Can you retire early with a robo-advisor?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

I have done many retirement simulations on this blog before. But I have always assumed direct investment in low-cost funds. But what would happen if you invested through a robo-advisor with higher fees?

In this article, I run simulations and present results of what would happen in retirement with a robo-advisor with different levels of fees. By the end of this article, you will know whether you can retire with your robo-advisor.

Retirement simulations

The Trinity study is the root of the Financial Independence and Retire Early (FIRE) movement. This study shows that by withdrawing a percentage of your initial portfolio yearly, you could sustain your retirement lifestyle for 30 years.

Since the story is not recent, I have updated and refreshed the results of the Trinity Study. I have shown that we could sustain a retirement for up to 50 years if we use reasonable stock allocation and a reasonable withdrawal rate.

But, until now, all my simulations have been done either without fees or with extremely low fees (0.1% or lower) corresponding to a DIY investor.

So, today, I want to reproduce these simulations but with conditions closer to robo-advisors.

In all my simulations, I will use yearly rebalancing and monthly withdrawal. I will use US stocks and bonds and US inflation. The fees will be withdrawn monthly as well. Each simulation will use the available historical data from 1871 to 2024.

The fees of robo-advisors

We have many Swiss robo-advisors. The good robo-advisors allow us to reach 100% (or close) stock allocation. And some would even allow us to invest in a US-only portfolio.

Several robo-advisors have degressive fees with large portfolios. Therefore, I assume a portfolio of about two million CHF, which most people would need in Switzerland to retire early.

We can take a few examples to see the ranges of fees we can expect (with a portfolio of two million CHF):

- True Wealth would cost 0.53% per year.

- Inyova would cost 0.90% per year.

- Selma would cost 0.69% per year.

So, we can expect fees from about 0.50% to 0.90%. Since these are only examples, I will add more price points to my simulation, but it is essential to understand where we stand.

Retirement success

We can start the simulation and see what happens with 0.50% TER, the minimum you could reasonably get.

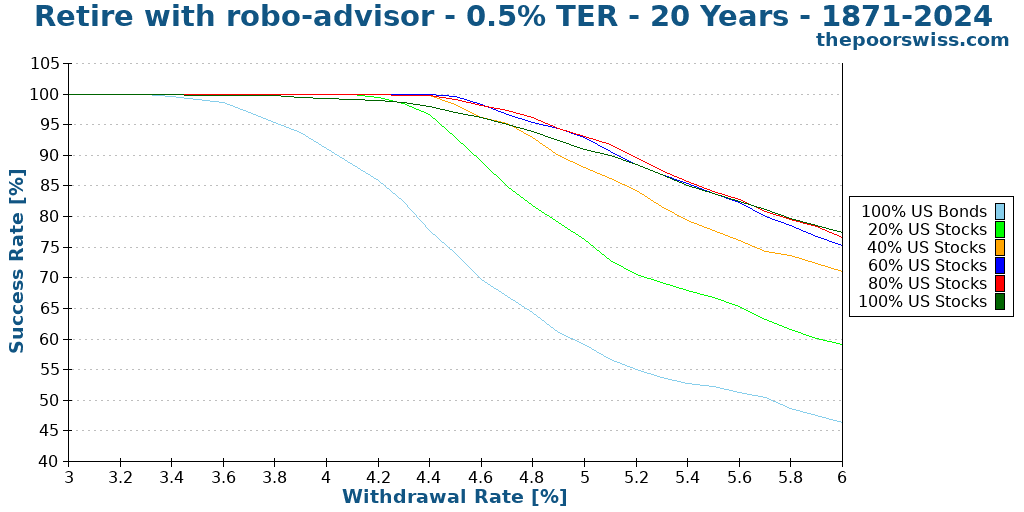

First, can we retire for 20 years with a robo-advisor?

So, a TER of 0.50% would not diminish our chances of retirement over 20 years. Except for 100% bonds, all portfolios perform well in this scenario. This makes sense because 20 years is a very short period to simulate, given the stock market returns.

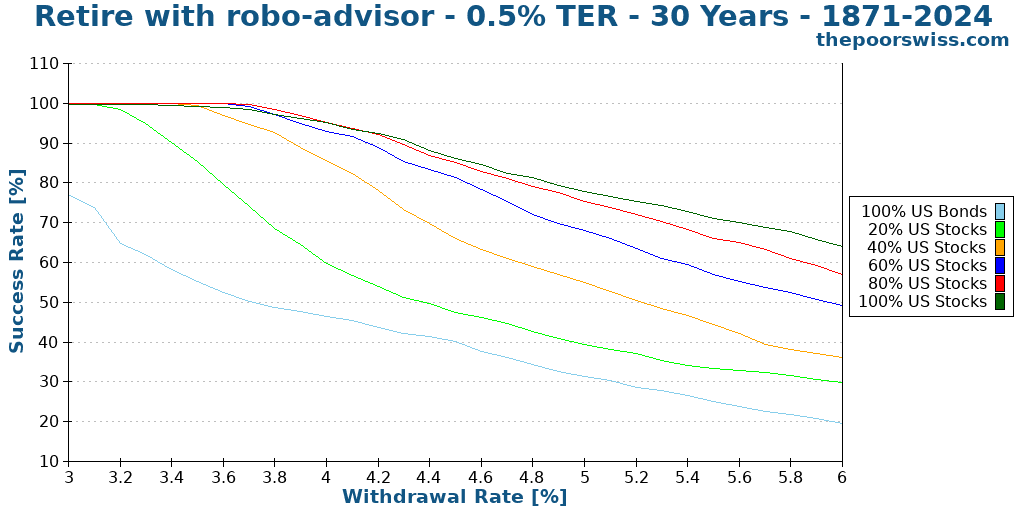

So, here is what happens when we jump over to 30 years.

This time, the results are starting to become more interesting. Even at a 4% withdrawal rate, portfolios with 100% bonds and 20% stocks would fare poorly.

Moreover, we can see that any withdrawal rate higher than 5% would also perform poorly. Therefore, we should remove a few options to make the chart easier to read.

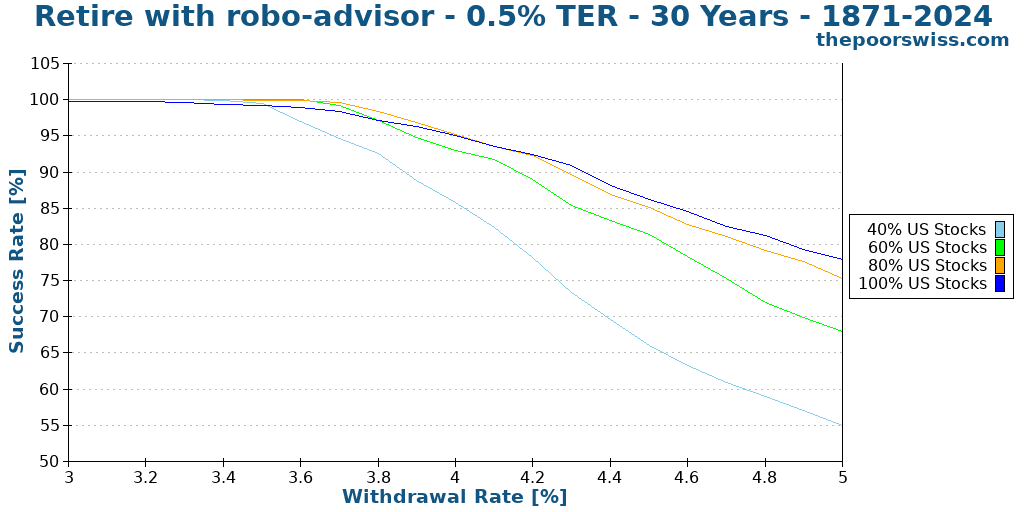

This is more interesting and focuses on more reasonable simulations. From this point on, we will not show higher withdrawal rates and portfolios with less than 40% stocks. We can see that even a portfolio with 40% of stocks would not perform well.

On the other hand, the three other portfolios still have more than a 90% chance of success at a 4% withdrawal rate over 30 years. These are excellent results. However, if you want to retire early, you will need more than 30 years, so we can see what happens for 40 years.

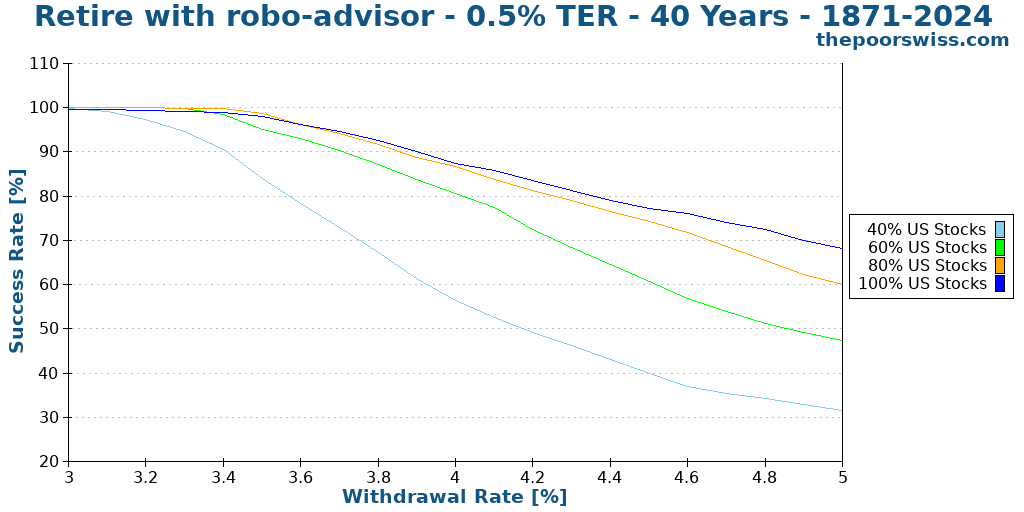

At 40 years, sustaining the withdrawal rate of 4% is becoming more difficult. At this point, none of the portfolios would have more than a 90% success rate, which is likely too low for most people. 90% is my threshold for a success rate. However, portfolios with a large stock allocation would still perform quite well at a 3.50% withdrawal rate.

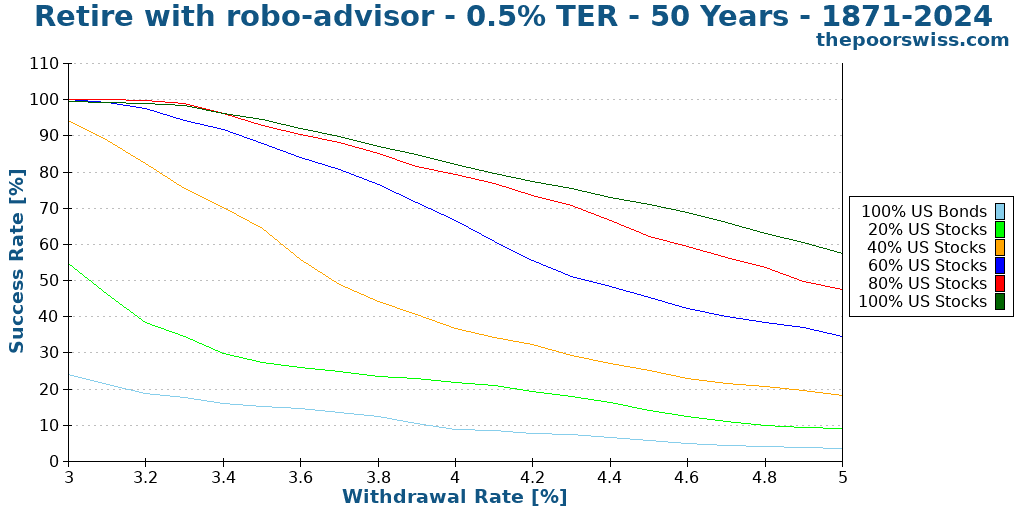

Finally, we look at 50 years.

There are no huge differences between 40 and 50 years. All success rates are lower. Both 80% and 100% stock portfolios would still perform well at a 3.5% withdrawal rate.

So, this shows it is possible to retire early with a robo-advisor at a 0.50% fee, but you would use a lower withdrawal rate, increasing the amount of money you need to accumulate.

But how does this compare exactly with lower TER? And with a higher TER? We will find out.

Different fees

I have chosen six different fees to compare with a 100% stocks portfolio:

- 0.10% and 0.20% as examples of DIY investing

- 0.50%, 0.60%, and 0.70% of examples of investing with a good robo-advisor

- 1.00% as an example of investing with an expensive robo-advisor

Of course, I could take many more fees, but this is a reasonable sample that will keep graphs readable.

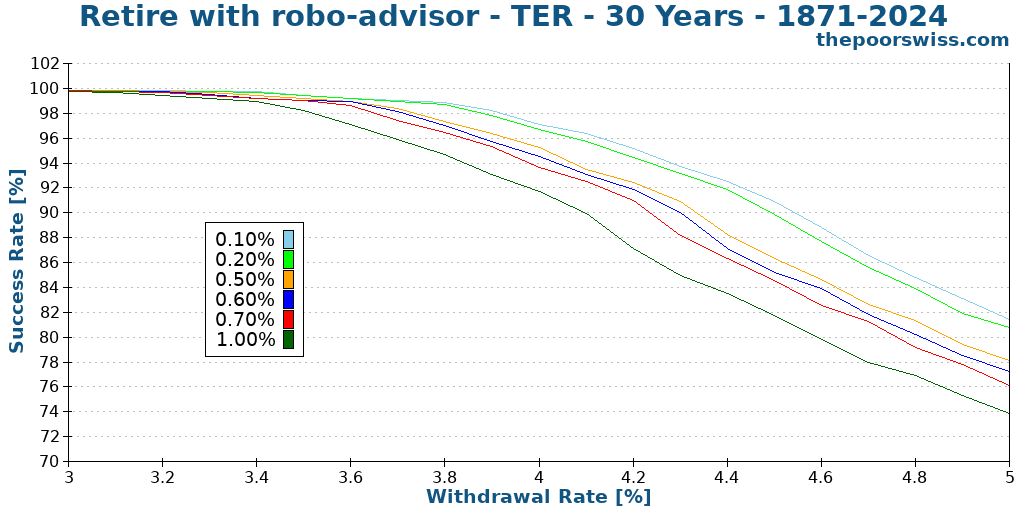

So, here is what happens over 30 years with these different fees.

As expected, each increase in TER decreases the success rate. It’s also interesting to note that the impact is relatively low at a 3.5% withdrawal rate. But as we increase the withdrawal rate, the fees’ negative effect also increases.

This means that lower withdrawal rates can tolerate higher fees. This makes sense since lower withdrawal rates have a higher margin for error.

At a 3.5% withdrawal rate, the difference between a 0.1% TER and a 1.0% TER is only a 1.1% chance of success. But at a 4% withdrawal rate, the difference is already 5.5%! And at 4.5%, it becomes 9%. So, the price you pay in fees can be pretty significant to your success rate.

At a 4% withdrawal rate, all the different TERs still have a 90% chance of success. However, three (the lowest three) have a 95% chance of success.

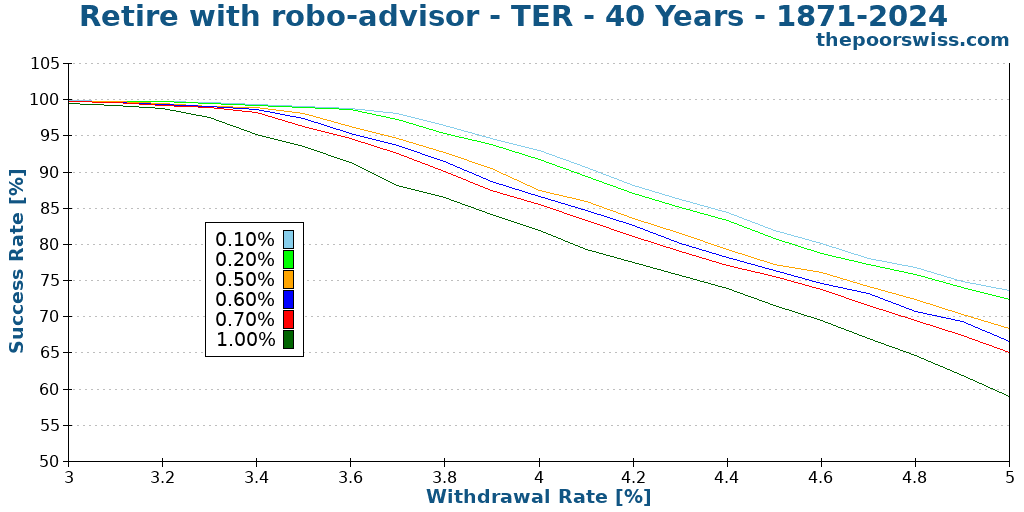

Here is how this plays out after 40 years of retirement.

Another thing that we can observe is fees are more impactful at 30 than at 40 years. So, as we increase the retirement period, the negative effect of fees increases as well.

Once again, this makes sense since a more extended retirement period has a lower margin for error.

At a 3.5% withdrawal rate, the difference between a 0.1% TER and a 1.0% TER is already a 5.7% reduction in success rate! At 4%, it becomes 11% already!

Only the DIY investing fees have more than a 90% chance of success at a 4% withdrawal rate. Nevertheless, they all have more than a 90% chance of success at 3.50%, and only the 1.0% TER has less than a 95% chance!

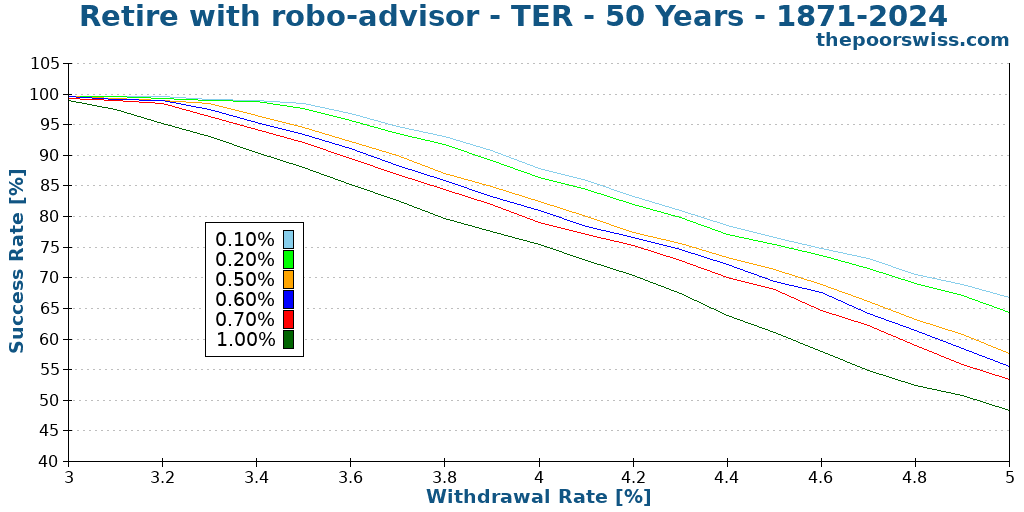

Finally, we look at 50 years of retirement.

Again, the differences are becoming more pronounced. None of the different TER would have more than a 90% chance of success at a 4% withdrawal rate.

At a 3.5% withdrawal rate, only DIY investing would have more than a 95% chance of success, and 1% TER would not even have a 90% chance of success. The difference between 0.1% and 1.0% TER is a staggering 11% lower chance of success!

This very significant difference shows that investing fees are significant.

Nevertheless, this also strongly suggests that we can retire early with a robo-advisor. We only need to be more conservative.

Terminal values with a robo-advisor

The original Trinity study includes terminal values for different scenarios. We can do the same for robo-advisor fees.

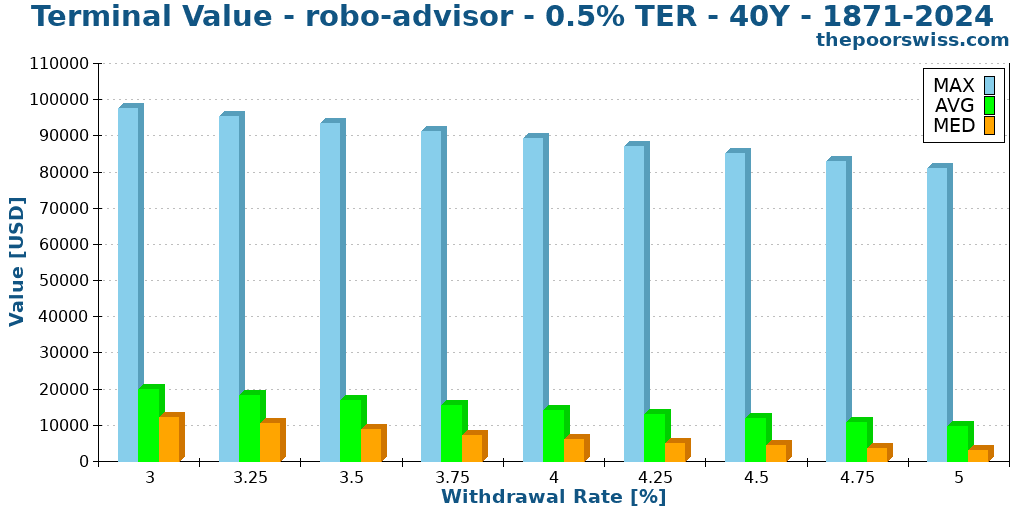

First, we can look at the terminal values of a 100% stock portfolio after 40 years, with a 0.50% fee.

We can see that even with a 0.50% TER, we would still have much money at the end of the 40 years. I have not shown the minimum value since it would always be zero.

With a 4% withdrawal rate, we would still end up with more than 13,000 USD on average, and even the median value would be about 5,700 USD. These are very high numbers.

If these numbers seem too high, remember that this is not only the money you pay in fees. This is also money that does not stay in the stock market and cannot grow. So, all the fees you pay have a considerable opportunity cost.

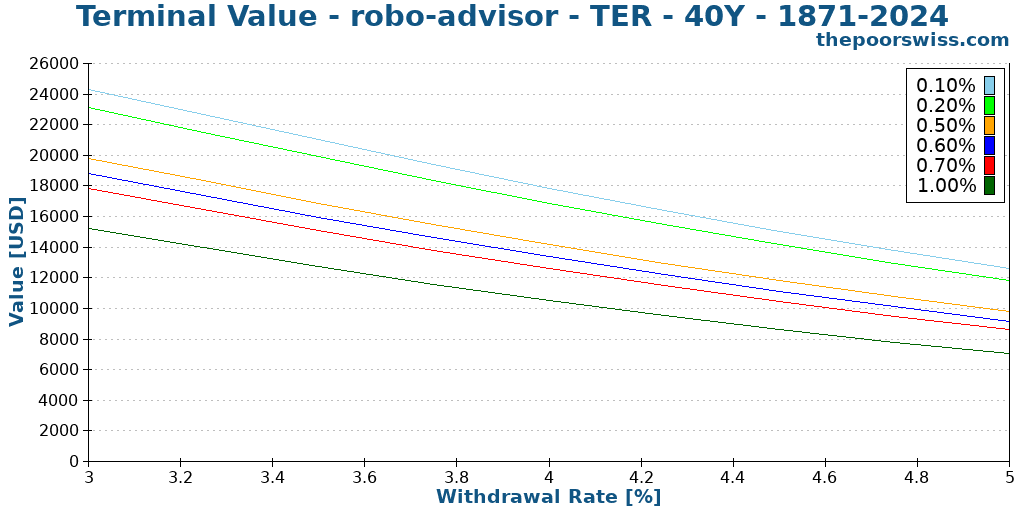

We can also see the difference between different levels of fees. I show the average between our different fees after 40 years with the 100% stocks portfolio.

We can see that the differences between the different fees are very significant. For instance, at a 3.50% withdrawal rate, the difference between the 0.1% fee and the 0.5% fee is 4038 USD for each 1000 USD in the initial portfolio. We are talking about potentially millions lost to fees!

So, if you want to leave your heirs a legacy, you do not want to pay high fees!

Worst duration with a robo-advisor

Finally, we should also see the impact of fees on the worst duration. Most people only consider the success rate metric, but the worst duration is another interesting metric.

The worst duration is how early a scenario can fail (deplete the money). For instance, a scenario may fail after only 200 months but have a slightly better chance of success than another scenario that may only fail after 400 months. In this case, it is essential to balance both metrics.

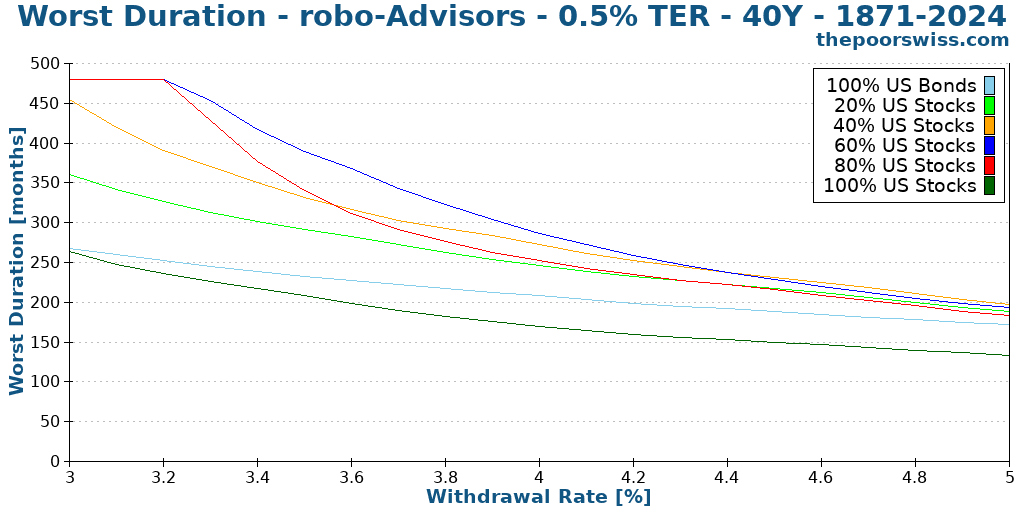

So, here is the worst duration over 50 years with a 0.50% fee.

There is nothing astounding in this result. The portfolio with 100% stocks is the worst for this metric, closely followed by the portfolio with 100% bonds. Having 20% and 40% bonds works better if you want to optimize for the worst duration.

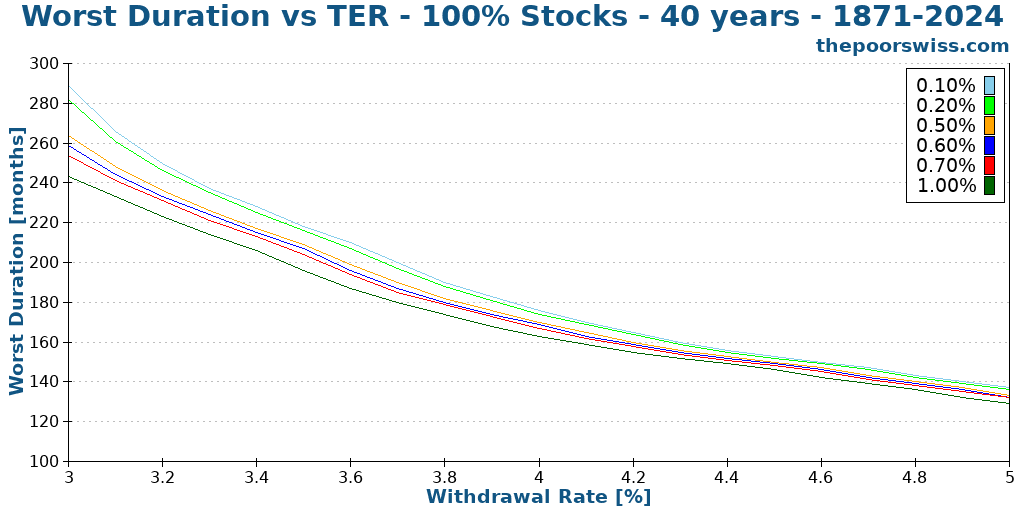

But more interestingly, we can compare the same portfolio with different levels of fees, starting with a portfolio with 100% stocks.

We can see that the differences are not huge between the worst and the best fees. Nevertheless, the differences are not negligible either.

At a 3.50% withdrawal rate, the portfolio could fail 22 months earlier if increasing the fee from 0.1% to 1.0% and nine months earlier if increasing the fee from 0.1% to 0.5%.

At a 4% withdrawal rate, the portfolio could fail 13 months earlier if increasing the fee to 1.0% and months earlier if increasing to 0.5%.

These decreases do not seem dramatic, but we have to remember that the worst duration of a 100% stock portfolio is already bad. So, we are making a bad situation worse.

Finally, we can see with an 80% stocks portfolio instead, since this portfolio has a much higher worst duration.

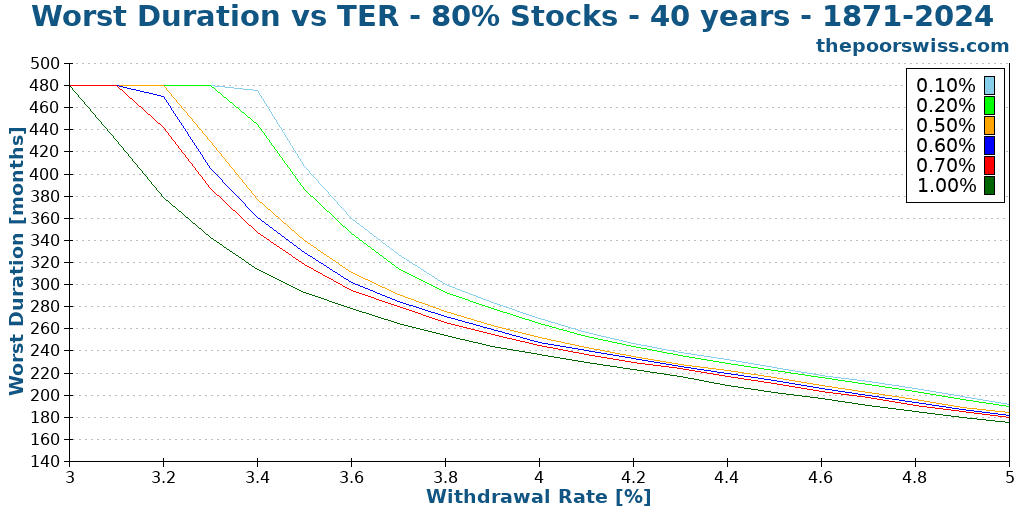

With this portfolio, the differences are much more significant. Using a robo-advisor can make your portfolio fail much earlier.

At a 3% withdrawal rate, a 1.0% fee can fail 81 months earlier! At a 3.5% withdrawal rate, this fee can make it fail 134 months earlier; that’s 11 years! Even at a 4.0% withdrawal rate, you can still fail 36 months earlier.

And even a 0.5% fee can make a significant difference. At a 3.50% withdrawal rate, a 0.5% TER can fail 79 months earlier than a 0.1% TER.

So, it is essential to realize that the higher fees of a robo-advisor can make your retirement run out of money faster than if you were investing by yourself.

Conclusion

Returning to the original question: Can you retire early with a robo-advisor? Yes, but retiring early with a robo-advisor means compromising on your retirement.

With a robo-advisor, you will have significantly higher fees than when investing directly by yourself. These higher fees will mean several things:

- Your chances of success will be lower than if your fees were lower.

- Your portfolio can fail earlier if you have higher fees.

- You will have to use a lower withdrawal rate, increasing the money you need to accumulate.

That does not mean it is impossible, but you must be aware of the impact of the higher fees. And you need to choose a robo-advisor with reasonable fees. I would not recommend paying more than 0.7% for a robo-advisor in retirement. The difference between a 0.5% and a 1.0% fee is significant already.

It also does not mean a robo-advisor is bad. In fact, for small amounts of money, robo-advisors can be cheaper than brokers.

I still recommend investing by yourself in most cases. It is not as difficult as people believe, and you can significantly reduce your fees. If you want to retire early, read how to implement the Trinity Study.

What about you? Are you planning to retire early? How?

More reading

The best and worst times to retire early

Timing is everything. We look at historical data to find the best and worst times to retire early and how market valuations predict success.

Equity Glidepaths in Retirement

Reduce sequence risk. Learn how an Equity Glidepath (increasing stocks after retiring) can improve your portfolio's survival rate.

How to retire early in Switzerland?

FIRE in Switzerland? A complete guide to retiring early in Switzerland, including cost of living, taxes, and healthcare considerations.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Roboadvisor or not, FIRE is dying. It took only a short time of market going sideways and a lot of “retired” people are looking for jobs. Not working for ten years or longer makes you virtually unemployable. I know a few of them who asked me about a job. Even the Financial Samurai (the .com one) is going back to work.

Hi Peter,

I would not say FIRE is dying, but easy FIRE is going away indeed. I think this is a good thing, because many people FIREd with high withdrawal rates thinking that bull markets would last forever and their expenses would never change.

And you make an excellent point that not working for 10 years (or even shorter) will really limit your opportunities.

I did not know that Sam was going back to work. But it’s quite surprising. He’s making 200K USD a year of “passive income” and retired with 3 million USD only 10 years ago. I don’t see how he needs to go back to work.

It is exactly what you say. The people thought the bull markets from the last years will take forever and their expenses will never change. Add the rampant inflation and even the die hard optimist will feel something is not right. I told a still “retired” guy about the T-Bills paying 5% and he laughed into my face… these guys expect (or better said were expecting) 15-20% over the years…

Sam has an additional issue on the spending site. The articles telling about how to scrap by on 500k a year weren’t merely ironic or fiction. Paying 1.5 mil for his kids college is imho an unnecessary luxury. After one year of work, it’s mostly irrelevant to which college you went. He’s already started keeping up with the Jones – expensive kindergarden, etc. Now it seems he is slowly waking up.

Yeah, some people in the US expect crazy returns every year :(

And I also do not understand why he wants that either. My son is going to public school like I did, and I am doing quite well, I believe.