What is the best Swiss broker in 2026?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

You need a broker account to invest in the stock market. Many Swiss investors only feel comfortable having a broker from Switzerland, or at least a broker with an office in Switzerland.

So, we need to compare these Swiss brokers and see which is best for a Swiss investor to invest in the stock market.

In this article, I compare seven Swiss brokers in different scenarios and see the best (the cheapest!).

What makes the best Swiss broker?

Swiss brokers are extremely similar. They are all regulated similarly, and most have the same features. What matters most in choosing the best Swiss broker is the price!

Some people will argue that we must look at their tools and reporting capability. However, this is not a good criterion for most investors. For a passive investor, you need to be able to buy shares of ETFs. That is it.

It does not matter how shiny your net worth graphs are or how many possible algorithms you can use for active trading. What matters is minimizing the price you will pay for your transactions.

I spend less than 10 minutes a month on my broker account, no matter how beautiful or easy it is. I want to be able to buy the ETFs from my portfolio at a low cost, and I want my money to be safe.

The other thing that matters is that the broker gives you access to the stock exchanges we need. In the case of a Swiss broker, we need at least access to the Swiss stock exchange. We also need access to the major European Stock Exchanges. Ideally, we want access to U.S. ETFs as well. Unfortunately, not all Swiss brokers still give you this access.

Even without U.S. ETFs, it would be great to have access to the major U.S. stock exchanges. Although passive investing is the way for most people, many investors still want access to American companies.

So, I compare some Swiss brokers over different scenarios. And for each scenario, we see which one is the cheapest. This article is not meant to be a review of these brokers. However, I have written reviews of most of these brokers.

Some Swiss Brokers

I have selected several Swiss brokers for this comparison:

- Swissquote, an online bank. You can read my complete Swissquote review for more information.

- PostFinance, the Swiss Post Bank. My complete review of PostFinance E-trading is also available.

- Saxo Bank Switzerland is a Swiss online broker. My review of Saxo bank is available as well.

- Cornèrtrader, an online broker. I have a complete Cornèrtrader review for more information.

- Migros Bank, the bank from Migros.

- Yuh, an online broker owned by Swissquote, is made for beginners. I also have a full review of Yuh.

- Neon Invest, the broker of the digital bank, Neon. You can read my full review of Neon Invest.

These are brokers that many people are using in Switzerland. And they are the cheapest brokers that I have found.

Cornèrtrader has multiple account tiers: Energy, Opportunity, Solidity and Consistency. However, high tiers require significant amounts. So I will focus on Consistency, the default tier.

Saxo has no minimum funding requirement for its default account, Saxo Classic. Saxo also has several account types depending on the initial funding. Starting at 250,000 CHF, you can get lower prices with the Platinum account. In this article, I will assume we are using the default account, Saxo Classic.

All of these brokers give you access to many stocks and ETFs. You will have to pay the Swiss Stamp Tax Duty with all Swiss brokers, so we will ignore it in our comparisons because it would be the same anyway.

In this comparison, I will ignore dividends. Indeed, in some cases, dividends may incur an extra fee. For instance, if you get a dividend in a foreign currency with Neon, you will have to pay a currency conversion fee. However, these dividends highly depend on which stocks and ETFs you choose, so they are too variable to include in this comparison.

I will start by comparing each broker’s individual fees. Then, I will run through some scenarios to see which is best in more detail.

Custody Fees of Swiss brokers

First, we look at the custody fees of these brokers.

A custody fee is something you pay just to keep your account open. The custody fee is often expressed as a percentage of the value of your portfolio. Furthermore, these fees often have a minimum and sometimes a maximum.

The custody fee is significant because you will pay it if you have an account. If you plan to retire on your portfolio, a large custody fee will make it more difficult during the accumulation and withdrawal phases.

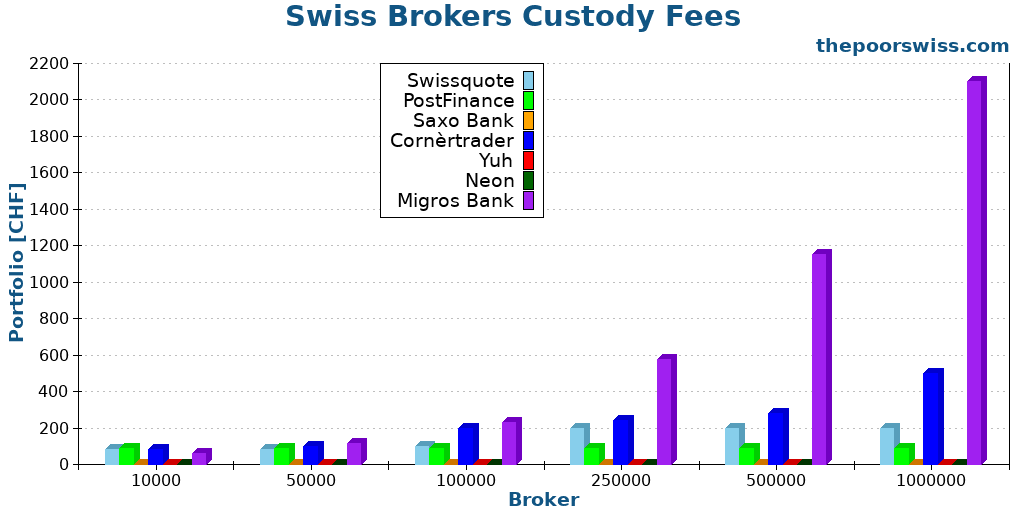

Here are the custody fees of our seven brokers:

- Swissquote has a quarterly fee between 20 CHF and 50 CHF depending on assets. They also have an extra 0.03% per year for assets over a million CHF.

- PostFinance has a 90 CHF per year custody fee. However, users can use this as trading credits, which is both an inactivity fee and a custody fee.

- Saxo Bank has no custody fees.

- Cornèrtrader has quarterly custody fees, based on the amount in the account.

- Migros has a 0.23% custody fee below 750K, 0.21% until 1.5M, and 0.19% after that, and an annual minimum of 50 CHF.

- Yuh has no custody fees.

- Neon has no custody fees.

Here are the custody fees you would pay with these brokers:

From this chart, the conclusion should be pretty obvious. Migros Bank does not look to be a good fit for a Swiss investor. To manage a one million CHF portfolio with Migros Bank, you would pay 2100 CHF per year! This is bad.

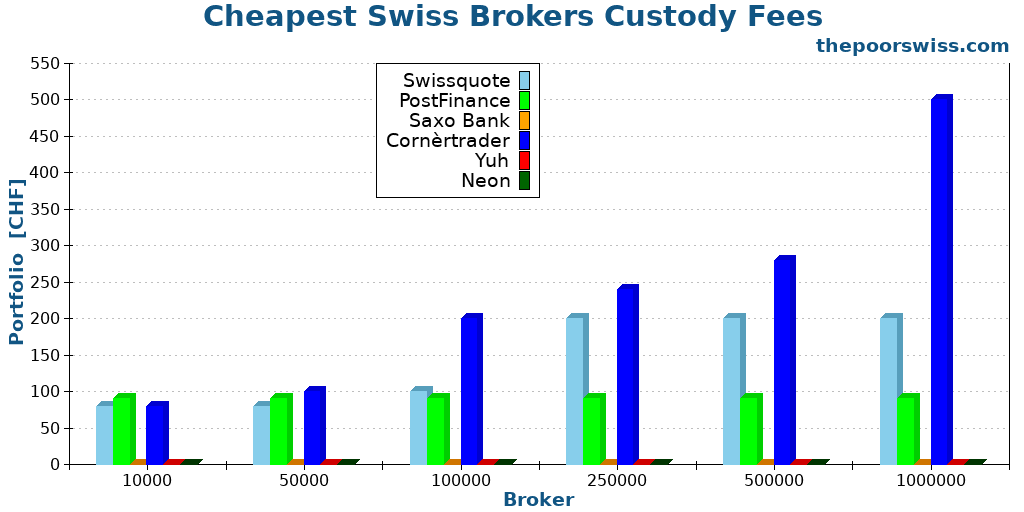

In comparison, all the other brokers are pretty good on that note. To see better, here is the same graph without Migros Bank:

The best brokers are Saxo, Yuh, and Neon since they have no custody fees. Cornèrtrader is the most expensive broker because they have the highest maximum. But to me, they all look acceptable.

You should not worry too much about a 200 CHF custody fee for large portfolios. On the other hand, in the long term, it is still better to keep that money for you.

However, the 0.05% Cornèrtrader fee on large portfolios (more than a million) can make a significant difference if you have to pay it during retirement. However, this will likely only matter for people wanting to retire early in Switzerland.

Inactivity Fee

The second fee we need to look at is the inactivity fee.

Some brokers charge a fee when you do not do any action on your account during a specific period. It is very close to a custody fee, but it is only charged when you do not use your account.

This fee is not as crucial as the custody fee since you will not pay it during the accumulation phase. But it is still essential if you plan to retire on your portfolio because you will pay it during your entire retirement.

As of October 2024, none of the seven brokers have any inactivity fee. In the past, some of these brokers had inactivity fees, but they got waived over time.

Buy shares of Swiss ETF with a Swiss broker

The next fee we will examine is the fee to buy shares of a Swiss ETF. A Swiss investor is likely to make several such transactions per year.

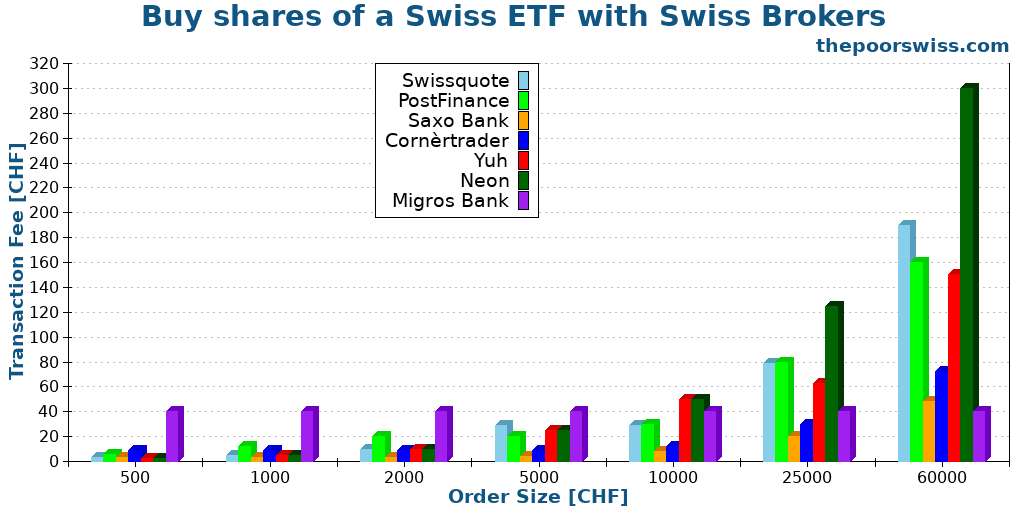

Here are the fees for ETFs on the Swiss Stock Exchange:

- Swissquote: From 3 to 190 CHF

- PostFinance: From 15 CHF to 350 CHF based on the order size

- Saxo Bank: 0.08% with a minimum of 3 CHF

- Cornèrtrader: 0.12% with a minimum of 9 CHF

- Migros Bank: 40 CHF

- Yuh: 0.50% with a minimum of 1 CHF (0.35% above 10,000 CHF and 0.25% above 20,000 CHF)

- Neon: 0.50% with a minimum of 1 CHF

Here are fees for one buy operation of a Swiss ETF with different order sizes:

Saxo, Yuh, and Neon are the most reasonable brokers for small operations, while Swissquote is the most affordable broker for large operations. Saxo, Neon, and Yuh can be significantly cheaper than the other brokers.

The other ones are relatively comparable. Migros Bank is quite expensive for operations up to 25,000 CHF. After this, it is becoming relatively okay. PostFinance is not bad for small operations but pretty bad for large operations. It is also worth mentioning that Yuh and Neon are bad for large operations since they have no maximum.

Buy shares of European ETFs with a Swiss broker

We can do the same exercise with European ETFs.

A Swiss investor who wants to diversify globally must invest in European ETFs. There are much more ETFs on the European Stock Exchange than on the Swiss Stock Exchange.

For this example, I take Euronext Paris as an example. Some brokers’ fees differ slightly based on which European Stock Exchange is being used.

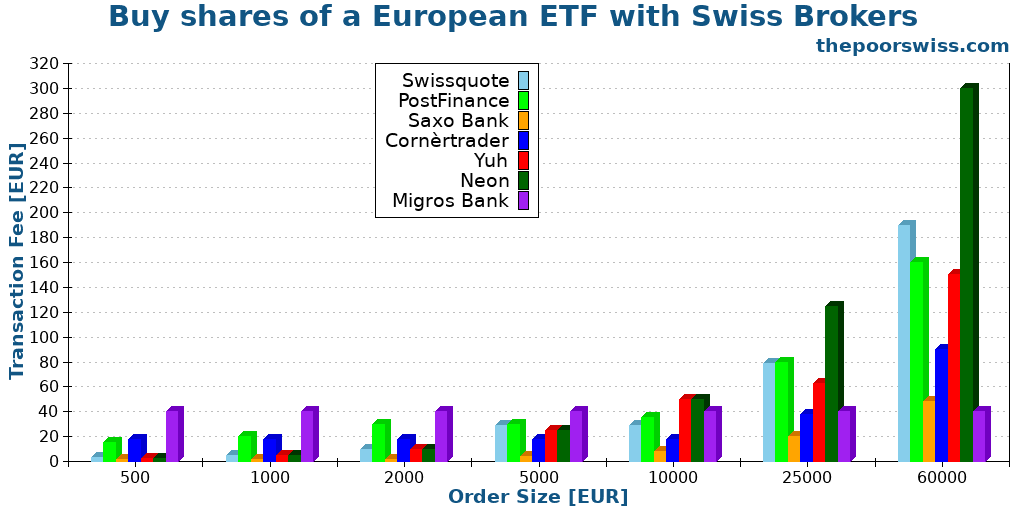

Here are the fees for ETFs on the Euronext Stock Exchange:

- Swissquote: From 3 EUR to 190 EUR based on the order size

- PostFinance: From 25 EUR to 350 EUR based on the order size

- Saxo Bank: 0.08% with a minimum of 2 EUR

- Cornèrtrader: 0.15% with a minimum of 18 EUR

- Migros Bank: 40 EUR

- Yuh: 0.50% with a minimum of 1 CHF (0.35% above 10,000 CHF and 0.25% above 20,000 CHF)

- Neon: 0.50% (ETFs on BX Swiss) with a minimum of 1 CHF

Here are fees for one buy operation of a European ETF with different order sizes:

These results are pretty interesting. For small operations (below 2000 EUR), Saxo, Yuh, and Neon are the cheapest, with a good margin. Then, for large operations, Saxo is significantly better than the others. With a minimum of only 2 EUR and a low percentage fee, Saxo Bank is quite interesting for trading European ETFs.

All the others are more expensive in this case. After Saxo Bank, the second cheapest Swiss broker is Cornèrtrader with its Capital account. Finally, Yuh and Neon become bad for large operations.

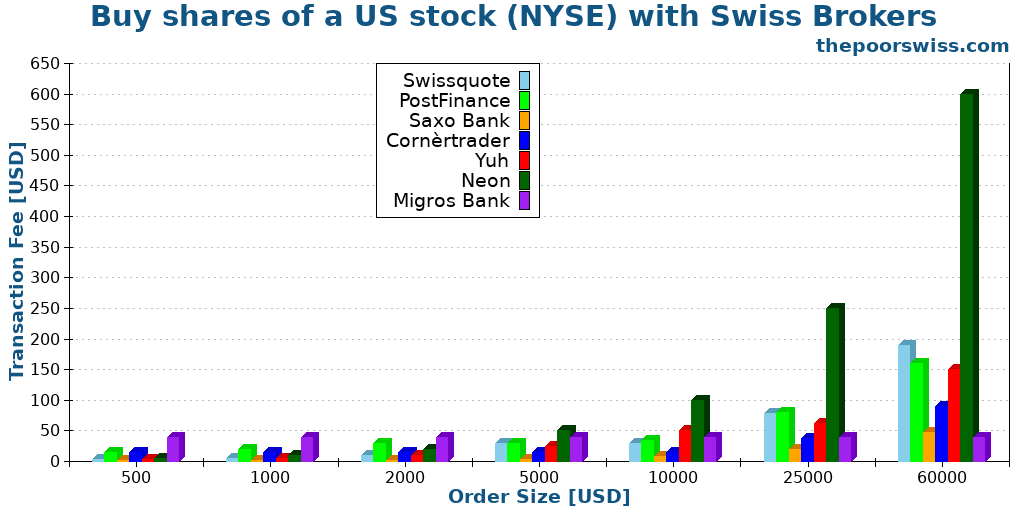

Buy shares of U.S. companies with a Swiss broker

The last fee we will look at is the fee to buy shares of U.S. companies.

Even though this is not passive investing, it is interesting because many passive investors still buy some shares of companies. In general, they buy shares of American companies. This will be the same fee for brokers that allow buying U.S. ETFs.

Here are the fees for stocks on the NYSE:

- Swissquote: From 3 USD to 190 USD based on the order size

- PostFinance: From 25 USD to 350 USD based on the order size

- Saxo Bank: 0.08% with a minimum of 1 USD

- Cornèrtrader: 0.15% with a minimum of 15 USD

- Migros Bank: 40 USD

- Yuh: 0.50% with a minimum of 1 CHF (0.35% above 10,000 CHF and 0.25% above 20,000 CHF)

- Neon: 1.0% (On BX Swiss) with a minimum of 1 CHF

Here are fees for one buy operation of a U.S. stock with different order sizes:

For all operations, Saxo Bank is the cheapest broker. Yuh, Saxo, and Cornèrtrader have small minimums, making them significantly cheaper than the others.

Swissquote and PostFinance are pretty bad for large operations in this situation. And Yuh and Neon are bad for large operations as well.

For these three stock operations, we can draw some conclusions:

- Saxo is great for all operations

- Swissquote is good on average

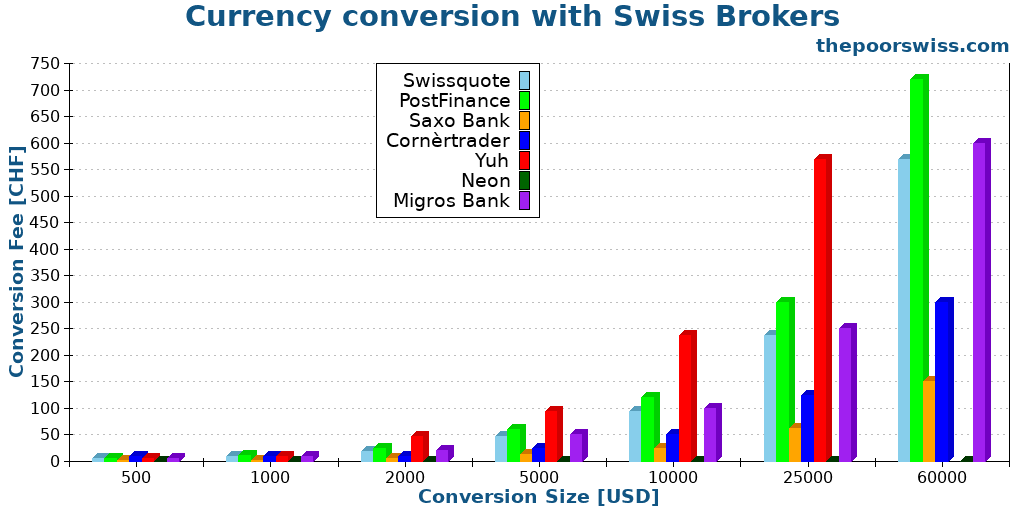

Currency Exchange Fees

Finally, before moving into the different scenarios, we need to consider the currency exchange fees. You must convert your CHF to EUR if you want to buy an ETF in EUR.

Here are the currency conversion fees of these seven brokers:

- Swissquote: 0.95%

- PostFinance: 1.20%

- Saxo Bank: 0.25%

- Cornèrtrader: 0.50% with a minimum of 10 CHF

- Migros Bank: 1%

- Yuh: 0.95%

- Neon: 0% (Trade everything in CHF at BX Swiss)

These fees are the same for CHF to USD and CHF to EUR. You may have to pay higher fees if you use more minor currencies. But these fees are all significant already!

Here are the fees for one conversion from CHF to USD for different order sizes:

Neon has a significant advantage if you can trade the stock on the BX Swiss stock exchange. If you cannot trade it on BX Swiss, you will need to find an equivalent or use another broker.

For other brokers: Saxo is much cheaper than the others, and all the others are much more expensive. Even with a minimum of 10 CHF, the 0.25% fee compared to the average 1% of the other Swiss brokers makes Saxo the only good Swiss broker for currency conversion. After that, Cornèrtrader is reasonably priced as well. But Neon is better if you can find your stock or ETF on the BX Swiss stock exchange.

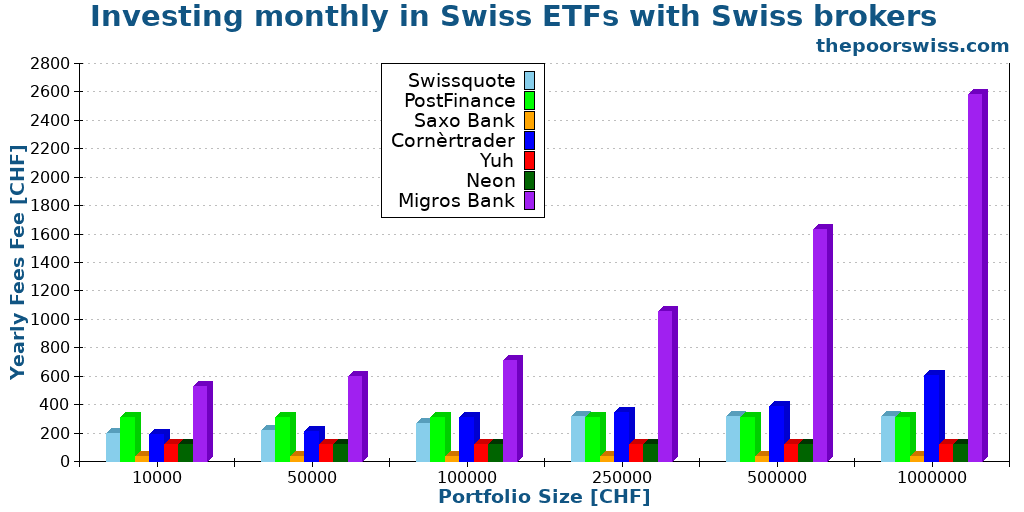

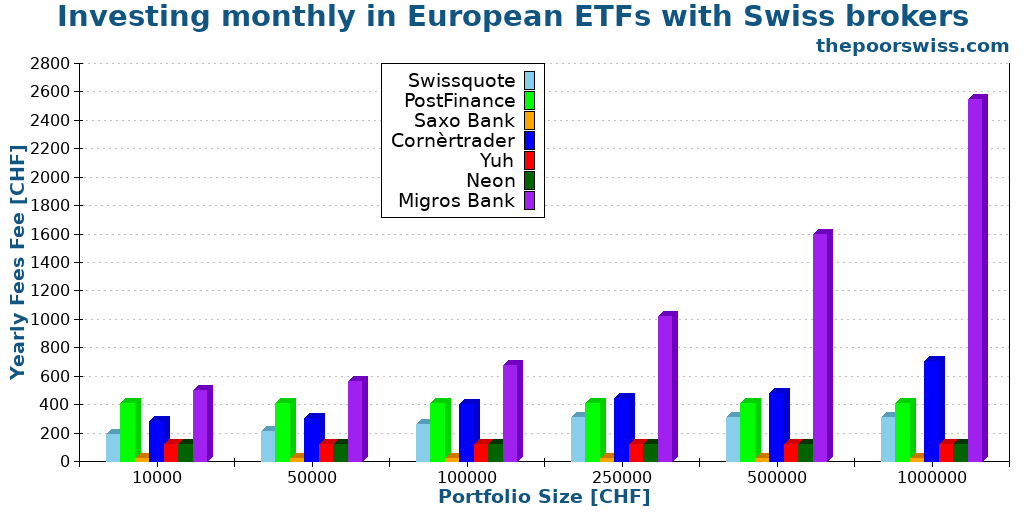

Scenario 1: One Swiss ETF per month

Until now, we have only considered a single operation in isolation. But it is much more interesting to look at everything together. We must look at a year of trading together with transaction and custody fees.

The first scenario is for an investor who buys shares of one Swiss ETF (in CHF) per month. Many Swiss investors only use the Swiss Stock Exchange. Since we must consider the custody fee, we must run the scenario with several portfolio sizes.

Also, since the prices change based on the order size, we must choose an order size. For this scenario, the investor is buying 2000 CHF worth of shares every month. 2000 CHF is a good average for monthly investing.

It is worth mentioning that some brokers (Saxo, Yuh, and Neon) have savings plans that can cut the costs in this case. Here I am assuming you are not using these plans, but if you are, fees can be even lower for these three brokers.

So, without further ado, we take a look at the fees of each of these brokers for one year for this scenario:

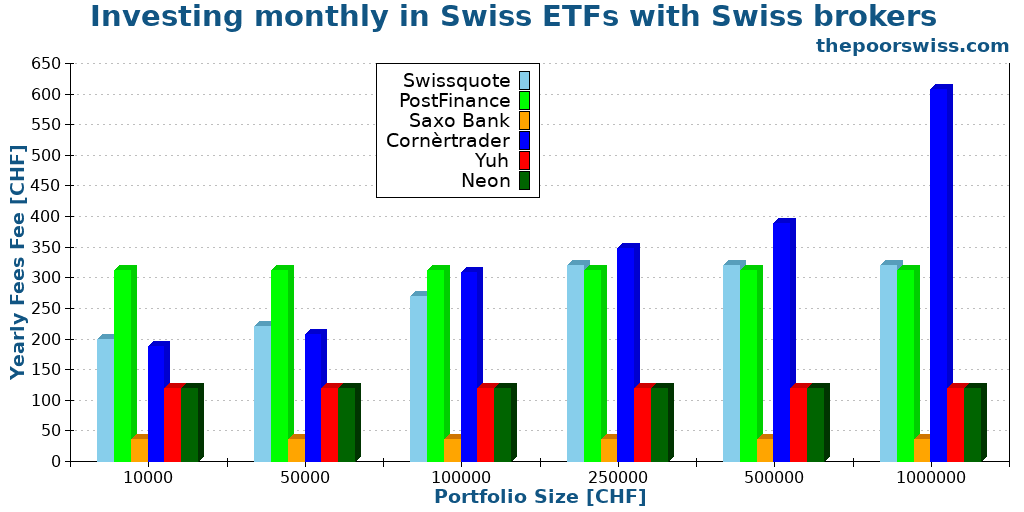

We can see that Swiss investors should entirely ignore Migros Bank. Their custody fees are too high for any serious investor. So, we can see this graph again with the reasonable brokers:

Unsurprisingly, Saxo is excellent since they have great transaction fees and low custody fees. Also, Neon and Yuh are great for large portfolios (having no custody fees). After this, Swissquote is excellent for small portfolios. On average, Cornèrtrader is the worst in this case.

So, overall, in this scenario, I would use Saxo. As a second choice, I would use either Neon or Swissquote.

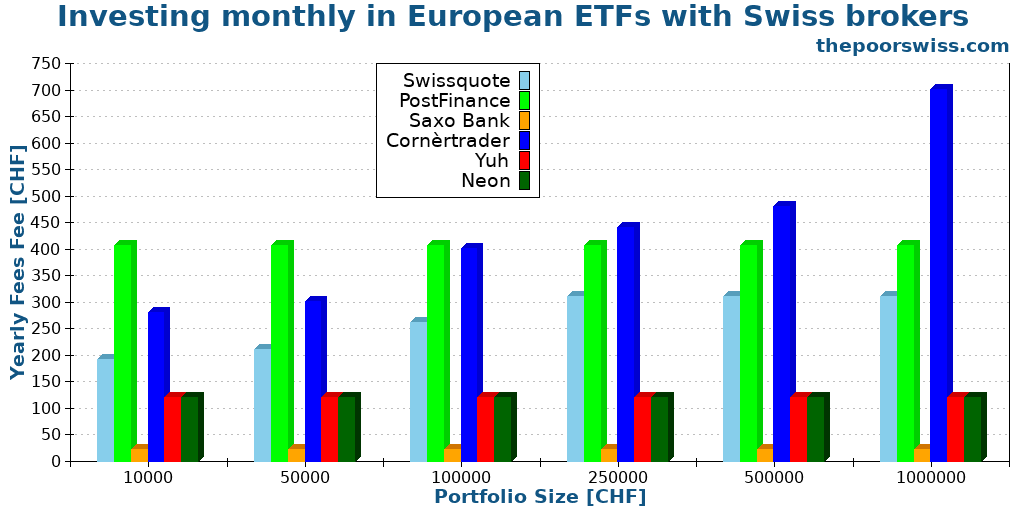

Scenario 2: One European ETF per month

A more interesting scenario would be to invest in ETFs on the European Stock Exchanges. Again, we look at one entire year of trading.

For this scenario, we will use a monthly investment of 2000 EUR in European ETFs. Again, since custody fees exist, we will use different portfolio sizes.

As expected, the broker with bad custody fees must be ignored again. So, here is the graph again without it:

When adding currency conversion fees into the scenario, we can see that the results are quite different, and everything is more expensive. With this, I would not recommend PostFinance anymore because of its bad currency conversion fee.

Saxo and Neon are the cheapest Swiss brokers. All other brokers are much worse. Swissquote, PostFinance and Cornèrtrader are the worst here, and Yuh is somewhere in the middle.

In this scenario, I would personally use Saxo or Neon.

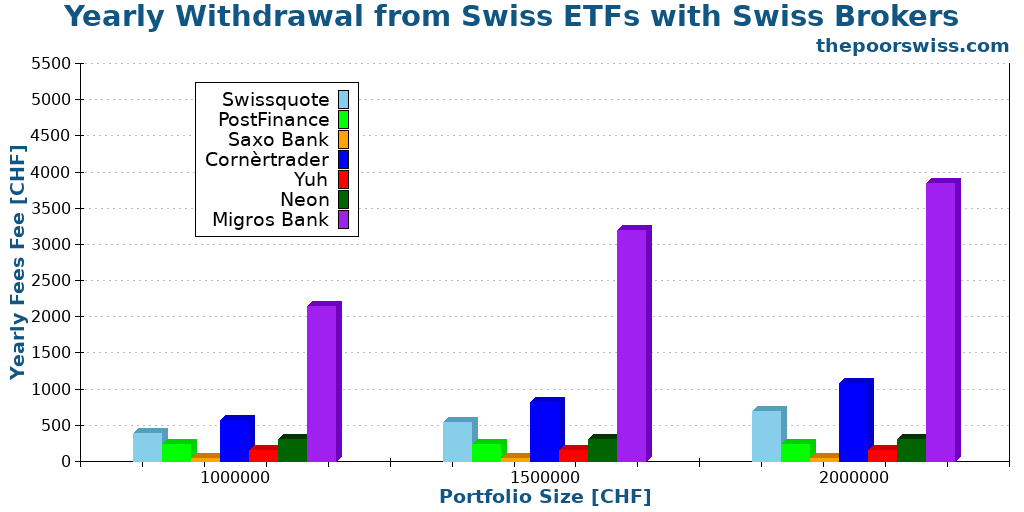

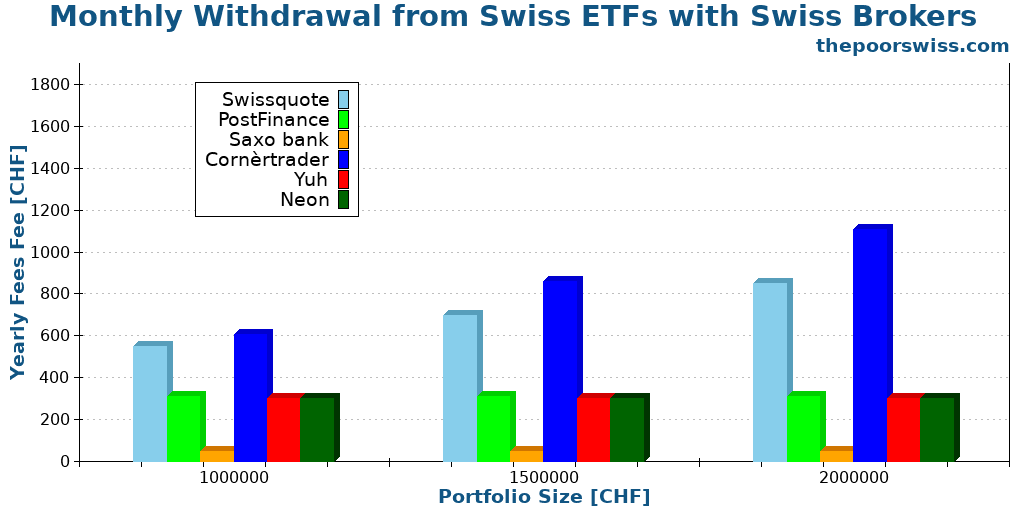

Scenario 3: Withdraw once a year

For our last scenario, we take something different.

The other two scenarios would represent an investor during the accumulation phase. Now, we can take a scenario that would represent the retirement phase.

If you want to retire based on your portfolio, you must sell shares to live from it. So, our scenario investor is selling for 60,000 CHF every year to live from his portfolio. We need different portfolio sizes since custody fees will play into this scenario.

First, we start with an investor selling 60,000 CHF of a Swiss ETF at the beginning of the year:

This is where we can see the impact of high custody fees. You have no income in retirement, and you could give your broker several thousand Swiss francs yearly! I would not recommend anyone to invest with such a broker! You need to find a broker for which the custody fee has a maximum.

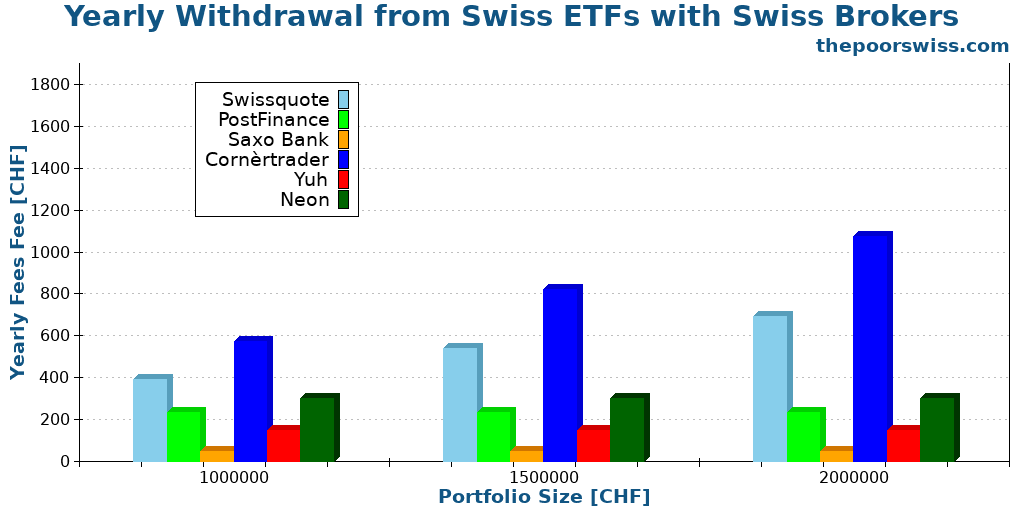

Here are the other choices:

In this scenario, Saxo is the cheapest broker. And Cornèrtrader is the most expensive, because of its custody fees. There is a 1000 CHF per year difference between the cheapest and the most expensive.

Withdrawing every month also has the advantage of keeping your money invested longer. I have run simulations, and historically, it is better to withdraw more frequently.

If the money is withdrawn each month instead, the results are still very similar:

The differences are about the same here. 100 CHF per year is not a huge difference. Nevertheless, Saxo is once again the cheapest option, quickly followed by PostFinance, Yuh and Neon. Cornèrtrader is significantly more expensive, given its higher custody fee.

Some people will argue that selling each quarter would be optimal to avoid large transaction fees. But this is a meaningless optimization. It will make very little difference whatsoever. You should withdraw either once a year or once a month. Ideally, once a month, you will have better returns in the long term since you keep the money in the market for as long as possible. But of course, there are other things to consider.

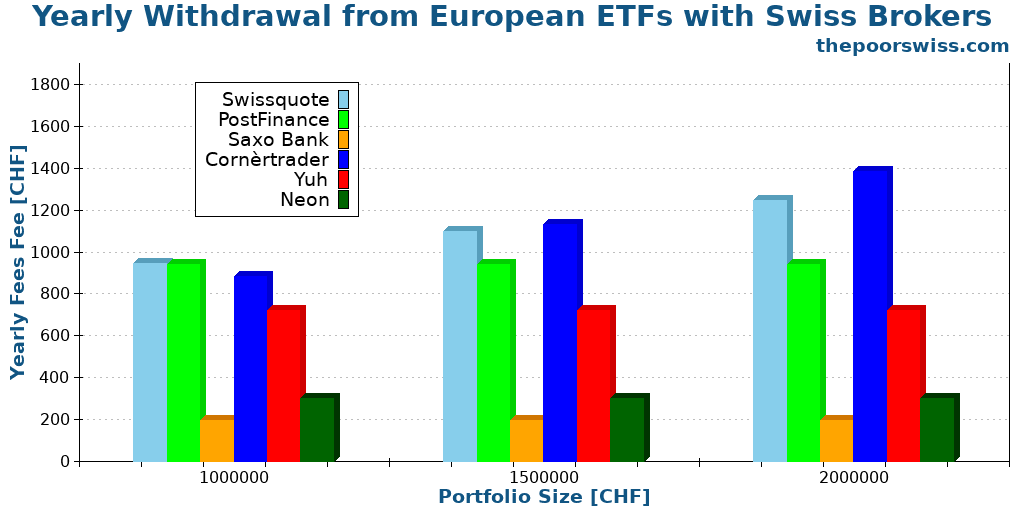

Finally, we can see what happens when we sell ETF shares on the European stock exchange instead of the Swiss Stock Exchange. Here are the results with our affordable Swiss brokers:

This time, the difference is more significant due to currency conversion fees. Saxo is the cheapest despite having currency conversion fees. Then, Neon is the second cheapest since you can avoid currency conversion.

Despite being twice as cheap at converting currencies, Cornèrtrader is still the worst one on average because of its custody fees.

In that scenario, I would use Saxo or Neon.

Conclusion

Start investing with a Swiss broker at incredible fees! Start trading with Saxo Bank and get 200 CHF in trading credits.

- Low currency conversion fee

- Swiss broker

Swiss brokers are expensive, but you can find some brokers cheaper than others if you search well. If you want a Swiss broker, I recommend Saxo as the best Swiss broker.

I use Saxo myself as my Swiss broker. They have excellent fees and will save you a lot of money. Additionally, they have all the features you need.

Neon and Swissquote are two decent alternatives. Neon is great for beginners, given its low costs on small operations. Swissquote is excellent for more advanced investors, with average fees overall. Furthermore, Swissquote has a good reputation and is well-established. You can avoid most currency conversion fees with Neon by trading on BX Swiss, which is a transparent service.

Another important conclusion from this article is that serious investors should not use a broker with a custody fee without a maximum. This quickly becomes too expensive. For this reason, I would not recommend using Migros Bank. They are far too expensive and will drag your returns down. And some Swiss brokers are even pricier than these two. So, Swiss investors should be careful.

If you are ready to use a foreign broker, I recommend investing with Interactive Brokers, which is cheaper. However, if you are afraid of having your money outside of Switzerland, it is much better to use a Swiss broker than not to invest at all! Since many of my readers have requested this from me so often, I feel like I had to write this article.

It is very fascinating to note that Swiss brokers have become cheaper over time. With the introduction of Neon and Yuh, prices have gone down. And since Saxo cut their fees significantly, they have become closer than ever to a broker like IB.

For transparency, Interactive Brokers is my main broker and Saxo is my secondary broker.

If you want more scenarios, you can use my broker comparison tool to suit them exactly to your needs.

If you want more details on the winners, you can read their reviews:

If you think investing fees can be taken lightly, you should read my article about investing fees and their impact.

What is your favorite Swiss broker?

More reading

FlowBank bankruptcy 2024: What happened to customers?

FlowBank Update. Essential information for former FlowBank customers: How to recover your funds, transfer your securities, and what happens next.

Saxo vs Interactive Brokers 2026

Local or Global? Saxo Bank vs Interactive Brokers: We compare fees, currency conversion, and safety to help you pick the best broker.

Yuh Review 2026: One app to pay, save and invest

Postfinance and Swissquote launched a new digital bank: Yuh. Yuh combines banking, investing, and cryptocurrencies in a single service!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Isn’t Trading212 better than IB?

There are no cash deposit fees with Trading212, but with IB there is. (min. 50CHF)

Hi FA,

Why would you deposit cash on your broker? Why don’t you do a bank transfer? It’s free.

I am not a big fan of Trading212. It does not have fees, but has larger spreads, which may make it more expensive than IB. It also insists on CFDs, which I don’t like.

And they don’t give access to the Swiss stock exchange.

It’s also regulated in Cyprus, which has a bad reputation.

Overall, I don’t trust them as much as I trust IB.

Really good post as always.

Something that is interesting to think about is the fee for moving your securities to another broker. I never thought about it until now.

I have opened a IB and a Flowbank account. And I was planning to move my stocks to my new accounts (swiss ones on Flowbank and US to IB).

My plan has changed a bit. Postfinance charges 107 CHF for each security you transfer. I have more than 10 of these, it would cost more than 1000CHF to move them.

Basically now I am waiting until I get to a good price to sell to then transfer money instead of moving the securities.

Flowbank charges 45 CHF for transferring securities for example.

That’s a good point. There are major differences between brokers for transferring securities. But most people should not worry about that since most people don’t have a portfolio to transfer in the first place :)

Personally, I use the sell and transfer technique, but I would not do it again. With timing and the time it takes to transfer money from one broker to another, it can be a big loss (or gain). Next time, I will simply pay the damn fee.

Hey Mr poorswiss

How good is the IB app? (Only 3* in Appstore)

Probably it would be good to exchange CHF to USD with Wise or Revolut to avoid currency fees?

Thanks for help!

Hi Dave,

For what I am doing with it, the IB app is good. But I rarely use it, I am desktop user. But it tells me how much is my portfolio worth and lets me buy and sell from it directly without issues. So, it does exactly what I need :)

No, it’s not really necessary. You will 2 USD per currency exchange, regardless of the size. Unless you are investing very little amounts, this will be better than Wise and likely better than Revolut given the monthly free limit.

Thank you for another amazing article! I love your blog !

I live in Switzerland and I have already an account with IB. I’m now considering trying flow bank with the goal on not holding all my assets in foreign broker like IB , but Having 50/50 or something like That for better security.

Do you think this could make sense or investing with 2 different brokers would become just too expensive in terms of fees ?

Thanks for your kind words!

I think it makes sense but only starting from some amount of money. If you have 10K, I would not do that. But starting from portfolios higher than 100K, it starts to make sense.

And in any case, if it helps you sleep at night, then do it, regardless of the amount.

I am considering doing that myself later.

Thank you for your reply, I really appreciate

Hi,

I really appreciate and enjoy your blogs.

You have mentioned that much (80%) of your shares are in the US stocks and in USD.

In case you plan to live in Switzerland after retirement, what is your plan for Exchange rates?

I looked at the trend of USD/CHF and CHF has appreciated from 1.37 in 2003 to 0.92 as of now.

Will this not eat up the savings if this continues?

Are you not better off investing in CHF than USD?

Hi Anuman,

In retirement, it could eat up some savings indeed. However, investing in CHF is not a great option either since there are not enough good ETFs in CHF. And hedging in CHF is expensive and in most cases not proven to be beneficial. You can read this article for more information: Should you use currency hedging in your portfolio?

For now, I believe that 20% in CHF is enough for me. But this could change in the future. I am extremely far from retirement, so I may change my mind in the future.

I will also receive a pension in CHF while retired and I will receive my second and third pillar in CHF, so this will help tilt the balance.

And with amount of US dollars “printed” during pandemic do you still think it is feasible to keep majority of your stocks in US?

PS: Great article, I would never be able to analyze it myself.

I think it’s still feasible yes. But it does worry me a little. Depending on how they take it, I may switch a little more of my money towards CHF funds.

Hi, many thanks for this research.

One thing I would like to ask: regarding trading ETFs at Swiss Stock Exchange with Swissquote, is the flat rate of 9CHF applying only to ETF listed in CHF or to all ETF listed at Swiss stock exchange?

Hi Kathrin,

It’s only for a selection of ETFs not all the ETFs of the Swiss Stock Exchange but there are several currencies: CHF, USD, EUR, and GBP, not only CHF.

Thank you very much!!!!

Hi, great read! I wanted to ask you one question. There is one graph (Yearly fees for Swiss Brokers for monthly investing in European ETFs), would you be able to share the excel of the same output with 1 trade every two months or 2 trade every quarter to compare the costs cross brokers/portfolios? Thank you in advance

I think Degiro and IB are the best solution for swiss investors

I agree, but many people a want a Swiss broker :)

For the moment I can’t wrap my head around one thing:

You have CHF, which you need to convert to USD to work with US broker. It incurs some conversion and transaction fee.

Then they need to buy Swiss shares with CHF, and incur conversion fee.

At the end story repeats.

So, it makes sense to buy long term only to offset these fees somehow, right?

Hi Alex,

With a good broker, such conversion is not that bad. But it’s true that with a Swiss broker, it’s pretty bad with a minimum of 0.50% with CornerTrader.

However, you can also transfer CHF to your foreign broker, like IB. When I buy CHF-stocks in IB, I directly use my CHF, no need to convert anything. I hold both CHF and USD on IB.

And a currency conversion on IB costs 2 USD.

Great article again, thanks.

How difficult/sensible would it be to change brokers dependent upon your portfolio size or accumulation vs withdrawal phases?

Hi,

It’s not that difficult to change brokers. In most cases, brokers have an automated system to transfer your shares from one broker to another. With this system, you will pay fees for each position you are transferring. So, if you have many positions, you will have to pay substantial amounts. If you only have one or two, you should be fine.

I have an article about changing brokers, this could be helpful.