely have much more money than when you started! For instance, a 3.5% withdrawal rate over 30 years with 100% stocks would leave you about six times more money than when you started!

For information about the original study, read my detailed article about the Trinity Study. If you are extremely conservative, you will also be interested in learning how to choose a failsafe withdrawal rate.

If you want to start investing to become financially independent, you will be interested in my guide on how to get started in the stock market.

More reading

How to Calculate your Financial Independence (FI) Ratio

How you can compute your ratio to Financial Independence (FI). How to use Safe Withdrawal Rate (SWR) to see how much you need to save.

Sequence of Returns Risk can ruin your retirement

Protect your retirement. Learn what Sequence of Returns Risk is and how a market crash early in retirement can destroy your portfolio.

Retire Early: The Simple Guide – I wrote a book

I wrote a book, Retire Early: The Simple Guide, with Thomas Walke, another Swiss blogger. Our book is about the basics of early retirement.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Thank you for this excellent article. It’s both intellectually interesting and very practical. Great combination.

It would be helpful to have a discussion of adjusting the withdrawal rate mid-retirement. If you are on track to have a terminal value that is 10x the initial value of your portfolio, it would seem like you could safely increase your rate of withdrawal. On the other hand, if things are trending poorly, at what point should you adjust your rate of withdrawal downwards?

The tricky part is that you don’t want to make these adjustments in response to short-term market conditions, i.e. bubbles or temporary bear markets that correct relatively quickly. Hence the value of having some rigorous guidance on when and how to make such adjustments.

Hi Andrew,

That would be an interesting discussion indeed! I should try to get something like this simulated, but there are many options to do it.

I would imagine that raising your withdrawal rate by 0.10% if your effective withdrawal rate stays lower than some threshold during 24 months (or more or less) would make sense. And same in the other direction but probably faster.

Good idea, but it will be difficult to simulate all the possible variants :)

Hi poor Swiss. Is there anyway you can show the numbers in the graph, or add a table below to show the actual %,with the large gaps between the numbers on the axes, it’s difficult to see exactly what the % are.

Hi Steve,

That’s a good point. Unfortunately, it’s difficult to maintain and display good graphs in WordPress. I will try to make them more readable on my next update.

In the meantime, you can get the exact numbers with my FIRE calculator. But you won’t have cool graphs.

Poor Swiss,

Both your and Big ERN’s work on SWR is extraordinarily valuable to everyone. For all that you do and contribute, Thank you.

I do have one concern that I would like to hear your view. All of the historical data (and the basis for the MC simulations) is based on US returns for the past 100 +/- years. The data set is robust.

My concern – is only using US historical data systematically biased? And is the bias overstating the ROI thus creating risk for those who rely / believe that the historical returns will continue?

However, the last 150 years have transformed human existence. Broadly, I believe the root causes are

1. scientific and mathematical knowledge

2. organized capital markets

3. human freedom and property rights.

And the US has been the transcendent economy during this time and the most powerful economic force in human history. Certainly, no other economy or capital market was its equal during this period. Number 1 (knowledge) should continue to increase / improve (although the US may no longer be the leader), and 2 and 3 now already exist.

Thanks for all you contribute,

Patientcash

Hi patientcash,

Thanks for your kind words :) I am glad to be cited next to Big ERN!

It’s somehow biased indeed. The problem is that this is the best dataset we have today. I personally do not invest 100% in U.S. stocks but in a world ETF. I think that we will see lower returns, in the future, but this may also be entirely wrong.

The last 150 years have a large impact, but I believe that technology will continue to grow very quickly in the next 50 years: space exploration, nuclear fusion, quantum computer, … We still have a wealth of things to discover and improve. And while it’s better than before, many countries still have a ton of work to do on human rights. Some countries stopping to fight could have a very positive impact on the world’s economy.

I am not too worried about the future of the stock market. But if you, it’s always good to diversify outside the stock market and be a little pessimistic.

Hi!!

Congratulations for this article, it enlighten me into financial independence world.

Is there any specific analysis for brazilian scenario?

Hi Mauricio,

Thanks for your kind words!

I have not heard of any specific analysis for a Brazilian scenario. I have done some simulations for a Swiss investor. But I do not have the resources to do it for every county.

My triggers above are not real nor tested. Instead, I wanted to offer the idea of variable-spend in retirement instead of a single withdrawal percentage kept for 30 years.

The Michael Kitces website has several articles considering variable-spend strategies. Here’s one: https://www.kitces.com/blog/the-ratcheting-safe-withdrawal-rate-a-more-dominant-version-of-the-4-rule/

Wade Pfau gives variable spend strategies some consideration: https://retirementresearcher.com/10-variable-spending-strategies-retirees-consider/

This is a powerful analysis that reinforces and updates the Bengen benchmark withdrawal rate. Let me propose a strategy of selective withdrawal rates that can be derived already from this analysis (no new coding in C++ needed, Mr. Swiss!).

Pick three withdrawal rates:

* Minimum spending just to exist without a job — rent, food, cell phone, utilities, etc. No vacations, takeout pizza or pay-per-view.

* Average Lifestyle — include now vacations, some restaurant, hobbies

* Luxury Lifestyle — Expensive hobbies: boats, foreign travel, golf membership

Those three numbers will be specific to you personally, based on your estimated spending at each level. Divide your spending by your portfolio to come up with three percentages. For example, the percentages could be:

* 3% — Base spending, high likelihood of success

* 4.25% — Lifestyle spending, decent likelihood of success

* 6% — Luxury spend level, lower likelihood of success but in a year where stocks return 12%, possible short-term

Now plan to tailor your retirement spending based on how the market performed. Even if the market goes down, you take 3%. If the market rose 1% or better, take 4.25%. If the market exceeded 8%, take 6% out. This plan reduces sequence-of-return risk by economizing during down years but allows higher spending than 4% in very good yours. We don’t need a European vacation or a boat every year, do we?

BTW, this retiree thinks you FIRE young people are absolutely outstanding. Keep it up.

Hi Walt,

That sounds like a good strategy for flexibility. I am just not sure about the 4.25% if the stock market rose 1%. If the stock market only does 1% in a year, you should not take 4.25% out, no?

But yes, being flexible is a great way to reduce your risks and also increase the money you can take out. But it requires good planning!

Are you actually this strategy?

Mr. Swiss, I agree with your criticism and am not using it yet. I’d like to give some thought to the trigger points and percentages that would make sense.

The specific values (e.g. 4.25% etc.) are customized for the individual. For example, if the person has $1 million saved and forecasts $30k needed for minimal expenses, $42.5k for lifestyle, and $60k for luxury spending, then the 3%, 4.25%, 6% withdrawal ratios are appropriate. For everyone else, calculate your own withdrawal rates. by dividing expenses by portfolio.

Similarly, the trigger points (e.g. “if the market goes up 1%….) are yours to set. The key concept is that spending varies depending on market conditions.

The idea is to relieve some pressure from the worst-case scenario; portfolio exhaustion due to sequence-of-returns risk. The Bengen 4% tries to prevent portfolio exhaustion by setting a single value for withdrawals, then calculating via Monte Carlo method whether that one percentage will survive 25-30 years.

Truth is, most people can tailor their spending within a range and need not settle on a single Goldilocks value that persists for 30 years. With a strategy for variable withdrawals based on per-year portfolio returns, they can have both the security of not running out (in worst-case scenarios) as well as the opportunity to spend more (in the best-case scenarios).

I’d like to hear your feedback on this. If you like the variable-spend concept, let’s consider what trigger points make sense. The percentages are up to the individual’s situation.

If you make the specific values customizable as well as the trigger points, it makes sense. Now, it still feels a little complicated for me. And it is very difficult to tune since you have to choose the trigger points very well.

And we have to be careful about taking inflation into account for the three values. Finally, most people grossly overestimate their capacity to spend less. So, flexibility is great, but most people are not good at it.

Interesting article recently on Marketwatch

about success rate:

“The failure rate of the same strategy in Italy? Er…67%.

In France and Germany it was more than 50%. In Japan, about 36%.

Even in Great Britain and Switzerland the 4% rule would have failed more than 20% of the time. And using data across the world, Estrada calculates the overall failure rate for the 4% rule would have been 22%. In other words, one time in five retirees would find themselves forced to scale back their standard of living to get their money to last.”

https://www.marketwatch.com/story/think-you-can-rely-on-the-4-rule-in-retirement-think-again-11617913126?mod=home-page

Hi,

Yes, it’s entirely true that the results of the trinity study only apply to the United States stock market.

And even in the United States, most people are now getting more conservative than 4%, with something like 3.5% (or even lower for some).

That’s why it is necessary to adapt this to each portfolio and to each country’s inflation. You could not retire with only stocks from Switzerland unless you got a tiny withdrawal rate.

This is a fantastic, detailed article! I’ve heard of this study referenced many times, but this is the only article I could find that outlines the study in detail, including the constraints (like defining success rate, asset allocations, and the time period).

I used to throw around the 4% figure, without fully understanding where that number came from. It looks like there is a sweet spot at 3.5% for folks seeking FIRE, and right now with high valuations (Shiller P/E~35) I personally think caution is even more important.

I’ll be sure to reference your article.

Thanks again.

Hi Jake,

Thanks a lot for your kind words :)

I am really glad my article was helpful!

Cheers

fine, fine work

one has to wonder how applicable these calcs are in this time of crazy (and longterm!) valuations and superhigh p/e, coupled w nearly trivial safer-bond returns

Hi David,

With the low-returns of the bonds, you need more stocks. I did a small study of that: Trinity Study and low-yield

As for the current high valuation, we have seen that many times in history, I do not think this would change much. I do not think right now is a great time to retire, unless you have a large margin of safety.

Great job with the post and all of the work to get the new graphs, etc. The one concern I have that you mention in the low yields post is that Trinity, and even your redo, rely on historical bond rates that will skew the bond portion of the overall results. I do not see any return to bond returns of double-digits and really only expect 2-3% before inflation… Is there an easy way to run the revised Trinity study using bond returns of less than 4% for 30-50 year periods? I think that would be the most useful for current and future retirees.

Hi Scoob,

I have an article that should answer this question about low yield and The Trinity Study: https://thepoorswiss.com/retire-low-yield-environment/

Hi.

I don’t think this part is right, or maybe just the wording is just throwing me off :

“This rule states that if you only withdraw 4% of your initial portfolio every year…”

In the Trinity Study I believe they only withdrew 4% in the first year, and then every year after that they adjusted the previous year’s withdrawal amount by inflation. Which in the long run I would guess would have noticeably different results than withdrawing 4% of your portfolio each year.

They also considered a failure running out of money, when the portfolio value ended up less than the calculated withdrawal amount for that year the run was over. In-fact strictly speaking if the rule is ‘withdraw 4% of your portfolio every year’ you would actually never run out of money. What did you use as a failure scenario, pegging a minimum lifestyle cost against the first withdrawal and then comparing your withdrawals every year to that (inflation adjusted) cost?

Not trying to be overly critical or a troll, just don’t understand the specifics, and I find the best way to figure out a misunderstanding is to point out what I think is wrong (and maybe be told what I am misunderstanding). I see ‘withdraw 4% of your portfolio every year’, is a common interpretation a lot of authors give, so maybe I’m the one misunderstanding something. Although I have also seen authors using the rule as I gave it.

Hi,

This part is right but maybe not very clear, I talk of inflation a little later. My computations take inflation into account, month after month.

And indeed, my computations are considering 4% of the initial portfolio (plus inflation), not 4% of the current portfolio, which as you said would never run out of money.

The failure scenario is when we are not able to withdraw the current withdrawal amount. If the current portfolio value is lower than the current withdrawal value, the simulation is ended with a failure.

Interesting and good to see based off this that my target SWR still falls in the safe range.

I definitely look forward to seeing your tests with different withdrawal methods. For example I would love to see what happens if you use a conservative SWR like 2-3% to establish your baseline, but then recalculate your dollar amount every time your portfolio doubles by moving up a half step. Say for example you start with 1 million and 3%, and bump it to 3% of 1.5m when and if your portfolio jumps to 2m. Worst case if your portfolio drops to 1.5m you would fall back to your baseline. I wonder if it would last the distance or if it might drive your SWR up to high to cause a failure.

Hi Bob,

That’s a good idea. I am sure there are many ways to increase the withdrawal in good market conditions. I will try to think of a few scenarios that are worth testing.

Thanks for the suggestions!