Can flexibility help your early retirement?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

If you are planning your early retirement, chances are that you will base it on the Trinity Study technique. With this strategy, you will withdraw each year a percentage of your initial portfolio, adjusted for inflation only.

Some people want to use a higher withdrawal and claim this works because they can be more flexible. Is that really the case? Can flexibility help your early retirement? We will answer this question by doing some simulations with some flexibility strategies.

What is flexibility?

Let’s start with a quick definition of what people mean with flexibility. We are talking here about being flexible with expenses. If you can reduce your expenses by 10%, this is a nice level of flexibility.

The idea of flexibility in early retirement is that when things are going well, we can spend more. And when things are not doing well, we must spend less (exercise our flexibility). That way, we can effectively reduce our withdrawals and increase our chances of success.

But when do we need to be flexible? That is the main issue. We do not know the future. So, we need to rely on heuristics. And heuristics have two issues:

- The flexibility heuristics may not make us flexible enough.

- The flexibility heuristics may make us spend too little.

And the problem is that if we optimize the heuristic for one case, we worsen it for the other case. So, having a good heuristic is very difficult. We will explore two heuristics in this article, but there are many more available.

The simulations

If you are not familiar with how I run simulations, I encourage you to take a look at my updated Trinity Study results.

In this simulation, I will assume the following variables:

- I will use the returns from US stocks and bonds

- I will use data from 1871 to 2023

- I will use monthly returns in all my simulations

- Each starting month will be used as a simulation

- The withdrawals will be adjusted monthly for inflation

- We will assume 0.1% TER on the portfolio

- The portfolio will be rebalanced yearly

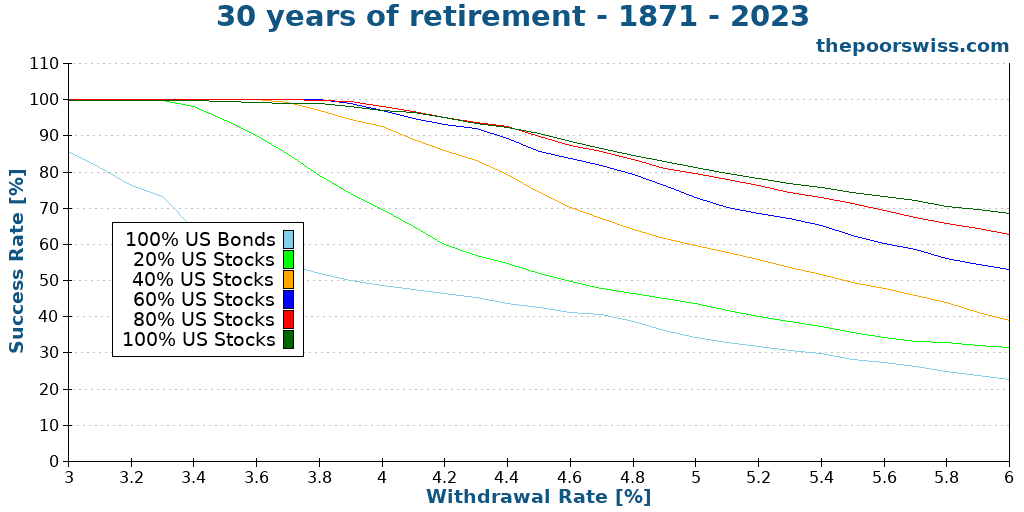

For reference, here are the standard results for multiple savings for 30 years of retirement:

Flexibility based on initial portfolio

The first strategy we can look at is to see whether we can compare the current portfolio value and the initial portfolio value to see and use this as a threshold to decide when to be flexible. For this, we will use two thresholds. At each of these thresholds, we will drop our expenses by a given percentage. For instance, one strategy could look like this:

- If the portfolio drops below 90% of the initial portfolio, we drop our spending by 10%

- If the portfolio drops below 80% of the initial portfolio, we drop our spending by 20%

With these, there are four parameters (the two thresholds and the two spending changes). I cannot test all combinations, so, we will try a few combinations and see what we can learn from the results.

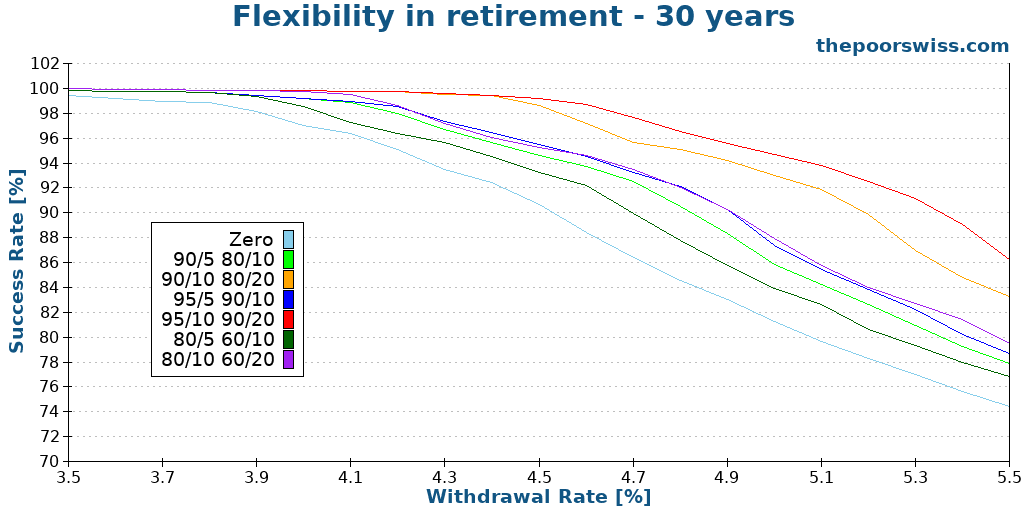

So, here are the results for 30 years of retirement, with various strategies. Zero is the reference with no flexibility. And the four numbers of the strategies, are the first threshold, the first change in spending, the second threshold and the last change in spending. All strategies are using a portfolio with 100% stocks.

We can see multiple interesting points from this first experiment. First, in all cases, flexibility helps our success rate. This finding makes sense since we are spending less. The second thing we can observe is that strategy where we drop 10% and 20% of our spending are more efficient than strategies where we drop 5% and 10%. Finally, given the same flexibility drop, dropping the expenses earlier increases our chances more than waiting.

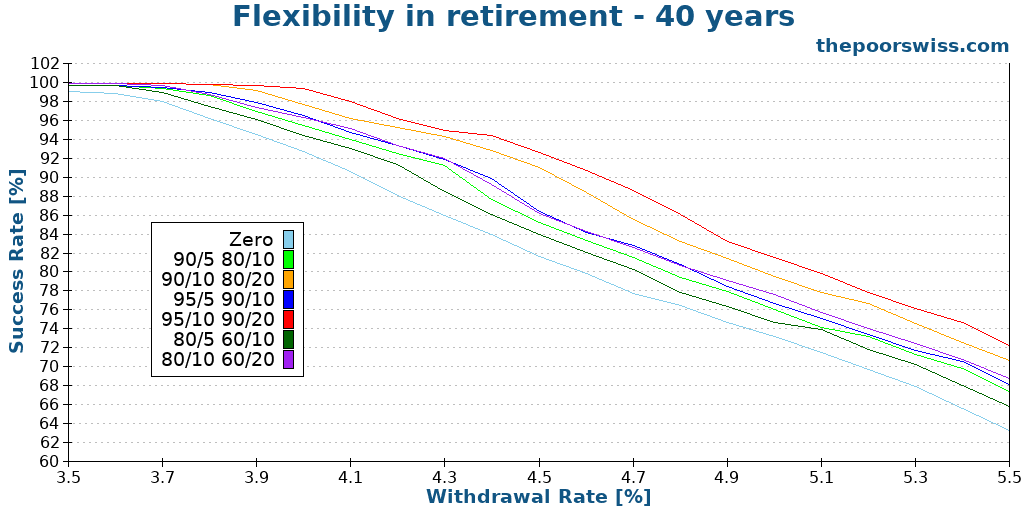

Since 30 years is a relatively short period, we can expand this to 40 years to see what happens.

We can draw the same conclusions on this graph. However, the different flexibility strategies are now less impactful than before. Indeed, the different between no flexibility and the best flexibility is lower than previously.

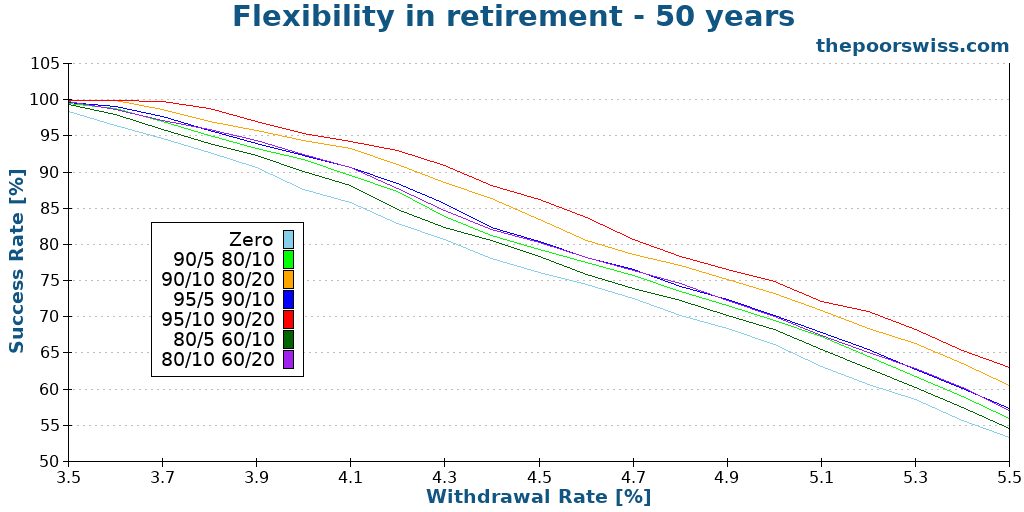

We can see if the same happens when we go over 50 years.

Interestingly, the difference between the best strategy and the strategy with no flexibility does not go down anymore. So, there is still a significant effect on success rate. Of course, once we go over some high withdrawal rates, the overall success rates are very low anyway.

Now, we must see if the flexibility rule itself works well. Being flexible is good when it is necessary, but it is not good when it is not because we just end up spending less for no reason. So, we must look at errors of the rule. By an error, I mean a simulation where we went flexible, but the simulation would have succeeded anyway without it.

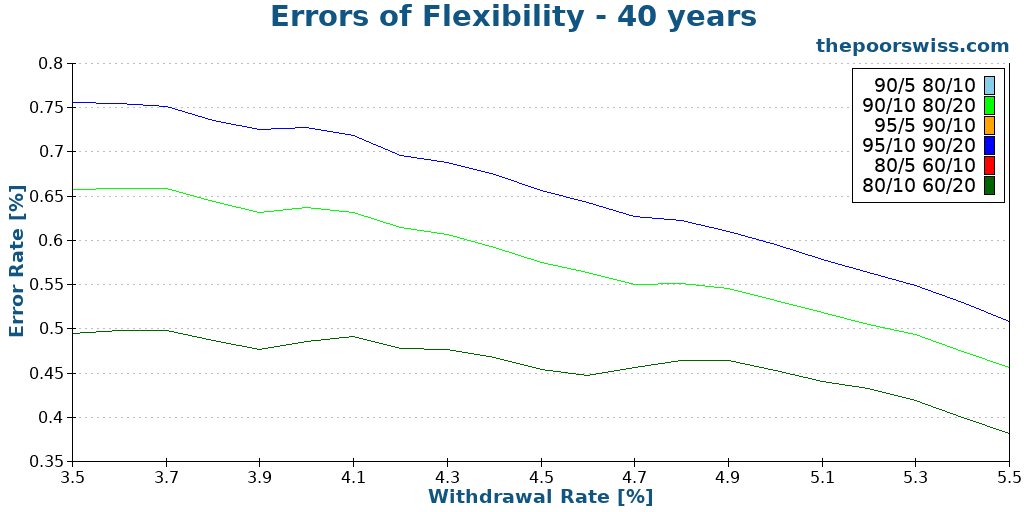

Therefore, here is the error rate over 40 years.

And here we can see the limits of this simple flexible heuristic: this strategy is often wrong. We have observed that we can significantly increase our success rate. But we can see that in numerous instances, we would reduce our spending for no good reason. The error rate depends on the two thresholds. The more aggressive (early) are the thresholds, the higher the error rate becomes. It also makes sense that the error rate decreases as the withdrawal rate increases, since the risk becomes higher. But even in the best case, we are talking about 40% error rates.

The good news is that the other kind of errors (not being flexible where we should have been) are very rare with this heuristic. This makes sense since this heuristic ends up being flexible a lot.

So, we would need a much better heuristic if we want to be flexible, or be ready to underspend a lot.

Flexibility based on market status

The second strategy is to use the market itself to see whether we are in a correction or in a bear market. A correction is when we are 10% below the previous historical high, and a bear market is when 20% below the previous high. Based on this status, we apply flexibility to our expenses to see how it would work. To be more flexible, we will apply the same thresholds as in the first example.

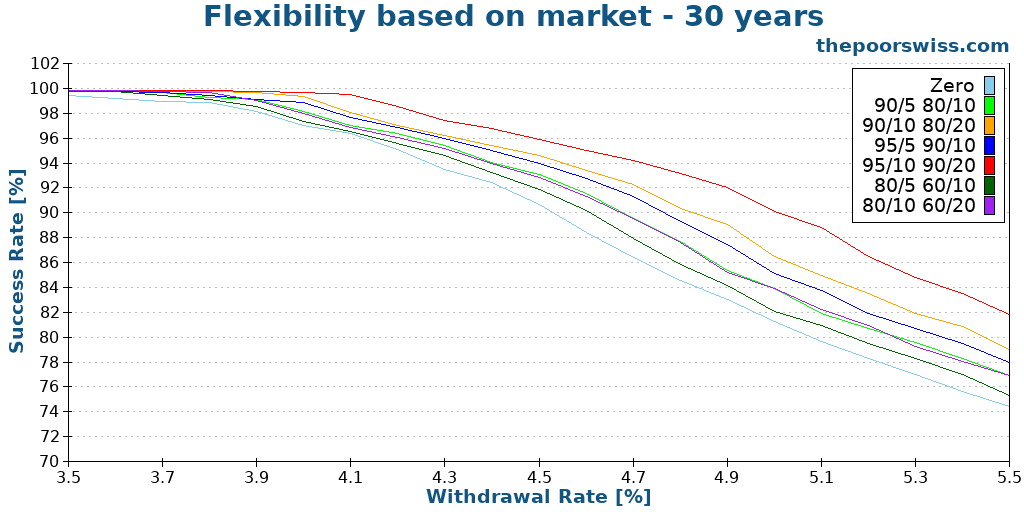

So, to start with, here are the results for 30 years of retirement, for our various strategies. The names are the same we used for the first strategy.

Again, all our strategies are doing better than the baseline. In this case, the impact of our strategies is lower than it was for the first strategy. Nevertheless, we can see still witness a nice improvement in success rate regardless of the strategy. As before, strategies that apply flexibility earlier are doing better than strategies that wait longer. And as before, the more we are willing to cut our expenses, the more we increase our chances of success.

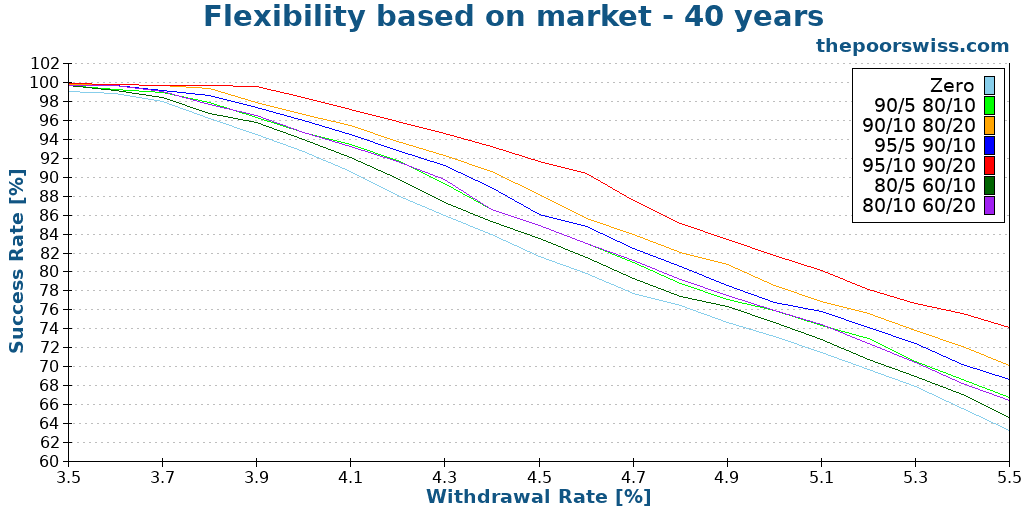

We can continue by increasing the retirement period to 40 years.

Interestingly, once we move over 40 years, we get better results than the first strategy. We could still get a 90% success with a 4.6% withdrawal rate in the best case. The zero-flexibility strategy would only get us to 4.1% withdrawal rate.

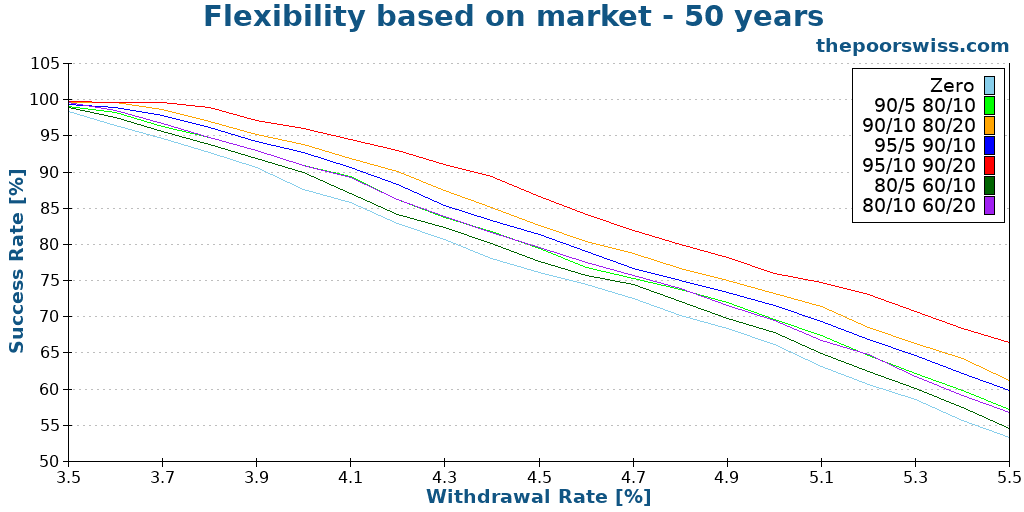

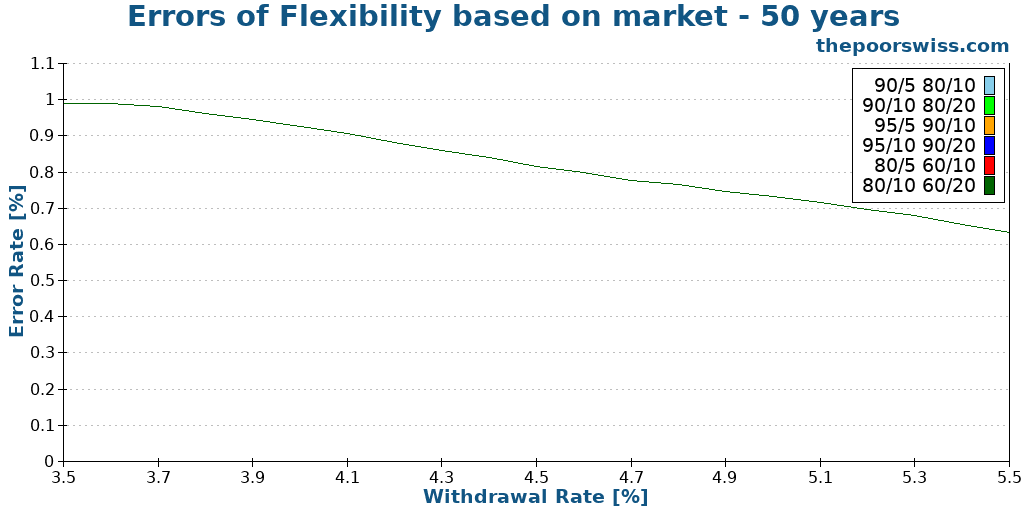

Finally, we can continue looking at the results for 50 years of retirement.

Again, the results are better than when using the first strategy. With a high withdrawal rate, the improvement in success rate is very large. We could use a 4.4% withdrawal rate and still get more than 90% success rate.

So far, it seems like this strategy is quite promising. Then, we should look at the error rate for this simulation.

The error rate for all the configurations is the same, so they all overlap.

Here is the secret to this strategy: it makes far too many errors. We reduce our spending in almost every simulation. The reason is simple: markets will always go up and down significantly over a 40-year period. So the likelihood of reducing spending is incredibly high. So, this strategy is almost the same as simply always reducing spending. It makes sense that it helps the success rate since we will effectively reduce spending most of the time. But it also means we will reduce spending when we do not need to.

Overall, this is a decent strategy, but it is worse than the previous one. With this strategy, we would have to reduce spending in too many cases. It is not precise enough to only consider the stock market. For instance, once we are in the past 10 years of the retirement, it is unlikely that a large decline in the stock market will hurt us because we probably have accumulated enough in the previous decades.

Therefore, I think this strategy is inferior to the first one. The only reason this strategy increases success rates higher is that it kicks in all the time.

Conclusion

Can flexibility of spending increase our success rate in retirement? Yes. However, it will also greatly reduce our spending in cases when we do not need it. In fact, it is very difficult to find a good heuristic to decide when to cut spending. And it is also very difficult to find by how much we should cut spending. We need a strategy that reduces spending when necessary and by a proper amount, and then does not reduce spending when it is not necessary.

The other issue is that once we rely on flexibility, we must be capable of holding this reduced spending for a while. There may be long periods where we spend significantly more than what was planned. And if we cannot keep that level of reduced spending, we end up in a situation where the success rate will be even worse than planned.

For me, the real issue is really that it is very difficult to find the proper heuristic to decide when to cut spending. If we could find an excellent heuristic that would kick at the proper time, it would be really helpful. In future articles, I will explore other strategies, and maybe we will find something interesting. From what we found in this article, this strategy should be based on the ratio between the current portfolio and the initial portfolio.

Meanwhile, I am not planning on introducing such strategies into my retirement plan.

If you are interested in this kind of articles, you may want to read more on variable withdrawal rate strategies, which also try to achieve something of the same sort.

As usual, if you have any idea for future articles about the Trinity study, please let me know in the comments below.

And you? What do you think about these flexibility strategies?

More reading

9 Things that are Wrong With FIRE

Is FIRE perfect? We discuss the common criticisms and downsides of the Financial Independence, Retire Early movement.

Retire Early: The Simple Guide – I wrote a book

I wrote a book, Retire Early: The Simple Guide, with Thomas Walke, another Swiss blogger. Our book is about the basics of early retirement.

Early retirement and social security

How can we factor social security into early retirement scenarios? Social security may be interesting, but it needs to be well planned.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste, Please enlighten me. I am clearly missing a point about the withdrawal rate.

Assuming that S&P would continue to return ~9% in the long term and we are starting with 1M CHF as the investment portfolio.

The trinity study shows that a withdrawal rate around 4% (30 years retirement) has a success rate close to 100% while at 6% around 70%. If I understand it right it was using the CPI for the US.

Now, taking the last 50 years into the account and looking at the avg inflation:

US:

1975–1984: 7.9%

1985–1994: 3.6%

1995–2004: 2.7%

2005–2014: 2.1%

2015–2024: 2.8%

Switzerland:

1975–1984: 3.64%

1985–1994: 2.86%

1995–2004: 0.96%

2005–2014: 0.48%

2015–2024: 0.53%

Would you agree that following the trinity study withdrawal rates is not entirely applicable to someone investing in the US but living in CH?

Taking a simplified approach: 1M*(9%-avgCH inflation of lets say 1.5%) = 75.000 of net income per year. That’s a 7.5% withdrawal rate and still on paper this should have a 100% safety.

Thank you for all your great work and helping so many people!

Jakub

Hi Jakub

You are missing two important points:

* Returns are not average. If you got a guaranteed average of even 7% per year, you could easily live off your portfolio with an aggressive portfolio. The problem is sequence of returns risk. You need to use a lower withdrawal rate for when the market does not go well. Retiring when the market only goes up is trivial. But retiring at the beginning of a bear market is all but trivial.

* Inflation is lower on Switzerland, yes. But the returns in CHF are lower as well. You need to account for USD/CHF and that have been going down historically and will eat some of your returns.

Got it, many thanks. One simply needs to wait for retirement until one can predict 5 juicy years in a row haha.

Ben’s video explains the sequence of returns risk nicely indeed: https://www.youtube.com/watch?v=QGzgsSXdPjo

Ben Felix just posted a video in line with this. “Sequence of Returns Risk’ in which he says that Amortization Based Spending or Flexible spending, addresses sequence of return risk head on.

There is an amortization formula that calculates the amount you can withdraw every year. This is considered optimal. It is a spending path that responds to changes in portfolio values, changes in expected returns and the remaining time horizon.

You posted about this before, in your Trinity Study analysis.

Hi Robert,

Yes, I watched that today. It’s interesting. It is very in line. He says that fighting sequence of returns risk is indeed better archived with spending adjustments rather than asset allocation strategies. This is interesting.

I want to try his method in the future to see how it works

Yeah would be interested to do some simulations based on your updated trinity study data.

In this method you need to guess expected returns. How will you do that reliable. Look at the big banks’ historical expected returns and how awful they have been about predicting what the future holds. I have come to the conclusion that we will withdraw 4% and adjust as time goes on. We have some flexibility but se don’t want to to die with large pile of money. It’s also impossible to even imagine what the next 30-50 years will bring to our lives. But I remain positive that we (or at least AI😄) will innovate and bring growth to the world. Even as the developed countries are getting old. Otherwise it wouldn’t make sense to invest to the world index.

You can still get around without estimating future returns. You can get the average return from the historical data. And then each year, you redo your ABW computation to get a spending plan for the future. And this is where the returns of the previous year will play, if they were higher than expected, you would get higher spending and lower spending otherwise.

But it still seems complicated to me and you would need to return the system every year I think.

Thanks.

I settled on the life cycle model, as it makes more sense to me and seems safer. The withdrawel variability is greatly reduce because portfolio fluctuations are modelled over the whole remaining lifespan. Check out the free TPAW planner.

Then again SWR with withdrawel flexibility makes sense to me too and adresses the risk of running out of money to soon if you have a bad sequence of returns.

Hi Dan,

Interesting, I need to read about the life cycle model. Thanks for sharing!

Hi Baptiste,

When you talk about a fixed withdrawal rate adjusted for inflation, how do you calculate inflation for a Swiss investor with mainly US ETFs and taking into account the exchange rate fluctuation (unfavorable in the long term)? I presume it’s the Swiss inflation rate plus the devaluation of the USD combined ….

Hi Max

In my simulations, I use US inflation. You would need to take Swiss inflation into account indeed, but this is lower than US inflation. And yes, a CH investor will need to take USD/CHF into account.

I have done a few simulations with that, but it’s difficult to get enough data: Can you retire early with Swiss Stocks and Bonds?