Welches ist der beste Schweizer Broker auf 2026?

| Aktualisiert: |

(Offenlegung: Einige der unten aufgeführten Links können Affiliate-Links sein)

Um am Aktienmarkt zu investieren, benötigen Sie ein Maklerkonto. Zahlreiche Schweizer Investoren fühlen sich ausschließlich mit einem Broker aus der Schweiz oder zumindest einem Broker mit einer Niederlassung in der Schweiz wohl.

Wir müssen also diese Schweizer Broker vergleichen und sehen, welcher für einen Schweizer Anleger am besten geeignet ist, um in den Aktienmarkt zu investieren.

In diesem Artikel vergleiche ich sieben Schweizer Broker in verschiedenen Szenarien und sehe die besten (die billigsten!).

Was macht den besten Schweizer Broker aus?

Die Schweizer Makler sind sich sehr ähnlich. Sie sind alle ähnlich geregelt und haben meist die gleichen Merkmale. Das Wichtigste bei der Wahl des besten Schweizer Brokers ist der Preis!

Manche werden argumentieren, dass wir uns ihre Instrumente und Berichtsmöglichkeiten ansehen müssen. Für die meisten Anleger ist dies jedoch kein gutes Kriterium. Als passiver Anleger müssen Sie in der Lage sein, Anteile von ETFs zu kaufen. Das war’s.

Es spielt keine Rolle, wie glänzend Ihre Vermögensgrafiken sind oder wie viele mögliche Algorithmen Sie für den aktiven Handel verwenden können. Es geht darum, den Preis, den Sie für Ihre Transaktionen zahlen müssen, so gering wie möglich zu halten.

Ich verbringe weniger als 10 Minuten im Monat mit meinem Broker-Konto, egal wie schön oder einfach es ist. Ich möchte die börsengehandelten Fonds meines Portfolios zu geringen Kosten kaufen können, und ich möchte, dass mein Geld sicher ist.

Ein weiterer wichtiger Punkt ist, dass der Broker Ihnen Zugang zu den von uns benötigten Börsenplätzen verschafft. Im Falle eines Schweizer Brokers benötigen wir zumindest einen Zugang zur Schweizer Börse. Wir brauchen auch Zugang zu den großen europäischen Börsen. Idealerweise wollen wir auch Zugang zu US-amerikanischen ETFs haben. Leider bieten nicht mehr alle Schweizer Broker diesen Zugang an.

Auch ohne US-ETFs wäre es gut, Zugang zu den großen US-Börsen zu haben. Obwohl die meisten Menschen passiv investieren, wollen viele Anleger dennoch Zugang zu amerikanischen Unternehmen haben.

Folglich vergleiche ich einige Schweizer Broker in verschiedenen Szenarien. Und für jedes Szenario sehen wir, welches das günstigste ist. Dieser Artikel soll keine Bewertung dieser Makler sein. Allerdings habe ich über die meisten dieser Broker Bewertungen geschrieben.

Einige Schweizer Makler

Ich habe für diesen Vergleich mehrere Schweizer Broker ausgewählt:

- Swissquote, eine Online-Bank. Für weitere Informationen können Sie meinen vollständigen Swissquote Test lesen.

- PostFinance, die Schweizerische Postbank. Mein ausführlicher Bericht über PostFinance E-Trading ist ebenfalls verfügbar.

- Saxo Bank Schweiz ist ein Schweizer Online-Broker. Meine Bewertung der Saxo Bank ist ebenfalls verfügbar.

- Cornèrtrader, ein Online-Broker. Ich habe eine vollständige Cornèrtrader Bewertung für weitere Informationen.

- Migros Bank, die Bank von Migros.

- Yuh, ein Online-Broker im Besitz von Swissquote, ist für Anfänger gemacht. Ich habe auch eine vollständige Rezension von Yuh.

- Neon Invest, der Broker der digitalen Bank Neon. Sie können meine vollständige Rezension von Neon Invest lesen.

Das sind Broker, die in der Schweiz von vielen Menschen genutzt werden. Und sie sind die günstigsten Makler, die ich gefunden habe.

Cornèrtrader hat mehrere Kontostufen: Energie, Opportunität, Solidität und Beständigkeit. Die hohen Stufen erfordern jedoch erhebliche Beträge. Ich werde mich also auf die Konsistenz konzentrieren, die Standardstufe.

Saxo hat keine Mindesteinzahlungsanforderung für sein Standardkonto, Saxo Classic. Saxo bietet auch verschiedene Kontotypen an, die von der anfänglichen Finanzierung abhängen. Ab 250.000 CHF bekommst du niedrigere Preise mit dem Platinum-Konto. In diesem Artikel werde ich davon ausgehen, dass wir das Standardkonto, Saxo Classic, nutzen.

Bei all diesen Brokern haben Sie Zugang zu vielen Aktien und ETFs. Da Sie bei allen Schweizer Maklern die Stempelsteuer zahlen müssen, lassen wir sie in unseren Vergleichen außer Acht, da sie ohnehin gleich hoch wäre.

Bei diesem Vergleich lasse ich die Dividenden außer Acht. In einigen Fällen können Dividenden sogar mit einer zusätzlichen Gebühr verbunden sein. Wenn Sie beispielsweise bei Neon eine Dividende in einer Fremdwährung erhalten, müssen Sie eine Währungsumrechnungsgebühr bezahlen. Diese Dividenden hängen jedoch in hohem Maße davon ab, welche Aktien und ETFs Sie auswählen, und sind daher zu variabel, um sie in diesen Vergleich einzubeziehen.

Ich beginne mit einem Vergleich der individuellen Gebühren der einzelnen Broker. Dann werde ich einige Szenarien durchspielen, um zu sehen, was am besten ist.

Depotgebühren von Schweizer Brokern

Zunächst betrachten wir die Depotgebühren dieser Makler.

Eine Verwahrungsgebühr zahlen Sie nur, um Ihr Konto offen zu halten. Die Verwahrungsgebühr wird häufig als Prozentsatz des Wertes Ihres Portfolios ausgedrückt. Darüber hinaus weisen diese Gebühren häufig ein Minimum und gelegentlich auch ein Maximum auf.

Die Verwahrungsgebühr ist von Bedeutung, weil Sie sie zahlen müssen, wenn Sie ein Konto haben. Wenn Sie planen, sich mit Ihrem Portfolio zur Ruhe zu setzen, erschwert eine hohe Verwahrungsgebühr die Aufbau- und Entnahmephase.

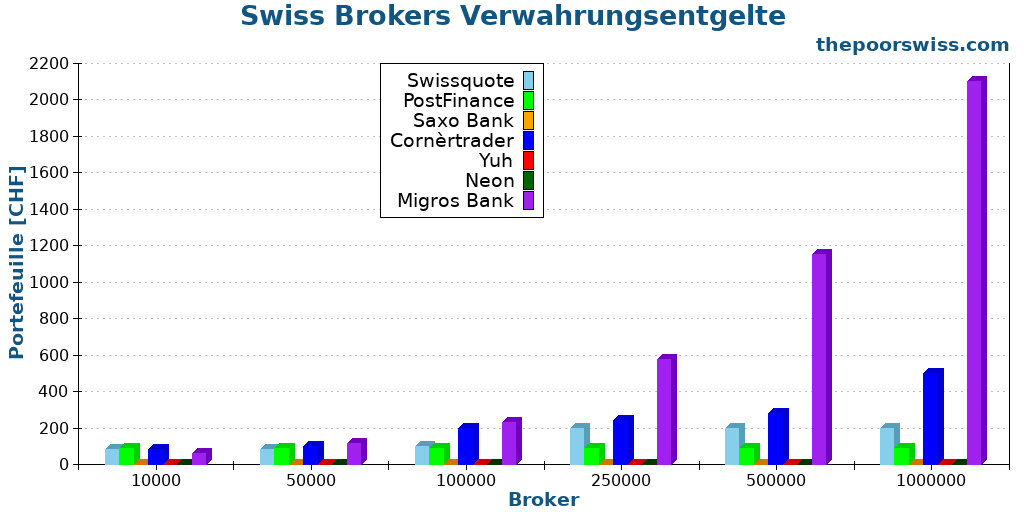

Hier sind die Depotgebühren unserer sieben Makler:

- Swissquote erhebt eine vierteljährliche Gebühr zwischen 20 CHF und 50 CHF, abhängig vom Vermögen. Für ein Vermögen von über einer Million CHF gibt es zusätzlich 0,03% pro Jahr.

- PostFinance erhebt eine Verwahrungsgebühr von 90 CHF pro Jahr. Die Nutzer können diesen Betrag jedoch als Handelsguthaben verwenden, was sowohl eine Inaktivitätsgebühr als auch eine Verwahrungsgebühr darstellt.

- Saxo Bank erhebt keine Depotgebühren.

- Cornèrtrader erhebt vierteljährliche Depotgebühren, die sich nach dem Betrag auf dem Konto richten.

- Die Migros erhebt eine Depotgebühr von 0,23 % unter 750.000, 0,21 % bis 1,5 Mio. und 0,19 % darüber hinaus, bei einem jährlichen Mindestbetrag von 50 CHF.

- Sie haben keine Sorgerechtsgebühren.

- Neon hat keine Verwahrungsgebühren.

Hier sind die Depotgebühren, die Sie bei diesen Brokern zahlen würden:

Aus diesem Diagramm sollte die Schlussfolgerung ziemlich offensichtlich sein. Die Migros Bank scheinen für einen Schweizer Investor gut geeignet zu sein. Um ein Portefeuille von einer Million CHF bei der Migros Bank zu verwalten, würden Sie 2100 CHF pro Jahr bezahlen! Das ist schlecht.

Im Vergleich dazu sind alle anderen Makler in dieser Hinsicht ziemlich gut. Zur besseren Veranschaulichung sehen Sie hier die gleiche Grafik ohne Migros Bank:

Die besten Broker sind Saxo, Yuh und Neon, da sie keine Depotgebühren erheben. Cornèrtrader ist der teuerste Broker, weil er das höchste Maximum hat. Aber für mich sehen sie alle akzeptabel aus.

Sie sollten sich nicht zu viele Gedanken über eine Depotgebühr von 200 CHF für große Portfolios machen. Andererseits ist es langfristig immer noch besser, das Geld für sich selbst zu behalten.

Die 0,05 % Gebühr von Cornèrtrader auf große Portfolios (mehr als eine Million) kann jedoch einen erheblichen Unterschied machen, wenn Sie sie während des Ruhestands zahlen müssen. Dies dürfte jedoch nur für Personen von Bedeutung sein, die sich in der Schweiz vorzeitig zur Ruhe setzen wollen.

Gebühr für Inaktivität

Die zweite Gebühr, die wir uns ansehen müssen, ist die Inaktivitätsgebühr.

Einige Broker erheben eine Gebühr, wenn Sie während eines bestimmten Zeitraums keine Aktionen auf Ihrem Konto vornehmen. Sie kommt einer Verwahrungsgebühr sehr nahe, wird aber nur erhoben, wenn Sie Ihr Konto nicht nutzen.

Diese Gebühr ist nicht so wichtig wie die Verwahrungsgebühr, da Sie sie in der Ansparphase nicht zahlen müssen. Dennoch ist sie unerlässlich, wenn Sie planen, sich mit Ihrem Portfolio zur Ruhe zu setzen, da Sie sie während Ihres gesamten Ruhestands zahlen werden.

Ab Oktober 2024 hat keiner der sieben Broker eine Inaktivitätsgebühr. In der Vergangenheit hatten einige dieser Broker Inaktivitätsgebühren, die aber im Laufe der Zeit aufgehoben wurden.

Kaufen Sie Anteile eines Schweizer ETF bei einem Schweizer Broker

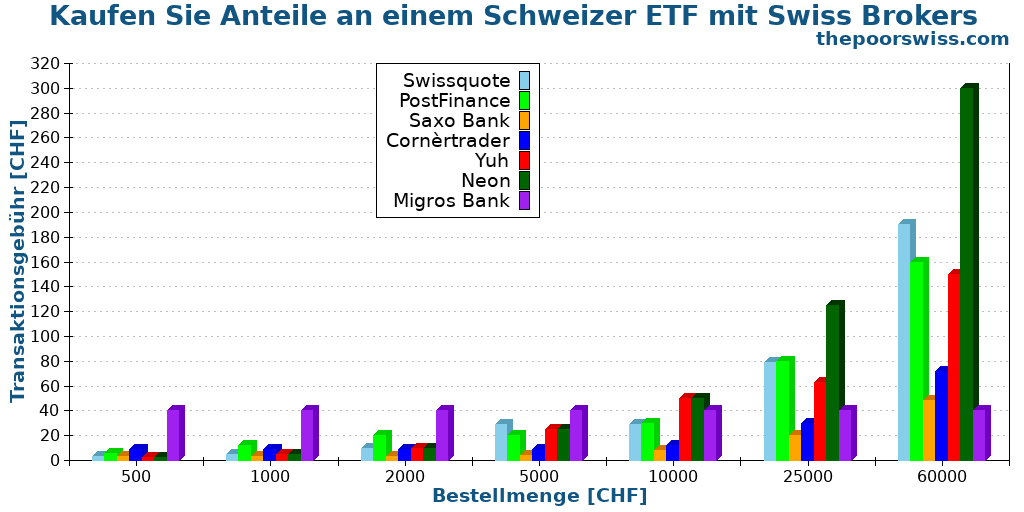

Die nächste Gebühr, die wir untersuchen werden, ist die Gebühr für den Kauf von Anteilen an einem Schweizer ETF. Ein Schweizer Anleger tätigt wahrscheinlich mehrere solcher Transaktionen pro Jahr.

Hier finden Sie die Gebühren für ETFs an der Schweizer Börse:

- Swissquote: Von 3 bis 190 CHF

- PostFinance: Von 15 CHF bis 350 CHF je nach Auftragsgrösse

- Saxo Bank: 0,08% bei einem Mindestbetrag von 3 CHF

- Cornèrtrader: 0,12% mit einem Mindestbetrag von 9 CHF

- Migros Bank: 40 CHF

- Yuh: 0,50 % mit einem Minimum von 1 CHF (0,35 % ab 10’000 CHF und 0,25 % ab 20’000 CHF)

- Neon: 0.50% mit einem Minimum von 1 CHF

Hier finden Sie die Gebühren für einen Kauf eines Schweizer ETFs mit unterschiedlichen Ordergrößen:

Saxo, Yuh und Neon sind die günstigsten Broker für kleine Transaktionen, während Swissquote der günstigste Broker für große Transaktionen ist. Saxo, Neon und Yuh können deutlich günstiger sein als die anderen Broker.

Die anderen sind relativ vergleichbar. Die Migros Bank ist für Transaktionen bis zu 25.000 CHF recht teuer. Danach wird es relativ gut. PostFinance ist nicht schlecht für kleine Betriebe, aber ziemlich schlecht für grosse Betriebe. Es ist auch erwähnenswert, dass Yuh und Neon schlecht für große Operationen sind, da sie kein Maximum haben.

Kaufen Sie Anteile an europäischen ETFs bei einem Schweizer Broker

Wir können die gleiche Übung mit europäischen ETFs durchführen.

Ein Schweizer Anleger, der global diversifizieren will, muss in europäische ETFs investieren. An der Europäischen Börse gibt es viel mehr ETFs als an der Schweizer Börse.

In diesem Beispiel nehme ich die Euronext Paris als Beispiel. Die Gebühren einiger Makler unterscheiden sich geringfügig, je nachdem, welche europäische Börse genutzt wird.

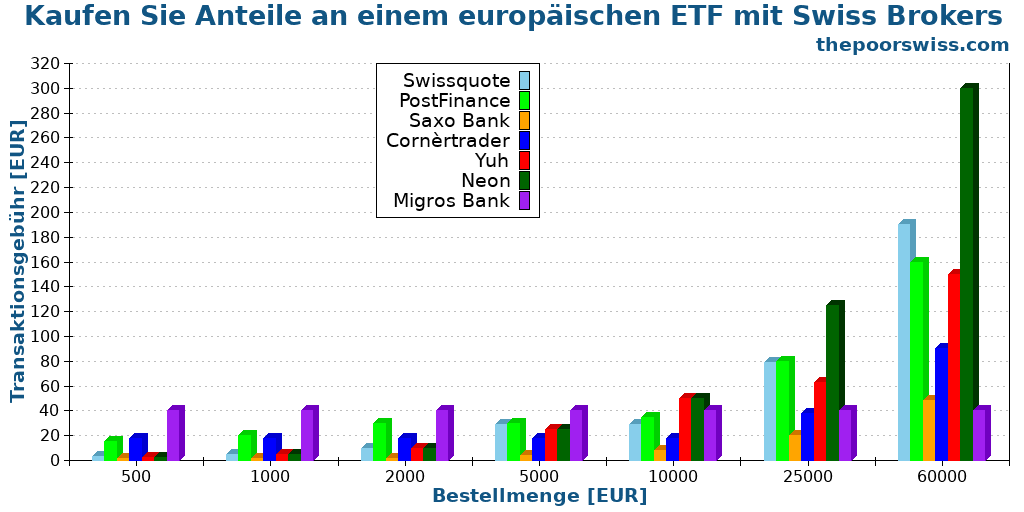

Hier finden Sie die Gebühren für ETFs an der Euronext Stock Exchange:

- Swissquote: Von 3 EUR bis 190 EUR je nach Auftragsvolumen

- PostFinance: Von 25 EUR bis 350 EUR je nach Auftragsvolumen

- Saxo Bank: 0,08% bei einem Mindestbetrag von 2 EUR

- Cornèrtrader: 0,15% bei einem Mindestbetrag von 18 EUR

- Migros Bank: 40 EUR

- Yuh: 0,50 % mit einem Minimum von 1 CHF (0,35 % ab 10’000 CHF und 0,25 % ab 20’000 CHF)

- Neon: 0,50% (ETFs auf BX Swiss) mit einem Minimum von 1 CHF

Hier sind die Gebühren für einen Kaufvorgang eines europäischen ETFs mit verschiedenen Auftragsgrößen:

Diese Ergebnisse sind sehr interessant. Für kleine Betriebe (unter 2000 EUR) sind Saxo, Yuh und Neon am günstigsten, mit einer guten Marge. Bei großen Operationen ist Saxo dann deutlich besser als die anderen. Mit einem Mindestbetrag von nur 2 EUR und einer niedrigen prozentualen Gebühr ist die Saxo Bank für den Handel mit europäischen ETFs recht interessant.

Alle anderen sind in diesem Fall teurer. Nach der Saxo Bank ist der zweitgünstigste Schweizer Broker Cornèrtrader mit seinem Capital-Konto. Schließlich werden Yuh und Neon schlecht für große Operationen.

Aktien von US-Unternehmen über einen Schweizer Broker kaufen

Die letzte Gebühr, die wir betrachten wollen, ist die Gebühr für den Kauf von Aktien amerikanischer Unternehmen.

Auch wenn es sich hierbei nicht um passives Investieren handelt, ist es doch interessant, weil viele passive Anleger immer noch Aktien von Unternehmen kaufen. Im Allgemeinen kaufen sie Aktien von amerikanischen Unternehmen. Dies ist die gleiche Gebühr für Makler, die den Kauf von US-amerikanischen ETFs ermöglichen.

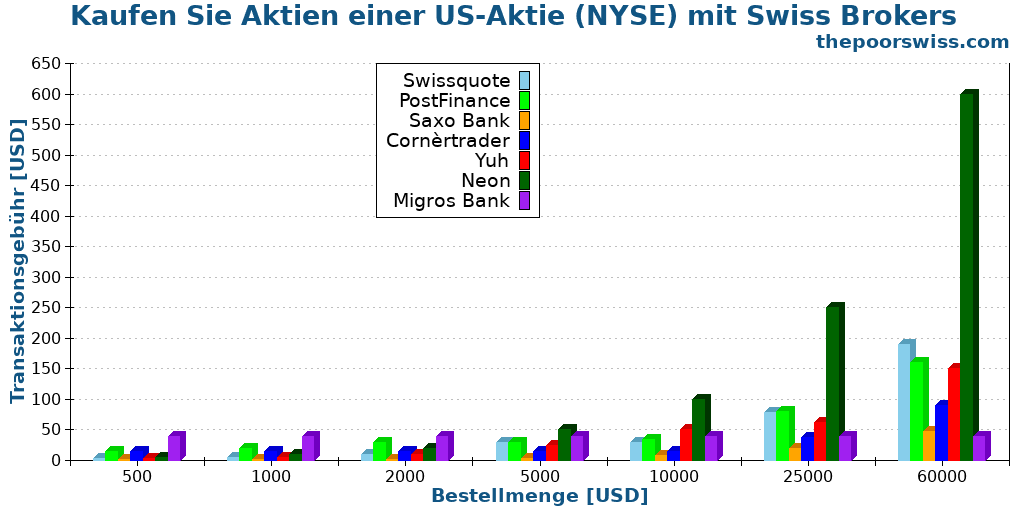

Hier finden Sie die Gebühren für Aktien an der NYSE:

- Swissquote: Von 3 USD bis 190 USD je nach Auftragsvolumen

- PostFinance: Von 25 USD bis 350 USD je nach Auftragsgrösse

- Saxo Bank: 0,08% mit einem Mindestbetrag von 1 USD

- Cornèrtrader: 0,15% bei einem Mindestbetrag von 15 USD

- Migros Bank: 40 USD

- Yuh: 0,50 % mit einem Minimum von 1 CHF (0,35 % ab 10’000 CHF und 0,25 % ab 20’000 CHF)

- Neon: 1,0% (auf BX Swiss) mit einem Mindestbetrag von 1 CHF

Hier sind die Gebühren für einen Kaufvorgang einer US-Aktie mit verschiedenen Auftragsgrößen:

Für alle Transaktionen ist Saxo Bank der günstigste Broker. Yuh, Saxo und Cornèrtrader haben geringe Mindestbeträge und sind damit deutlich günstiger als die anderen.

Swissquote und PostFinance sind für Grossbetriebe in dieser Situation ziemlich schlecht. Und auch Yuh und Neon sind schlecht für große Betriebe.

Für diese drei Vorgänge können wir einige Schlussfolgerungen ziehen:

- Saxo ist ideal für alle Transaktionen

- Swissquote ist im Durchschnitt gut

Gebühren für den Währungsumtausch

Bevor wir uns den verschiedenen Szenarien zuwenden, müssen wir die Umtauschgebühren berücksichtigen. Sie müssen Ihren CHF in EUR konvertieren, wenn Sie einen ETF in EUR kaufen möchten.

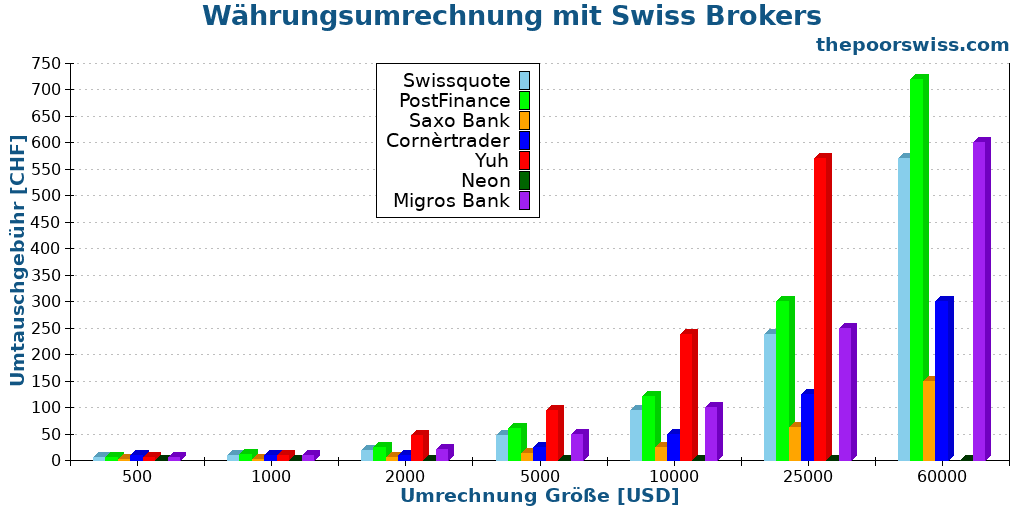

Hier sind die Währungsumrechnungsgebühren dieser sieben Broker:

- Swissquote: 0.95%

- PostFinance: 1,20%

- Saxo Bank: 0.25%

- Cornèrtrader: 0,50% bei einem Mindestbetrag von 10 CHF

- Migros Bank: 1%

- Yuh: 0.95%

- Neon: 0% (Handeln Sie alles in CHF bei BX Swiss)

Diese Gebühren sind für CHF in USD und CHF in EUR identisch. Wenn Sie mehrere kleinere Währungen verwenden, müssen Sie möglicherweise höhere Gebühren zahlen. Aber diese Gebühren sind bereits erheblich!

Hier sind die Gebühren für eine Umrechnung von CHF in USD für verschiedene Bestellmengen:

Neon hat einen erheblichen Vorteil, wenn Sie die Aktie an der Schweizer Börse BX handeln können. Wenn Sie es nicht auf BX Swiss handeln können, müssen Sie ein Äquivalent finden oder einen anderen Broker verwenden.

Bei anderen Brokern: Saxo ist viel billiger als die anderen, und alle anderen sind viel teurer. Selbst bei einem Mindestbetrag von 10 CHF macht die Gebühr von 0,25% im Vergleich zu den durchschnittlichen 1% der anderen Schweizer Broker Saxo zum einzigen guten Schweizer Broker für Währungsumrechnungen. Auch danach ist der Cornèrtrader preisgünstig. Aber Neon ist besser, wenn Sie Ihre Aktie oder Ihren ETF an der BX Swiss Stock Exchange finden können.

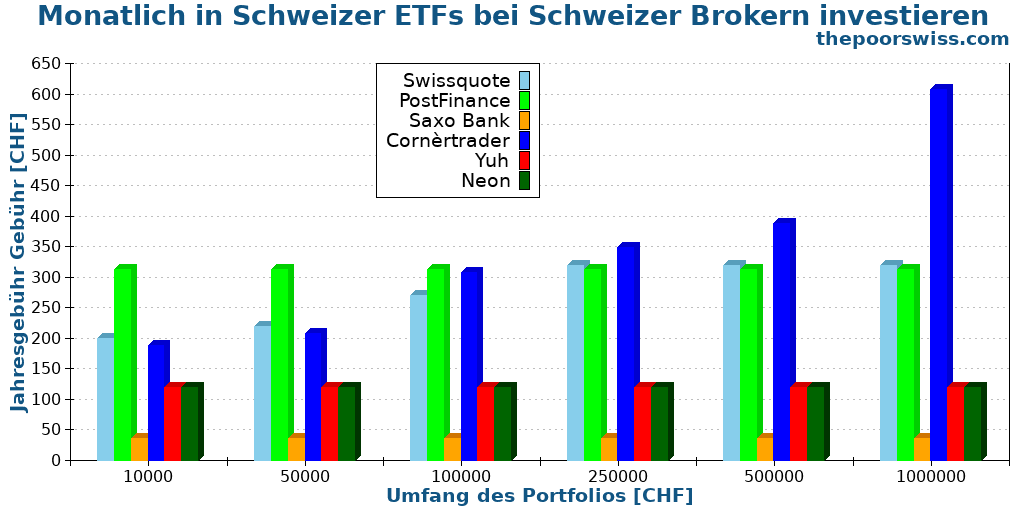

Szenario 1: Ein Schweizer ETF pro Monat

Bis jetzt haben wir nur einen einzigen Vorgang isoliert betrachtet. Aber es ist viel interessanter, alles zusammen zu betrachten. Wir müssen ein Jahr des Handels zusammen mit den Transaktions- und Verwahrungsgebühren betrachten.

Das erste Szenario ist für einen Anleger, der monatlich Anteile eines Schweizer ETF (in CHF) kauft. Viele Schweizer Anleger nutzen nur die Schweizer Börse. Da wir die Verwahrungsgebühr berücksichtigen müssen, müssen wir das Szenario mit verschiedenen Portfoliogrößen durchspielen.

Da sich die Preise je nach Auftragsgröße ändern, müssen wir eine Auftragsgröße wählen. In diesem Szenario kauft der Anleger jeden Monat Aktien im Wert von 2000 CHF. 2000 CHF sind ein guter Durchschnitt für monatliche Investitionen.

Es ist erwähnenswert, dass einige Broker (Saxo, Yuh und Neon) Sparpläne haben, die in diesem Fall die Kosten senken können. Hier gehe ich davon aus, dass du diese Pläne nicht nutzt, aber wenn doch, können die Gebühren für diese drei Broker sogar noch niedriger sein.

Werfen wir also kurzerhand einen Blick auf die Gebühren jedes dieser Makler für ein Jahr in diesem Szenario:

Wir können sehen, dass Schweizer Anleger die Migros Bank völlig ignorieren sollten. Ihre Verwahrungsgebühren sind für jeden ernsthaften Anleger zu hoch. Wir können diese Grafik also noch einmal mit den vernünftigen Maklern sehen:

Es ist nicht überraschend, dass Saxo hervorragend ist, da sie ausgezeichnete Transaktionsgebühren und niedrige Verwahrungsgebühren aufweisen. Auch Neon und Yuh eignen sich hervorragend für große Portfolios (da keine Depotgebühren anfallen). Danach ist Swissquote hervorragend für kleine Portfolios geeignet. Im Durchschnitt ist Cornèrtrader in diesem Fall der schlechteste.

Insgesamt würde ich in diesem Szenario Saxo verwenden. Als zweite Wahl würde ich entweder Neon oder Swissquote verwenden.

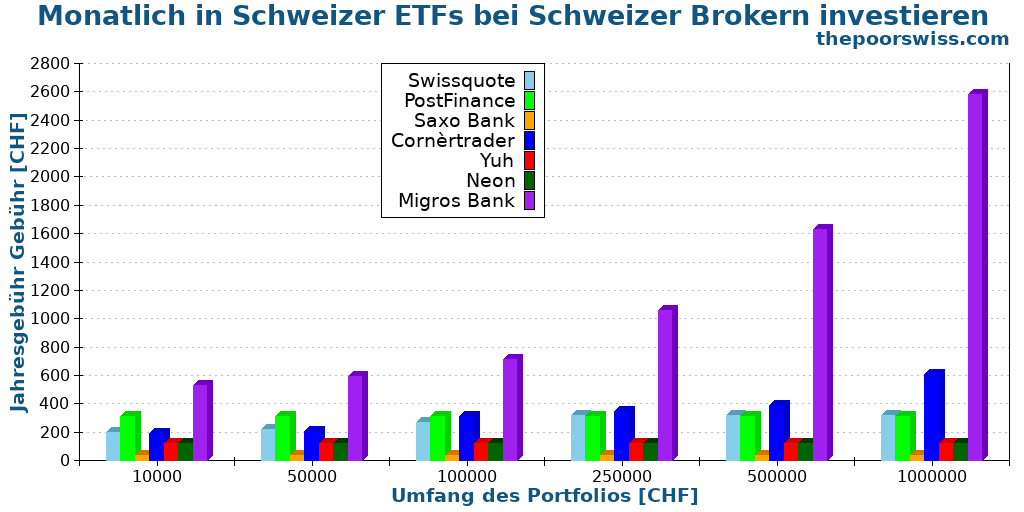

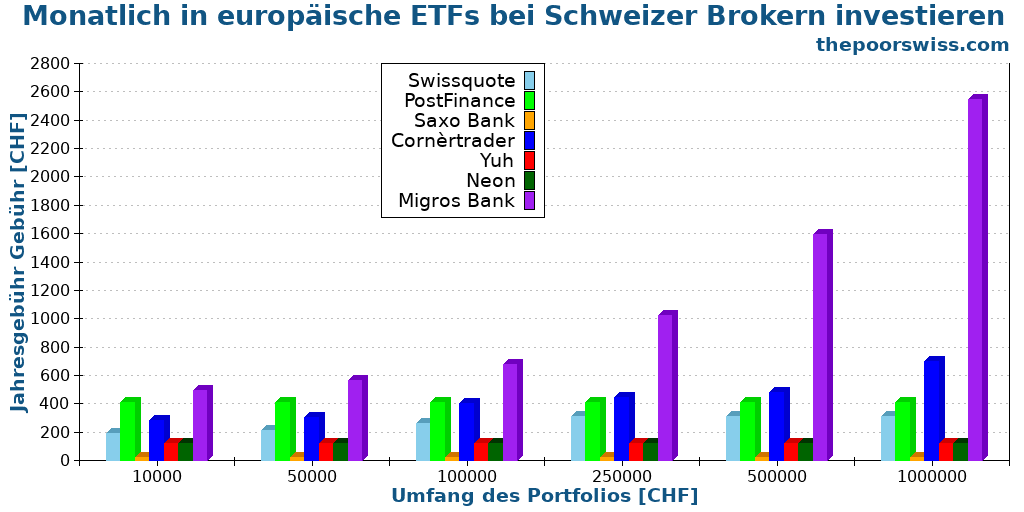

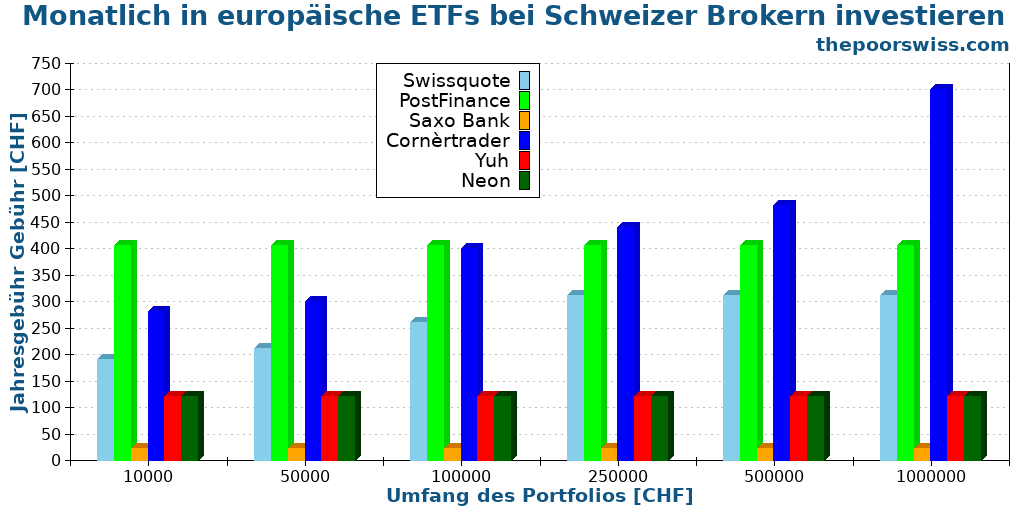

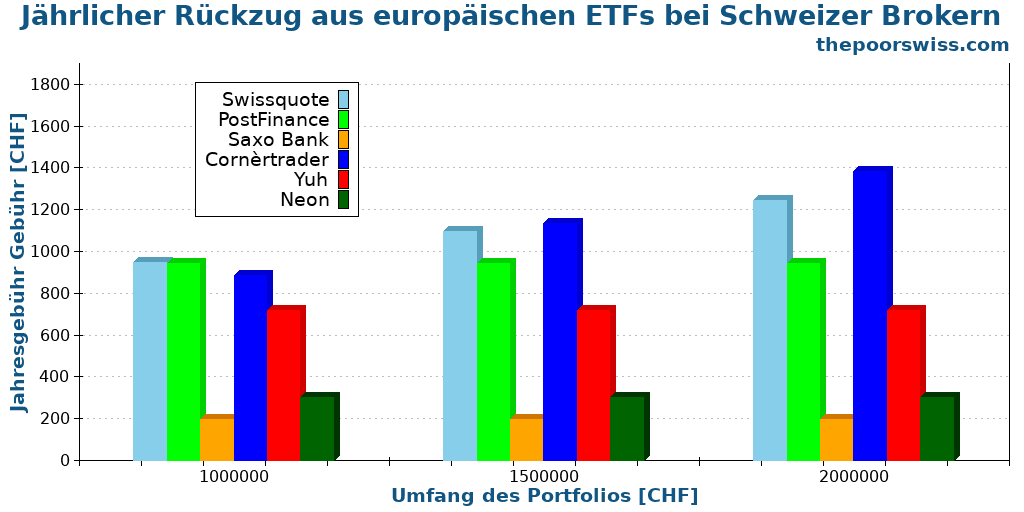

Szenario 2: Ein europäischer ETF pro Monat

Ein interessanteres Szenario wäre es, in ETFs an den europäischen Börsen zu investieren. Auch hier betrachten wir ein ganzes Jahr des Handels.

Für dieses Szenario werden wir eine monatliche Investition von 2000 EUR in europäische ETFs verwenden. Da auch hier Depotgebühren anfallen, werden wir unterschiedliche Portfoliogrößen verwenden.

Wie erwartet, muss der Broker mit schlechten Depotgebühren wieder ignoriert werden. Hier ist das Diagramm also noch einmal ohne diese Angaben:

Wenn Währungsumrechnungsgebühren in das Szenario einbezogen werden, ist ersichtlich, dass die Ergebnisse durchaus unterschiedlich ausfallen und alles kostenintensiver wird. Damit würde ich PostFinance wegen der schlechten Umrechnungsgebühren nicht mehr empfehlen.

Saxo und Neon sind die günstigsten Schweizer Broker. Alle anderen Broker sind viel schlechter. Swissquote, PostFinance und Cornèrtrader sind hier die schlechtesten, und Yuh liegt irgendwo in der Mitte.

In diesem Szenario würde ich persönlich Saxo oder Neon nutzen.

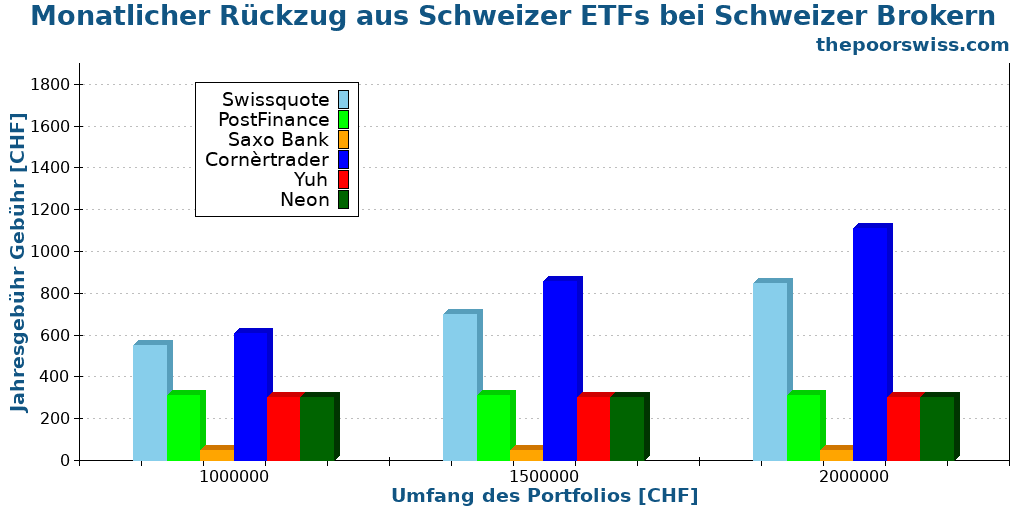

Szenario 3: Einmal pro Jahr abheben

Für unser letztes Szenario nehmen wir etwas anderes.

Die beiden anderen Szenarien würden einen Anleger in der Akkumulationsphase darstellen. Nehmen wir nun ein Szenario, das die Ruhestandsphase darstellt.

Wenn Sie auf der Grundlage Ihres Portfolios in Rente gehen wollen, müssen Sie Aktien verkaufen, um davon leben zu können. In unserem Szenario verkauft der Anleger also für 60’000 CHF pro Jahr, um von seinem Portfolio zu leben. Wir brauchen unterschiedliche Portfoliogrößen, da die Verwahrungsgebühren in diesem Szenario eine Rolle spielen werden.

Wir beginnen mit einem Anleger, der zu Beginn des Jahres für 60’000 CHF einen Schweizer ETF verkauft:

Hier zeigen sich die Auswirkungen der hohen Verwahrungsgebühren. Sie haben kein Einkommen im Ruhestand und könnten Ihrem Makler mehrere tausend Franken pro Jahr geben! Ich würde niemandem empfehlen, mit einem solchen Broker zu investieren! Sie müssen einen Broker finden, bei dem die Depotgebühr ein Maximum hat.

Hier sind die anderen Auswahlmöglichkeiten:

In diesem Szenario ist Saxo der günstigste Broker. Und Cornèrtrader ist aufgrund seiner Depotgebühren am teuersten. Es gibt einen Unterschied von 1000 CHF pro Jahr zwischen dem billigsten und dem teuersten.

Eine monatliche Entnahme hat auch den Vorteil, dass Ihr Geld länger angelegt bleibt. Ich habe Simulationen durchgeführt, und in der Vergangenheit war es besser, häufiger Geld abzuheben.

Wenn das Geld stattdessen jeden Monat abgehoben wird, sind die Ergebnisse immer noch sehr ähnlich:

Die Unterschiede sind hier etwa gleich groß. 100 CHF pro Jahr sind kein großer Unterschied. Dennoch ist Saxo wieder einmal die günstigste Option, gefolgt von PostFinance, Yuh und Neon. Cornèrtrader ist aufgrund seiner höheren Depotgebühr deutlich teurer.

Einige Leute werden argumentieren, dass ein vierteljährlicher Verkauf optimal wäre, um hohe Transaktionsgebühren zu vermeiden. Aber das ist eine sinnlose Optimierung. Es wird nur einen sehr geringen Unterschied machen. Sie sollten entweder einmal im Jahr oder einmal im Monat abheben. Im Idealfall erzielen Sie einmal im Monat eine bessere langfristige Rendite, da Sie das Geld so lange wie möglich auf dem Markt halten. Aber natürlich gibt es noch andere Dinge zu berücksichtigen.

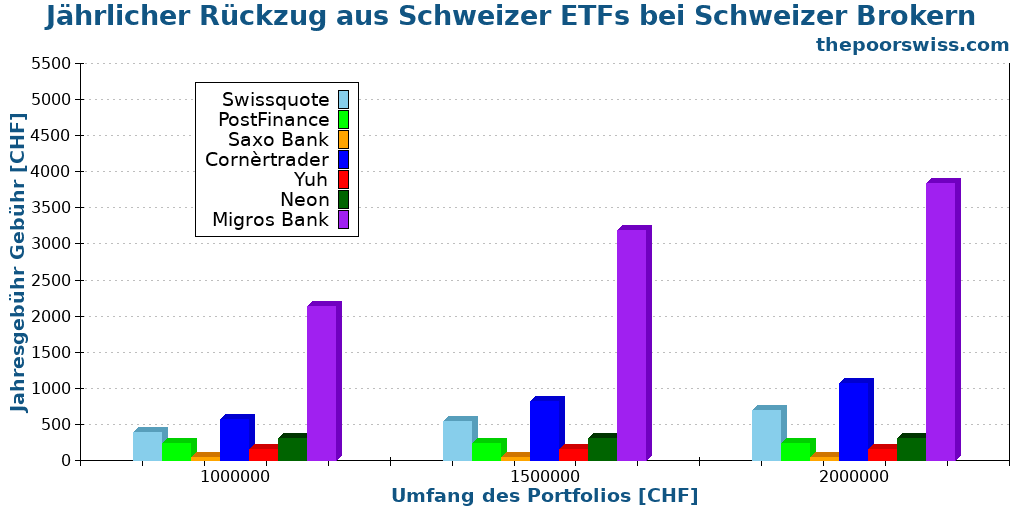

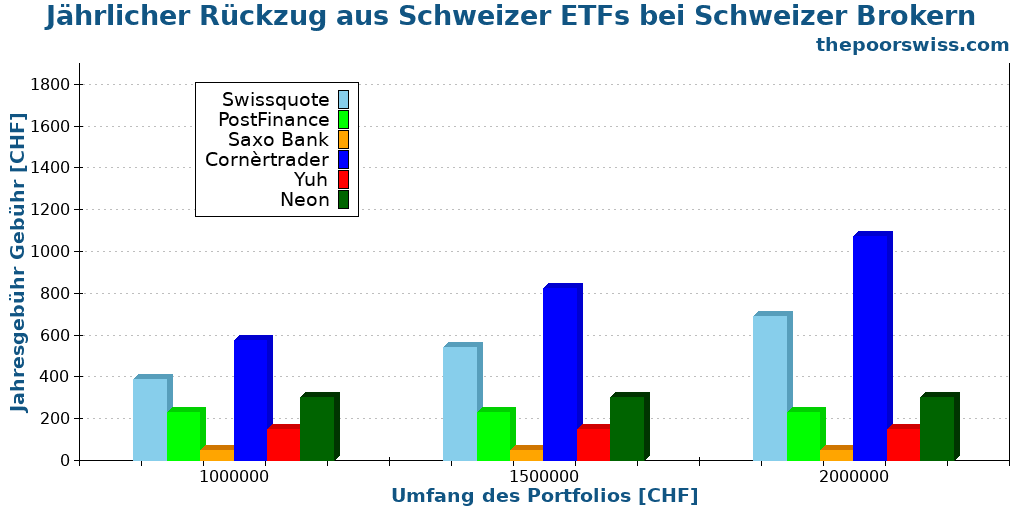

Schliesslich können wir sehen, was passiert, wenn wir ETF-Anteile an der europäischen Börse statt an der Schweizer Börse verkaufen. Hier sind die Ergebnisse mit unseren günstigen Schweizer Brokern:

Diesmal ist der Unterschied aufgrund der Währungsumrechnungsgebühren signifikanter. Saxo ist trotz Währungsumrechnungsgebühren am günstigsten. Neon ist dann die zweitgünstigste Option, da Sie die Währungsumrechnung vermeiden können.

Obwohl Cornèrtrader bei der Umrechnung von Währungen doppelt so günstig ist, ist er im Durchschnitt immer noch der schlechteste, da er Depotgebühren erhebt.

In diesem Szenario würde ich Saxo oder Neon verwenden.

Fazit

Beginnen Sie mit dem Handel bei der Saxo Bank und erhalten Sie 200 CHF an Handelsguthaben.

- Schweizer Broker

Schweizer Makler sind teuer, aber Sie können einige Makler billiger als andere finden, wenn Sie gut suchen. Wenn Sie einen Schweizer Broker möchten, empfehle ich Saxo als den besten Schweizer Broker.

Ich selbst nutze Saxo als meinen Schweizer Broker. Sie haben ausgezeichnete Gebühren und werden Ihnen viel Geld sparen. Zudem bieten sie alle Funktionen, die Sie benötigen.

Neon und Swissquote sind zwei solide Alternativen. Neon eignet sich hervorragend für Anfänger, da die Kosten für kleine Betriebe gering sind. Swissquote ist hervorragend für fortgeschrittene Anleger, mit insgesamt durchschnittlichen Gebühren. Darüber hinaus genießt Swissquote einen guten Ruf und ist gut etabliert. Sie können die meisten Währungsumrechnungsgebühren bei Neon vermeiden, indem Sie über BX Swiss handeln, einem transparenten Dienst.

Eine weitere wichtige Schlussfolgerung aus diesem Artikel ist, dass seriöse Anleger keinen Broker mit einer Verwahrungsgebühr ohne Höchstgrenze nutzen sollten. Das wird schnell zu teuer. Aus diesem Grund würde ich nicht empfehlen, die Migros Bank zu benutzen. Sie sind viel zu teuer und werden Ihre Renditen beeinträchtigen. Und einige Schweizer Broker sind sogar noch teurer als diese beiden. Daher sollten Schweizer Anleger Vorsicht walten lassen.

Wenn Sie bereit sind, einen ausländischen Broker zu nutzen, empfehle ich Ihnen, bei Interactive Brokers zu investieren, denn das ist billiger. Wenn Sie jedoch Angst haben, Ihr Geld außerhalb der Schweiz zu haben, ist es viel besser, einen Schweizer Broker zu benutzen, als gar nicht zu investieren! Da viele meiner Leser mich so oft danach gefragt haben, musste ich diesen Artikel schreiben.

Es ist äußerst faszinierend festzustellen, dass Schweizer Broker im Laufe der Zeit günstiger geworden sind. Mit der Einführung von Neon und Yuh sind die Preise gesunken. Und seit Saxo ihre Gebühren erheblich gesenkt hat, sind sie einem Broker wie IB näher denn je gekommen.

Der Transparenz halber: Interactive Brokers ist mein Hauptbroker und Saxo ist mein Zweitbroker.

Sollten Sie weitere Szenarien wünschen, können Sie mein Broker-Vergleichsinstrument verwenden, um diese exakt auf Ihre Bedürfnisse abzustimmen.

Wenn Sie mehr über die Gewinner erfahren möchten, können Sie deren Bewertungen lesen:

Wenn Sie der Meinung sind, dass Anlagegebühren auf die leichte Schulter genommen werden können, sollten Sie meinen Artikel über Anlagegebühren und ihre Auswirkungen lesen.

Welches ist Ihr bevorzugter Schweizer Broker?

Mehr zum Lesen

Schritt-für-Schritt-Anleitung: So kaufen Sie einen ETF mit Saxo in 2026

Handeln Sie auf Saxo. Eine Schritt-für-Schritt-Anleitung zum Kauf Ihres ersten ETF mit der Saxo Bank, einschließlich Währungsumrechnung, Orderarten und Gebühren.

Yuh Erfahrungen 2026 – Review

Postfinance und Swissquote lancieren eine neue digitale Bank: Yuh. Yuh kombiniert Bankgeschäfte, Investitionen und Kryptowährungen in einem einzigen Service!

eToro Erfahrungen für Schweizer Anleger 2026

eToro ist eine beliebte soziale Handelsplattform. Aber ist das gut für Schweizer Anleger? Wir finden es in diesem ausführlichen Bericht heraus!

Erfahren Sie, wie Sie Ihre Finanzen ganz einfach optimieren und in der Schweiz Tausende sparen können, mit unserem exklusiven E-Book. Entdecken Sie die kostengünstigsten Finanzdienstleistungen, maßgeschneidert für clevere Einwohner und Expats!

Ihren KOSTENLOSEN Schweizer Sparratgeber

Hallo,

Herzlichen Dank für die ausgezeichneten Informationen!

Ich frage mich, warum Swissquote am besten oder gleich gut wie Saxo sein soll, während Saxo *erheblich* billiger ist?

Liebe Grüße

Hi

Swissquote hat den Vorteil, stabiler zu sein. Bis vor Kurzem war Saxo extrem teuer, ist jetzt aber sehr günstig geworden. Und seit Februar gibt es dort keine Depotgebühren mehr (was bald in diesem Artikel aktualisiert wird, sobald ich aus China zurück bin).

Derzeit sind sowohl Saxo, Swissquote als auch Neon sehr gute Optionen, je nach Bedarf. Wenn du die günstigste Variante möchtest, kannst du je nach deinem Anlageprofil Neon oder Saxo wählen. Und wenn du die etablierteste Lösung bevorzugst, ist Swissquote die beste Wahl.

Hallo Baptiste

Vielen Dank für den Artikel und die tollen und bestimmt sehr aufwändigen Vergleichn. Saxo Bank hat gerade ihr Preismodell massiv angepasst und könnte somit eine Konkurenz zu Swissquote werden. Bin gespannt wie es mit schweizer Brokern weiter geht, wir haben da ja schon noch massiven Aufholbedarf was die Preise betrifft.

Liebe Grüsse

Hallo Sunny

Ja, sie haben ihre Gebühren massiv geändert, das ist wirklich beeindruckend. Sie scheinen jetzt sehr wettbewerbsfähig zu sein. Ich plane, meinen Inhalt über SAXO zu aktualisieren, sobald ich Zeit habe und eine richtige Bewertung ihres Dienstes zu schreiben.

Ich war noch vor ein paar Jahren Kunde der Saxo Bank und war sehr zufrieden mit den Kundendienst und die super tech platform. Jetzt das sie ihre Preise angepasst haben, werde ich sicher wieder ein Konto öffnen bei der Saxo.

Danke für den Austausch. Das ist wirklich gut zu wissen! Ich denke, sie haben mit den neuen Preisen gute Arbeit geleistet. Ich hoffe, dass ich nächsten Monat die Zeit haben werde, einen vollständigen Bericht zu veröffentlichen.

Vielen Dank für den informativen Artikel!

Vielen Dank für Ihr Feedback!

Offenbar ist ein Teil des Artikels nicht übersetzt. Ich werde überprüfen müssen, was mit dem Übersetzungs-Plugin passiert ist.

Dear Baptiste

Thank you for this summary, its very helpful.

Swissquote is charging 9 sf per order in ETF on their leader list, including usa etf Vanguard all world.

So did change for usa etfs or im i interpreting it wrongly?

With best regards

Soweit ich weiß, gibt es keine US-amerikanischen börsengehandelten Fonds auf den ETF-Leader-Listen. Es gibt einige ETFs von Vanguard, aber das sind die europäischen ETFs, nicht die US-amerikanischen. Außerdem habe ich in diesem Artikel nicht über US-ETFs gesprochen, weil viele Broker Schweizer nicht zulassen, sie zu kaufen.