Interactive Brokers Review 2026: Pros & Cons

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Are you looking for a great broker? Look no further!

Interactive Brokers (IB) has all the features you need as a passive investor. Plus, their fees are almost unbeatable in the industry.

I have been using IB for several years and could not be more satisfied. They offer a wide range of products at excellent prices.

In this review, you will find all you need to know about Interactive Brokers, what you can do with IB, how much IB will cost you, and much more!

By the end of this review, you will know whether IB is a good broker for you!

| Custody Fees | 0% per year |

|---|---|

| Inactivity Fees | 0 CHF |

| Buy Swiss ETF | 5-15 CHF |

| Buy American Stock | 0.50 – 1 USD |

| Currency Exchange Fee | 2 USD |

| Languages | English, French, German, and Italian |

| Mobile Application | Yes |

| Web Application | Yes |

| Custodian Bank | 8 different US banks |

| Established | 1978 |

| Headquarters | United States |

What is Interactive Brokers?

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Interactive Brokers (IB) is a well-established brokerage firm (a broker) from the United States. IB was founded in 1978 already.

Today, Interactive Brokers is a huge brokerage company. They are the largest electronic brokerage firm in the United States. They are also leading the forex broker market. IB is also profitable, with over one billion US dollars in yearly revenue. IB employs more than 1500 employees worldwide.

IB offers access to stocks, bonds, options, futures, and other financial instruments on the leading stock exchange in the world. You will have access to all the investing instruments you will ever need. As of 2026, they offer access to more than 170 different markets in many countries.

If you are going to trade US bonds, it is worth mentioning that IB offers access to the US bond market 22 hours a day, 5 days a week. This makes it very available to buy US bonds during European hours.

So, here is precisely what IB offers as a broker.

Interactive Brokers Account Types

Interactive Brokers offers two types of accounts.

The default account type is the Cash account. With this account, you can only trade with the money you have in it. I am using this account type, which is good for most people.

The other account type is the Margin account. With this account, you can trade on margin, which means that you can buy stocks with money you do not have. So, IB will lend you money to trade on the stock market, and you will pay interest on the money loaned to you.

Generally, with margin accounts, you have a certain level of margin. For instance, if you have 10K cash and a 4:1 margin, you will have 40K available.

If you are interested in margin accounts, you should first read IB’s page on Margin accounts. You should also be careful about the risks of trading on margin.

For most people, a Cash account will be the best choice. If you do not know about margin accounts, do not consider getting a Margin account. You could lose a lot of money if you do not know what you are doing. On the other hand, if you know what you are doing and want to use leverage, you can choose a Margin account.

It is also worth noting that you can get a free trial. In this trial, you will get paper money. And you can simulate investments in the stock market with your paper money. This is a good way to start investing without putting any of your money. For many people, this is a good way to put them at ease with investments. Once they have mastered the account, they can seamlessly upgrade the free trial account to a live account and start trading for real.

Interactive Brokers Fees

In the long term, you need to reduce your fees. Investing fees are extremely important.

Interactive Brokers has two fee systems:

- Fixed Fee System

- Tiered Fee System

The fixed fee system is straightforward. You will pay a fixed fee for each exchange. For instance, you will pay 0.10% on transactions on the Swiss Stock Exchange (with a minimum of 10 CHF).

The tiered fee system is much more complicated. You pay individual fees, such as clearing fees, trade reporting fees, and transaction fees. The rules are different for each stock exchange.

The complexity of the tiered fee system turns many people away. However, for simple investors, the tiered system is often significantly cheaper. In most of my calculations, the tiered fee system was less expensive than the fixed system. So, if you want the lowest fees possible, you should generally opt for the tiered system.

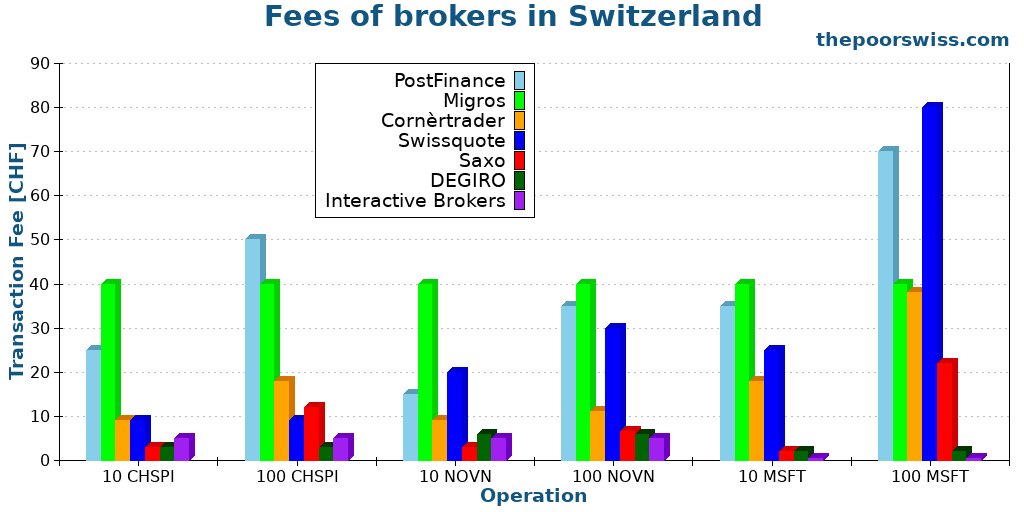

I will not go into details about all the fees of Interactive Brokers because they are complex. But overall, the fees of Interactive Brokers are really low. For instance, here is a comparison I did for the best brokers in Switzerland:

When you compare IB with other brokers available in Switzerland, we can see that the fees of Interactive Brokers are excellent. If you trade a few times per month, your costs will be really low!

We use Interactive Brokers as our primary broker because of its excellent fees and its wide access to ETFs.

Currency Conversion Fee

IB is doing currency conversion at the best rate available. However, conversions are not free.

If you are doing a manual conversion, you will pay 0.002% of the conversion, with a minimum of 2 USD. Unless you are doing massive conversions, you can assume you will pay 2 USD.

If you are letting IB do automated conversions (with a cash account only), you will pay 0.03% of the conversion size, without a minimum.

The automated system is cheaper for conversions below 6500 CHF, and manual conversions are cheaper after that.

Overall, these fees are incredibly cheap! This is among the best available fees for currency conversions. And this is orders of magnitude better than a Swiss broker.

However, it is worth mentioning that Interactive Brokers does not like accounts that are solely used for currency conversions, without investing. Some people had some features blocked on their accounts for doing that.

Custody and inactivity fees

Fortunately, there are no custody fees or inactivity fees at IB!

IB’s no custody fee advantage over most other brokers is fantastic! Not only do they have outstanding transaction fees, but having no custody fees is fantastic!

Cash Interest Rates

The interest rate on CHF cash was negative in the past. However, it has been growing steadily since 2023.

Currently, the interest rate on CHF balances is 0.0% (as of April 2025). And the interest rate on USD balances is 0.0% up to 10'000 USD and 4.080% above that (as of December 2024).

You can get the current interest rate on this page.

Other fees

One fee that is worth mentioning is the withdrawal fee. Indeed, you are only allowed one withdrawal per month. If you do more than one withdrawal in a month, you will pay for each one starting from the second one. Each paid withdrawal is 11 CHF for a CHF withdrawal, 8 EUR for an EUR withdrawal, and 10 USD for a USD withdrawal.

If you want to register your Swiss shares in the share register, you will have to pay 150 CHF. This is relatively expensive, even compared to Swiss brokers. However, this is something not everybody needs and is not necessary for each position. But if you are planning to register your shares, it is important to know this fee.

Opening an account with Interactive Brokers

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

Opening an account with Interactive Brokers is not complicated, but it will take some time. The procedure asks many questions and has many steps.

First, they will ask for general information about you (name, address, and such). You will also need to select the type of account you want. This choice is essential. This step is also where you will choose the base currency of your account.

The second step of the procedure is to provide financial information. IB will ask you how much money you have and how much experience you have with stocks. And you will have to choose which instruments you want to invest in. Do not worry too much since you can register for new investing instruments later.

The next step is about accepting the terms and conditions of Interactive Brokers. I would recommend at least skimming through them. After this, they will ask for proof of your identity and extra tax-related information.

Finally, you only need to fund your account for it to be complete. While this is not the most straightforward procedure, it is not too complicated.

If you want more information on the process, I have a guide on creating an Interactive Brokers account.

Subaccounts

It is worth mentioning that you can have subaccounts in your Interactive Brokers account. It means that you can manage several accounts in the same primary account.

The best usage of subaccounts is if you want to invest for your children and easily separate your stocks from theirs. Legally, the stocks are still yours since you cannot create accounts for minors. Nevertheless, it is good to see them separate. I have bought a share of VT every month for my son.

If you want further information, I have an article about investing in stocks for your children.

Using IB to trade

Interestingly, IB has many user interfaces:

- The standard web application

- The mobile application (IBKR Mobile)

- The WebTrader web interface

- The IBKR Desktop application, for Windows and Mac

- The Trading Workstation (TWS) desktop application

So, there should be an interface for everybody!

You can do most things from all interfaces. For instance, you can trade stocks from each of these interfaces. The problem with IB is that many people have been discussing the TWS interface. So, many beginners believe they should use it. However, the TWS interface is the most complicated of these interfaces by far.

I have never used the TWS application for trading. It is just too complicated for most investors. You only need the Account Management interface if you are a simple investor and invest in ETFs. If you prefer phones, you can also use the IBKR Mobile application to trade.

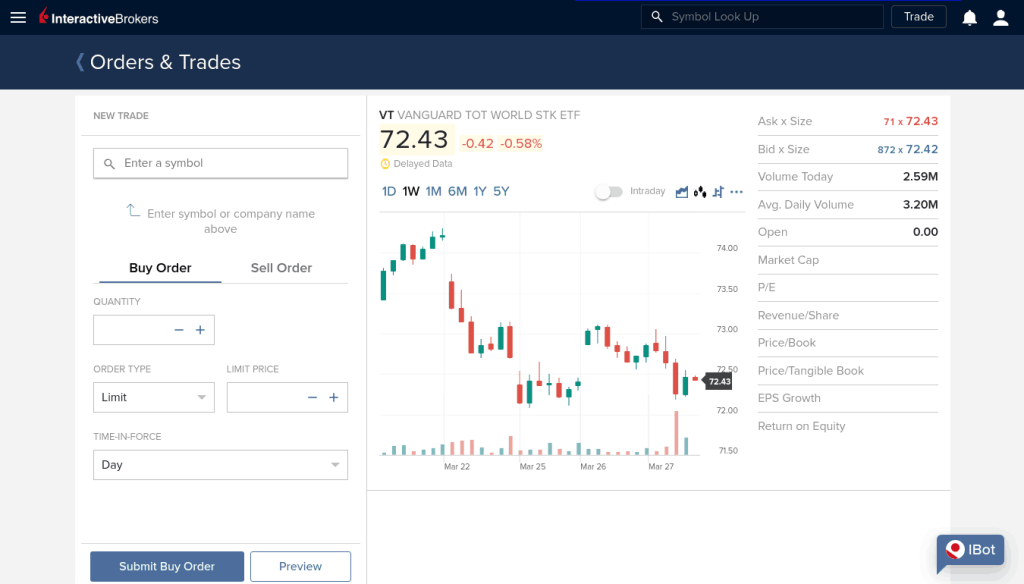

From account management, you can trade everything you want. And you can also transfer money to and from your account. All these operations are relatively simple.

You can fund your account for free with a bank transfer. First, you must declare your bank account in IB, and then you can make a deposit. Withdrawals work the same way. You can only send money to accounts in your name. I never had any issues with either deposits or withdrawals.

For currencies, you have multiple choices:

- You can do a forex trade directly. For instance, you could buy USD.CHF, which is buying USD with CHF.

- You can use the currency converter and let IB do the operation for you.

- Since April 2024, you can let IB do the currency conversion for you by buying shares in a currency you do not have. For instance, if you buy VT in USD and only have CHF, IB will do the conversion for you. This will only work on a cash account, since a margin account would go negative on the currency you do not have.

In any case, IB is outstanding at converting currencies. They use an excellent rate and have very low fees.

It is also worth noting that you can automate your investments with IB. You can set up standing orders starting weekly or monthly. If you use a recurring order for the transfer, you can entirely automate your investments. This feature is something some people are looking for.

If you want further instructions, I have a guide on how to fund your IB account and trade an ETF.

Other features

IBKR has some other interesting features.

I would like to mention the Stock Yield Enhancement Program. If you enable this option in the settings, IB can lend your shares to other investors. This system is called securities lending.

I like that IB shares 50% of the profit with you if you use that option. This sharing starkly contrasts with other brokers that would lend your shares to other people by default without giving you any profits.

I am not saying everybody should enable this option, but for me, this indicates that IB is a great broker.

Another interesting feature is that you can trade fractional shares. This feature allows you to buy fractions of shares. This feature is helpful if you want to buy some expensive shares or if you want to purchase many companies without having a large portfolio. You can read more about fractional trading at IB.

One thing that is missing from Interactive Brokers is the ability to register Swiss shares as a shareholder. Some people want to be registered so they can attend shareholder meetings and receive some gifts.

While IB itself does not provide e-tax statements, Datalevel AG, a Swiss company, is offering this service. With them, you can generate e-tax statements from your IB account.

Is IB safe?

If you invest significant money, you want your broker to be safe. So, we must look at the safety and security of IB.

Regulations

First, we can take a look at regulations.

Interactive Brokers has seven legal entities depending on the customers’ country. For instance, Interactive Brokers LLC works in the US, while Interactive Brokers (UK) Limited works for European clients.

Each of these entities is regulated. For instance, the US entity is regulated by the Securities and Exchange Commission (SEC), and the UK entity is regulated by the Financial Conduct Authority (FCA). So, overall, IB is extremely well-regulated.

Financial Strength

Currently, Interactive Brokers is considered very strong financially. They have a strong capital position and advanced risk controls.

The company manages over two million accounts and executes almost two million daily trades. These are substantial numbers showing that IB has many active users.

In April 2023, IB had over 7 billion USD above the regulatory capital they needed. The company invests mostly in the short term to ensure it has enough money to cover issues in the short term. So, IB’s money is not locked when it needs to be available.

Overall, Interactive Brokers’ financials are good. The company has not shown any signs of financial trouble.

Protections

Moreover, protection in case of bankruptcy is also critical. Even though IB is financially strong, we still want to know what would happen should it go bankrupt.

It is important to know that IB does not segregate each country. This means a Swiss investor using IB UK will use the same trading system as a US investor. This is great news for protection!

The SIPC will protect US investors. It protects your assets up to 500K USD, but it will only protect your cash up to 250K USD. And since Swiss investors are protected like US customers, we also get SIPC protection!

Now, there is an exception for some instruments. For instance, Contracts for Difference (CFDs) are prohibited in the United States. But they are offered to other investors. If you use them, the protection for your CFDs will fall to the FCA protection, up to 85K GBP.

Again, you have excellent protection against bankruptcy with Interactive Brokers. We have higher protection with IB than with a Swiss broker.

It is important to note that since Brexit, European investors have been using other entities of IB. In that case, the protection is worse since you will not get SIPC protection on stocks, only FCA. But Swiss investors still have SIPC protection. We should note that SIPC has a global limit of about 7.5 billion USD.

If you would like to learn more, I have an entire article about Interactive Brokers safety.

Technical security

Finally, technical security is also essential.

With Interactive Brokers, you will have strong technical security. All communications with the server are encrypted, but all honest brokers use encrypted traffic.

Most importantly, you can use Two-Factor Authentication for your account. You have two choices for that. First, you will be able to use the IBKR Mobile Application for that. Every time you log in from the web interface, you must confirm the login and enter one more code on your phone. But you can also use your standard TOTP application to generate a code. This second factor adds a great layer of security to your account.

So, Interactive Brokers has excellent security!

My Experience with IB

I started investing with Interactive Brokers when DEGIRO suddenly blocked access to US ETFs to Swiss Investors. Since then, I have been delighted with Interactive Brokers. I have been investing with IB for more than three years.

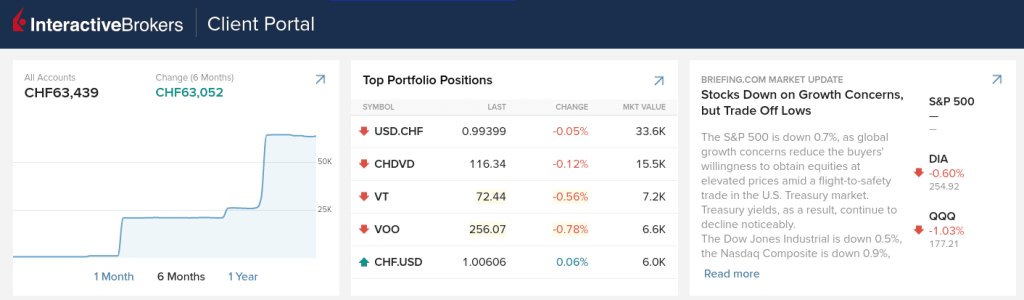

My entire stock portfolio is in my IB account. I buy new ETF shares every month from the default web interface, but I have also tried other interfaces. The IBKR Mobile application is very well done, but I generally prefer using my desktop computer rather than my phone.

I do everything from the Account Management interface, which suits all my needs. IB also fits my needs perfectly well. With time, I have learned to ignore most of the tool’s features. I only need a few features for my trading.

Since I sometimes get paid in USD, I can wire the money directly to my Interactive Brokers account. That way, I would not have to pay any currency exchange fees and could invest the money directly.

Overall, I am happy with my experience with IB. I never had an issue with the broker, and all my transfers reached IB very quickly. When I needed to withdraw money for the down payment on our house, I had no problems. All my trades have been flawlessly executed. The reporting on the web interface is also precisely what I need. I can only recommend IB!

IB Reputation

It is essential to look at a broker’s reputation before using it to invest in the stock market.

As a source of review, I always use TrustPilot. So, we look at the reviews of IB on TrustPilot. On average, users rate IB at 3.3 stars. Before looking at this, I was expecting a higher score.

First, we look at what people do not like about IB. We can categorize most of the negative reviews into two categories:

- Poor user interfaces. It takes a while to get used to the IB user interface. But after some time, it is straightforward to use.

- Poor customer service. It seems that many people have issues getting help from customer service. I cannot comment on that since I have never used their customer service. But I know people in Switzerland who did and have never had issues with them.

Overall, I am not too worried about these negative comments. A lot of them do not seem serious. And many commenters seem pissed off at making mistakes with the platform. But of course, it would be better if they are fewer negative reviews.

One good thing is that most reviews (39%) rate IB at five stars. So, we should also look at what positive reviews are saying:

- Excellent customer service. It is interesting to note that there are both negative and positive reviews of IB’s customer service.

- Excellent fee system

- Excellent order execution

- Good platforms

So, we can see that overall the reviews are mixed for IB. I think it comes from the fact that it takes a while to get used to it. Once you get used to it and focus only on the things you need, IB is quite simple to use.

Interactive Brokers Awards

One way to see how a broker is doing is to check out the awards they got from external sources. Over the years, Interactive Brokers has received many awards.

They received seven awards only in the year 2022:

- Best Online Brokers of 2022, by Barron’s

- Three awards from Investopedia, including best broker for international investing

- Several award titles from stockbrokers.com

- Several award titles from forexbrokers.com

- Several award titles from brokerchooser

While this is not the only thing that matters, awards are a good sign for Interactive Brokers.

Alternatives to Interactive Brokers

There are many alternatives out there.

The one that is the most interesting for a Swiss investor is DEGIRO. However, we should also compare IB with Swiss brokers.

Interactive Brokers vs Saxo

Start investing with a Swiss broker at incredible fees! Start trading with Saxo Bank and get 200 CHF in trading credits.

- Low currency conversion fee

- Swiss broker

Many Swiss investors prefer to use a Swiss broker. So, we should compare Interactive Brokers vs Saxo, my favorite online Swiss broker.

Both brokers have a ton of features, and simple investors will not miss a feature on either service. Both brokers offer access to US ETFs as well.

Saxo is the most affordable of the Swiss brokers. However, it will still be more expensive than IB. Neither of the two brokers has custody fees. The transaction fees are significantly higher at Saxo than at IB, especially on foreign stocks. Currency conversions are also cheaper at IB.

If you want to purely optimize your investing for fees, you should opt for Interactive Brokers. If you want to opt in for the cheapest Swiss broker and retain Swiss custody, you should opt for Saxo and accept higher fees.

Overall, both of these brokers are great and I am actually using both.

Interactive Brokers vs Swissquote

|

Best broker overall

|

Great Swiss Broker

|

|

Primary Rating:

5.0

|

Primary Rating:

4.5

|

|

Extremely cheap

|

Very affordable

|

|

Pros:

|

Pros:

|

|

Cons:

|

Cons:

|

- Outstanding prices

- Many investing instruments

- Excellent execution

- Access to US ETFs

- Good reputation

- A little intimidating at first

- Swiss broker

- Easy to use

- Many investing instruments

- Access to US ETFs

- Good reputation

- Expensive to trade US shares

- Expensive currency conversion

Another interesting Swiss broker is Swissquote, probably the most established Swiss broker. Both brokers offer access to US ETFs and have roughly the same features. If you are a simple passive investor like me, both brokers will have more than enough features for you.

You can trade with both brokers from your computer and your mobile phone or tablet. Swissquote is slightly easier to use than Interactive Brokers, but not by a long shot.

The main difference between these two brokers is price. If you use a stock exchange other than the Swiss Stock Exchange, IB is much cheaper than Swissquote. In some cases, IB can be 100 times cheaper than SQ. This difference can be very significant.

In addition, SQ has some custody fees, while IB has zero account management fees. So, if you are looking to optimize the price, IB is the clear winner.

For many investors, Swissquote will have the advantage of being in Switzerland. It may make it easier to deal with them if you have issues, while it could be complicated with IB. So, if you are looking for an affordable (not cheap) Swiss broker, Swissquote is an interesting alternative.

For more information, read my review of Swissquote or my comparison of Swissquote vs Interactive Brokers.

Interactive Brokers vs DEGIRO

|

My top pick

|

Good broker for Europe

|

|

5.0

|

4.0

|

|

No custody fees

|

Very affordable

|

|

|

|

|

- Great prices

- Many investing instruments

- Excellent execution

- Access to US ETFs

- A little intimidating at first

- Affordable

- Wide range of investing instruments

- Expensive currency conversions

- No access to US ETFs

- Lend your shares by default

For European investors, DEGIRO is another interesting alternative. So, it is interesting to compare these two brokers.

The first main difference between the two brokers is that only Interactive Brokers offers access to US ETFs to Swiss investors. This difference makes IB a much better choice than DEGIRO for Swiss investors. It will make a significant difference in the performance of your portfolio. If you invest with DEGIRO, you must invest in inferior European funds.

But we can also look at the fees of both brokers. There are a few differences between DEGIRO and IB:

- IB is much cheaper for the American Stock Market

- DEGIRO is very slightly cheaper for the European Stock Market

- IB is much cheaper for Foreign Exchange (FOREX)

There are a few differences in the features part as well. IB is also a FOREX broker, so you can hold many currencies in your account. And foreign currency exchanges are cheap. On the other hand, DEGIRO offers automatic currency exchanges when you buy and sell, but it is much more expensive than IB (unless you do small conversions).

You can also opt for manual currency conversions on DEGIRO, making currency conversions even more expensive. Overall, DEGIRO is not a great choice for trading currencies.

For the user interface, DEGIRO is slightly easier to use than IB. On the other hand, IB has many more features, but simple investors will likely not need many of these features.

Finally, IB was established in 1978, while DEGIRO only started offering brokerage accounts to retail investors in 2013. So, IB has more extensive experience.

So, overall, Interactive Brokers is a much better broker than DEGIRO. You will be able to access US ETF if you are Swiss. And you will be able to get excellent service at very low prices.

If you want more details, you can read my DEGIRO Review.

Interactive Brokers FAQ

What is the minimum deposit for Interactive Brokers?

There is no minimum deposit at Interactive Brokers. You can open an account without any money inside. Since there are no inactivity fees, this is perfectly fine for a small amount.

Is Interactive Brokers safe?

Yes. Interactive Brokers has been around for more than 40 years and has a great reputation. On top of that, it is well regulated in several different countries. Finally, your money is insured at Interactive Brokers for up to 500’000 USD, thanks to SIPC.

Is Interactive Brokers good for beginners?

Yes. While it is not the simplest broker out there, IB allows you to get started with little money and very low fees. The basic interface is simple enough to use and will allow you to do everything you need to start investing in the stock market.

What Interactive Brokers entity should I use?

As a Swiss investor, I recommend using the Interactive Brokers UK entity that offers the best regulations, protection, and features.

Who is Interactive Brokers good for?

Interactive Brokers is great for all investors that want to trade themselves and do not mind a foreign broker.

Who is Interactive Brokers not good for?

Interactive Brokers is not the best if you want to keep it very simple. If you are afraid of using a foreign, there are some Swiss alternatives, but at higher fees.

Can you use an IB account for currency conversions only?

No. IB may block your account if you use it only for currency conversions, without investing.

Can you register Swiss shares in your name with IB?

No, you cannot. Currently, it is not possible to register Swiss shares in your name as a shareholder with Interactive Brokers.

Interactive Brokers Summary

Interactive Brokers is an excellent broker with everything you need to buy stocks and ETFs, reliably and at extremely affordable prices. With IB, you can trade U.S. stocks for as little as 0.5 USD!

Product Brand: Interactive Brokers

5

Interactive Brokers Pros

Let's summarize the main advantages of Interactive Brokers:

- A vast range of investments

- Very low fees

- No custody or inactivity fees

- Very professional service

- Offers US ETFs to Swiss Investors

- Good overall reputation

- Long experience

- Excellent security

Interactive Brokers Cons

Let's summarize the main disadvantages of Interactive Brokers:

- It can be intimidating at first

- Too many user interfaces

- Cannot register Swiss shares as a shareholder

Conclusion

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Overall, Interactive Brokers is an excellent broker. Their fees are incredible, and their service is top-notch. Interactive Brokers should be your choice if you want a professional broker at a very fair price.

Since they are still offering US ETFs to Swiss investors (why US ETFs are the best), Interactive Brokers is currently the best broker for Swiss investors. No other broker even comes close if you want to optimize your portfolio.

I have been using Interactive Brokers for more than five years now. IB is the broker I am currently recommending to Swiss investors. It is also an excellent choice for European investors. I am pleased about IB and plan to continue using it for a long time.

Many people argue that we should not pay fees for brokers since there are free brokers. However, you have to be careful. There are many downsides to commission-free brokers. I much prefer paying very little for a great broker than not paying for a bad broker.

If you are interested in IB, I have a guide on opening an IB account.

What about you? What do you think of Interactive Brokers?

More reading

DEGIRO vs Interactive Brokers for European Portfolio: Who is cheaper in 2026?

In-depth analysis of who is cheapest: DEGIRO vs Interactive Brokers. We are considering European investment portfolios for Swiss and European investors.

Neon Invest vs Swissquote 2026 – Which is the best broker?

Neon Invest vs Swissquote. We compare the fees, ETF limits, and features to help you choose between the low-cost app and the established bank.

Cornèrtrader Review 2026 – Cheap Swiss broker

Honest review of Cornèrtrader, a very affordable Swiss broker: how good is it really? Is it really affordable? We will find out!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hello,

Thanks for the good explaination. Can I trade after hours on IB?

Thanks!

Mark

Hi Mark,

Yes, you can trade after hours with several instruments on the stock exchanges that allow it.

When you create an order, you can set an option to allow order to be filled outside of regular hours.

Thanks for stopping by!

Hi,

where did you find the information that from 100kUSD the Inactivity fee is waived? I don’t find it in their website, only in secondary sources.

https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&cad=rja&uact=8&ved=2ahUKEwiO_-P1jpvtAhVsMewKHQNMCJEQFjAEegQICBAC&url=https%3A%2F%2Fibkr.info%2Fnode%2F1287&usg=AOvVaw24aBqOp0WXLLDU0TNTxbWq

Thanks, César

Hi Cesar,

Good question!

It’s not in their pricing but in their account minimums documentation: https://www.interactivebrokers.co.uk/en/index.php?f=4969

Thanks for stopping by!

Why are you concerned about security of your assets and bankrupcy of IB? This company operates for DECADES, survived 2 major recessions in last 20 years (biggest after 1929 and 70s) and it seems it is growing even bigger. I don’t undrestand these fears, why lose sleep over something that it is so unlikely?

Hi small_potato,

I am definitely not losing sleep over that. IB is indeed a very strong broker, but that does not mean it’s infallible.

If you are planning to retire based on your portfolio, you still need to consider the risks. Currently, there is no alternative. But if one good alternative comes with higher protection, it could be interesting.

Thanks for stopping by!

What about opening an international account with SCHWAB? They are also US based, with the SIPC 500.000 USD. diverse selection of U.S. dollar-denominated stocks, options, bonds, ETFs…

Hi baseldon,

That could be a way to get back some protection. And looking at their fees, they are looking quite good.

However, it seems that they only handle USD, so it would be difficult for Swiss investors. And you probably can’t invest in Swiss ETFs.

But it’s a good option :)

Thanks for stopping by!

Great article and great information in the comments!

It sucks now that we are moved to IB lux and we have only €20.000 assets protection.

How someone could feel safe if has 300k-400k invested in IB?

I personally don’t have so much money invested there but I was planning to have in 25-30 years :)

Isn’t there a better option out there?

Hi,

It does suck indeed.

Unfortunately, there is currently no better option no. You could use several broker accounts in order to increase your coverage.

Thanks for stopping by!

Not entirely clear to me. The 20K asset protection is only for the CASH assets, correct?

So if you have 100K cash and everything goes belly up you will only get 20K back.

If you have 300-400K in STOCKS, those are ‘protected’ due to being in a custodial account, correct?

This applies to both, IB and deGiro.

The two main differences btw IB and deGiro are (1) trading with US ETFs is possible only on IB till 2021 for Euro ppl and (2) deGiro charges 3% on your dividends if you have their custodial account. And IB offers many more options..

Another question/thing: Since deGiro now merged with flatex and they are replacing their

MMFs with a Flatex Bank account you CASH now will be protected up to 100K. So wouldn’t deGiro in case of protection be a better option?

Thanks for taking the time and all your effort Mr.ThePoorSwiss!

Hi Schmakes,

Yes, 20k protection is only for cash.

Now, IB has 500K protection with IB UK, with a maximum of 250K in cash. And they have special SIPC protection for shares. This will protect you also against the misuse of your shares and theft. This is something that we are going to lose.

Regarding the merge with Flatex, I have no idea what will change, to be honest. It seems that if they have a real bank account, in each name, then yes, that protection will be better than IB’s.

Thanks for stopping by!

@Mr. The Poor Swiss

Did you transfer your assets you had with DEGIRO to IB? If so, how does that work in practice? I would imagine this has a lot of fees associated with it?

I currently have shares in my Postfinance but also Swissquote broker account and am contemplating moving everything to IB. Do you personally think to have assets with different brokers in terms of security makes more sense? Although I saw you wrote that the assets in IB are secured up to USD 500k so does that mean that if IB goes bankrupt that the assets would be transferred to another broker of choice?

I am always excited to receive your newsletter and read up on new content.

Hi Stefano,

I have an article about that. I have sold everything, transferred the cash and then bought back everything. But it was a bad idea. And I recommend people to pay a little more and use automated transfers. Unless it’s a tiny portfolio.

There are some advantages to diversification yes. Currently IB has the best protection. But this protection is likely to go away for us because of stupid Brexit. So, we have tiny protection again. For now, we still have good protection.

In any case, it depends on how much money we are talking about. If it’s 50K, it’s probably easier to have it in one broker. If it’s 500K, it may be another story.

Thanks for your kind words about my articles :)

Thank you for sharing your other article. I am definitely considering the automatic transfer!

Can you elaborate a bit more on the change in protection and what that means? Also on this article in the comments section https://thepoorswiss.com/change-broker-transfer-portfolio/ I have read that due to PRIIPS regulations Swiss people will soon not be able to buy American issued ETFs anymore? I have not found anything on the web pointing to that.

IB UK has a special status where we get SIPC (US) protection for our assets. This is a 500K protection in case of bankruptcy. But if we are moved to IB IE, for instance, we will get the standard protection which is 20K. So, in the case of bankruptcy, we will have a hard time getting money back.

But we can see it that way: We will have the same protection as the other EU brokers.

Regarding regulations, we are not impacted by PRIIPS, but by a similar set of laws for Switzerland. It’s not entirely clear, but the current consensus is that we will lose access to U.S. ETFs in 2022.

Thanks for stopping by!

A question on the topic of protection: would shares/etf’s i hold with ibkr end up in the ibkr’s bankruptcy estate if they would go bankrupt?

Hi Michael,

That’s a good question.

No, they would not. With IB, your shares are hold in your name, in a separate legal entity. So nobody else can claim your assets. In case of bankruptcy, you would be able, in theory, to transfer your shares to another broker.

There are some exceptions: If you lend your shares, or if you have a partial share (half a share for instance). But in general, the protection is quite good at IB.

Now, if it goes bankrupt, you may have to wait a while to get back your shares, but it should still happen.

Thanks for stopping by!

Hey

Are you sure that IB holds assets in you name and not theirs? If this is the case the protection being lowered to 20k is not really an issue as long as one does not store more than 20k in cash at IB right?

Is that the case for Degiro as well?

Could you provide a source of that?

Thanks!

Hi Kev,

It’s not exactly in your name indeed. They do not have an account for each of their investors. Brokers use big accounts called omnibus account. This account is a pool of all the shares of IB investors, with an account of who owns what.

But this omnibus is not owned by the main IB entity, but by a secondary entity. This separation allows assets to be protected in case of bankruptcy of the broker.

DEGIRO uses a similar system.

Thanks for stopping by!

So then the 20k security limit only becomes an issue if both IB/Degiro and the secondary entity go broke at the same time and one stores more than 20k in cash?

Where can such information, which is kind of important in my eyes, be found? I tried on the homepage of both brokers but did not really find anything definite.

Hi Kev,

In theory, the second entity cannot go bankrupt since it does no activity. The problem could arise if DEGIRO or IB does not do their job properly with this second entity. But it should be regulated.

But it could take a long time to recover the investments.

It’s really painful to find information about that. DEGIRO has some information here: https://www.degiro.co.uk/helpcenter/faq/safety/1112

I have an article about this coming this month, hopefully this will help clear this up.

Thanks for stopping by!

Are you sure that IB holds the assets in the clients name?

Is that the same for Degrio?

If yes then the reduction of security to 20k should not be an issue as long as one does not store more than 20k in the broker account right?

Could you provide a source for this statement?

Thanks a lot!

Hey, good and interesting post, I use degiro holding 4Etfs, what do you mean by “It means that if you invest with DEGIRO, you will have to invest in inferior European funds” why inferior? Gruess, Oli

Hi Oli,

European ETFs are not that bad, but they have two disadvantages:

* Their TER is generally higher

* You lose on American Dividends since 30% of these dividends are withhold at source. If you have an American ETF, you can reclaim half of the withholding (15% of the U.S. Dividends). This is like a 0.30% reduction in fees for U.S. stocks.

Thanks for stopping by!

How can this be true on European ETFs?

* You lose on American Dividends since 30% of these dividends are withhold at source. If you have an American ETF, you can reclaim half of the withholding (15% of the U.S. Dividends).”

If you are holding UCITS ETFs in a diversified portfolio, it’s impossible not to own American stocks. But that’s why you have to fill in the W8BEN form at any broker, so that they can calculate your withholding tax dependent on your country’s tax treaty with US.

Or am I missing something?

Hi,

It’s indeed impossible not to own U.S. stocks in a diversified portfolio.

But you are indeed missing something. A W8-BEN is only useful when you hold U.S. Stocks or U.S. ETFs directly. It’s not useful if you own U.S. stocks via a non-US ETFs like an UCITS ETF.

The dividends are withheld at the source by the U.S. government. It means that these dividend are lost before they reach the UCITS ETF. If you have a U.S. ETF, you can get back half of the dividends that were withheld with a W8-BEN, but only with an U.S. ETF.

Hope it’s clearer now :)

:) Yes, it’s more clear now…but then why does everybody say that it’s better to hold accumulating ETFs as opposed to distributing ETFs? In distributing case, I loose the trading commission when I buy with dividends money but I gain 20% back from the dividend tax…

Hi,

For several reasons:

1) There is (almost?) no accumulating ETFs in the U.S., so these people are talking about European ETFs

2) In some European countries, it is more tax-efficient to own accumulating ETFs rather than distributing ETFs. It’s not the case in Switzerland.

I prefer distributing and since I invest in U.S. Funds, I do not really have choice anyway ;)

Thanks for stopping by!

One more addition :)

I think that you don’t always loose 30% on the dividend tax as most UCITS ETFs are domiciled in Ireland and I do believe Ireland has a 15% tax treaty with US. So…at least there’s that :)

Cheers.

It’s true, Ireland funds are the next best thing. You also save on the 15% dividends. But you cannot reclaim the lost 15%. But they are indeed better than other countries without a tax treaty with the U.S.!

Hi,

Just found your blog and finding it quite useful so thanks for the effort.

Did you have any issues withdrawing funds? I’ve heard a lot of complaints about IKBR happily accepting funds but making withdrawals problematic (globally).

Thanks a lot

Hi Mariusz,

No, I have never had any issues. We recently had to withdraw a ton of money for our downpayment et there was no issue at all.

I have actually never heard complaints about this. Overall, it’s a very respectable, I would be surprised if they make any difficulty, on purpose, to withdraw money.

Thanks for stopping by!

Hi there,

Just got an email from IB UK that, due to brexit, they will need to move my account to Ireland, Luxembourg or Hungary.

“Over the next few weeks, IBKR will be seeking your permission to transfer your account U**** from IBUK to one of the IBKR brokers based in the European Union. We will specify, in our next communication, whether your account is eligible for transfer to IBIE, IBLUX or IBCE (“EU Brokers”).

Do you have any thoughts on this? What would you choose and why?

Thanks

P.S.: I’m from Romania

Hi IronM,

I honestly have no thought about that. I would probably choose IE or LUX from the top of my head, but I do not know the difference.

What you can check is the difference in asset protection between these three IB subsidiaries. This should be the only difference.

Thanks for sharing this! It’s interesting to know that European investors are going to get moved.

I received that communication about accounts being moved either to Luxembourg or Ireland. The ‘asset protection’ topic is covered in the final question and it doesn’t sound good:

“Currently, provided they meet eligibility requirements, IBUK clients may be protected in relation to investment services under the UK Financial Services Compensation Scheme (“UK FSCS”) at an amount of up to £50,000. As IBUK clients are carried by our US broker, IBL, the securities segment of their account may be eligible for insurance by the Securities Investor Protection Corporation (“SIPC”) at an amount of up to USD 500,000 (subject to a cash sublimit of USD 250,000).

Under the EU Brokers IBLUX, IBIE and IBCE eligible claimants may be entitled to claim compensation up to a maximum of EUR 20,000. More information on the applicable scheme, coverage and claim eligibility will be provided together with our request to transfer. “

Ìt seems indeed that the great protection from IB UK will be greatly reduced if we have to move to another provider of IB. That would indeed suck.

But according to the FAQ that you mentioned, this should only apply to citizens of the European Union, not clients from Switzerland. It may still change, but for now, it should not concern me.

Now, I do not think this makes IB any worse. The protection they were offering at IB UK was exceptional. And the protection they are offering in other countries is still acceptable even if minimal.

From https://retireinprogress.com/interactive-brokers-thanks-brexit-screw-you/ :

“I called the IB customer support and their representative told me that Swiss accounts will be moved to EU anyway.”

Hi Marcelo,

Yes, I have seen that, it really sucks…

There is unfortunately not much we can do about this. Even with lower security, it still remains an excellent broker.

Thanks for stopping by!

Hi, thank you for the article. Do you know if they offer non-Swiss Iban for funding? I need to fund part of my funds from Polish bank account and I was wondering if I can get some Polish Iban account number for finding. If you don’t know, I think you can try selecting it in options for funding – is there anything else than Swiss or UK account? Or maybe someone else knows,please?