How to invest for your children in 2026?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Even before my son was born, I knew I would invest for my children. Investing for your children is a great idea, and it makes a lot more sense than letting money rest in a bank account with very low interest rates.

However, until recently, I never worried about how to achieve that. Once my son was born, it was time to research the best way to invest for my children! And I found a great way to do so.

In this article, I share how you can invest for your children and what I will do for mine.

Why invest for your children?

First, you may wonder why invest for your children in the first place. That is a good question.

Most parents will gift some money over time to their children and then give it to them once they reach their majority (or any other specific age). In most cases, this money will end up in a bank account. The problem with that is that bank accounts have little to no returns. So, the money will slowly lose its value due to inflation.

The same reasons to invest that apply to you also apply to your children. We want to increase returns and avoid losing value to inflation.

Another reason to invest for my children is to teach them the value of investing. It may be naive, but I hope to teach my children how to handle their money properly. I will tell you in 20 years how it went!

I also plan to have a bank account for my children. In this bank account, I will deposit whatever he receives as gifts. I also prefer this to be separated.

Remember that you must pay net worth taxes on these assets as long as your children do not pay taxes. So, this is not a way to reduce your net worth taxes!

Decide on what to invest for your children

First, you must decide what you want to invest for your children. In this article, I am assuming you want to invest in stocks. But this technique would work with anything available on the stock market, including funds with real estate, crypto, or gold.

If you are thinking of investing for your children, you are likely to have a portfolio yourself. So, you could replicate your portfolio for your children.

Personally, our portfolio is very simple. It has only two ETFs:

- 80% Vanguard Total World (VT) – An ETF investing worldwide.

- 20% iShares Core SPI (CHSPI) – An ETF investing in Switzerland.

And I could replicate that for my children. However, I have decided to simplify it and invest in VT. I may change this in the future and switch some to CHSPI (or others) as my children get closer to their majority, but for now, I feel comfortable with only VT. Using a single ETF will also make it much cheaper since buying on American stock exchanges is more than ten times more affordable than buying on the Swiss stock exchange.

If you do not know where to start, check out my guide on setting up a portfolio from scratch. But you should try to make it as simple as possible.

The best way to invest for your children

After some research, I have found the best way to invest for my children.

First, I wanted an account in their name, which was impractical since it would significantly limit access to the stock market and good services. So, in the end, the account will be in my name. But this does not matter since I will gift that account once my child is major. And in any case, even if the money is in your child’s name, you are responsible for it until their majority.

The second thing I wanted was for their account to be entirely separated from mine. I did not want to see their shares in my investment account. This separation is crucial because I can separate my net worth from theirs. And it will also show the performance of each portfolio since they will be slightly different.

Third, I needed something where I could start with little money. I do not want to start with 2000 CHF or more just to fit the minimum of some services.

Finally, I wanted something cheap and efficient. That meant investing in index ETFs with low transaction fees for buying.

With all these points, I found only one good investment solution for my children. I will use a separate Interactive Brokers account for each of my children.

This solution is straightforward. You can manage the accounts directly from the same interface on Interactive Brokers. You only have one login. All the accounts are linked together. But they are separated, so each has shares and cash, each with its configuration.

This solution is very cheap since Interactive Brokers is the cheapest broker for Swiss investors. In 2021, Interactive Brokers removed the custody fees below 120’000 USD. So, you can have several accounts with little money and pay no fee. All the accounts are in my name, but this should change nothing.

So, in the rest of this article, I will detail how to invest for your children with Interactive Brokers.

Create a second Interactive Brokers account

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

This article assumes that you are already using Interactive Brokers. As such, we will create a second IB account linked to your main account. If you do not have an IB account, I have a guide on creating an IB account and starting investing.

Creating a second account at IB to invest for your children is relatively easy. You will see a button to open an additional account if you go into your account settings. This button will start creating an account automatically linked to your current account. It means you will have only a single login but two accounts behind it.

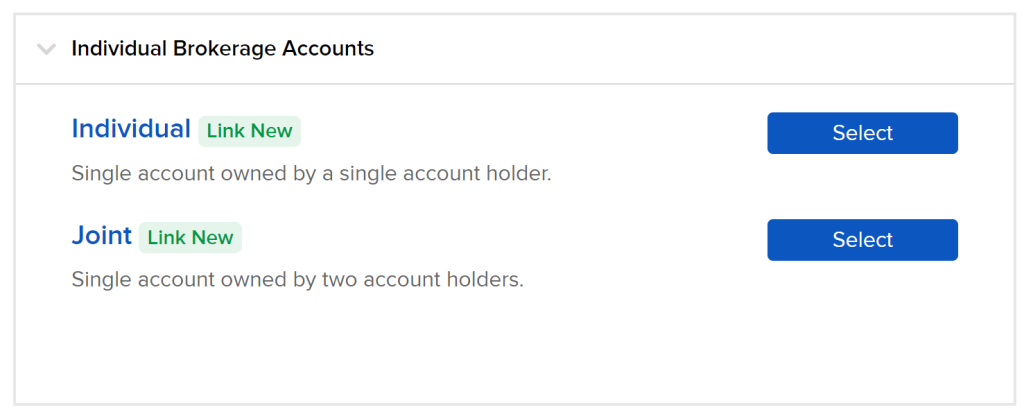

In the next step, you must select whether you want an individual or a joint account. I recommend you create an account similar to your main account.

Then, you must select whether you want a cash or margin account. It would be best if you were unlikely to use leverage with your children’s money, so you probably want to use a cash account here.

After this, you will have to choose which permissions you want. These permissions will decide which stock exchange you can access. This will be the same as your main account and should be fine already.

Then, you will have to check all the agreements and review all the information you have entered. Once you verify this information is correct, you can sign with your name and finish the application.

They will finally ask you why you asked for this account. I answered truthfully, and there did not seem to be any problem.

Then, this will be up to the approval team to approve or deny your account. I honestly do not know what criteria they are using to do so. In my case, getting the new account approved took one working day.

Finalize the new account

Once IB approves your new account, you can view both in Interactive Brokers’ web interfaces. For instance, when you view your portfolio, you can choose between your accounts.

You need to wire money directly to the new account at least once. After this, you can do internal transfers between your accounts. The first deposit is to validate the newly created account.

Once the first deposit is validated, you can access the new internal funds transfer feature in Interactive Brokers. With that feature, you can transfer funds from one account to another. And you can also transfer positions from account to account.

Invest in the new account

You have several ways to invest for your children with this account. And each way has advantages and disadvantages.

The first way is to transfer money monthly, convert it (if necessary), and buy shares in the second account. This technique is fairly simple. But it means doing two transfers (one to your main account and one to your children’s account). And it is also expensive.

You will pay 2 CHF per conversion if you convert CHF to USD. And then, you will pay 0.35 USD to buy a share of a USD ETF. If we take one monthly share of VT, that’s currently about a 2.5% fee on buying shares. This price is high. It becomes an acceptable price if you do not have to convert currency.

If you buy ten shares of VT, that is acceptable. But most parents will not invest that much every month. You could decide to invest less regularly, but that is a bad option since investing often is better.

The second way is to transfer funds from your main account. That way, you can do conversions and transfer some converted cash to your children’s accounts. And then, you can buy shares from there. You will only pay about 0.35 USD per investment.

Finally, you could simply transfer shares from your main portfolio into your children’s account. That way, you can buy shares and transfer some of these to the second account. This is the cheapest way to do it.

Even though it is not the optimal way, I will use the second option. I want to keep track of each operation in the children’s account to know how much I paid for shares. This technique will cost 0.35 USD in extra fees each month, but that is something I can live with.

Limitations

Remember that this technique to invest for your children does not work if you have several IB accounts with the same email address. In that case, you will not even see the button to add a new account.

In this case, you have two options:

- Delete the other accounts.

- Change your email in your other accounts so that your main account is the only one with this email.

This issue happened because I had an Investart account with the same email address for testing. And Investart is using IB accounts to invest in your name. Once I cleared this out, I could create a new account.

Alternatives with robo-advisors

|

|

|

4.5

|

4.5

|

|

Very affordable

|

Very affordable

|

If you would rather not use a foreign broker, robo-advisors offer a decent alternative to IB . There are two good robo-advisors with this feature in Switzerland:

- True Wealth will invest in general-purpose ETFs (our True Wealth review)

- Findependent will invest in ETFs as well but has a lower minimum (our Findependent review)

It is interesting to note that there is a difference in how this is implemented. With True Wealth, the account is in your child’s name. At 18, it will be transferred because it then is legally owned by your child. With Findependent, the account remains in your name. You can then transfer it to your child when you see fit (after he reaches 18). For instance, you may wait until the end of the studies.

There is one significant advantage to this technique compared to a broker! The transfer will be done entirely internally without any fees. The shares will not be sold, and you will be left with precisely what was on the account. This is a sound system!

If you are worried about using a foreign broker, Swiss robo-advisors will offer an excellent alternative.

Conclusion

There you have it! A second Interactive Brokers account is a great way to invest for your children. This solution is very cheap, very simple, and very complete.

I use this technique to buy one share of VT every month until I give this account to my son once he is 18. If I have other children, I will then open yet another account.

There are probably other ways to invest for your children. Unfortunately, this is the best way I have found. All other brokers have strong disadvantages, either in costs or efficiency (or both!).

If you are not interested in using a foreign broker, opt for a Swiss robo-advisor like Findependent or True Wealth.

If you do not already, I recommend investing for yourself before investing for your children. To help you, I have a guide on how to get started investing in the stock market.

What about you? Do you invest for your children? How?

More reading

What is Currency Inflation? How to Fight it?

Protect your wealth. Understand the relationship between currency and inflation and how to hedge your portfolio against purchasing power loss.

13 Greatest Stock Market Myths that do not die

Stop believing lies. We debunk the 9 most common stock market myths that keep people from investing and building wealth.

The 5 Most Used Stock Market Order Types for Investing

Market or Limit? Learn the different stock market order types, when to use them, and how to avoid costly mistakes when buying shares.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi, would a child account or a joint account in the family structure not be suitable? Is there any way with IB that family members can transfer money directly to IB?

Thank you!

Hi Diane,

As far as I know, we can’t open child accounts on IB as Swiss residents.

Joint accounts for two people are possible indeed, but you cannot have a joint account for a parent and a child (or minor age at least).

Ah ok, thanks for the response.

Hi Baptiste.

Thank you for all your insight.

A simple question. Why VT and not VTI?

Br,

Francesco

Hi Francesco

Diversification!

VT is world, VTI is US only.

Hi Baptiste,

I am trying to open a new individual account for my kids.

Each time I start the process, the system tells me I first have to complete an existing open application.

I do not remember to have started one, but anyway I canceled it so that I can start a new one.

When I do so, I get again the same message with a new account number.

Did you experience the same issue? If so, how did you solve it?

Or could it be a poor UX interface which is confusing the users? Meaning I should proceed with the application presented on the screen?

Hi Francesco

I have never had this issue.

But normally, you don’t have to create a new account from scratch. Do you already have an IB account? The children should be in subaccounts not in entirely new accounts (unless they are 18+).

It worked in the end. Indeed, there were some misleading front-end messages.

I now have an account for my kids and can make internal transfers.

Thank you for your excellent content and reply!

Francesco

I am glad you were able to reach a solution!

Hi Baptist! Apologies if this has already been asked and answered, but what are the tax implications of your investment solution, please? Assuming you will be paying tax on these accounts until they are gifted – and once they are gifted, will there be any “gifting tax” applicable?

Thanks for your help!

Hi Baptiste

Good question. Since the account is in my name in my strategy, I will have to declare that money and pay taxes on it until I gift this to my son and at this point, my son will then have to pay taxes on these assets.

My son will have to declare this gift in his tax certificate. In general (in most cantons, including Fribourg), descendants are exempt from gift taxes in Switzerland.

Thank you for the great article!

Sorry if I missed this; why not create a Family Account in IB with you as the “head of the family” and individual accounts ‘below’ it?

Is there an advantage or disadvantage either way?

Thank you already!

Hi Simon

I wanted to keep things simple. That’s why I prefer sub-accounts instead of the complicated advisor system. However, in theory, it could work unless there are some conditions to the family account.

@Joel L This is correct, he can use FEIE up to whatever the amount will be by then. However, if your son will be living in the US for whatever personal reason. Studies, Internship, Job…then he will have to pay taxes on it I guess.

But then who knows how things look like in the future. Don’t know how old your son is, respectively when he will turn 18.

Hello, and once again, congratulations on your blog! I absolutely love it and find it incredibly helpful, especially on days like today when I seem to get a bit confused. Apologies for that. I need some clarification on a particular part. In the section where you mention transferring funds from the main account to buy shares for your children, I’m a bit puzzled. If you still have to pay the 2 CHF for currency conversion when buying for your account, how is this method better?

I’m considering whether it might be more beneficial to use a cheaper conversion tool first, like Neon or Revolut, and then transfer the funds into the IB account to purchase stocks in USD. What are your thoughts on this approach?

Also, I noticed you haven’t mentioned Selma anymore. Is it still a viable option?

Lastly, regarding passing the IB account to your kids, is it really necessary to sell everything and buy again? That sounds quite cumbersome. Have I understood this correctly?

I’ll definitely delve into your other articles about opening an IB account. Thank you!

Hi Carla

Thanks for your kind words!

I am not doing the conversion for each transfer. Each month, I do a conversion for myself and then transfer USD from my main account to my son’s account. So, I pay the 2 USD anway for me and it’s shared.

Currently, you can’t use Selma for kids (yet).

I don’t know whether it’s going to be possible to transfer shares to my son’s account. If possible, I will transfer everything, if not, selling and buying again is really not that cumbersome once in 18 years.

Thanks Baptiste, I had missed this post when I searched for exactly this info just 2 weeks ago, so todays email was perfect timing :) I followed your advice to open my IB account last weekend and I’m now trading, and now I’ll just open a separate account for my nieces. Thank you!

Hi Julie

Thanks for sharing and glad my article and emails were useful for you!

Thank you Baptiste for your detailed insight into this topic. How can you transfer the funds to the kid(s) eventually from the second IB account? Only by closing all the positions and giving them the money, or it would be possible to transfer the whole account on their name/ or the positions on a newly opened account on their name? Thank you for any info.

I hope to be able to transfer it to my son directly through IB since we are in the same family and could be creating a family account in IB for that. If not possible, I will indeed have to sell everything and buy back.

Leider kenne ich kein digitales Konto, das funktioniert, wenn Sie in Norwegen sind. Weder Yuh noch Neon würden funktionieren.

I am still thinking what the best way is for my kids. I really liked the idea of TrueWealth but now thinking for two reason to also do the IB approach

– better pricing on IB than TrueWealth

– my kids are US and Swiss Citizen. Meaning by turning 18 they will be probably start to owe money to the IRS. Keeping it in my IB (I gave up my green card) it will stay in my name and we can figure out what the beet approach will be then.

I just loved the idea that grandparents and others can easily pit money in their account with TrueWealth

Hi Ralph,

Being a US citizen complicates everything in Switzerland unfortunately. I am not sure it will make a huge difference. If you “gift” them the money once they are 18, won’t they have to report it the same way.

Also, if they are in Switzerland, I am not sure they have to report everything? Don’t they only pay taxes in Switzerland?

Gifting is a whole other topic. Not sure what the rules are around it. Depends on the amount of course.

The US taxes you on global income (hence we had to renounce our greencard after returning). While they do not tax you on wealth, it’s more so about dividends and gains. But who knows, maybe that system will eventually change once they are 18.

Keeping the money in my IB has the advantage that it does not automatically transfer to our kids. We can plan better depending on what they want to do with their citizenship or anything else.

In general, I think many people simply also prefer to be able to decide when and what for their kids vs putting it in the hands of the banks.

Indeed, gifting is a whole topic, but if you wait until your kid is 18 and transfer him money from an account in your name, that will be considering gifting I think.

But in any case, there is probably no perfect solution in your case so it makes sense to delay and decide when you know everything. And sometimes, it can be a good idea to delay the transfer until they “can handle” it.

Hi Ralph – my son is a US citizen but I am not so I had similar constraints to you. In the end though invested in my son’s name with Inyova as its unlikely he will end up paying taxes on it when turns 18 due to the foriegn earning income exclusion which goes upto $120K.

@Joel L

I am afraid you are misinformed about the Foreign Earned Income Exclusion. It only pertains to “earned” income, that is wages and such. You cannot exclude dividends and capital gains taxes with the FEIE, since they don’t count as “earned” income. There is a different process for that called FTC, foreign tax credit, which you can opt for instead of the FEIE, but which only makes sense above a certain income level. So your son will have to pay US taxes on dividends, and when he sells, capital gains taxes unless certain steps are taken. I would recommend you talk to an expat tax advisor.

Hi Baptiste. Thanks for very useful post (as usual!). Do you ever consider any ethical aspects of investing money? This seems to me particularly important given we talk about next generations(s). It’s very noble to take care of your offsprings but if the index fund (which I guess you have no control over where it invest) supports company that drills for oil in indigenous land, cuts rainforest or sells weapons in some dodgy country – does the aim justifies the mean? Does it make sense to make sure that one’s children are better off at the cost of someone’s else children paying for the mess created? Or should one just ignores that and focus on the profit margins?

Hi Radek,

Currently, it’s not a main focus of mine. I invest for my son, the same way I invest for me.

Many people invest in ESG funds to help in that matter, but it’s not perfect because the focus is very small. Currently, I believe that broad invest is still the way to go even though this means investing in a few bad companies.

Hi Radek, this is top of mind when I invest not just for myself but also for my son. I’ve invested quite a bit for my son and my self through inyova which Baptiste mentions above. I also don’t invest in an index funds unless they have a strong ESG rating, and the good news is there is more and more of those.