Investart Review 2026 – Pros and Cons

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Investart is a new online robo-advisor service that lets you invest in Exchange Traded Funds (ETFs) for a small fee! And not only that! They allow you to invest in custom strategies. So, you could use it either as a robo-advisor or as a broker for ETFs!

I only recently discovered this service. But it looks exciting. I even started investing some money myself. So, it is time I review Investart.

In this article, I review Investart’s advantages and disadvantages and compare it against similar services!

I wrote this article in collaboration with Investart.

| Management fee | 0.30% per year |

|---|---|

| Product Costs | 0.10% – 0.25% |

| Withholding Costs | 0% |

| Total Costs | 0.40% – 0.55% |

| Investing strategy | Passive |

| Investing products | ETFs |

| Minimum investment | 2000 CHF |

| Currency conversion | Included in custody fee |

| Customization | High |

| Sustainable | Not by default |

| Languages | French, German, and English |

| Custody bank | Interactive Brokers |

| Users | Unkown |

| Established | 2019 |

| Headquarters | Zürich, Switzerland |

Investart

Investart is a Swiss company founded in 2016 by Richard Toolen. The service was publicly launched in 2019. At the beginning of 2021, they reduce their fees to zero! But then, they reintroduced some fees in mid-2021.

They also make money with other services. Indeed, they are proposing several financial services:

- Financial consultation

- Pension planning

- Wealth planning

So, you could invest your money there and then consult with them to plan your financial life and your future investments. Remember that I have not tested their paid services, only their online investment platform.

For more information on the company, I interviewed Investart CEO Richard Toolen. This interview should give you more details about this service.

Investing with Investart

So, we can now review how you can invest with Investart.

The interesting thing is that Investart is a robo-advisor, not a broker. But it can do a little bit of both. And it can do it well. I would say that Investart is a portfolio investing service. The service can create a portfolio for you, or you can create one, and the service will automatically invest your money into the portfolio.

There are three ways to invest with Investart:

- Accumulate. You can set a target amount of money you want to reach and your target date. Investart will then derive a portfolio and a monthly amount from reaching your goal on your target date.

- Grow. You can set an initial and monthly investment, and the service will create a portfolio to grow this money.

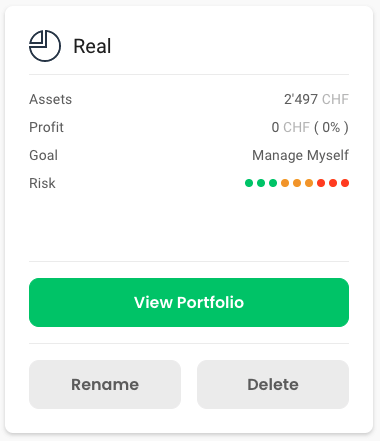

- Manage yourself. You can create your portfolio from scratch and choose your ETFs.

Moreover, using the Accumulate or Grow methods, you can choose between Conservative, Balanced or Aggressive strategies. In that case, the allocation to bonds will vary. Given the current state of bonds, I think it would be better to keep CHF cash. But this is not a huge deal since most robo-advisors do the same thing.

Indeed, even if you start from Accumulate or Grow methods, you can modify the portfolio and switch to a Manage Yourself strategy. If you do not like the bonds, you can switch them over to cash. Of course, you will then have to manage your portfolio yourself.

Investart will rebalance your assets for both methods if they deviate too much (more than 5%) from the target allocation.

With a custom portfolio, rebalancing is semi-automatic. Once your current allocation deviates more than 5% from the target allocation, you can rebalance it. You can then trigger the rebalance from the web interface.

Rebalancing is checked daily, so you cannot change your portfolio during the day and expect changes to be made. Daily rebalancing is an excellent thing since it prevents intraday trading, which is not a good idea.

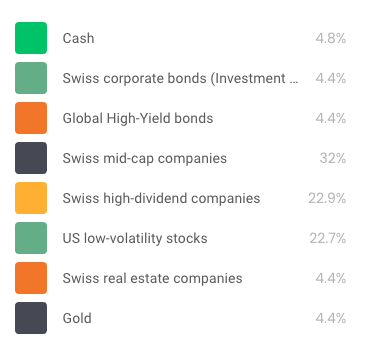

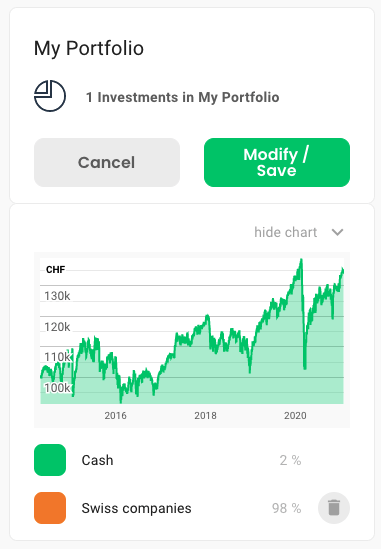

Here is an example of an Aggressive Grow portfolio that Investart generated for me:

This portfolio is typical, although probably a little overcomplicated for me. The amount of bonds is too high for my case. I do not think an aggressive portfolio should need any bonds or gold. And it could have better international diversification. However, this is a typical portfolio generated by most investing models. If you look at other Swiss robo-advisors, they will always add bonds to a portfolio. So. I am not surprised by this portfolio.

But again, this is not a huge deal since more involved investors can choose their own portfolios. For this, we have access to a large list of Exchange Traded Funds (ETFs). When I wrote this article, there were 70 ETFs. They have a large selection of ETFs for Switzerland, Europe, and the United States. They even have a few (4) ETFs for sustainable investing. But they plan to add more options in the future.

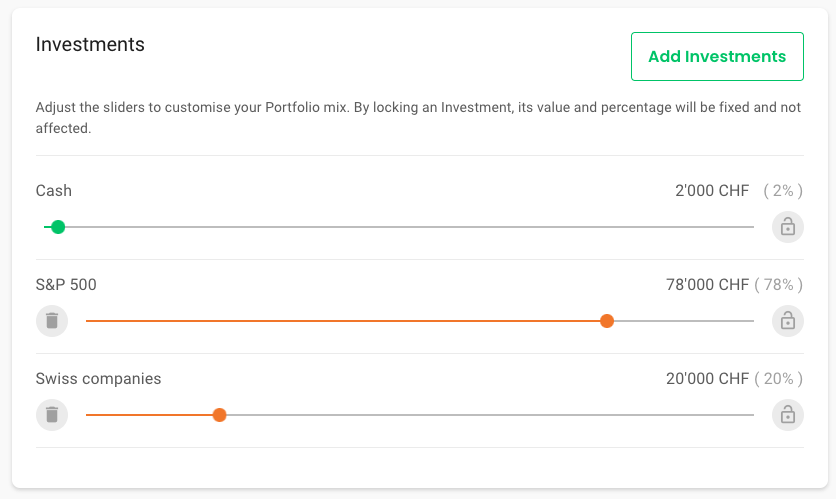

For instance, here is one simple custom portfolio I did:

You can do a lot of things with your custom portfolio. But there are a few things we should note:

- Many of their ETFs are currency-hedged, and I would prefer more non-hedged alternatives. However, there are probably enough non-currency-hedged ETFs to make a decent portfolio for many people.

- You need to keep a minimum of 2% in cash. This is fairly standard since they keep the cash for rebalancing.

You can start investing with Investart with at least 2000 CHF. It is not possible to invest in amounts lower than this.

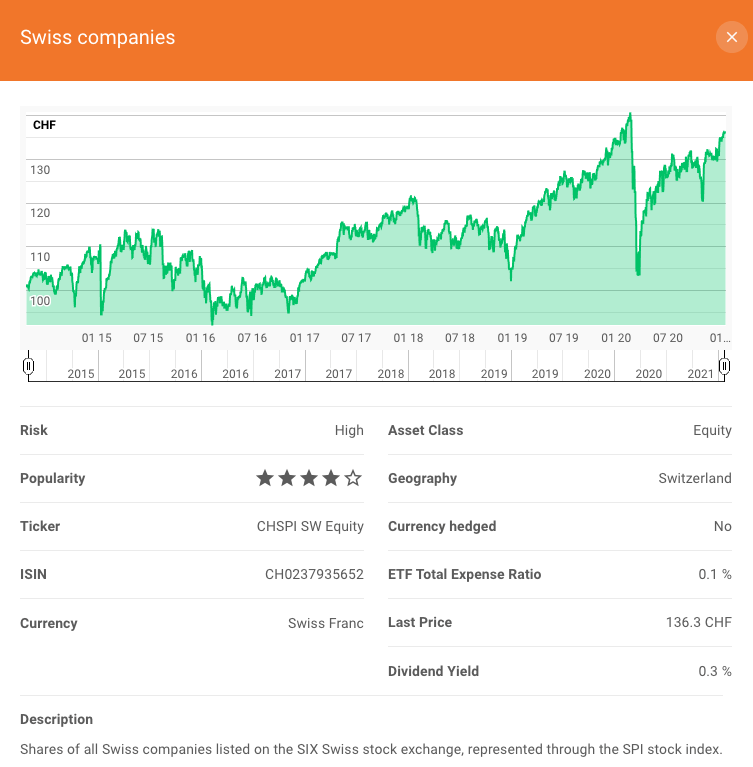

One great thing is that they share the exact ETFs they invest in. For instance, the Swiss Companies block is investing in CHSPI, my favorite ETF for Swiss stocks:

Overall, the investing options at Investart are excellent. For people who are not experts (or do not want to spend the time), the generated portfolios are acceptable. For others, the fact that we can create custom portfolios is really interesting.

With Investart, we also have access to U.S. ETFs. These ETFs are the most efficient ETFs available to Swiss investors.

However, some limitations will make this not entirely optimal. For instance, many ETFs are currency-hedged, which may not be the best option for everybody.

Fees

We should also review the fees of investing with Investart.

With Investart, you pay a 0.025% fee per month. Over a year, this is a management fee of 0.30% of what you have invested with them. Everything is included in this management fee: transaction fees, foreign exchange fees, and Swiss Stamp Tax Duty.

The only other fee you will pay is for the ETFs you are using. And this can go very low. For instance, the CHSPI ETF (the best ETF for Swiss Stocks) only has a Total Expense Ratio (TER) of 0.1%. Such a level of fee is as good as you can get.

And Investart will provide the necessary documents if you use US ETFs so that you can reclaim the dividend withholding. This makes them very tax-efficient.

This total fee is really low. With only a 0.3% management fee, Investart is the cheapest Swiss robo-advisor I know. Most robo-advisors in Switzerland are about twice as expensive as that, sometimes even more.

Since investing fees are extremely important, this can make a significant difference in the long term.

Create an Investart account

Update: As of May 2026, onboarding of real accounts is temporarily on hold.

Creating an Investart account can be started online.

To start the signup process, you can go to Investart and click the big green Sign Up button in the top right corner. Then, you must choose whether you want a Demo or a Real account.

The first step is to choose a username and a password. Then, you will have to verify your ID. The verification can be done with your passport or your national ID.

The verification was not smooth at all for me. I tried to do it from my computer with my webcam (full HD), and it never worked. After ten tries, I gave up and switched to my phone, which worked directly. So, I would encourage you to do the verification on your phone. But this means people on computers need to use two devices.

After this, you will have to fill in your personal information and then your employer’s information.

Then, you will have to provide information about your net worth and your trading experience. This is fairly standard. The only weird part is that you have to set the different components of your net worth. And you have to set if they will contribute to the Investart account. These are the same questions you get if you open an Interactive Brokers account, and Interactive Brokers mandates these questions.

Then, you must accept all the terms and conditions, sign the documents digitally, and upload proof of residence.

Then, you will be connected to your account. You will probably see a Demo portfolio on your account. But do not worry. This portfolio will be transformed into a Real (non-demo) portfolio once funding has passed.

The first time you log in to your account, you must set up Two-Factor Authentication (2FA). This is a great idea, and it will increase your security!

Your Investart account will be instantly created. However, you must wait for the Interactive Brokers account to be created. And this is a manual process at IB that can take one or two days. In my case, it took one working day to be created. In the meantime, you will have access to your account as a Demo account.

You will then receive an email indicating that your account has been created, and you can deposit money on it. You must do a bank transfer (directly to Interactive Brokers) to top up your portfolio.

Once the money has been received and processed (one more working day), your account will be fully operational. Here is my simple portfolio:

I funded my account with 2500 CHF, which was invested the next day in my straightforward portfolio. I decided to invest in the CHSPI ETF (Swiss companies), part of my IB portfolio.

Overall, the account creation process at Investart is okay but could be improved. Several things could be improved and cleaned up. For instance, the verification process on a computer camera should be improved. It would also be great if this could be done faster. However, since the main bottleneck is creating the IB account and the money transfer, Investart cannot do much on the speed side.

Security

Of course, we need to look at this service’s security if we invest any money.

From a technical standpoint, everything looks good with Investart. Their website uses good encryption levels and shares good security information. They are also following FINMA compliance for their network infrastructure, which is always a good thing.

One great thing is that Investart is forcing people with a real account to use a second-factor authentication! This is great since this adds a good layer of security.

I have not been able to find information about security issues with Investart. However, since they are very young, this does not mean much, even if it is already a good sign.

Your money and shares are held by Interactive Brokers (IB) UK. Indeed, they use IB as their trading platform for all operations. IB itself is extremely well-regulated and well-protected. Investart will open a dedicated IB account for each customer. This is excellent since it improves the segregation of assets.

The level of protection is entirely appropriate. IB UK is a member of the Financial Services Compensation Scheme (FSCS). This scheme offers compensation for up to 85,000 GBP in case of failure of IB. This protects slightly more than 100,000 CHF (depending on the exchange rate).

Moreover, IB UK is also part of the Securities Investor Protection Corporation (SIPC), which provides an extra level of protection. However, this may not last due to Brexit. But currently, this provides an extra 250,000 USD in protection.

Investart is regulated as an asset manager by VQF (The Financial Services Standards Association). And they are also registered with FINMA. VQF regularly audits them.

Overall, I think that investing with Investart is safe. They are taking the necessary measures to ensure the security of the invested money. The technical security is also quite good. The only thing in their disfavor is their young age as a public investment company.

Alternatives

It is important to consider alternatives when reviewing a product. We can compare Investart with some alternatives.

Investart vs a broker

Investart is not a broker, but it lets you invest in a portfolio of ETFs. For a passive investor, this is all that matters, so it is interesting to compare Investart with other brokers.

It is difficult to compare with other brokers since the fees are flat regardless of how much money you have and how much you invest. For small accounts, Investart may be slightly more expensive than some brokers. And with large accounts, Investart may be slightly less expensive than some brokers, especially large brokers. But overall, the prices are in the same order of magnitude.

However, with an actual broker, you can access more ETFs than the 70 ETFs available at Investart. Now, for most people, these 70 ETFs will be enough. However, if you have some niche needs, this may not be the case.

If we compare it with Swiss brokers, I think that Investart is better for simple and passive investors. They will be slightly cheaper and offer enough ETFs.

Compared with the best broker for Swiss investors, Interactive Brokers, IB still leads the way. IB will be even cheaper than Investart. And with IB, you can invest 100% of your money. So, I think that the ability to choose more ETFs at IB is a nice advantage. On the other hand, with Investart, you will get a slightly easier experience and robo-advisor service. Investart is the only Swiss service that even comes close to IB.

Overall, Investart could be an excellent alternative to a broker, especially a Swiss broker, if you can make a portfolio with a choice of 70 ETFs.

The main advantage of Investart is that it is easier to use than a traditional broker.

Investart vs a robo-advisor

Investart offers the same services as a robo-advisor. Indeed, with the Grow and Accumulate strategies, your portfolio will be adapted based on their financial models. So, we can compare Investart with other robo-advisors.

From a fee point of view, it will all depend on the amount of money invested. Investart is expensive for small portfolios and cheap for large portfolios. They may be significantly cheaper than affordable robo-advisors like Finpension Invest (our review) and True Wealth (my review).

Since they give you strong strategies, they provide the same features as other Swiss robo-advisors. Having about 70 ETFs in the choice makes it very interesting. And they are the only robo-advisor with U.S. ETFs.

Investart has a few missing features compared to other robo-advisors. For instance, they do not have options for sustainable investing. Also, the reporting is a little lacking compared to other robo-advisors to give you an overview of your finances.

The other disadvantage is the company’s young age compared to most established services. However, since they are well-regulated, I do not think this is a big issue.

Overall, Investart is much cheaper than other Swiss robo-advisors. As such, it has a major advantage. So, if you are looking for an affordable robo-advisor with a good investment portfolio, it is a good choice.

Investart FAQ

Is Investart free?

No, Investart has a 0.025% management fee per month. This amounts to a total 0.30% fee per year.Since they invest in ETFs, you will also have to pay for the ETF fees yourself (the TER).

How does Investart make money?

On top of the management fees, they are providing paid services to their users. For instance: Pension planning, Wealth planning and Personal consultations for investing.

What happens if Investart goes bankrupt?

The great thing with Investart is they are opening IB accounts in the name of each investor. So, if they went bankrupt, this money would still only belong to the user. The money would not be part of the bankruptcy settlement. In case of bankruptcy, the user could claim the Interactive Brokers account as his own. That way, he would be able to keep his shares and continue investing. Of course, this means he would have to pay IB fees, and he would not have a managed portfolio. But this is a great way to ensure the safety of the money.

Who is Investart good for?

Investart is good for investors that want to aggressively invest in the stock market, with medium to large sums of money. These investors should not mind having their funds held by a foreign broker (Interactive Brokers).

Who is Investart not good for?

Investart is not for investors who are afraid of foreign brokers. And Investart is also not great for people wanting to start to invest small sums because of relatively high fees in that segment.

Investart Summary

Investart is a very interesting robo-advisor, based on Interactive Brokers. They offer low fees and good access to ETFs.

Product Brand: Investart

4

Investart Pros

Let's summarize the main advantages of Investart:

- Very cheap Robo-advisor

- Invest in index ETFs

- Access to U.S. ETFs

- You can create your own portfolio

- Transparency on the ETFs being used

- Well-regulated

- Good technical security

Investart Cons

Let's summarize the main disadvantages of Investart:

- Very young company

- A limited set of ETFs to invest in

- Focuses on currency-hedged ETFs

- You need to keep at least 2% in cash

- Few options for sustainable investing

- Online verification process could be better from a desktop computer

- It takes a few days to open an account

Conclusion

Overall, I am impressed by Investart! Their offer is interesting. When it was free, I opened an account and started investing with Investart to test it.

Even now that it is not free anymore, it remains very cheap, at a 0.30% custody fee per year.

You can use Investart like a robo-advisor, and it will choose a portfolio based on your needs. Or you can manage your portfolio directly. And you have access to U.S. ETFs! So, this is a very efficient portfolio.

There are also some other disadvantages. For instance, you have only a limited set (about 70) of ETFs you can invest in. Also, Investart is a very young company, and they still have to work on the business model. So, we will have to wait and see how this works long-term.

If you need help setting up your portfolio, you can look at my guide for creating your own ETF portfolio from scratch.

What about you? What do you think about Investart?

More reading

Swiss robo-advisors 2026: Invest without any hassle

Automate your investing. We compare the best Robo-Advisors in Switzerland to help you find the right service to manage your wealth automatically.

arvy Review 2026 – Pros & Cons

Is arvy the right robo-advisor for you? We review arvy’s active investing strategy, its high total fees, and how it compares to top Swiss alternatives.

Interview of Patrik Schär – CEO of Selma Finance, Robo-Advisor

Meet the CEO of Selma. Read our interview with Patrik Schär and discover how this Swiss Robo-Advisor makes investing simple for everyone.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi there,

What sets off a warning signal for me is that investart does not charge stamp duty. This makes no sense or is not financially viable in the long term, as these costs are effectively incurred.

What’s your take on this?

Investart is using Interactive Brokers. So, they do not have to pay Swiss Stamp Duty :)

You are right, my mistake:)

I’m curious to see how investart develops.

Many thanks for this awesome article .

Do you understand why the ETFs on investart have such a low yield??

For instance for S&P 500 it says 0%.

Personally I own VOO on IB and it is usually 2/3% per year.

Same thing with CHSPI or others .

Many thanks !!!

Hi Michael,

Great question. I have no idea :) I will ask Investart about this.

I can see the same for CHSPI, 0.3% on investart, 2.5% on ishares.

Thanks for letting me know!

Hi Michael,

I just got an answer from them (very fast!).

They are using the Bloomberg indicated yield which only counts the last dividend dividends by the price per share. So, it’s not an annual measure. But what you will receive will be the same thing.

Cheers

They use IB as broker. What is the advantage to invest directly using IB? Investing directly in IB allows me to have a margin account and SMA. Greater flexibility when investing.

Only advantage I see is a simpler interaction with IB.

Please read the “Investart vs a broker” section.

I use investart since about 2 weeks.

Their support is very responsive and helpful. Their website still has some youth errors, but the figures are overall correct. TW reporting accuracy at the moment is not available at IS though.

My biggest doubt is how they can finance themselves.

And I find the 5% clause does not take full advantage of the rebalancing. ie true wealth has 1%, viac 2%. And I have some doubts on their handling of rounding.

On the other hand the access to IB account is fully available so in the unfortunate case investart ceases to exist it will be easy to take the funds back. You can see even the value of the portfolio live, live TWR, historical data and so on.

I find the funds choice more than satisfactory for a non expert, finally a place where to buy an msci world etf and it seems they increase the choice with time too. You can have max two portfolios which means 2 IB accounts.

On their blog I found this

Wir bieten unseren vermögenden Kunden kostenpflichtige Premium-Dienstleistungen wie persönliche Beratung, Vermögensplanung und Vorsorgeplanung an. Da diese Leistungen massgeschneidert sind, gehen wir auf die potenziellen Premium-Kunden zu und besprechen den Rahmen sowie die Konditionen solcher Leistungen individuell.

Hi Karl,

Thanks a lot for sharing your experience.

I agree that the choice in ETFs is more than enough for most investors.

I also agree that the only downside is that there is doubt at how long they will last. If they can manage to keep their costs low, they may well manage to turn a profit. I am sure there are people interested in unbiased investing recommendations.

Regarding rebalancing, I don’t see this as a problem. 5% is more than enough. I have done some simulations about rebalancing and it does not make as a big of a difference as people think. And actually, there are many cases where rebalancing would hurt your performance since you are selling good assets.

Thanks for stopping by!

If I understood Karl correctly, I think he is suspicious that Investart is using the rebalance cash (5%) remaining in your account to finance themselves and generate money (that will be an indirect/hidden/unannounced fee)!

no actually but meanwhile I understood the whole better.

the current money allocation algorithm has flaws, i.e. it never allows the % to be higher than target %. and even if you add cash you can still end up with 30% cash because only the positions breaking the 5% rule get rebalanced. this if you have several positions.

a new algorithm will be implemented in 2-3 months… but at the moment it’s impossible to profit from the weak stock values, and TW on this is far ahead. we’ll see

Keep in mind that this is the invest yourself strategy. The idea is for Investart to use your strategy. If you want to let Investart do something smarter on their own, you can use one of their other strategies where they could do something smarter when something is cheap on the market.

fyi :)

I had a very interesting conversation with Investart today and there are lots of plans ahead.

new asset allocation calculation method, new ETFs, possibly US ETFs too…

as tax declaration form end of year an extract from IB is provided

Hi Karl,

That sounds good :)

It would be great to have more choices of ETFs!

Interesting indeed

Can I see the ETFs options or do I really need to create an account to see ETF options?

Eagerly waiting on an update in the future.

Hi Stefano,

Yes, you can! Go to “Manage Myself” (here). There you can see all the possible investments. And if you click on the (i) icon on each of them, you will see the exact ETF that is being used.

Hi there,

thanks for the very interesting post.

I was looking to the ETF choise. Checking for example USCHWH, the TER should be 0,19% but on investech is 0,30%. Didn’t check them all but some others are ok. It’s probably just an error.

Anyway, it could be a good solution once we’ll lose access to US ETFs.

Hi Azz,

There was a case before where the information was not correct because the ETF changed their fees and investart did not see it directly. And they made the change already for that previous one.

I am sure they will make the change for this one too.

Indeed, if (or when) we lose access to U.S. ETFs, this will be even more interesting!

Hi, this service look interesting to start before creating an IB account directly. If I understood the money will be invest at IB without having to pay the fee for a portfolio below 100k right? Does it make it even more interesting than Degiro for small Swiss investors?

I’ve tried to create an account and after the very very painful authentication (why is the camera mirrored to scan the document?! and why is it so hard to get the selfies accepted? took me 10 times at least both on PC and phone), I’m stuck at the question of the NIF number. Should I leave the default one, second answer, I don’t have to provide one by law? Does it mean I’ll not be able to recover the source tax from US? How do I get a NIF, can I add one later? It’s really not clear. Or is it just the AVS number here?

Hi,

Yes, that is correct, you won’t pay the IB fees.

I think it makes it better than DEGIRO yes. But then, you are limiting your choice of ETFs. On the other hand, there are 70 ETFs. So most investors should have enough.

Yes, the camera thing is a nightmare. I gave up on PC but had an okay time on the phone.

I believe I use my AVS number for the NIF. This is what I do in general when I get asked this question.

Keep in mind that they cannot offer access to U.S. ETFs, so you won’t have to do deal with U.S. source tax.

Thanks for stopping by!

Hi, Thanks for your article.

I have a question about annual fiscal documents. Do they provide those kind of papers?

thanks again

Hi Mat,

Yes, Robo-Advisors have to provide an annual statement that you can use in your tax declaration. This statement will contain the wealth and the dividends generated.

Thanks for stopping by!

Does this also apply to the manage-youself-portfolio?

So far I always discarded the Robo-advisor option, but this article prompted me to reconsider my position.

I was eagerly looking for some explanation re. Taxes. I’m afraid that if the system makes a few transactions every week my tax declaration becomes a nightmare. Any thoughts on that?

Hi Luis,

I do not think this is a risk. I have not yet seen the annual statement from Investart, but Robo-Advisors in Switzerland do not give you the entire list of transactions for your tax declaration. You only have to declare your wealth and your dividends/incomes. At least, this is what Selma is doing and I assume that this is what Investart is doing as well.

Also, Investart will only rebalance if your portfolio changes or if it gets out of balance by more than 5%. This should not happen more than a few times a year (or monthly if you invest monthly). So, that would not be that many transactions.

Thanks for stopping by!

Thx for the nice article.

I have been watching the company for a while now and find their offer really interesting.

What I find a bit suspicious is that the company (besides the founder) seems to consist only of freelancers. Compare the alleged team on the website with their LinkedIn profiles.

If the company still exists in a year, then the offer would be really exciting.

Hi Beluno,

That’s an interesting point. I did not see that before. I did not search the other members on LinkedIn.

It could simply that this is still a small project and they do not need a full team. (just a supposition).

It’s a good point! If they manage to live for a full year without introducing new fees, it would be a great sign for their business model and a great sign for Swiss investors!

Thanks for stopping by!

Same thing for me. I found it weird to don’t have a team behind.