Interactive Advisors Review 2026 – Pros & Cons

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

I have reviewed many Swiss robo-advisors on this blog. However, until now, I have never reviewed a foreign robo-advisor. This is about to change with this review of Interactive Advisors, a robo-advisor by Interactive Brokers and available to Swiss investors.

On paper, Interactive Advisors looks like an excellent robo-advisor with a good investing strategy and very attractive fees. In this review, I will delve deeper into this robo-advisor, its features, fees, and advantages and disadvantages. By the end of the review, you will know whether you should use Interactive Advisors or not.

| Management fee | 0.10% – 0.75% |

|---|---|

| Product Costs | 0% |

| Withholding Costs | 0.15% |

| Total Costs | 0.25% – 0.90% |

| Investing strategy | Active and passive |

| Investing products | Stocks and ETFs |

| Minimum investment | 100 USD |

| Currency conversion fee | Included in management fee |

| Customization | Advanced |

| Sustainable | Available |

| Languages | English |

| Custody bank | Interactive Brokers |

| Users | N/A |

| Established | 2007 |

| Headquarters | Boston, United States |

Interactive Advisors

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

At the beginning, in 2007, Interactive Advisors (then known as Covestor) was a free service that would allow investors to replicate the trades of some portfolio managers. It became a robo-advisor in 2015 when Covestor was bought by Interactive Brokers. And in 2019, its name changed to Interactive Advisors (IA).

Recently, new portfolios have been added to the tool, and fees have been improved as well. And recently, Interactive Advisors added support for Switzerland. It is interesting that IA currently only supports residents of the United States and Switzerland.

So, in this review, we see exactly what Interactive Advisors does, its advantages and disadvantages.

Investing Strategy

It is important to look in detail at the investing strategy of a robo-advisor before starting to invest.

The investing strategy of Interactive Advisors is different from that of other robo-advisors.

Indeed, you can use IA to invest in one of the 70 portfolios offered to investors. There are many of them, with different sustainable options, diversification options, and sectors. Many of these portfolios are passive, but there are also some active options. Having such a choice is good for many advanced investors, but it is not great for beginners.

The questions to evaluate your risk capacity will need to be answered. These will lead to a risk score (from 1 to 5). This score indicates how much risk you can take (5 is the riskiest) and which portfolios you can use. If your risk capacity is 3, you will not be able to invest in a portfolio of category 4.

The minimum investment is different for each portfolio. The minimum ranges from 100 USD to 50,000 USD. The majority of portfolios have a 100 USD minimum, which is great. There are only 12 portfolios that have a portfolio of 1000 USD or more.

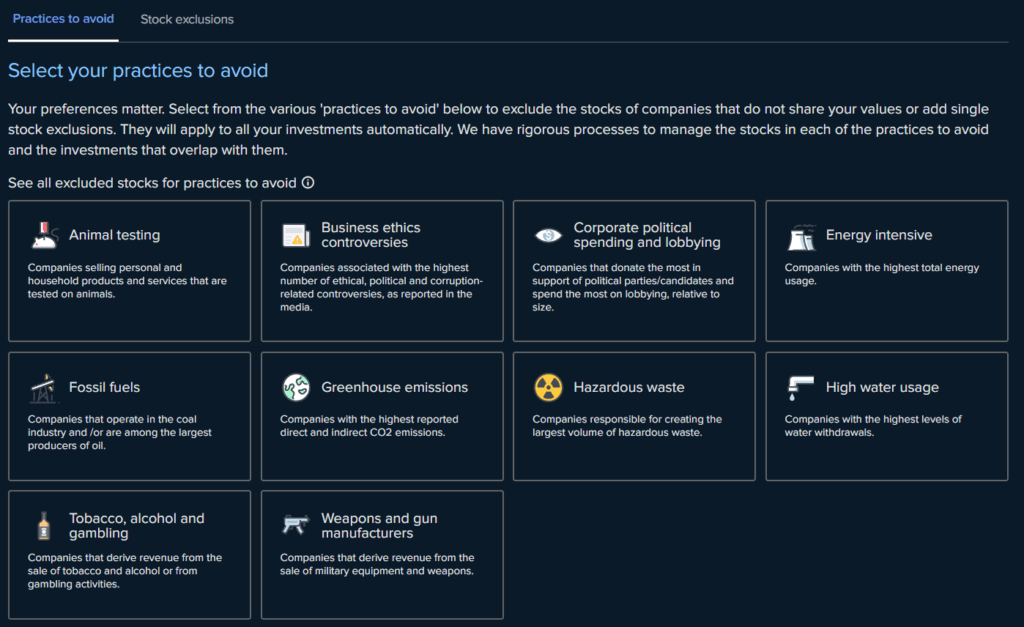

If you wish, you can also opt for sustainable investing portfolios. These portfolios are based either on Socially Responsible Investing (SRI) or Environmental Social Governance (ESG).

You can also set up some exclusions. For instance, you could remove all fossil fuel companies from your investments. With that and the sustainable portfolios, you already have a high level of sustainability, higher than simply using sustainable ETFs.

Each of the portfolios can invest up to 100% in stocks, but there are also some portfolios with bonds. And you can combine multiple portfolios together if you like, but then you are close to using it as a broker instead of using it as a robo-advisor.

There are multiple portfolios with some international diversification. But you may have to opt for multiple portfolios if you have specific needs. And you will not be able to get a Swiss home bias in your portfolio.

Unfortunately, IA does not allow investing in US ETFs. So all portfolios with US ETFs are unfortunately unreachable for Swiss investors. As a result, we have a much more limited choice of portfolios. And we only lose on the tax efficiency of US ETFs.

Overall, the investing strategy is not ideal for Swiss investors. In general, the investing strategy is excellent for aggressive investors but not great for beginner investors since it will require picking a portfolio.

Investing Fees

We also must look at the fees of any robo-advisor.

Fortunately, the fees of Interactive Advisors are very straightforward. Each portfolio has a given yearly fee. This yearly management fee is computed daily and due monthly.

What makes these fees straightforward is that the management fee is the only fee! Everything is included. All transaction fees, custody fees, and currency conversion fees are included.

For portfolios that hold ETFs, the product costs are not included in the fees. But the vast majority of portfolios use stocks and not ETFs.

Portfolios can charge anywhere between 0.10% and 0.75%. Looking across the portfolios, we can see that the vast majority has a 0.20% fee. There are only six portfolios with a 0.10% fee. And the remaining portfolios have 0.75%.

Overall, these fees are excellent. You will pay between 0.10% and 0.75% for your portfolio, and it is up to you to choose the portfolio.

How to create an Interactive Advisors account?

We can now look at how to start investing with Interactive Advisors.

Since IA is based on Interactive Brokers, you will need an Interactive Brokers account. This can be done directly through IA. However, it means that the process will be much faster if you already have an IB account, since opening an IB account is already quite a few steps. So, in this article, I will focus on the IA account. If you require help with the IB account, you can read my article about opening an IB account.

From the IA website, you can sign up directly. Then, this will ask you to connect to your IB account. And from there, it will create a partition. This is the same as a subaccount. This will be created instantly, and you can then do an internal transfer from your main account into your IA account.

Once the account is created and funded (it took less than a minute for me), you can fill out the risk questionnaire. These are the usual questions about your income, net worth, and risk capacity. Out of these, I got the highest score (5), which means I can invest very aggressively, which makes sense for my situation.

From this point, you can already start investing. So, it is really easy to create an Interactive Advisors account.

How to invest with IA?

Once you have created an account, you can directly start investing with this service.

You must use the Interactive Advisors website to invest. There is no app available. And this service is separated from the IB main interface. Therefore, you will have one interface for your IB account and one web interface for your IA account.

Investing is not complicated but also not straightforward. The only thing you can do is to choose a portfolio out of the 70. There are no recommendations by the robo-advisor. Your risk score only defines what you can invest in but does not give you any recommendation.

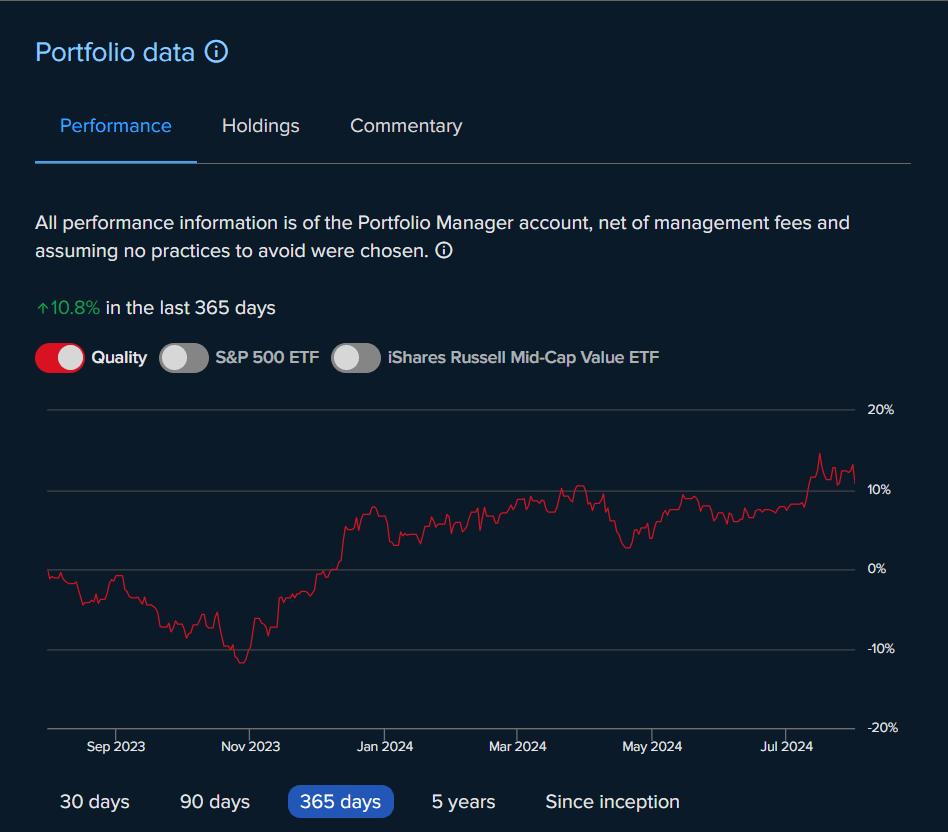

For each of the portfolios, you have access to a lot of data, including all the holdings and allocations. Interactive Advisors is very transparent about how it invests.

And once you pick a portfolio, you can simply invest any amount of money (above the minimum) and you will be done.

So, if you know your way around portfolios, this is easy to use. But if you are a beginner and need more guidance, this is not a smooth process for beginners.

Is IA safe?

Before putting any money into any financial service, we must ask ourselves whether that service is safe.

IA is based on Interactive Brokers, where all assets are deposited. Interactive Brokers itself is one of the safest brokers available. The broker has good technical security with strong two-factor authentication. As far as I know, there has been no major breach at IB or IA.

Assets deposited in IB are protected through SIPC (the US protection for brokers). SIPC protects up to 500,000 USD. This protection includes protection for 250,000 USD in cash.

Overall, I feel like Interactive Advisors is a safe place to invest money.

User Reviews

Ideally, we want to know what users think of a service before using it.

Unfortunately, I have not been able to find good data on the users of Interactive Advisors. There are a few reviews on Trustpilot, but they are all for Interactive Brokers, not for IA.

I looked in other places as well, but I have not been able to find reliable data on the users. Interestingly, this seems to be the case for other US robo-advisors as well. Since there is no app for IA, we cannot look into the different app stores.

I would prefer good data on the customers of IA, but it does not seem possible. Either American users are not keen to leave reviews online, or there are simply not enough users. It is not a dealbreaker, but it still is a point against Interactive Advisors.

If you have ever used IA, I would love to hear about it in the comments below.

Alternatives

We should compare Interactive Advisors against some alternatives. Since I have only reviewed Swiss robo-advisors until now, I will compare it against two Swiss robo-advisors.

Interactive Advisors vs Finpension Invest

An excellent and innovative Robo-advisor by Finpension.

- Most tax-efficient Robo-advisor

- Access to private markets

Finpension Invest is an excellent Swiss robo-advisor by the provider of the best third pillar.

Finpension Invest will provide you with a recommended portfolio that you can then customize. On the other hand, Interactive Advisors will let you invest in multiple portfolios of your choice, according to your risk score.

At Finpension Invest, you will pay about 0.49% per year in fees. At IA, you will pay 0.10% to 0.75% in fees. So you will either be much cheaper or slightly pricier with IA. On the other hand, Finpension Invest will let you reclaim US dividend withholding, while you cannot invest in US ETFs from IA. So, some portfolios will be cheaper with Finpension Invest because of that.

For sustainable investing, Interactive Advisors goes further with the possibility to exclude some sectors and stocks.

Both offers have value. For beginners, Finpension Invest is definitely better because IA is difficult to use without prior knowledge. For aggressive investors, Interactive Advisors may be better because you can get much lower fees if you opt for the cheaper portfolios.

Interactive Advisors vs True Wealth

TrueWealth is an excellent Swiss robo-advisor with very affordable prices, making it a great robo-advisor for serious investors.

Use code SWISS100 to receive up to 100 CHF in fee credits.

- Very customizable

True Wealth is another great Swiss robo-advisor.

True Wealth will give you a recommended portfolio for your needs. Then, you can heavily customize it. But you will not have multiple portfolios to choose from like with IA.

At True Wealth, you will pay a 0.50% management fee on top of the product costs (ranging from 0.13% to 0.20%). So, you will pay a minimum of 0.63% per year in fees.

True Wealth has an option for sustainable investing, but this simply switches to sustainable ETFs. Interactive Advisors goes further in that regard with multiple portfolios and custom exclusion rules.

Overall, IA has the potential to be much cheaper than True Wealth. However, it will not be as easy to use for a beginner. If you are an aggressive investor with some knowledge, you may want to give IA a try. But if you are not, True Wealth will be a better fit.

Interactive Advisors FAQ

Who can open an Interactive Advisors account?

Currently, only residents of the United States and Switzerland can open an Interactive Advisors account.

Who is Interactive Advisors good for?

Interactive Advisors is good for advanced investors that want to invest in advanced portfolios, with very good fees.

Who is Interactive Advisors not good for?

Interactive Brokers is not ideal if you are a beginner investor because it requires you to pick a portfolio out of 70.

Can you invest sustainably with Interactive Advisors?

Yes, you have access to multiple sustainable portfolios in IA. And you also set up sectors and stock exclusions. This should make IA an excellent place to invest sustainably, according to your standards.

Can you use US ETFs with Interactive Advisors?

No, Swiss investors cannot use US ETFs on Interactive Advisors.

Interactive Advisors Summary

IBKR's Robo. Read our review of Interactive Advisors. Can this low-cost robo-advisor compete with Swiss alternatives for automated investing?

3.5

Interactive Advisors Pros

Let's summarize the main advantages of Interactive Advisors:

- Very low fees

- Safe

- Many portfolios available

- Very low minimums

- Excellent for aggressive investors

- High customization

- Good stock exclusions for sustainable investing

- Good transparency in portfolios

Interactive Advisors Cons

Let's summarize the main disadvantages of Interactive Advisors:

- Fees can vary highly from one portfolio to another

- No mobile app

- No access to US ETFs as a Swiss resident

- Not suited for beginners

Conclusion

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Overall, Interactive Advisors is a decent robo-advisor open to Swiss residents. It allows you to invest in many portfolios, with fees as low as 0.10%. I am glad there are also some foreign options for Swiss investors looking for a robo-advisor.

Unfortunately, since they cannot offer US ETFs to Swiss residents, they are not as good for Swiss residents as they are for US residents. This diminishes the fee efficiency significantly.

If you find a portfolio that suits your investment needs, Interactive Advisors is probably the cheapest robo-advisor you will find. Doing so will require some understanding of the portfolios. However, if you are a beginner and do not want to pick a portfolio yourself, Interactive Advisors will not be easy to use.

For Swiss investors, it may be interesting, but I feel like if you are advanced enough to go that route, you are advanced enough to use Interactive Brokers directly.

What about you? What do you think about this service?

More reading

arvy Review 2026 – Pros & Cons

Is arvy the right robo-advisor for you? We review arvy’s active investing strategy, its high total fees, and how it compares to top Swiss alternatives.

VIAC Invest Review 2026 – Pros & Cons

Invest without limits. Read our review of VIAC Invest. We test their private investment solution to see if it's as good as their famous 3a pillar.

Raiffeisen Rio Review 2026: Pros & Cons

Is Rio worth it? Read our review of Raiffeisen Rio. We analyze the high fees and structured products to see if this app is a good way to invest.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

I see there are only 14 portfolios with ETF strategy. And… I can’t invest in any of them because of:

“This portfolio contains U.S. ETFs and is unavailable due to regional Investor Protection Rules (PRIIPs)”.

I have created my account based on the IKBR one, with Swiss residency, CHF as the main currency etc. Only my citizenship is not Swiss. Does it mean it’s not possible to invest into ETF-based portfolios by non-US residents? That would be quite disappointing.

On your IB account, are you allowed buying US ETFs? I would expect the permissions to be the same in both case. Maybe you can try asking the support to be sure.

Today I have received the following answer:

‘The reason for the message is because Swiss residents, as of last year, are also held to the EU PRIIPs rules regarding US ETF’s unfortunately.

You may invest in any of the other portfolios that do not invest in US ETF’s. You may filter on the left side of the portfolios page, by choosing “Stocks” under the “Composed of” box’.

I believe it’s worth to highlight that fact in the review, it makes this offering much less interesting.

We have never been subject to the EU PRIIPs rules since we are not part of the EU, so their statement is wrong. We are subject to FINSA rules. In this case, since they actually advertise portfolios, it’s possible that FINSA will apply to IA unlike IB. I will update the article.

I have just received yet another response (as I have sent a link to this article: https://thepoorswiss.com/swiss-investors-lose-access-us-domiciled-etfs/#0-2024-update):

“Definitely interesting commentary, however, compliance at both IA and IB have confirmed the PRIIPs issue applies to Swiss residents as well”.

I would be happy to add you to that email conversation with IB representative to clarify that situation once and for all. I don’t know your email, but I believe you can see mine, so just please reach out to me there if you are interested.

I’ll drop you a line.

Can one pick more than one portfolio? If so, how often does IA rebalance across portfolios and cash on the account?

Yes, you can invest in multiple portfolios. However, IA won’t do any rebalancing, you will have to put money in each portfolio.

There is a big part of social trading on IA, because in the background, there is a marketplace where portfolios from registered US portfolio managers co-exist with the ones from IB.

These managers license their trade data and every portfolio is assessed and graded by IB to then be matched with the risk profile of the client.

Can we see who the manager is when reviewing a portfolio?

Yes, you can see that. If you look at the list of all portfolios (here), you can see who it comes from for each of them.

Awesome, I really like the transparency of IBKR. Thank you Baptiste.

Great review, thanks!

some weeks ago I created an account with IA and I invested initially in an aggressive portfolio for my daughter. I agree with your conclusion – IA is not really for beginners. It is really a joy to browse through the various portfolios they offer, with various risk levels. And the fees are really amazing.

Cheers!

Thanks for sharing Zoltán! Indeed, if you use one of the cheap portfolios, the overall prices are very good.