Saxo Bank Review 2026 – The Best Swiss Broker

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Since they reduced their fees, SAXO Bank has become a very competitive broker for Swiss investors. SAXO has many features, and this package now comes at a low price.

But is that enough? We find out in this review.

In this review, I cover Saxo Bank in detail, including its advantages and disadvantages. By the end of this review, you will know whether SAXO is a good broker for you or not!

| Custody Fees | 0 CHF |

|---|---|

| Inactivity Fees | 0 CHF |

| Buy Swiss ETF | 0.08%, min 3 CHF |

| Buy American Stock | 0.08%, min 1 USD |

| Currency Exchange Fee | 0.25% |

| Languages | English, French, German |

| Mobile Application | Yes |

| Web Application | Yes |

| Custodian Bank | Saxo |

| Established | 1992 |

| Swiss Headquarters | Zürich |

| Global Headquarters | Copenhagen, Denmark |

Saxo Bank

Start investing with a Swiss broker at incredible fees! Start trading with Saxo Bank and get 200 CHF in trading credits.

- Low currency conversion fee

- Swiss broker

Saxo Bank is an investment bank from Denmark. It was founded in 1992. It is a large institution with over one million clients and operates in 28 countries.

Saxo Bank is a private company. As of July 2026, the only shareholder is the J. Safra Sarasin Group (a Swiss private banking group). The original founder and CEO, Kim Fournais, remains chairman of the board.

In Switzerland, investors deal with Saxo Bank (Switzerland) Ltd, a fully licensed Swiss bank. Some people will argue that Saxo Bank is still a foreign broker, but a Swiss investor will only deal with the Swiss entity, subject to the same rules as any Swiss broker.

So, there is little difference between dealing with a Swiss broker and a foreign broker that is domestically regulated. Therefore, I will sometimes refer to it as a Swiss broker, but it is more a Swiss-regulated broker.

In 2019, Saxo Bank acquired BinckBank, significantly increasing its size. Thanks to scale, Saxo Bank was able to reduce fees later and grow faster.

Indeed, in January 2024, Saxo Bank drastically reduced its fees in Switzerland (and other countries). Some fees were reduced by an order of magnitude.

I was really surprised by these changes because Saxo used to be an expensive broker. But this is excellent news for Swiss investors. And I hope that other Swiss brokers follow this trend and reduce their costs.

Saxo Features

We can start by looking at Saxo features. With Saxo, you can trade many different products:

- Stocks and ETFs

- Bonds

- Mutual Funds

- Options

- Futures

- CFDs

- and more…

So, you should have more instruments than you need. Most people will only need stocks, bonds, and ETFs for their investment journey.

Saxo has a full Swiss banking license from FINMA. This is a good point because many Swiss brokers are not banks but only securities dealers and use a third-party bank as an intermediary.

Saxo offers an excellent range of ETFs. This range of ETFs include US ETFs, meaning there is no penalty by using inferior European ETFs.

Saxo is available in German, French, English, and Italian. However, the Italian support is partial only because the website and the onboarding are not available in Italian.

A limitation of Saxo is that you cannot register your shares in the share register. This means you will not be able to get some shareholder perks if you want to (for instance, getting Lindt chocolates). On the other hand, you can vote by proxy on the shareholder meetings, but this will cost you some fees.

Another limitation is that Saxo does not offer access to fractional shares on stocks and ETFs.

Finally, it is worth mentioning that Saxo only accepts deposits from your personal accounts (in your name) and not third-party accounts. This is done for security reasons. And as a result, withdrawals are also limited to your personal accounts, which is an important security feature.

So, with the basics covered, we should delve into the details of Saxo Bank for a Swiss investor.

Saxo account tiers

Saxo has three different account tiers:

- Classic, without any minimum

- Platinum, with a minimum initial funding of 250,000 CHF

- Same as Classic, but lower prices

- Priority support

- VIP, with a minimum initial funding of 1,000,000 CHF

- Same as VIP, but even lower prices

- Access to trading experts and events

In this review, I focus on the Classic account. However, it is important to know that you can get even better conditions if you have more initial funding.

Even if you start with a Classic account, you can switch to a higher tier once you reach the necessary threshold.

Saxo Fees

When investing long-term, it is critical to limit your fees. You want your money, not to give it to your broker. So, we must look at Saxo’s fees in detail.

First, you will pay no custody fees. Saxo used to have custody fees, but they were removed in February 2025. Saxo does not have any extra account management fees or inactivity fees.

For all the stock exchanges I have checked, the trading fees are the same for stocks and ETFs. So, here are the fees for some major stock exchanges:

- SIX Swiss Stock Exchange: 0.08% (minimum of 3 CHF)

- Euronext Paris: 0.08% (minimum of 2 EUR)

- London Stock Exchange: 0.08% (minimum of 3 GBP)

- NYSE: 0.08% (minimum of 1 USD)

- NASDAQ: 0.08% (minimum of 1 USD)

These fees are good for Switzerland. The percentages are relatively low, and the minimums are excellent. The fees are the same for selling and buying stocks and ETFs.

As a Swiss investor, you must often trade in foreign currencies because few suitable ETFs are priced in CHF. When this happens, you will need to pay a currency conversion fee.

Fortunately, Saxo has an excellent currency conversion fee of 0.25%, the best among Swiss brokers.

We use Saxo to invest because Saxo has all the features we need, at an excellent price.

Finally, we must also look at the Swiss Stamp Tax Duty fee. Being regulated by FINMA as a Swiss entity means paying this fee for each stock market operation. You will pay 0.075% for Swiss shares and 0.15% for foreign shares. This fee is the same for each Swiss broker.

Overall, these fees are outstanding. Saxo seems much cheaper than most Swiss brokers. The currency conversion fee is especially nice compared to other brokers, where the average is more than 1%.

Starting from 2025, Saxo will generate e-tax statements for free! Among the traditional brokers, Saxo is the only one doing that for free. These certificates are optional, since you can file your taxes without them. However, if you do not use it, you will need to enter all your operations one by one. So, it is really good that brokers start to offer this for free!

Securities Lending

As of the 26th of June 2024, you can enable Securities Lending on your account. If you do so, Saxo will be able to lend your shares to other market participants.

By doing that, will receive 50% of the revenue generated by securities lending.

Since your shares will be lent, there are some extra risks. If Saxo bankrupts while some of your shares are lent, you are not entitled to the shares directly, only to the collateral value. Saxo will always provide 102% of the loan value as collateral. In theory, you cannot lose much. The more you can lose is the difference between the current share value and 102% of the value when the lending started.

While shares are lent, you also lose your voting rights.

It is really up to you to decide whether this feature is worth it for your strategy. Depending on your portfolio, it could be interesting to get some extra income.

If you want additional information, I have an entire article on securities lending.

Saxo AutoInvest

Starting in September 2024, Saxo introduced the AutoInvest feature. This feature lets you automatically invest in a portfolio of ETFs.

With that feature, you can choose a portfolio of ETFs and a monthly investment. Saxo will then invest automatically each month in your portfolio, based on a fixed monthly amount. Moreover, the purchase fees are waived, and there are no extra fees for using that feature. The sale fees still apply. Stamp duty and currency exchange will also be charged if they apply to these fees.

This is a great feature, but there is a catch. You cannot use all ETFs, only a selection (more than 100 ETFs) provided by Saxo. And this selection does not contain any US ETFs or any Vanguard ETFs. So, on one hand, we are saving on transaction fees, but on the other hand, we are losing on US ETFs. This can be a great feature if you do not plan to invest in US ETFs or if you have a small portfolio where purchase fees outweigh the advantage of US ETFs.

If you are interested in this feature, I wrote an entire article on automating your investments with Saxo.

Margin loans

As of July 2025, Saxo added support for margin loans (often called Lombard loans). This feature lets you borrow money against the value of your stocks.

Saxo has very interesting margin rates and has a high leverage capacity. This is a great feature for advanced investors that want to either withdraw money without selling stocks or want to invest with leverage.

If you want to learn more about this feature and see how Saxo compares against other brokers, you can read our article on margin loans.

Opening an account at Saxo

Opening an account with Saxo is simple. Everything happens online from their website, which should not take more than 15 minutes.

The online application is fairly straightforward and similar to most brokers these days. It consists of three main steps:

- The usual form filling.

- Approval of your account (proof of identity and residency).

- This is done either with your webcam or from your phone.

- You will need to have your ID ready and be in a well-lit place.

- Funding.

I will not bore you with the details of each step because they are easy to go through. Overall, it should take about 10 minutes to create the account fully. The only thing that can take time is the funding, which can only be done through a wire transfer. The funds may take time to arrive in Saxo.

There is no minimum for opening an account. This is good news because you can start trading with little money. This is great if you want to test a service. And since there is no custody fee, you can test the service with little fees.

So, overall, opening an account at Saxo will be very simple.

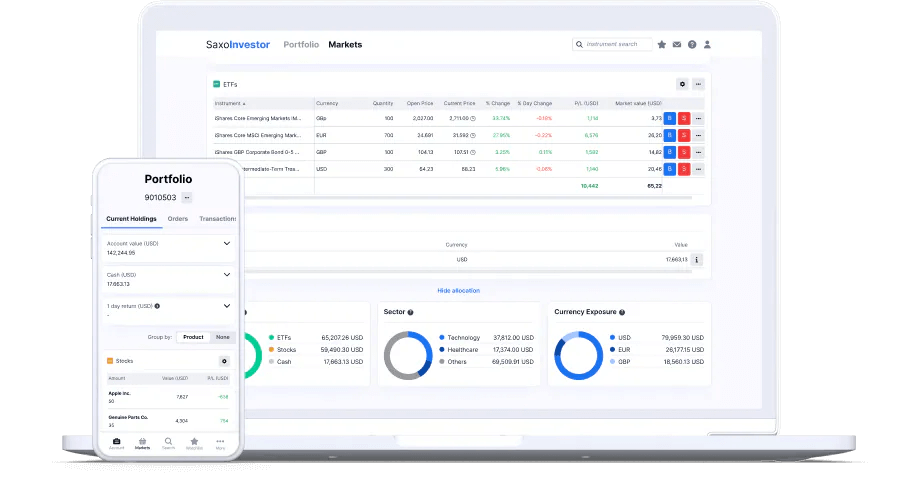

Trading with Saxo

To trade with Saxo, you have several options:

- The SaxoTrader platform, supported on web, mobile, and desktop

- This is the default interface for most clients on the browser, allowing you to do all your trade operations and get access to data.

- The SaxoTrader platform is also available as a desktop application on PC and Mac, supporting up to 6 monitors.

- The SaxoInvestor platform, supported on mobile and desktop.

- A simple investing platform done for simple investors. This interface is limited to stocks, ETFs, bonds, funds, and options.

- The idea is to provide only the necessary features and make it easier.

In most cases, simple investors will have more than enough features with the SaxoTrader web interface or the SaxoInvestor platform. And people preferring mobile trading can also do it with both apps. But it is good to have advanced options for investors that need them.

Overall, everybody should find what they need to trade with Saxo.

If you want all the details, read my guide about buying an ETF with Saxo.

Is Saxo safe?

Before using a broker, you must ensure it is as safe as possible.

Saxo is regulated in Switzerland by FINMA. And all its other entities are also well-regulated in different countries. As they have to obey many regulations (by being in many countries), they have to run a tight ship.

Saxo has been well-established since 1992. It has also been profitable for several years. Financial security is a good sign because the risks of going bankrupt are slim.

Saxo is a bank. Therefore, it does not have to use another custody bank. However, like any Swiss bank, your cash will be protected by Esisuisse. This protection guarantees up to 100,000 CHF per person.

The securities should be safe in the event of bankruptcy because they are held in segregated accounts in your name.

Saxo enforces a second-factor authentication (2FA) to protect your account further. 2FA is essential for your online personal finances! Currently, they only offer SMS 2FA. While it is much better than nothing, I would prefer a more robust 2FA option.

You can also choose to trust a device on which you log in. You only have to enter your second factor once, not at every login. While this is convenient, it reduces security and should be avoided, in my opinion.

As mentioned before, Saxo will only accept deposits from your personal accounts. And it will only accept withdrawals to your accounts, which is an important security feature.

Investing with Saxo is safe, like investing with any other Swiss broker.

Saxo Reputation

We should also look at a broker’s reputation before using it to invest in the stock market.

I generally use TrustPilot as a source of reviews. So, we can start by looking at the reviews of Saxo Group on TrustPilot. It is essential to mention that this includes reviews for all parts of Saxo, not only the Swiss entity. Overall, Saxo gets a 3.7 score out of 5, which is not great but also not horrible for brokers.

We can also find reviews for Saxo Switzerland on Trustpilot. Here, Saxo gets a score of 4.4 out of 5, which is great. However, this is only out of 75 reviews, which is a very low number.

Looking at the negative reviews, we can find a few common themes:

- Difficult to reach customer support.

- Fees are too high (before the changes from 2024).

- Difficult to fund the account because of KYC procedures.

- There are a few technical and speed issues on the platform.

On the positive side, we can find the common themes:

- Good customer service.

- Easy-to-use platform.

- Good execution of trades.

After reading through many of these reviews, I am not worried about the negative comments or the global score. First, many people complain about the fees, but I would guess that most did not read all the fees carefully before. This happens in almost all brokers I have reviewed.

As for customer service issue, this is also the same in almost every broker. Sometimes, it is difficult to resolve some issues, and people get heated and post negative comments. But reading into the positive reviews, it looks like there are also some positive reviews of the customer service.

I also looked at the Google reviews of Saxo Switzerland. They got 4.3 stars out of 5. The negative and positive reviews are very similar to those on TrustPilot, with more positive reviews than before. Again, this also includes people using a broker without reading their pricing structure.

Overall, I think Saxo’s reputation is good but not impeccable.

Alternatives to Saxo

It is always important to compare a broker with its alternatives. We should compare Saxo with at least Interactive Brokers (a foreign broker) and Swissquote (a Swiss broker).

Saxo Bank vs Swissquote

Everything you need to start investing in the stock market! Open an account with Swissquote and get 100 CHF in trading credits with my code MKT_THEPOORSWISS.

- Swiss broker

- Easy to use

Swissquote is a well-established Swiss broker. It provides many features, and its prices are decent, as far as Swiss brokers go.

Both brokers have a good reputation and have been established in Switzerland for a long time. They are both regulated in Switzerland and will provide the same level of security. They both offer access to many stock exchanges. And since they are both in Switzerland, they must levy Swiss Stamp Tax Duty.

We start with the custody fees. You pay nothing at Saxo, while you pay 200 CHF per year at Swissquote, a significant advantage for Saxo. Also, Swissquote charges an extra 0.03% fee (without maximum) on assets above one million CHF.

Fortunately, neither of these brokers has any extra inactivity or management fee. And both brokers have an excellent range of ETFs, including US ETFs.

We need to compare the trading fees of these two brokers. On the SIX Stock Exchange, here are some examples of costs for these brokers:

- 500 CHF: 3 CHF at Saxo and 3 CHF at Swissquote.

- 2000 CHF: 3 CHF at Saxo and 10 CHF at Swissquote.

- 5000 CHF: 4 CHF at Saxo and 29 CHF at Swissquote.

- 12000 CHF: 9.60 CHF at Saxo and 49 CHF at Swissquote.

The differences are pretty significant. Saxo can be several times cheaper than Swissquote!

Here are a few examples of trading fees for a stock on the NYSE:

- 500 USD: 1 USD at Saxo and 3 USD at Swissquote.

- 2000 USD: 1.60 USD at Saxo and 10 USD at Swissquote.

- 5000 USD: 4 USD at Saxo and 29 USD at Swissquote.

- 12000 USD: 9.60 USD at Saxo and 49 USD at Swissquote.

Again, the differences are significant. Saxo is, again, much cheaper than Swissquote.

Another significant advantage of Saxo is its currency conversion fee. Indeed, at 0.25%, Saxo is almost four times cheaper to convert currency than Swissquote at 0.95%.

Overall, Saxo appears to be significantly cheaper than Swissquote. This is excellent news because we have few affordable brokers in Switzerland.

If you want even more information, you can read my full comparison of Saxo vs Swissquote.

Saxo Bank vs Interactive Brokers

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Finally, we should also compare Saxo Bank with a foreign broker, Interactive Brokers.

Both brokers are well-regulated and have a good reputation. Saxo Bank is regulated in Switzerland, while Interactive Brokers is regulated in the UK and US. From a safety standpoint, both brokers are on the same level.

Neither of these brokers has custody fees, inactivity fees or any other account management fees.

For trading fees, I will use the Interactive Brokers Tiered pricing system. This system is generally cheaper for small operations but not always for large operations.

On the SIX stock exchange, here are the fees for both brokers:

- 500 CHF: 3 CHF at Saxo and 4.45 CHF at IB.

- 2000 CHF: 3 CHF at Saxo and 4.68 CHF at IB.

- 5000 CHF: 4 CHF at Saxo and 6.13 CHF at IB.

- 10000 CHF: 8 CHF at Saxo and 9.38 CHF at IB.

Interestingly, Saxo is cheaper than IB for operations on the Swiss Stock Exchange. This is precisely what I would expect of a Swiss broker. However, many Swiss brokers are more expensive than Interactive Brokers.

Here are a few examples of trading fees for a stock on the NYSE:

- 500 USD: 1 USD at Saxo and 0.36 USD at IB.

- 2000 USD: 1.60 USD at Saxo and 0.41 USD at IB.

- 5000 USD: 4 USD at Saxo and 0.51 USD at IB.

- 10000 USD: 8 USD at Saxo and 0.67 USD at IB.

IB can be significantly cheaper on US stocks. However, I am still impressed by how Saxo comes close to IB. Other Swiss brokers are much more expensive than IB.

Another advantage of IB is that you will save on stamp tax duty since this tax is only due to Swiss brokers.

Finally, currency conversion is 0.25% at Saxo Bank, while IB charges 2 USD for each conversion. So, Saxo will be cheaper for conversions below 800 USD, and IB will be cheaper after that.

If you have a portfolio that uses US ETFs or stocks, Interactive Brokers will be significantly cheaper than Saxo. But Saxo is quite competitive.

For more information, read my detailed comparison of Saxo and Interactive Brokers.

Saxo Bank FAQ

How much is the currency conversion fee at Saxo?

You will pay 0.25% currency conversion fee for each currency conversion.

Can you buy US ETFs with Saxo Bank?

Yes, since August 2024.

Who is Saxo Bank good for?

Saxo bank is good for Swiss investors that look for a very affordable Swiss-regulated broker with many features.

Who is Saxo Bank not good for?

Saxo Bank is not great if you want to minimize fees and are open to foreign brokers.

Do you pay custody fees with Saxo?

No, since February 2025, you do not pay any custody fees with Saxo.

Can you register Swiss shares in your name with Saxo?

No. Currently, this is not possible with Saxo.

Can you open joint accounts with Saxo?

Yes. When registering the account, say that you are not the sole beneficiary of the account, and you will then have to finalize the account as a joint account (extra paperwork).

Saxo Bank Summary

Looking for the best broker?.Discover the lower fees, 0 CHF custody costs, and why the Saxo Bank broker is now a top choice for investors.

Product Brand: Saxo

4.5

Saxo Bank Pros

Let's summarize the main advantages of Saxo Bank:

- No custody fees

- Excellent prices

- Excellent currency conversion fee

- Many investments available

- Well-established company

- Good security

- Access to US ETFs

- Free e-tax statements

Saxo Bank Cons

Let's summarize the main disadvantages of Saxo Bank:

- Onboarding not available in Italian

- Cannot register Swiss shares in your name

Conclusion

Start investing with a Swiss broker at incredible fees! Start trading with Saxo Bank and get 200 CHF in trading credits.

- Low currency conversion fee

- Swiss broker

Saxo is a good, well-established, and very affordable Swiss broker. This service offers access to all the stock exchanges you need and many investment products. When compared with other Swiss brokers, they are consistently among the cheapest.

I appreciate that Saxo reduced its fees significantly. I hope this will start a good trend in Switzerland, where many services are overpriced. If you want to see how this compares against an existing broker, you can read my comparison of Saxo and Swissquote.

I currently use Saxo as my secondary broker (Interactive Brokers is my primary broker). And I am happy about the experience on the broker interface.

If you are interested in Saxo, you may be interested in learning how to buy ETFs with Saxo.

What about you? What do you think of Saxo?

More reading

Should you use multiple brokers?

Having a single broker is simple, so why would you want multiple brokers? This article outlines multiple reasons why this may be good for you.

Automate your investments with Interactive Brokers in 2026

Put your investments on auto-pilot with Interactive Brokers, in a very easy way, available to anyone! It's time to automate your investments!

Swissquote Review 2026 – A great Swiss Broker

The bank leader. Read our 2026 review of Swissquote. We analyze their fees, safety, and features to see if Switzerland's largest online bank is for you.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste

I tried to compare investing in the Invesco FTSE All-World ETF through investment plans at Neon and Saxo. Here the major differences I came up with.

Neon:

Buy – 0% (since its one of the selected 0% ETFs)

Sell – 0.5%

Currency Conversion Fee – 0%

Total – 0.5%

Saxo:

Buy/Sell – 0.08%

Currency Conversion Fee – 0.25%

Total – 0.41%

Saxo would be less than 0.1% cheaper. Am I missing something major that I would have to consider?

I am aware of some small differences. It is for example better to have a fee while buying compared to having the same fee while selling. Assuming that the value of the ETF goes up. ;)

Greets J

Hi Jay,

As you pointed out, the fee while buying is better than the fee while selling. I think you are underestimating this. If you are investing for the long-term, the final portfolio should be more than 2x the initial portfolio.

And I think you missed computing the currency conversion fee twice with Saxo. So, it’s 0.33% for buying and then 0.33% for selling.

One slight thing you missed is also that you will receive dividends (unless you go with an Acc ETF) in EUR and this will be converted at 1.5% fee with Neon. So that’s an extra fee each year.

Other than that, i think you are good.

Hi Baptiste

Thanks for the quick answer. I’m starting to get the hang of it.

Just to expand on the previous example with your input. I’m looking at Acc ETFs. Let’s assume we invested all capital (100CHF) at once and sell it exactly when its value has doubled. We would then pay:

Neon: Sell(200CHF)0.5% = 1CHF

Saxo: Buy(100CHF)0.33% = 0.33CHF + Sell(200CHF)0.33% = 0.66CHF => Total = 1CHF

So it seems (once again ignoring some ‘minor’ factors) that after the value of an investment doubles Saxo is cheaper.

I already invested quite a bit with Neon and am pretty happy with how ‘easy’ it is for me to follow their pricing model. This also made it easier for me to get started with investments(time in the market😉). I don’t think I will switch to Saxo because selling and rebuying will probably incur more costs than savings, but I will do some more calculations.

Thanks for your help!

Greets J

Yes, your math looks right now. The more increase in value you get, the more interesting Saxo will become.

And as you said, selling and rebuying can be expensive. You could consider Saxo as your secondary broker, but if you are happy with Neon Invest, you could totally stay with them, nothing wrong there :)

Hi Baptiste

While talking to a friend he mentioned that it is also possible to transfer Assets for 100CHF each from Neon: https://www.neon-free.ch/en/faq/is-it-possible-to-transfer-securities-from-neon-to-another-bank-or-another-broker

Do you have any experience with such transfers? This might be a way to avoid selling and rebuying assets and still profit from lower selling fees at a different broker. I am aware that these fees might change in the future 😅

Thanks for your input and helping me learn!

Jay

Hi Jay

Yes, you are right, you can transfer assets to another broker. This works like a standard broker transfer.

And you could indeed use that strategy (pending any future change of fees) to mitigate the selling fees.

Hi Baptiste,

I thought I’d share my experience with the Saxo joint account, because it is not so obvious:

You can open a joint account for a couple, giving each person a login with full rights. The process is paper based, requiring IDs validated by Post/SBB (costs a little). So it is a bit more inconvenient than an individual registration process.

A joint account is similar to an individual account with power-of-attorney granted to the partner. In the event of death the joint account is completely blocked until inheritance is sorted out.

Through this investigation I discovered the Saxo telephone support is good in CH.

Hi Sean,

Thanks for sharing your experience, this is very valuable.

We also did that in our case. It was not very convenient, but it was also not such a hassle. The funny thing is that it was easier to open a joint account at IBKR than a joint account at Saxo, go figure…

Hello Baptiste

I am alarmed.

Today is now the 3rd time that my buy order of a stock has been bought at a higher price than I specified. How can the Saxo system do this?

The bought price is only slightly above the price which I ordered, but nevertheless I am alarmed and it has caused me an unnecessary loss.

Today it was some stocks in Rieter in a falling market and my order was executed at above the ordered price. As I ordered Rieter using my CHF account there can be no question of an exchange rate effect.

It’s the 3rd time this has happened in the space of 2-3 months. I have placed orders on other stocks which have been executed at the ordered price, so how can it happen in only 3 cases out of about 10-12?

This is very disturbing and I would appreciated your expert opinion.

Regards, John

Hi John,

Sorry to hear about your experience. I have never noticed that but I am only using market orders, so never have a limit on my orders.

I would not expect that with limit orders.

I would recommend asking support how this is possible.

I recently opened an account with Saxo and made some trades.

I also have an account at SQ which I opened before saxo removed their custody fees.

Am thinking I wish I had waited because saxo is quite a bit cheaper on trades and their FX conversions are and way better than SQ.

One nice thing about SQ is the no cost virtual debit card which is multi currency and comes with a 0.5% cashback in the form of trading credits.

Hence when I receive USD and EURO dividends, I can spend these directly using the virtual debit card.

Yes, the fees are much better indeed. But SQ is really not a bad broker.

And it’s true that the virtual debit card can be useful if you don’t have to convert money, it’s a good idea to use USD/EUR dividends with these, I did not think about that before.

I have also opened an account with Saxo and have done some trades. I am surprised at the much lower fees compared to other Swiss platforms, and I question whether such a big difference is necessary at the present time. Although I have transferred significant funds to Saxo, I am not yet comfortable with their very low fee income causing low profitability in recent years. It looks like they could be leaning unnecessarily too far out of the window.

On the other hand, J. Safra Sarasin which is part of the large Brazilian Safra Group is the majority owner of Saxo Bank, which gives some confidence. I prefer to keep the majority of my assets at UBS (where I have a flat fee arrangement) for security reasons, until Saxo becomes significantly more profitable. This could be difficult because of unfavourable reactions to any increase in fee levels. Unfortunately the economics of Saxo Bank are not published, unless somebody here has up to date infos in addition to the Wiki entry.

Thanks

Actually, Saxo is quite profitable, they had record profit in 2024. You can read their financial statements here: https://www.home.saxo/en-ch/about-us/investor-relations

However, this shows the health of the entire group, not only Switzerland, but if I read the document correctly, the Switzerland entity has generated a profit of 5 million CHF in 2024.

Can you trade FX directly (buy USD for CHF), to beat the 0.25% FX fee?

I think you can, but FX trading is limited to a minimum of 10’000 units. So if you are doing large transactions, you should be able to save money that way.

Hi

thanks for the great review and also the book I’m just reading! I wonder if you could go into more detail regarding cost. Everybody only seems to take into account buy costs (0.08%), but there are sell costs (0.08%) and spread (0.054%). All-in-all it’s 0.215%. Is this still good? How is this with other brokers, e.g. IB?

BTW, this also seems to be missing from moneyland’s comparisons.

Thanks, Mark

Hi Mark

I am glad you like the review and hopefully the book as well :)

For almost all brokers, the buy and sell fees are the same, that’s why I do not detail them both. I will add a note in the article to make sure this is clearer.

Normally, the spread is inherent to the market, not to the broker. I am not aware of any 0.054% fee with Saxo.

If you invest a lot in US ETFs, no other broker comes close to IB in my tests. You can check out the broker comparison tool for that: https://thepoorswiss.com/broker-comparison-tool/

Hello Readers of the Blog,

I opened a bank account with Saxo and I really like it. Easy to open, nice GUI, reliable, etc.

Just one recommendation: do not transfer too much money, because otherwise they start to investigate where the money comes from, and asking a lot of documents e.g. copy of your tax return, copy of your payslips, evidence where your salary is credit, etc. A nightmare, have never experienced something like that with other banks. I decided to close the bank account instead to provide all these information, which can (in theory) stored and exchanged with SAXO foreign subsidiaries or you do not know where these information are landing.

Very sad

Hi Lorenz

Aren’t all banks and brokers supposed to ask this eventually? There are some strict AML rules that require information like this.

Do you mind sharing how much money you are talking about? A ballpark. Maybe it was because you very quickly increased the account balance, and it triggered something on their end.

He said “transfer”. If the money is transferred from another Swiss bank, no I would not expect these questions. Or, I would expect Saxo to accept a copy of my account statement/transactions/balance. In my application which has not been approved yet, I already told Saxo that my money will come from UBS.

I am very interested knowing how big the transfer of money is that we are talking about, because I intend to transfer over 100,000 and I don’t want this kind of hassle. If I know how much money causes the problem, I will transfer it more gradually. Saxo will be getting the use of my money without paying interest. If they don’t like it, I will send less, but I need to know how much that is.

What’s up with “transfer”? I would expect banks and brokers to adhere to AML on a wire transfer. I am not sure a bank can forego AML just because the money comes from another Swiss bank.

But it would be interesting to know how much we are talking about.

Money transfers that I managed were funds from my UBS account and within the savings limit of the annual salary that I gave when opening the bank account.

If Saxo suspect that I am involved in criminal activities or money laundering, they can also notify the authorities: have nothing to hide and they have all the relevant information. I personally do not see any reasons to disclose my tax return to a Bank.

In 40 years and working with many different banks, never happened to me. Perhaps I was unlucky 😂

Thanks for sharing more details, Lorenz.

You were perhaps unlucky. I never had such events happen either on my end. But I never transferred massive sums either, since I never switched brokers for a massive sum of money.

I’ve been through this many times with multiple banks (PostFinance, SwissQuote, ZKB, etc.). Transfers over 6 digits unfortunately always trigger such KYC/AML checks.

Hello Baptiste,

I did open an account with Saxo and wanted to use the auto invest account.

During the setup of the account and after choosing CHSPI as ETF I got the message below. I have asked customer support what it means and they have no clue (sic!).

Do you happen to know?

Thank you.

Best regards,

Guido

This is the messsage:

Remunerations from product providers:

For its distribution activities and related services the bank receives remunerations from some product providers. The one-off amount of the remuneration is calculated by multiplying the percentage by the value of the respective investment volume at purchase. The compensation may change at any time and ranges from 0.03%-0.08%. By investing in Exchange Traded Funds under Autolnvest, the client expressly agrees that the remuneration shall remain in full with Saxo Bank (Switzerland) Ltd., should the delivery of the remuneration to the client be required by law and no agreement to the contrary be concluded. The client expressly waives any right to the restitution of any remuneration.

Hi Guido

I think this only means that Saxo gets a kickback when you use AutoInvest with iShares and Swisscanto. This is how they can waive the buy fees with these products on AutoInvest. And this is also why they only provide two ETF provider in this feature.

Hello

I opened a saxo account with your link and funded it initially with 10 chf. All fine and account active. However I do not see the trading credits. When and how should they be credited? Thank you!

Hi Erikk

The trading credits is not a balance on your account, it means you will save 200 CHF in fees. The first fees (up to 200 CHF and 90 days) are free.

Yes that was clear. Just i do not see any mention of these credits. I called Saxo they told me it takes up to 3 days to see this mentioned on my account

Thanks, I did not know it would take that long to show up on the accounts. Let me know if they do not appear, I can contact them as well to make sure the system works. Thanks for using my link.

Hi Baptiste

Thank you for the excellent Infos. I am thinking of moving my trading from UBS to Saxo and have a couple of questions:

1. I will start with a Classic account and invest more after a while moving me up to the next account level. But I don’t understand the difference between SaxoTraderGo and SaxoInvestor. What are the advantages between these 2 platforms if I only invest in stocks (in various countries)?

2. Does Saxo give Lombard Credit secured on my stock holdings?

Thanks

Hi David

1) These are simply two platforms for the same account. Once you have created your account, you can try both. SaxoInvestor is supposed to be simpler for passive investors, while SaxoTraderGO is supposed to be simpler for slightly more active investors. I personally use SaxoTraderGo even though I am a passive investor since I find it more intuitive.

2) I do not think they do. From what I can see, they only offer margin investing on Forex, Options, CFDs and futures, not on stocks.

The option to request a Lombard loan has been enabled recently, see https://www.home.saxo/en-ch/accounts/lombard-loan

Thanks for sharing, this is great news!