Should You Contribute to Your Second Pillar in 2026?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

In Switzerland, you can make a voluntary contribution to your second pillar. These contributions come with tax advantages since you can deduct them from your income. Therefore, you have a return equal to your marginal tax rate. And this return is almost instant.

However, the money is then blocked into the second pillar. And the returns on that blocked money have been very low in recent years. Finally, you can only withdraw the money from your second pillar if you retire, buy a house, start a company, or leave the country.

Many ask whether they should contribute money to their second pillar or continue investing in stocks. In this article, I answer this important question. And we even have a calculator that will let you do all this without any math!

Second pillar contribution

So, how does a voluntary contribution to the second pillar work?

Usually, you pay each month some amount of your salary to the second pillar. And this is matched by your company. You do not have a say in this. So, there is no way to optimize that.

However, you can contribute some amount to cover the holes in your second pillar. If you had a low salary when you started, you will surely have holes in your contributions. When you contribute, you can deduct it from your taxes, just like the third pillar. The second and third pillars are among the best tax deductions.

How much of a reduction in taxes this will realize is challenging to calculate correctly. It depends on your marginal tax rate. The amount will depend on your income, your wealth, and where you pay your taxes. In most cases, this will be between 30% and 40%. That means that the immediate rate of return of this contribution will be 30% to 40%. We can view voluntary contributions as a form of investment.

Now, the invested money will be blocked until you can take it. In the second pillar article, we have seen only four cases when you can take this money out:

- building a house

- starting a company

- retiring

- leaving Switzerland definitely

When withdrawing the money, you will pay a withdrawal tax. This tax depends heavily on each canton. The withdrawal tax is significantly lower than the taxes you can save with the contributions. You can save on the withdrawal taxes with staggered withdrawals.

Voluntary contributions are always blocked for three years (only the amount of the voluntary contribution is locked, not the entire second pillar).

As long as it is inside the second pillar, your money will get some interest rate. Unfortunately, the interest rate is currently low now. You can expect about a 1% interest rate in most pension funds in Switzerland. Nevertheless, it is a safe interest rate for now. It cannot go down. So, you can consider the second pillar as a place to allocate your bond.

However, if you are lucky, you will get a better pension fund. Some pension funds have average of up to 5% per year, but they are quite rare.

There is a second tax advantage to the second pillar. You do not have to pay taxes on the second pillar assets. So, if you have a large net worth, you will not have to pay wealth tax on your second pillar assets.

But this is a smaller advantage than the first one. It will still reduce your taxes a little further, but where the first tax advantage can be up to 40%, the second advantage is about 1% in the best case. Nevertheless, it is still important to know that you do not pay any wealth tax on your second pillar.

Scenarios

The obvious alternative is to invest in stocks. We can check how the same sum behaves if invested in stocks or contributed to the second pillar. First, we run some scenarios to see how that works. We will simulate a one-time investment of 10,000 CHF.

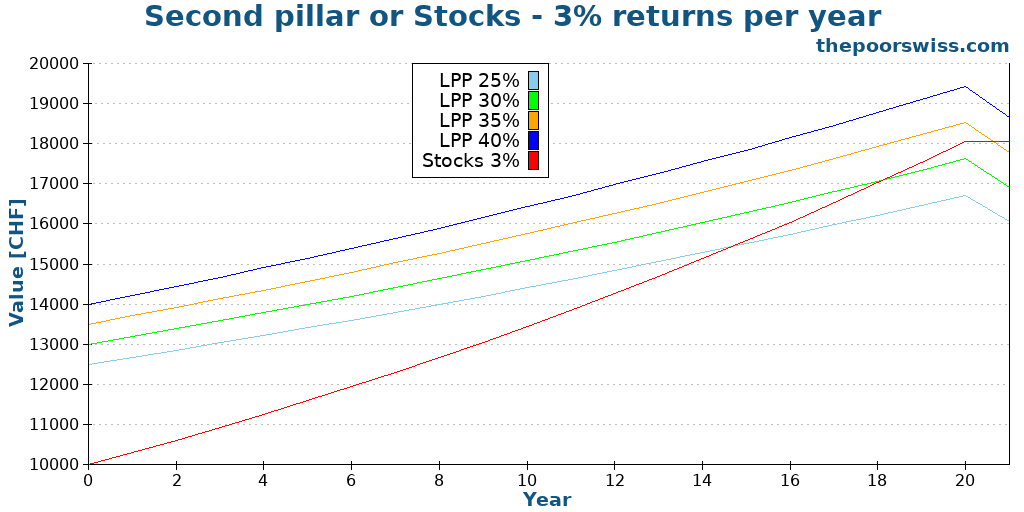

We start with a return per year of 3% for the stocks. This is a very conservative estimate. For the second pillar, we will consider 25%, 30%, 35%, and 40% marginal rates. The current interest rate on most second pillars is 1%. So we will take that as the reference.

The tax savings of the second pillar will be reinvested in stocks directly. So, if you have a marginal tax rate of 30%, 10,000 CHF invested in the second pillar will also result in 3,000 CHF in stocks.

Finally, we will consider a 4% withdrawal tax on the entire amount. In practice, this would only apply to the second pillar, not to the savings you have invested. But in practice, the tax is often higher than 4%, so applying 4% to the total is a reasonable assumption.

Here are the results for twenty years.

As you can see, it takes about 15 years for the stocks to catch up with even the lowest marginal rate. And it would take more than 20 years for the stocks to catch up with the high marginal tax rates.

In that case, a 3% return per year on the stock market is slow to catch up with a substantial interest rate as a tax deduction. So, if you expect 3% from stocks, you should probably favor your second pillar.

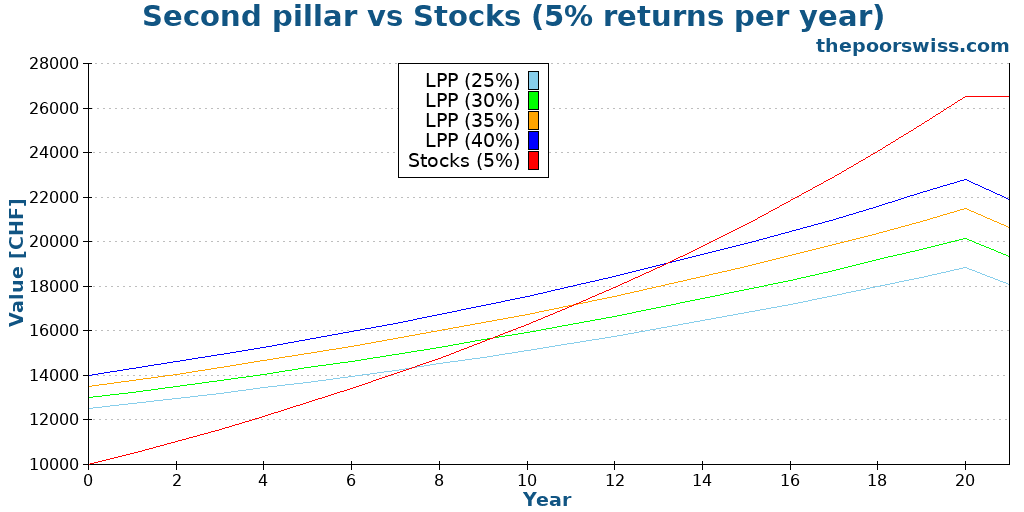

But generally, stocks are returning more than 3% per year. So, we will see what happens with a 5% return per year. This is what I expect on average from the stock market.

This time, it takes less than ten years for the stocks to increase as much as the second pillar, with the lowest marginal tax rate. But it almost takes 15 years to catch up with the highest marginal tax rates.

This exponential growth is the power of compounding. Even 5% per year can return a lot in the long term. 5% per year is what I expect from the stock market.

Obviously, in practice, you will not get 5% per year. You may get 10% one year and -20% the next year. But this is how the stock market works, and I am prepared for this. You can only expect average returns over the long term.

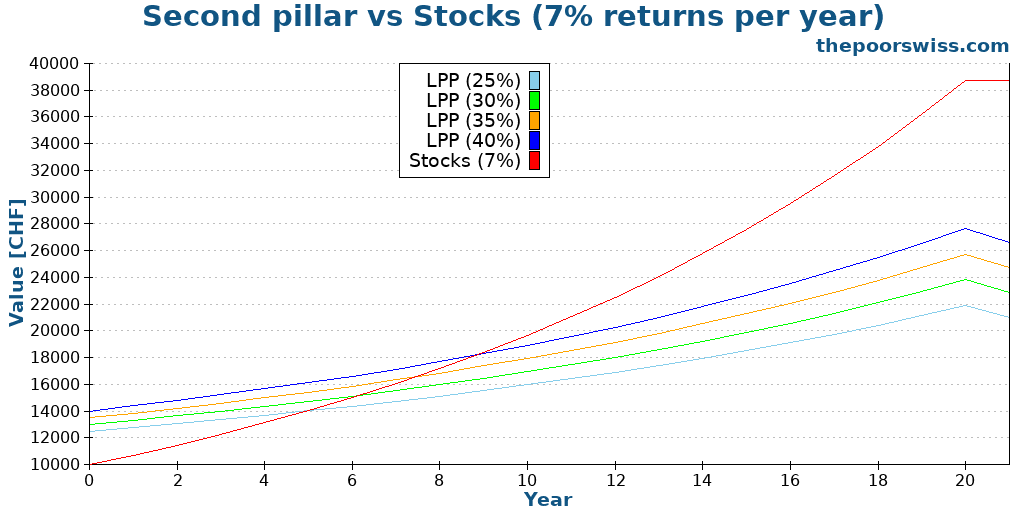

Now, some people are counting on about 7% of yearly returns. So, here is how that will go:

With 7% of stock returns per year, the return on the second pillar contributions is dwarfed. Even the highest marginal tax rates would be beaten after less than ten years. Compounding gets stronger and stronger as the returns increase.

So, we can draw a few conclusions from these results:

- The second pillar is interesting if you have a high income.

- The second pillar is interesting if you reinvest the tax savings in stocks

- If you expect very high returns from stocks, you should avoid the second pillar

- Over ten years, the second pillar is interesting

- Over more than 20 years, the second pillar is rarely interesting

However, there are other considerations. First, it will depend on the term of your investment. If you are investing long-term, it is probably better to stick with stocks. But if you are to get access to your second pillar soon, it may be a solid investment. It could be a good investment if you retire soon, build a house, or start a company in the medium term.

But do not forget that voluntary contributions are blocked for three years. So, if you intend to buy a house in the next three years, you should not invest in the second pillar (unless you already have enough in the second pillar without the voluntary contribution). If you plan to buy a house without the second pillar, you can continue your contributions if you have enough cash for the down payment.

Another thing you need to consider is whether you have a great second pillar account or not. If you have a good second pillar account invested in stocks, it will become more interesting to invest in it! But most people in Switzerland will not have access to a good second pillar.

The other consideration is whether you need bonds in your net worth.

Your bond allocation

Due to its safe nature and the guaranteed interest rate, I consider my second pillar bonds. I integrate my second pillar into my net worth as bonds.

So, another reason to buy into the second pillar depends on your allocation. If your bond allocation is too low for your current allocation, you can voluntarily contribute to increasing it. Given that it also has a nice tax advantage when you purchase it, it is probably better than bonds.

When Swiss bonds are negative, the second pillar is also much more interesting than Swiss bonds. If I need to increase my bond allocation, I will invest more in my second pillar instead of bonds.

At the start of 2021, we had 5.2% allocated to bonds in our net worth. Since we aim for 10% bonds. So, it shows that we should contribute a little to our second pillar. Unfortunately, it is not a good time for us, as we will see in the next section.

Proper Timing

There are some cases where it becomes very interesting to make such contributions.

- When you know that you will retire or buy a house in the medium term (but further than three years). Since they are short-term investments, it is good to use them as such.

- When you know that you will leave your company and switch to vested benefits account. This could be the case when you are retiring early or leaving Switzerland. These accounts are often much better than second-pillar funds. So it could be interesting to max out your contributions to have them invested properly.

On the other hand, there is one case where you should not contribute to your second pillar: when you do not get any tax advantage. When you withdraw money early from the second pillar (for a house or business), you will not get any tax advantage until you have paid back the withdrawn money. So, as soon as you withdraw money from the second pillar, it becomes pretty much useless to put more money into it.

This is the case for us. We just withdrew money from our second pillar and cannot get any tax advantage until we contribute at least 50,000 CHF. So, without the tax advantages, it does not make sense for us to invest in the second pillar.

These examples show that timing is important for second pillar contributions.

Our second pillar strategy

We have decided to contribute to our second pillar each year. So far, we intend to contribute 10,000 to 20,000 CHF each year.

We have a few elements to back up our decision.

- I plan to retire early. If my plan works, my money will only sit in a second pillar for at most 15 years. Then, it will go into a vested benefits account where it can be aggressively invested.

- We have a high income in a high-tax canton, meaning a high marginal tax rate (at least 40%).

- We currently have a decent second pillar. The conditions are good, and the historical average return has been more than 3% per year, which is above the average of second pillars.

If these conditions were not met, we would probably not contribute. But together, these conditions make the second pillar a good investment for us.

Use our calculator

If you do not want to do the math yourself for your exact situation, we have developed a second pillar calculator. This calculator will let you enter all the data about your situation:

- How many years until retirement?

- Your taxes.

- How much returns do you expect from your second pillar.

- How many returns do you expect from your investments.

- How much withdrawal tax you will pay on your second pillar at retirement.

We hope this helps you find out for yourself whether a contribution to your second pillar makes sense for your situation or not.

Conclusion

We have been contributing to our second pillar for the last few years to reduce our taxes.

From an investment standpoint, contributions to the second pillar can be a good medium-term investment. However, you should only do them if you have a high income.

Moreover, if you expect very high returns from your stocks, the second pillar becomes less interesting. And you should try to reinvest your tax savings in stocks. Even though they have a substantial initial return on investment, they have very low returns per year after that.

Moreover, the money in a second pillar is an excellent alternative to bonds. They have a guaranteed (at least for now) interest and offer an excellent tax reduction. These tax reductions would be quite interesting as one is nearing retirement. But remember that you can only contribute to your second pillar if you have a salary or have your own company.

But it is not necessarily the best investment at all times. Like every other investment, it will depend on your context and your situation. You should consider every element before you decide on any investment. And never make any rash decisions!

Finally, keep in mind that if you are withdrawing your second pillar from another country, the withdrawal taxes may be entirely different, so you will have to adapt the calculations if that will be the case for you.

If you are interested in saving money from taxes, you can read my article about the best tax deductions in Switzerland.

What do you think about this? Are you contributing to your second pillar?

More reading

How many years until you can retire?

Did you know how long you need to retire only depends on your savings rate? Find out how many years until you can retire!

Second Pillar: All you need to know to retire in Switzerland

Maximize your Second Pillar (LPP). Discover how occupational pensions work in Switzerland and how to optimize your contributions for a better retirement.

Disaster File – A Simple Way to Prepare for Your Death

Secure your family's future. Learn how to create a "Disaster File" with essential documents and passwords to help your loved ones if you pass away.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

1. I have a B permit (and pay tax at source) and consider making a voluntary contribution to 2nd pillar. Will I benefit from related tax deduction, even though I pay tax at source?

2. If yes, are there any thresholds to consider for amounts to contribute with regards to % deductions?

Thank you.

Hi,

Keep in mind that I have never paid tax at source.

My understanding is that you will only benefit if you do a full tax declaration. So, you will have to ask for a full tax declaration and will have to fill it entirely, including your second pillar contributions.

The higher your taxes, the more interesting it is to contribute. But as you contribute, the marginal tax rate diminishes and the interest of your contribution lowers as well.

I don’t think there are thresholds. The way I would do it is put the numbers into the tax declaration software and see at which point it becomes less interesting.

Dear TPS,

I performed the same simulation for the 3rd pillar.

Cause I thought the same principle would apply. Stocks invested independently Vs 3rd pillar 100% in stocks. I assume both portfolios have same return.

Does it really make sense?

A. Stocks. No tax deduction today but no capital gains tax in X years.

B. 3a. Tax deduction but 16% tax rate on the withdrawals which will for sure have a higher taxable base.

Do I make sense?

Hi Héctor,

the principle will mostly apply but the numbers must be changed. I did the same simulations for the 3rd pillar.

A) You will not pay capital gains tax. But you will pay wealth tax and this is applied on the total, including capital gains.

B) You will not get 16% tax on withdrawals unless you have a huge third pillar and you don’t spread your withdrawals.

Thank you very much for your article and the great blog in general!

I moved to Switzerland and started to work in September. Would it make sense to pay my gap to the second pillar this year or wait for next year to have a larger tax benefit?

Hi Andreas,

If you are planning to contribute to your second pillar, you should definitely wait until a full year working. Otherwise, the tax credit will be too low. And you should probably only do that if you have a large income.

Ciao poorswiss,

I am in a situation where I have to take 2 decision

1) choose my 2 pillar contribution, either 5.5% or 7% (that’s a difference of ~150chf taxed at a marginal tax of 30%).

2) Decide if I will do a 60k buyback.

How can I apply some math here, given that my 2pillar as a flexible interest as it’s managed by the enterprise I work for (1,2,5 even 8% once), or that I would use the extra money to invest in VT as I do monthly.

I’m going to be 30 soon, I’m at 35% of my FIRE, I don’t know how long I will stay in Switzerland and if I will buy a house, therefor is pretty difficult to make any decision due to too many variables.

I guess that if I want to buy a house it’s good to buyback and increase the 2 pillar as max as i can, as i get tax advantages (to use for the house or invest) and the actual 2 pillar to buy whenever I want, rather than depending on the market situation if I can withdraw or not.

Also if my 2 pillar would return at least 3% or 4% constantly, I would still benefit from increasing my 2 pillar.

Am I missing something, or do you have a special formula? :D

Hi Daniel,

To apply some math, you need to take into account some average returns. Try to find the track record of the returns and use an average.

I don’t have a special formula, just a few scenarios in my spreadsheet :)

Investing in the second pillar mostly depends on the time you are going to let the money in the second pillar. If you are thinking of buying a house in the next 10 years, or leaving Switzerland in the next 10 years, I would say go for it since you seem to have a good second pillar.

Just be careful they are going to be locked in for 3 years.

Anoter interesting thought is whether you need bonds in your allocation. If you already have too much in stocks, it could be interesting to have some extra money in the second pillar.

Hi there,

Maybe joining the debate a bit late, but do you consider that your tax saving investing in a 2nd pillar where reinvested. I.e you buy back 50K CHF of second pillar save 20K CHF of tax that you can re-invest. That’s a massive argument for second pillar.

Good article and good comment section globally, thanks for that

Hi,

Yes, the tax savings are reinvested in my scenarios :)

Hi,

Joining the debate even later :).

I am wondering if your calculations are correct in this case. I see 2 ways you can reinvest the tax savings:

1) Reinvest in the 2nd pillar. In this case, if you put 10k every year and save 30% in taxes, then:

– Year 1: deposit 10k

– Year 2: deposit 10k + 3k

– Year 3: deposit 10k + 3k + 900

In particular, I don’t think you considered the tax savings on the tax savings reinvested in the 2nd pillar (0.30*3k = 900 in the example above). Which actually goes on (tax savings of the tax saving of the tax savings reinvested in the 2nd pillar, … :)).

2) Reinvest in stocks. I don’t think you considered this option in your blog, which I atually think is the best option and, if I did the math correctly would provide more total asset value for ~18 year (for 5% stock return, 1% pension return, 30% tax saving) with respect to investing only in stocks.

Or did I misunderstand something?

Apparently, I did not consider tax savings at all, at least looking at the formulas on my spreadsheets. I will need to update this article by redoing all computations.

And yes, it should be reinvested in stocks which definitely makes more sense.

Hi, I was just wondering if in your simulation you took into account that the money invested in stocks is subjected to 1) Capital tax during the entire period and most importantly 2) withhold tax when converted back to cash. I guess if you consider this the figures would look less attractive for the stock investment option?

Hi Investor,

I did not take 1) into account because wealth tax is generally small and extremely different in each canton and for each investor. For instance, because of my house, my taxable wealth is zero. But that’s still an argument in favor of second pillar.

I do not understand what you mean by 2) ? There is no withholding tax when converting stocks to cash. What do you mean?

Hi,

How is the tax-gap specified?

Assume someone who starts working in Switzerland in 2021

I assume initial tax-gap is zero?

Or can there be a contribution for years prior to 2021 (out of Switzerland)?

Hi Fred,

I believe it only starts when you start working. But you can easily obtain that number from your pension provider.

Thank you.

They seem to think there is some problem with me not earning a threshold amount of CHF 22,000 a year (or so) which they call the threshold amount. It is for this reason they do not want to accept the money from the vested benefits account. I will persue the matter further. Your input was greatly appreciated.

Hi Bruno,

Unfortunately, they are correct. To contribute to the second pillar, you need a minimum yearly income of around 21K CHF. Below that, you will not be eligible to the second pillar.

The 2nd pillar is highly underrated. Sure it’s boring and it doesn’t make headlines, I understand it. A lot of people have a 40%+ marginal tax rate, so the initial tax saving is huge. Even for those of us living in lower tax cantons we save around 30% from the taxman. Speaking for myself I never paid more than 6-7% in tax and I am proud of it. My 2nd pillar average return for the last years is around 3.5%. My fund(s) were only average, there were good years and bad years. Not great but ok considering the much lower risk. Even if your retirement is far away – lets say you are only 40 you can use the money to pay off your house or buy your home with cash. I know this is very unswiss, but you get rid of your debt. The only issue I have is that I am running out of the retiring plan gap and find myself chasing a new higher paid job in order to have the gap again. Not paying tax is kind of addictive.

There are a lot of cons and pros but I think the 2nd pillar is a no brainer. 2nd pillar investments are not so efficiently managed, the whole financial industry takes advantage of it. But so do you. For me it’s show me the money and just future profits won’t do it.

Should I say that I have a small investment made 15 years ago in some small markets and until now I haven’t got my initial investment back. The same can happen to any market.

Probably the best way is to consider the 2nd pillar some kind of bond investment and also invest in the stock market taking into account that you can lose most of the money invested.

Hi X41,

I would think it highly depends on the second pillar you have. You may not realize it, but you already have a good second pillar. My second pillar returns 1% per year (and only on the mandatory part).

If my second pillar had a 3% return, I would invest.

So, I do not agree that this is a no-brainer. If you have a bad (average) second pillar, like me, you should not invest. If you have a good second pillar like you, it’s a good investment indeed.

Also, it is only interesting when you have the tax advantages (like most people).

But I completely agree that the second pillar should be considered as bonds.

Thank you for the article. Very nice and informative. Would 3 year lock-in for voluntary contribution be applicable even if you decide to leave the country? Or in that case, it would be possible to withdraw earlier?

Hi Vishal,

That’s a good question. I am not sure honestly. I would think that it does not apply in that case, but I am not sure. I would contact your second pillar provider to ask them this question.

In reply to the question above, the 3-year lock-in period still applies even when you leave the country. You have to wait until the expire of 3-year to be able to withdraw it.

Thanks for pointing that out! It makes sense that it applies indeed!

Dear Mr. The poor Swiss.

I have recently got a new job but it is only working 9 hrs a week for 9 months of the year.

I am over 61 and have been collecting unemployment benefit for over a year.

The new employer has a pension fund. My question is:-

a. Can I transfer the money from my Vested benefits account into the new employers pension fund.

b. Can I make personal payments into the new pillar 2 fund.

If I am unable to do a. or b. are there any other ways I could reduce my tax burden and save effectively for my upcoming retirement?

Hi Bruno,

a) You can transfer the money from your vested benefits account to the new pension fund. And in theory, you are obligated to do so, but nobody will check and as such, this is kind of a grey area. However, this will make nothing for your tax burden.

b) Normally yes. You have to contact the pension fund and ask them how much you can contribute. And then you can do some contributions. Keep in mind that these contributions will be locked for 3 years.

i can confirm this. 3yr lock-up applies for cash withdrawal too. I am currently in the same situation. I will be leaving Switzerland in 2022 to live in the EU so I have been filling up all my previous years gaps (buy-ins) in my 2b pillar (extra-mandatory). Literally the best 3-year investment as my marginal tax rate is quite high.

Would I also be able to access my 2a pillar (mandatory 2 pillar) in case of being self-employed in my new country?

thank you, Adam

Do you mean whether you can use your second pillar to create a company abroad? I have no idea. My guess would be no, but I am really not sure.

Hi Hector

If I leave Switzerland and transfer my second pillar to a vested benefits account, can I also transfer the 3-year locked-in tax free component?

Hi Neil,

My understanding is that you should be able to transfer into a vested benefits account, but you won’t be able to withdraw it outside of the vested benefits account.

It’s pretty much a moot point because you can transfer to a vested benefits which is properly invested rather than keep it in your workplace pension where de facto you are subsidising the old people.

So even if it is locked in it doesn’t matter really.