How to invest for your children in 2026?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Even before my son was born, I knew I would invest for my children. Investing for your children is a great idea, and it makes a lot more sense than letting money rest in a bank account with very low interest rates.

However, until recently, I never worried about how to achieve that. Once my son was born, it was time to research the best way to invest for my children! And I found a great way to do so.

In this article, I share how you can invest for your children and what I will do for mine.

Why invest for your children?

First, you may wonder why invest for your children in the first place. That is a good question.

Most parents will gift some money over time to their children and then give it to them once they reach their majority (or any other specific age). In most cases, this money will end up in a bank account. The problem with that is that bank accounts have little to no returns. So, the money will slowly lose its value due to inflation.

The same reasons to invest that apply to you also apply to your children. We want to increase returns and avoid losing value to inflation.

Another reason to invest for my children is to teach them the value of investing. It may be naive, but I hope to teach my children how to handle their money properly. I will tell you in 20 years how it went!

I also plan to have a bank account for my children. In this bank account, I will deposit whatever he receives as gifts. I also prefer this to be separated.

Remember that you must pay net worth taxes on these assets as long as your children do not pay taxes. So, this is not a way to reduce your net worth taxes!

Decide on what to invest for your children

First, you must decide what you want to invest for your children. In this article, I am assuming you want to invest in stocks. But this technique would work with anything available on the stock market, including funds with real estate, crypto, or gold.

If you are thinking of investing for your children, you are likely to have a portfolio yourself. So, you could replicate your portfolio for your children.

Personally, our portfolio is very simple. It has only two ETFs:

- 80% Vanguard Total World (VT) – An ETF investing worldwide.

- 20% iShares Core SPI (CHSPI) – An ETF investing in Switzerland.

And I could replicate that for my children. However, I have decided to simplify it and invest in VT. I may change this in the future and switch some to CHSPI (or others) as my children get closer to their majority, but for now, I feel comfortable with only VT. Using a single ETF will also make it much cheaper since buying on American stock exchanges is more than ten times more affordable than buying on the Swiss stock exchange.

If you do not know where to start, check out my guide on setting up a portfolio from scratch. But you should try to make it as simple as possible.

The best way to invest for your children

After some research, I have found the best way to invest for my children.

First, I wanted an account in their name, which was impractical since it would significantly limit access to the stock market and good services. So, in the end, the account will be in my name. But this does not matter since I will gift that account once my child is major. And in any case, even if the money is in your child’s name, you are responsible for it until their majority.

The second thing I wanted was for their account to be entirely separated from mine. I did not want to see their shares in my investment account. This separation is crucial because I can separate my net worth from theirs. And it will also show the performance of each portfolio since they will be slightly different.

Third, I needed something where I could start with little money. I do not want to start with 2000 CHF or more just to fit the minimum of some services.

Finally, I wanted something cheap and efficient. That meant investing in index ETFs with low transaction fees for buying.

With all these points, I found only one good investment solution for my children. I will use a separate Interactive Brokers account for each of my children.

This solution is straightforward. You can manage the accounts directly from the same interface on Interactive Brokers. You only have one login. All the accounts are linked together. But they are separated, so each has shares and cash, each with its configuration.

This solution is very cheap since Interactive Brokers is the cheapest broker for Swiss investors. In 2021, Interactive Brokers removed the custody fees below 120’000 USD. So, you can have several accounts with little money and pay no fee. All the accounts are in my name, but this should change nothing.

So, in the rest of this article, I will detail how to invest for your children with Interactive Brokers.

Create a second Interactive Brokers account

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

This article assumes that you are already using Interactive Brokers. As such, we will create a second IB account linked to your main account. If you do not have an IB account, I have a guide on creating an IB account and starting investing.

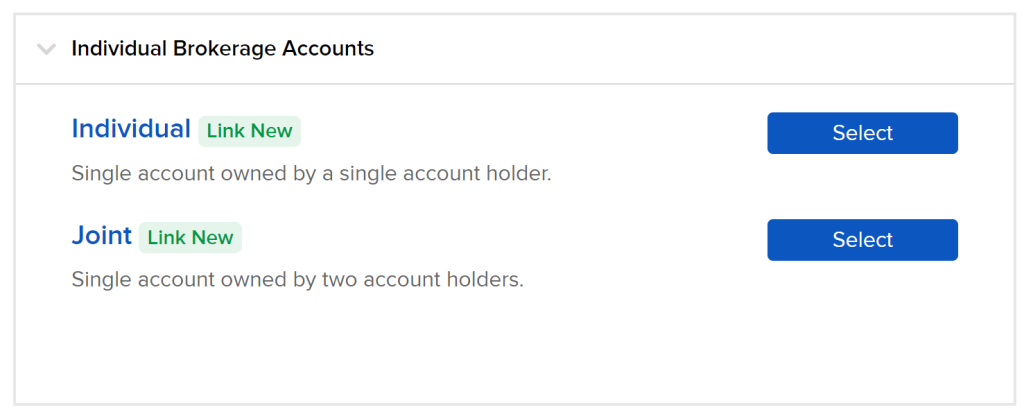

Creating a second account at IB to invest for your children is relatively easy. You will see a button to open an additional account if you go into your account settings. This button will start creating an account automatically linked to your current account. It means you will have only a single login but two accounts behind it.

In the next step, you must select whether you want an individual or a joint account. I recommend you create an account similar to your main account.

Then, you must select whether you want a cash or margin account. It would be best if you were unlikely to use leverage with your children’s money, so you probably want to use a cash account here.

After this, you will have to choose which permissions you want. These permissions will decide which stock exchange you can access. This will be the same as your main account and should be fine already.

Then, you will have to check all the agreements and review all the information you have entered. Once you verify this information is correct, you can sign with your name and finish the application.

They will finally ask you why you asked for this account. I answered truthfully, and there did not seem to be any problem.

Then, this will be up to the approval team to approve or deny your account. I honestly do not know what criteria they are using to do so. In my case, getting the new account approved took one working day.

Finalize the new account

Once IB approves your new account, you can view both in Interactive Brokers’ web interfaces. For instance, when you view your portfolio, you can choose between your accounts.

You need to wire money directly to the new account at least once. After this, you can do internal transfers between your accounts. The first deposit is to validate the newly created account.

Once the first deposit is validated, you can access the new internal funds transfer feature in Interactive Brokers. With that feature, you can transfer funds from one account to another. And you can also transfer positions from account to account.

Invest in the new account

You have several ways to invest for your children with this account. And each way has advantages and disadvantages.

The first way is to transfer money monthly, convert it (if necessary), and buy shares in the second account. This technique is fairly simple. But it means doing two transfers (one to your main account and one to your children’s account). And it is also expensive.

You will pay 2 CHF per conversion if you convert CHF to USD. And then, you will pay 0.35 USD to buy a share of a USD ETF. If we take one monthly share of VT, that’s currently about a 2.5% fee on buying shares. This price is high. It becomes an acceptable price if you do not have to convert currency.

If you buy ten shares of VT, that is acceptable. But most parents will not invest that much every month. You could decide to invest less regularly, but that is a bad option since investing often is better.

The second way is to transfer funds from your main account. That way, you can do conversions and transfer some converted cash to your children’s accounts. And then, you can buy shares from there. You will only pay about 0.35 USD per investment.

Finally, you could simply transfer shares from your main portfolio into your children’s account. That way, you can buy shares and transfer some of these to the second account. This is the cheapest way to do it.

Even though it is not the optimal way, I will use the second option. I want to keep track of each operation in the children’s account to know how much I paid for shares. This technique will cost 0.35 USD in extra fees each month, but that is something I can live with.

Limitations

Remember that this technique to invest for your children does not work if you have several IB accounts with the same email address. In that case, you will not even see the button to add a new account.

In this case, you have two options:

- Delete the other accounts.

- Change your email in your other accounts so that your main account is the only one with this email.

This issue happened because I had an Investart account with the same email address for testing. And Investart is using IB accounts to invest in your name. Once I cleared this out, I could create a new account.

Alternatives with robo-advisors

|

|

|

4.5

|

4.5

|

|

Very affordable

|

Very affordable

|

If you would rather not use a foreign broker, robo-advisors offer a decent alternative to IB . There are two good robo-advisors with this feature in Switzerland:

- True Wealth will invest in general-purpose ETFs (our True Wealth review)

- Findependent will invest in ETFs as well but has a lower minimum (our Findependent review)

It is interesting to note that there is a difference in how this is implemented. With True Wealth, the account is in your child’s name. At 18, it will be transferred because it then is legally owned by your child. With Findependent, the account remains in your name. You can then transfer it to your child when you see fit (after he reaches 18). For instance, you may wait until the end of the studies.

There is one significant advantage to this technique compared to a broker! The transfer will be done entirely internally without any fees. The shares will not be sold, and you will be left with precisely what was on the account. This is a sound system!

If you are worried about using a foreign broker, Swiss robo-advisors will offer an excellent alternative.

Conclusion

There you have it! A second Interactive Brokers account is a great way to invest for your children. This solution is very cheap, very simple, and very complete.

I use this technique to buy one share of VT every month until I give this account to my son once he is 18. If I have other children, I will then open yet another account.

There are probably other ways to invest for your children. Unfortunately, this is the best way I have found. All other brokers have strong disadvantages, either in costs or efficiency (or both!).

If you are not interested in using a foreign broker, opt for a Swiss robo-advisor like Findependent or True Wealth.

If you do not already, I recommend investing for yourself before investing for your children. To help you, I have a guide on how to get started investing in the stock market.

What about you? Do you invest for your children? How?

More reading

What is Compound Interest? Is it Magic?

The 8th wonder of the world. Learn how compound interest works, see real examples, and discover why starting early is the key to massive wealth.

What is the Efficient Market Hypothesis (EMH)?

Can you beat the market? Learn about the Efficient Market Hypothesis (EMH) and why it suggests that passive investing is better than active trading.

The 5 Best Short-Term Investments

Park your cash. Discover the best short-term investment options in Switzerland for money you need soon, from savings accounts to Kassenobligationen.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hello, many thanks for the article. Is there any other Robo-advisor options you could recommend, except Swiss ones? E.g. fidelity go? Trying to understand if it is good.

Hi Margarita

I have never looked at Fidelity Go.

I have looked at Interactive Advisors: Interactive Advisors Review 2026 – Pros & Cons

If you are ready to take a foreign robo-advisor, my thinking is that you could use a foreign broker directly and save on fees even more.

Great article as usual Baptiste!

One question: in addition to a separate sub account in IBKR, do you also have a separate regular bank account for the kids (postfinance, neon, ubs or the like)?

Thanks, Pascal!

Yes, we have a kid account at Migros Bank. It’s not any good, but it’s free. We keep the money he receives in cash gift there.

Thanks, that’s helpful!

Yes, I chose open an additional account in the settings but somehow I cannot find the setting that allows me to open a sub account.

An additional account is a subaccount, so I think it’s the same thing, but we are using different words :)

Thanks for this article!

How will you transfer the account to your child when he/she is 18?

Currently the account is in your name and from what I could gather IB does not allow transfers to accounts that are not registered to the same person. Will you sell the positions and give the child the money to buy the positions on its own account?

Hi Andy

Indeed in this case, I will have to liquidate, transfer the cash and then help him set up his investments.

My goal is to show him how much returns he got in 18 years and then show him how to set it up so that he can get started as well.

Do you know if we need to pay for “donating” the cash once the children are 18yo?

What do you mean by paying? I will have to pay the fees for selling and my son will pay the fees for buying. But there should be no other things to pay. The donation from parents to children are generally tax-free in most cantons (there are exceptions).

Do you know if in canton VD is tax-free for this type of donation? Additionally, I am wondering also about the taxes on wealth. As they are under my name, it means every year my “wealth” will increase, no?

As far as I know, a parent can give up to 300’00 CHF per year to a child in the canton Vaud. And wealth tax is due indeed. As a parent, you are liable for this money until your child pay taxes (even if the money if in his own name).

Hi Baptiste,

I am starting to look at investments for my kids. I have seen that IBKR proposes a Family account. Is this the one you have used? If not, what is the reason why you preferred an individual account?

BR,

Claude

Hi Claude

I have simply used a sub-account. This is like an account inside my account, on my name, under my login.

If you do a family account, you will have one account for you and then one account for your child and a master account to manage everything. I think it would work well, but it’s more complicated to setup and manage.

Hi Baptiste!

I just became a proud aunt, and I want to do the same for my nephew. What I dont like about the option you chose is that then, the day I finally transfer this money to my nephew, this will be tax as a heritage, right? Losing a chunk of this money. On the contrary, if the account is already on his name, on a trusted or custodian account, this would literally be his money, only he cannot access it until he’s 18? Or am I missing something here?

Does that instrument even exist in Switzerland?

Thank your for your great work!

Hi Emilia and congratulations!

You are correct. But for children, this should not be an issue, because gifts to children are generally tax exempt.

However, for a nephew, this is likely to be a problem. In this case, you will really want an account in your nephew’s name. True Wealth may be a better option for you then.

thanks for your insights!

Any idea where we can open an account under a child’s name? IB doesn’t let us do that unless you are in the US.

Hi bapt

If you want an account in your child’s name, True Wealth is quite good for that.

Hi Mr. Poor Swiss,

Thanks for you article!

I was trying to open an account for my child yesterday and I saw the option “custodian account” which is specifically designed for minor.

Maybe check that out!

BR,

Yinan

Thanks Yinan, I will check this out!

Hi Yinan

Was the custodian account with interactive brokers?

BR

Leo

Hello Yinan

I have tried searching for this option but have not found it. Do I somehow need a special account for the custodian account, and how easy was it to set up for a minor?

Many thanks.

Thanks for the article, very good. So this subaccount will still be under my/or parents name, right ? IB wont allow an actual minor be the account holder, or has ownership of the funds ?

Correct, it’s not a true account in your child’s name, unfortunately.

Hi Bap

I could not set up an account for my child in IB. They have to be atleast 18 years old. How did you do it?

Best

Iman

Hi Iman

As written in the article: with IB, you need to create a sub-account, but in your name. It’s just a way to separate your finances from your child’s , but it’s not an account in their name unfortunately.