Neon Bank Review 2026: A Great Swiss Digital Bank

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Neon is a great Swiss digital bank that offers an affordable bank account. As Swiss banks become increasingly expensive, switching to a free bank account is excellent.

With a free bank account from Neon, you can easily save money on your banking fees. You will not find a better deal anywhere else!

Over the years, Neon has been adding new features over time and has become one of the best digital banks in Switzerland.

Sign up for a free bank account with Neon today!

I have been using Neon for several years. So, I want to share my experience in this Neon review.

In this article, we see what Neon is! And whether you should use it? How does it compare to other Swiss banks and neo-banks?

If you keep reading to the end, I even have a special Neon code for you!

| Monthly fee | 0 CHF |

|---|---|

| Card | Mastercard Debit |

| Currencies | CHF |

| Withdrawals in Switzerland | 2 CHF per withdrawal |

| Withdrawals abroad | 1.50% |

| Languages | English, French, German, and Italian |

| Custody bank | Hypothekarbank Lenzburg |

| Depositor protection | 100’000 CHF |

| Customers | 250’000 |

| Established | 2017 |

| Headquarters | Zürich, Switzerland |

Neon

All the services you need to pay, save and invest, in a neat package, with extremely good prices!

Use code tpsummer to get one year of Neon Plus and your debit card for free!

- Invest with great fees

Neon is one of the earliest digital banks in the Swiss banking industry. It is an entirely digital bank. You will do everything with your smartphone. They do not have any office you can do business at.

Neon started in 2019. But even though the company is only five years old, Neon has reached 250,000 customers in 2026. And they are expanding features quickly. The company founders are Simon Youssef and Michael Noorlander.

Their main point is to provide free banking to everybody in Switzerland. They can afford excellent prices since they do not have big offices, not many employees, and do not pay massive bonuses to their managers. Unfortunately, most large banks in Switzerland are not free anymore!

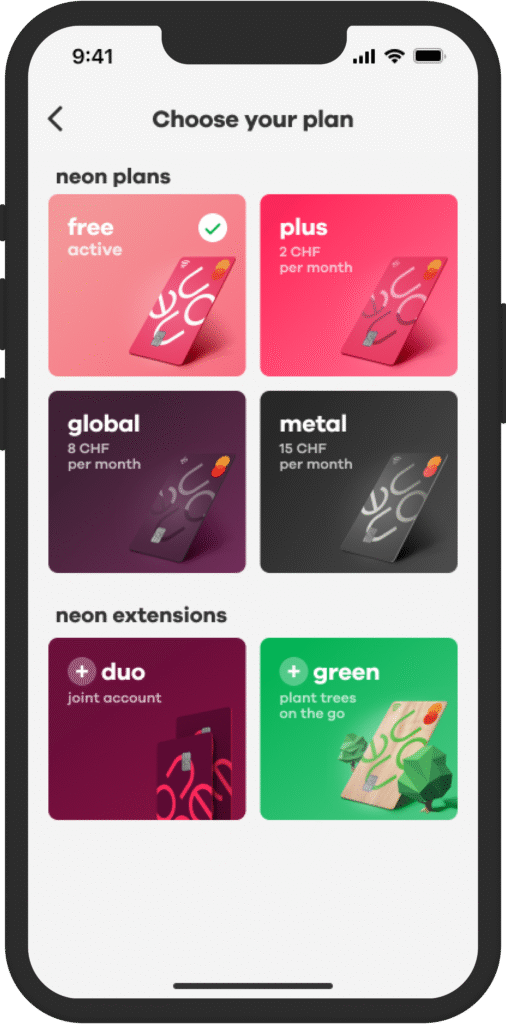

In May 2025, Neon has refreshed their plans. They now have 4 different plans (or tiers):

- Neon Free (the default account)

- Neon Plus

- Neon Global

- Neon Metal

Additionally, they also have two extensions:

- Neon green, to make the account more sustainable

- Neon Duo, to make the account into a joint account

We will see each of these tiers and extensions in the sections below, especially since they vary in fees and features.

There are some limitations as to who can open a Neon account:

- Only Swiss residents can open an account. The identity check system supports people from 19 different countries!

- Foreigners need a B or C permit to open an account. You will need to present your residency card to open an account.

- You must be over 15, which is slightly younger than other banks.

- You need to pay taxes exclusively in Switzerland.

- You cannot be an American citizen.

These limitations are reasonable. Neon is an account for people living in Switzerland, and most people in this category can open an account! Unfortunately, the limitation for American citizens is in effect with many small banks that do not want to deal with the complicated regulations for these clients.

Do not pay for a bank account. Use Neon, the new Free Digital Bank.

Is Neon a Bank?

Interestingly, Neon is not a bank! Indeed, they do not have a banking license. However, they do not need one! An official bank, the Hypothekarbank Lenzburg (HBL), manages your accounts.

The most significant advantage is that your money is fully insured according to Swiss laws, contrary to other digital banks. So, 100’000 CHF of your account will be protected by law!

Moreover, this also means Neon can focus on its mobile application and products, and the custody bank can focus on managing money!

So, there is no disadvantage to Neon not being a licensed bank.

Neon Features

So, we first look at the features of the Neon bank account.

Neon is a digital bank account, so you must access it with a smartphone. It is available on Android, iPhone, and Huawei (without Google Play Store). And you can even access it on a rooted Android phone. Therefore, you should be good regardless of your phone.

You can see your balance and make payments and transfers from the application. In addition, you will get some basic information on how your account is doing (expenses versus earnings). And all these features work pretty well. I use Neon monthly to pay my bills, and I am pretty satisfied with their system.

With Neon, you can also send money directly to other Neon users. So, if you have people in your contacts with a Neon account, you can send them money directly.

With your Neon account, you will get a Neon Mastercard Debit. Until September 2024, Neon was coming with a Mastercard prepaid card, but this has changed to a Debit card. In practice, this should not change much but Mastercard Debit cards are slightly more widely accepted than prepaid. With this card, you can pay in Switzerland and abroad and withdraw money. And as we will see later, the fees on this card are outstanding!

Neon was the first digital bank to introduce support for electronic bills (e-bills). The support is simple since they simply use the SIX portal for e-bills. But it works well.

The application also lets you freeze your card temporarily. This feature is great if your card is lost or stolen.

Since May 2022, you can have Spaces in your account. It means you can create sub-accounts dedicated to your needs. For instance, many people want to save money for holidays in a different account.

It is important to note that you can get a higher interest rate on your Spaces. Currently, you get an interest rate of 0.00% (as of April 2025). On the other hand, there is a limit on the monthly withdrawal, as we will see in the sections below.

You can also use Neon with Google Pay and Apple Pay to pay from your phone, and you can use Neon with TWINT. That way, you will not need a physical card to pay for your groceries!

Neon uses two-factor security to make your account more secure. You need to activate this feature. And you need to use a strong password to ensure nobody can access your account.

A great thing about Neon is that they are available in English and in the three national Swiss languages: French, German, and Italian. These languages make Neon an excellent option for expatriates in Switzerland.

Overall, Neon has more than enough features for any bank user. I do not think anything is missing to make it an excellent bank account.

TWINT

While Neon has support for TWINT, it is unfortunately quite limited. Indeed, Neon does not have its own TWINT app.

Instead, you have two choices. The simplest way is to use the UBS TWINT app that allows to add a debit card. Unfortunately, this only works with the old card from Neon (the prepaid). For new cards issued since September 2024, this will not work. It is also important to know that this app has a 500 CHF monthly limit.

The other option is to use the TWINT prepaid option. This option works with both cards and has no monthly limit. However, you must charge your account beforehand, which makes it much less convenient.

So, if you are a heavy TWINT user, you may want to think about these limitations.

Instant payments

As of June 2026, Neon also offers instant payments. These payments can be an alternative to TWINT.

Currently, instant payments are available to all three premium tiers (Plus, Global, Metal). These instant payments are free for these users. Currently, it is not possible to use instant payments on the free tier.

Neon is among the first banks to introduce instant payments; this is a great extra feature.

Technical issues

A significant issue with Neon is that they often cannot scale when many users are on the platform. In 2023, almost every month, the platform was overwhelmed on the 25th, when people receive their salary and pay their bills. This means that basic banking features were unavailable at the time when people needed them the most.

This was an important issue that Neon acknowledged several times. This issue has already led several people to leave Neon.

This was a major issue in 2023, but this has become significantly better in 2024. In 2025, this is not an issue anymore. I have not had any difficulty accessing the app in many months.

Neon Fees

Originally, almost everything was free. In May 2025, Neon introduced more plans in their lineup.

First, opening an account is free, and there is no management fee! All your payments in CHF will be free as well. Your Neon MasterCard has no yearly fees, either. A free payment card is essential because the essential feature of a payment card is to be free! However, you must pay 20 CHF to deliver your card.

By default, there is no free ATM withdrawal with the card. For every withdrawal, you will have to pay 2 CHF per withdrawal.

The card is also relatively interesting abroad! You will pay an exchange rate surcharge of 0.35% on top of the Mastercard exchange rate when you use the Neon card outside Switzerland or in foreign currencies online.

To save money, we use our Neon card when we are abroad or when we pay in foreign currencies.

If you withdraw money abroad, you will pay a 1.5% fee. Generally, you should avoid withdrawing money abroad with any card.

Neon also has a partnership with Wise for outgoing foreign payments. So, you can profit from cheap foreign currency transfers with Neon. With this, transfers abroad cost a 0.40% fee on top of the Wise fee. This partnership makes Neon the best Swiss bank account for foreign transfers.

These default fees are good, ahead of most traditional banks. But they are not that great compared to some new digital banks or special banking packages.

These are the default fees for the base accounts, but there are also three premium tiers:

- Plus at 2 CHF per month or 20 CHF per year

- Global at 8 CHF per month or 80 CHF per year

- Metal at 15 CHF per month or 150 CHF per year

And these tiers change the fees of some operations and add some bonuses, so we must cover them in more detail.

Neon Plus

Neon Plus has several advantages over the default tier:

- You get 2 withdrawals in CHF for free per month

- The exchange rate surcharge is removed, so you use only the Mastercard exchange rate

- You will only pay a 1.0% fee on withdrawals abroad (default is 1.5%)

For 2 CHF per month (or 20 CHF per year), this tier offers decent value. If you do one withdrawal per month, it is already worth using it. Or, if you spend about 600 CHF per month in foreign currency, it is already cheaper to use Neon Plus over Neon Free.

Neon Global

Neon Global has even more advantages over the default tier:

- You get 3 withdrawals in CHF for free per month

- The exchange rate surcharge is removed (like Neon plus)

- You will only pay a 0.5% fee on withdrawals abroad (default is 1.5%)

- You get back 20% of the Wise convenience fee for international transfers (20% of 0.40% saved)

- You get the card for free when opening an account (20 CHF), but this is only a one-off advantage

- You can get a new card delivered abroad if necessary for free (instead of (80 CHF), but this should be a very rare event

Additionally, you also get some extra insurance when using the card, as we will see in the next section.

At 8 CHF per month (or 80 CHF per year), this tier is too expensive in my opinion. Unless you do a ton of international transfers or withdrawals abroad, you are better off with the Neon Plus account (or even Neon Free).

Neon Metal

Finally, Neon Metal has the most advantages:

- You get 5 withdrawals in CHF for free per month

- The exchange rate surcharge is removed (like Neon plus and Neon global)

- You will not pay fees on withdrawals abroad (default is 1.5%)

- You get back 40% of the Wise convenience fee for international transfers (40% of 0.40% saved)

- You get the card for free when opening an account (20 CHF), but this is only a one-off advantage

- You can get a new card delivered abroad if necessary for free (instead of (80 CHF), but this should be a very rare event

You also get a full package of purchase insurance, as shown in the next section.

For me, at 15 CHF per month or 150 CHF per year, this package is overpriced. The only reason to use it would be if you do a ton of withdrawals abroad or if you do so many purchases in Switzerland that you need the insurance (and there you will lose cashback compared to a credit card).

Summary of Neon Fees

Here is a summary of the most important fees of the four tiers:

| Plan | Neon Free | Neon Plus | Neon Global | Neon Metal |

|---|---|---|---|---|

| Price | 0 CHF | 2 CHF per month or 20 CHF per year | 8 CHF per month or 80 CHF per year | 15 CHF per month or 150 CHF per year |

| Exchange Rate surcharge | 0.35% | 0% | 0% | 0% |

| Withdrawals free per month | 0 | 2 | 3 | 5 |

| Withdrawals abroad | 1.5% | 1.0% | 0.5% | 0% |

| Cashback on international transfers fee | 0 | 0 | 20% | 40% |

In most cases, the plan that makes the most sense is the Neon Free plan. You would need to either spend a lot abroad or withdraw a lot abroad to make other plans worth it.

With the introduction of the new fees in May 2025, Neon has become pricier. We personally will not subscribe to any plan and keep the Neon Free account. But we may be seeking an alternative to save on the 0.35% if that becomes necessary.

Overall, Neon Fees are good, but not exceptional. Recently, many more accounts are available with good currency exchange rates, which was the primary strength of Neon. And these accounts can be found for free. Furthermore, the fact that there is not even a single free withdrawal per month irks me.

Extra insurance with Neon

With Neon Global and Neon Metal, you get several insurances included:

- Three-year warranty on electronic devices

- Shopping insurance, if what you received is not what was advertised, for instance

- Cyber insurance, if one of your online accounts gets hacked, for instance

- Travel insurance, insurance for your luggage, for instance

Additionally, Neon Metal has three more insurances:

-

- Mobile-phone insurance

- Ticket insurance

- Best-price guarantee insurance

These packages cover many more areas I did not cite here. Like all insurance policies, you will need to read the fine print to know exactly what you are getting into.

It is essential to know that these insurance policies only cover what you purchase with the card itself. So, if you purchase a holiday with your credit card, it will not be covered by the travel insurance, for instance. And this means you have to forfeit cashback from your credit card to use the Neon debit card (without cashback).

Medical care outside of Switzerland may also be covered by complementary insurance. Household insurance may cover some issues with your phone, and it is generally possible to get travel insurance on your travels should you decide to.

For me, these insurance packages are not really worth it in most cases. If you want a single package and you have no credit card, this may be interesting, but otherwise a lot of these are already included in credit cards or other insurances. And you would get cashback with a credit card.

Neon Extensions

On top of the four account tiers, Neon has two extensions.

Neon Duo – Joint account

Since 2024, Neon offers joint accounts! Neon is the first digital joint account in Switzerland.

A Neon duo account can be opened for a household of two people where both have already neon accounts. The account costs 6 CHF per month (3 CHF per month for each account).

The Neon Duo account is entirely integrated inside the Neon application, there is no need for an extra app or set of credentials. It is really great that neon started offering these joint accounts!

If you have a premium neon tier, you will profit from it as well in your neon duo account. However, this will only apply to the neon duo card from the person with the premium tier. So, if one of the users only have the premium tier, this will not apply to the purchases with the neon duo card of the other user.

For more information, you can read my article about Neon Duo.

Neon Green – Carbon-Neutral account

Neon Green is the second extension. The idea of Neon is to be carbon-neutral. And to achieve that idea, Neon will plant trees for all Neon Green users. This extension costs 3 CHF per month.

Neon Green users can choose between a wooden card and a recycled PVC card. Both of these cards have a very low carbon impact.

Neon will plant one tree for every 500 CHF spent with this account. You would need to spend a lot of money with your account for this to make a difference.

I am not convinced by this approach. Planting trees is good, but there are better ways to impact the climate. And 3 CHF per month still requires you to spend 500 CHF per tree, so the impact will be rather limited.

Neon Limits

Like with most bank accounts, there are some limits to your Neon Bank account.

Most of the limits are related to the card itself. Here are the limits of the card:

- You can withdraw 2000 CHF per day at most

- You can spend 5000 CHF per day online and another 5000 CHF per day in stores

- You can only spend 10’000 CHF per month with the card

These limits are acceptable since they are similar to most payment cards. I have never been over these limits with any of my cards.

There is also a daily transaction limit of 50’000 CHF. In most cases, this will not be an issue. In my life, I only had to do a more significant transaction once (for the down payment on our house). So, it should be fine for most people. But it is still important to know this limit.

If you are using Neon spaces, it is important to know there is a 50’000 CHF monthly withdrawal limit as well.

Investing with Neon Invest

Since July 2023, you can now invest directly from your Neon account! Neon has introduced great trading features where you can trade stocks and ETFs directly in CHF without currency conversion fees.

If you would like to learn more about this nice feature, you can read my Neon Invest Review.

Saving for retirement with Neon 3a

Since November 2025, Neon also has its own 3a. This is a fairly priced product with efficient investment funds.

To learn more, you can read our Neon 3a Review.

User Reviews

If you want more points of view than my own, we can take a look at online reviews for Neon.

On the App Store, Neon got a 4.5-star average rating out of about 7000 ratings. This is an excellent score! On the Play Store, Neon got a 4.2-star average rating out of about 9.7K ratings.

The positive reviews talk about several points:

- Low fees

- Very easy to use

- Nice looking app

The negative reviews also mention several specific points:

- It takes a few days to activate the app since you will receive the code by mail

- People complain they cannot open an account while being out of Switzerland (but this is well explained on the website)

- The app is sometimes a little slow (with many users).

Given the excellent ratings and positive reviews, I would not worry too much about these negative ratings. Most negative reviewers do not read the conditions and complain they cannot open an account.

So, overall, users are extremely satisfied with Neon!

Extra features of Neon

Neon does not have any extra features. But you do not need any additional features! Neon already has all the features you need.

Nevertheless, Neon has several partnerships with interesting digital companies. You can access these deals directly from the application:

- Cheap car insurance with smile.direct

- Cheap Third Pillar with Frankly (my review here)

- Withdraw cash in many shops with Sonect

- Sustainable investing with Inyova (my review here)

It is good that Neon is partnering with innovative companies that care about their customers. This strategy is much better than reinventing the wheel and doing everything. I like Neon’s approach there.

However, these companies are not necessarily the best for your money. For instance, Frankly is far from being the best third pillar available. So, do not choose a financial account only because you have a tiny benefit using it from your bank. Remember that you always need to do due diligence.

Alternatives

We should also compare Neon against some alternatives, both digital and traditional banks.

Neon Bank vs Yuh

|

Best Digital Bank

|

Good to start investing

|

|

4.5

|

4.0

|

|

No custody fees

|

No custody fees

|

|

|

|

|

- Swiss broker

- Very easy to use

- Good fees abroad

- Excellent fees for all operations

- No free withdrawal

- Expensive for large operations

- No fractional trading

- Technical issues on salary day

- Swiss broker

- Very easy to use

- Fractional trading in stocks

- Good fees for most operations

- Hold multiple currencies in your account

- Free withdrawals

- Foreign transactions could be cheaper

- Expensive for large operations

- Cannot transfer shares to another broker

Yuh is a digital bank owned by Swissquote. It is entirely digital, and since no offices are available, everything is done on the mobile app. These two digital bank accounts have much in common.

Both accounts are free by default. You will pay no monthly fee, and all basic operations are free with these two accounts. You can also get joint accounts with both. But Yuh’s joint account is free while Neon is not.

Interestingly, both digital banks offer investing features. You can invest in stocks and ETFs with both. They both have similar features for most investors. But Yuh packs a few extra features like fractional trading, savings plans, and theme investing.

However, there are a few places where they differ:

- Yuh has some free withdrawals, while Neon has none.

- Neon is cheaper than Yuh when it comes to foreign currency exchange (0.75% against 0.95%).

- Neon is also cheaper when investing in foreign stocks and ETFs.

- You can hold multiple currencies with Yuh but only CHF with Neon.

- Neon is significantly more transparent about trading than Yuh.

If you want additional information, I have a full comparison article of Neon vs Yuh.

Neon Bank vs Migros Bank

Before Neon, I was using Migros Bank. Now, we are using both accounts. We can see how they compare with Neon.

Neon is entirely digital, while Migros is still a traditional bank with offices. However, it does not matter much these days. You can do everything on both banks with your smartphone. Migros has a few more options, like broker accounts. But these are not services you should generally take with your bank anyway.

Both accounts are free.

The cards offered by Migros and Neon are very similar. Neon offers a Mastercard, while Migros offers a Visa. Both cards are free and have the same features. Neither of these two offers a Maestro.

You will not be entirely blocked with only a Mastercard, either. And with Neon’s Mastercard, you can pay abroad for a small fee of 0.75%, while it would be costly with Migros Bank (up to 5% reported by users).

I keep Migros Bank as a bank account because it has higher daily limits, and I have my mortgage there.

Another advantage of Migros is that you have no limits on withdrawals. So if you use a lot of cash, you should use Migros over Neon.

Neon is superior to Migros Bank. The most significant advantage of Neon is that Neon’s mobile application is much better than the app from Migros. I have had many issues with the app from Migros. I do not like it. And with Neon, you only need a single card, and you can use it abroad for a fair price!

If you would like to learn more, you can read my review of Migros Bank.

Neon vs Zak

|

Best Swiss Bank

|

|

|

|

|

|

4.5

|

3.5

|

|

|

|

|

|

2 free withdrawals per month

|

Free withdrawals at Bank Cler ATMs

|

|

0

|

0

|

- Pay abroad for cheap

- Cheap international transfers

- Everything from your phone

- Medium limits

- Translated in English

- Difficult to deposit cash

- Expensive withdrawals abroad

- No Maestro card

- Pay abroad for free

- Can deposit cash in account

- Support for e-bills

- Not very transparent fees

- Low limits

- Expensive international transfers

- Expensive withdrawals abroad

- No Maestro card

- No physical card for abroad

- No English support

Another popular digital bank in Switzerland is Zak, from Bank Cler. We can quickly compare both banks.

Both banks are fully digital, and both banks are Swiss. That means they have the same features, more or less, and they have the same security. However, Neon is available in English, which may be important for expatriates.

Neon is much better to pay abroad thanks to its great exchange rate. Indeed, Neon has about a 0.75% surcharge on the interbank rate, while Zak has about a 2% surcharge.

And Neon has an extra advantage for fees. Indeed, by partnering with Wise, Neon can offer affordable international bank transfers.

On the other hand, it is difficult to deposit cash in a Neon account. With Zak, it is easy since you can deposit it at some Bank Cler ATMs.

For me, Neon is significantly better than Zak. If you would like to learn more, read my comparison of Zak vs Neon.

Neon vs Revolut

|

Best Digital Bank

|

Good for travelers

|

|

4.5

|

3.0

|

|

Free

|

Free

|

|

|

|

|

|

yes

|

yes

|

|

no

|

yes

|

- Great support in Switzerland

- Pay abroad for cheap

- Money is insured

- International transfers are not free

- Cannot hold several currencies

- Great worldwide support

- Great transfer fees

- Hold many currencies

- Not transparent exchange rate

- Very limited withdrawals

- Expensive during the weekend

- Poor customer service

- Poor reputation

Another option I have discussed before is using a Revolut card. Revolut allows you to do transactions in foreign currencies with no transaction fees.

Since 2020, Neon has offered free payment abroad with the card in any currency. Free payment abroad is awesome! Furthermore, Neon is cheaper than Revolut since they do not have weekend fees, for instance.

Neon has one big advantage over Revolut. Your assets are insured for up to 100,000 CHF. Assets on Revolut are not insured by law. It is because Revolut is not a bank.

Another advantage of Neon over Revolut is that there is no limit on free withdrawals in Switzerland. With Neon, you will pay for each of your withdrawal, but with no limit. With Revolut, you can only withdraw 200 CHF per month for free.

On the other hand, with Revolut, you can receive money in other currencies for free and hold money in foreign currencies in your account. However, for now, you can only keep CHF on your Neon account, and receiving foreign currencies will not be free.

So you need both a Swiss bank account and a free foreign currency card to minimize your fees! With Neon, I feel you have all the advantages.

Since I started using Neon, I stopped using Revolut. And I will probably close my Revolut account to simplify my accounts.

To learn more, I have made an in-depth comparison of Neon and Revolut.

Neon as a Payment Card

While it is an excellent bank account, it is not the best option as a payment card. If you want to optimize your cash back, you should avoid this card for payments in Switzerland.

The reason is simple: there is no cashback using the Neon card. It is free, but it is not enough to make a good payment card.In my credit card strategy, I am using my Certo One Mastercard with 1% cashback in three shops. This card is free and has some good cashback.

So, you may use it as your bank account. But using Neon as a payment card is not optimal!

Now, will it change your life? No! It is a small optimization. If you are not using payment cards often, you will be fine with Neon only. And if you would rather not carry several cards, Neon is good. Moreover, there is value in having all your expenses in the same place. Indeed, Neon lets you expert your transactions in a CSV file which is a very convenient file format to import your transactions into different applications. Certo One, my credit card, cannot do that. So, I sometimes use Neon to save time on tracking my expenses.

How to open a Neon account?

Opening a Neon account is very easy. You can download the app from the App Store (search Neon in any app store!). Then, you can go through the entire process step by step.

At some point, you will need to authenticate yourself via video chat. This seamless process allows you to open an account in about 10 minutes. Neon will then send you the card by mail.

If you need more information, you can read my guide on opening and using a Neon account.

%seo_title% FAQ

What is Neon?

Neon is a great Swiss digital bank. It is an entirely mobile bank providing modern banking features with no account management fees.

What is Neon Green?

Neon Green is an alternative to the Neon Free account. With Neon Green, every time you spend money, Neon will plant more trees. This advantage makes Neon Green a carbon-neutral account.

Who can open a Neon account?

Swiss residents at least 15 years old can open an account with Neon. Foreigners from 19 countries with a B or C permit can create accounts.

Is Neon entirely free?

Not really. The free tier does not include any free withdrawals (2 CHF each) and there is an exchange rate surcharge of 0.35%.

Is Neon a Bank?

Technically, Neon is not a registered bank in Switzerland. However, your assets are held by Hypothekarbank Lenzburg, a licensed bank. So you have the same security as with any other Swiss bank!

Who is Neon good for?

Neon is great for anyone who wants a digital bank account in Switzerland and does not want to deal with cash too much.

Who is Neon not good for?

Neon is not great if you often get cash, since you cannot deposit it for free in your account. Finally, Neon is not great if you want to make payments in an office, since they are only digital.

Can you deposit cash on your Neon account?

You cannot deposit cash directly to your Neon account. However, there are two ways of achieving this. You can buy TWINT top-ups at Coop or at the Post Office with your cash and then load them to your account. Or, you can generate a QR bill online and then pay yourself at the post office, but this will not be free.

Neon Bank Summary

Neon is a free digital bank in Switzerland. It is entirely free, is used from your smartphone and is an extremely attractive Swiss Bank!

Product Brand: Neon

4.5

Neon Bank Pros

Let's summarize the main advantages of Neon Bank:

- Extremely cheap bank.

- Free purchases abroad and in foreign currencies!

- Cheap transfers in foreign currencies

- Support of ebills.

- Neon was the first digital bank supporting ebills.

- Protection of your assets up to 100'000 CHF

- Excellent reviews

- Excellent reputation

- Fast-growing company

- Carbon-neutral option with Neon Green

- You can freeze the card from the app

- Can be opened at 15 years old

- Mastercard Debit card

Neon Bank Cons

Let's summarize the main disadvantages of Neon Bank:

- The account takes a few days to be fully activated.

- You cannot deposit cash (bank notes) for free in your account.

- You need to wire funds to your account

- No offices. If you have an issue, you have to call support.

- Technical issues often on the 25th of the month.

Conclusion

All the services you need to pay, save and invest, in a neat package, with extremely good prices!

Use code tpsummer to get one year of Neon Plus and your debit card for free!

- Invest with great fees

Neon is an excellent bank for Swiss people. Using it correctly, it is one of the best Swiss banks. You will not have to pay any fees. Neon is currently among the best Swiss digital banks.

If you are still using an expensive bank such as PostFinance, UBS, or Credit Suisse, you should consider changing to a cheaper bank such as Neon! If you do not want a digital bank, Migros Bank is the next best alternative, but you will pay more.

I opened a Neon account several years ago and am entirely pleased. It replaced my Revolut account for usage in foreign currencies. And since the mobile application is so much better than the applications at Migros, we even switched to Neon as our main bank (with Neon Duo, their joint account).

That being said, the new plans introduced in 2025 make it less interesting than it used to be. The base account is still free, but you pay an extra exchange rate surcharge, and there are no more free withdrawals.

If you open a Neon account, please use the code "tpsummer" during the registration process, and you will receive 1 free year of Neon Plus and your debit card for free (20 CHF value). And I will also receive 15 CHF.

If you want more digital bank alternatives, you can look at my comparison of Zak vs Neon.

What do you think about Neon? Do you use this bank?

More reading

UBS Bank Review 2026 – Pros & Cons

Is the giant worth it? Read our 2026 review of UBS. We analyze the fees and services of Switzerland's biggest bank to see if it offers good value.

Dukascopy Bank Review 2026: Pros & cons

Dukascopy Bank is an atypical Swiss bank, with a multi-currency account. Is it an interesting bank account? We find out in this detailed review.

Interview of Victor Cianni CIO of Alpian

Interview of Victor Cianni, CIO of Alpian. He answers my questions about how Alpian invests and what we can learn from it.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

I have accounts with Zak, N26, Revolut, Bunq, Monzo,… and I tried to open an account with Neon.

The app states it will be opened in 1-2 days. The next day you receive an email saying it will take another week…

I’m not impressed so far: the look and feel suggests you’ll get a product like N26, but they fail upfront with a really slow opening process, while – funny enough – they use the same IDcheck provider as N26.

Also reading that you don’t get instant notification is another issue: this is what iPhone banks are good at.

Zak, so far looks much better

Hi Philippe,

Thanks a lot for sharing your review :)

It’s true that it takes some time to get fully opened. It’s a bit disappointing indeed for a digital bank.

But if I remember correctly, it’s the same with Zak. You can use the app directly, but most features will have to wait until you receive the letter in the mail, no?

Thanks for stopping by!

You said its free for for transactions and withdrawals abroad, then you say you have to pay 2 CHF?

is it free or do you have to pay for withdrawals abroad??

Hi Kei,

Only transactions abroad are free, not withdrawal. For withdrawals abroad, you will pay a 1.5% fee.

Thanks for stopping by!

Hello!

What do you mean is not good for monthly payments income? If i give it to my job for my salary, do i need to pay fees? I wanna leave ubs and was looking to use neon

Hi Daniel,

Neon will be fine for monthly payment incomes. You will not pay fees for getting your salary into Neon.

Where did I say that? If it’s in the part with Revolut, I just meant to say that you need a Swiss bank (like Neon) for your salary, for which Revolut is not great.

Thanks for stopping by!

What about the new pricing as 2020?

You should update and see if its worth it now.

Hi Thierry,

What do you mean by new pricing? Do you mean the removal of the currency exchange fees? If yes, I plan to update that part.

Thanks for stopping by!

zak is way better than neon (except the missing ebill feature)

Do you care to elaborate? Just saying it’s better without any other points adds nothing.

Many of my readers speak only English and Zak is not available in English. For me, that’s enough of a blocker.

ZAK is good and i like the way you can create “spaces” the same as you have on N26. This is awesome. But the fact is, depends how you use it, that Neon can a lot cheaper, especially with their new 2020 fees. Speaking of fees Neon is now side by side with Revolut and N26.

If you want what Neon offers when you use ZAK you need to pay 8.-/month for the plus plan. Can’t wait for Yapeal to be released to the public very soon to see what they offer ;-)

Hi Lemon,

Thanks for sharing your point of view on Zak, this is very interesting!

I am not a fan of Zak plus either. I will take a look a Yapeal, it looks interesting but it really lacks details so far.

Thanks for stopping by!

Thanks to your blog I learned about Neon! I wanted to open an account but unfortunately they currently only offer accounts for users based and taxable exclusively in Switzerland (Americans living here at not eligible).

Hi Ellie,

Sorry to hear that, I didn’t think about that. It’s more and more difficult to get a bank account in Switzerland if you are not Swiss. I know several expats that had to close their bank accounts in some banks.

Hopefully, this will change in the future and you will be able to get a good bank.

Thanks for stopping by!

Hello im from Philippines living in Switzerland and able to get my Neon account.😁

Cool, that’s good to hear!

Hello,

I think you forgot to mention the fact that you can use the Sonect App together with your neon-free bank account and this way you can withdraw money for free as many times as you want. There is a withdraw maximum limit but you no longer have the twice per month limitation that you have with the card.

Hi Tiago,

Actually, I had no idea this app existed! This looks really interesting, I didn’t know this was a think. There are not many places where I can withdraw cash with Sonect around me, but this can become bigger.

Are you using Sonect yourself?

Thanks for sharing!

I’m looking for a new Swiss bank and Neon “looks” attractive – but 2 issues for me are: No ApplyPay (yet) and slow updates on transactions – on their own web site is says, they are “trying” to get updates (ie. transactions on your account history/status/statement) down to “2 days” [they are trying for 2! The average is 5-7!]. With Revolut it’s instant – actually “quicker” than instant. I get a Push notification from Revolut, BEFORE the SSB app shows me the QR code for the ticket I just paid for. To me – this is the new wave of banking. So far, Neon just looks like a slick (but slow) wrapper on an incumbent mortar bank. Nothing new but some marketing and design. I know they are working on all the extras – but as yet, they still have a long way to go.

Hi MountainAsh,

I may ask a dumb question but here it is: what is applypay? I never heard of that.

I did not know about this limitation. For me, it is not really an issue since I only do my bills once a month and I almost never use my debit card to pay for my purchases.

Revolut is impressive for that I agree! It’s instant, as soon as the page is confirming, the confirmation pops on Revolut before the page finishes :) It’s quite cool.

I honestly think this is not a big deal for Neon since most Swiss banks are like this. It is much faster for me to make a transfer from Revolut than from my bank account. Swiss banks are slow, and slow to evolve. It’s just the way it is :)

Swiss people don’t like change (I am one of them)!

Thanks for stopping by!

“ApplyPay” – is a typo of “ApplePay” (I’m pretty sure you know what that is – Apple’s contactless payment wallet (like Google/Samsung Pay), that Swiss banks are adverse to including in their products (but that’s slowly changing).

Every “neo” bank I’ve looked at includes ApplePay and all the other “x”Pay providers – but Neon says in their FAQs (as at 23 Jul 2019):

How do I use Apple/Google Pay with neon?

We’re not quite ready for that yet, but we’re working hard on making it possible soon, because we believe in being digital.

Haha, I didn’t even think of ApplePay :(

Yes, I know what it is. But I never used it. I know that Swiss banks are fighting against it and against Google Pay. That’s why they are trying to push Twint as much as possible.

If you rely on this, I guess, you will have to wait for a while before you could switch.

Not true – all shops that allow “tap to pay” (Paypass) also allow mobile phone NFC payments (ApplePay/GooglePay). One Swiss bank of interest to me is Cler with their “neo” offering called “Zak”. They support “device”Pay, have an app, 0 account keeping and join fees. They seem to have what Neon has but with a real bank directly connected (with branches and ATMs] – I’ve also seen referral codes offering 100 CHF starter bonus – which is very decent.

Another one to look out for in this space is called Yapeal from Zurich, but it hasn’t launched to the public yet.

I’m in the market for a Swiss account now which is why I’m looking. I’m very surprised that a country known for its banking (and insurance) is so far behind the rest of the world now – and they’ve lost that lustre of anonymity, have lots of fees, next to 0 interest on my money and old-skool technology. What went wrong?

Hi MoutainAsh,

Zak is also a good option. My biggest issue with them is that they do not offer an English version of their application. But that is not a big deal for many people. I still prefer Neon for their openness and their philosophy. But that’s subjective.

I didn’t know about Yapeal, I will check it out.

Yeah, the offer in Switzerland is pretty bad. I think it was always only good for rich people. It has never been really good for common people like us. I do not know what went wrong. But the Swiss bonds are negative, so the banks are following this movement. 20 years ago Swiss bonds were really good and banks were offering obligations at more than 6%. Today, everything is at 0%.

Thanks for stopping by!

Nice Post!

Does Neon let you get your bank statements in a .csv (Import to YNAB)?

Hi Thomas,

To be honest, I do not know for sure. I have never seen this feature mentioned anywhere. I would be surprised if they had such a feature already.

If this is important for you, I would ask them directly either on their site or on Twitter.

Thanks for stopping by!

Nice post – hoping to move to Switzerland next year so will make a note of both banks :)

Hi Dird,

Glad to be of help!

Let me know if you got any question once you are moving ;)

Thanks for stopping by!