The 13 Steps of My Monthly Personal Finance Routine

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Having a personal finance routine can help save time and money! For many people, having a strict routine will help them remember essential things. It is the case for me. Each month, I follow the same personal finance routine for my budget. In this article, I describe the steps I am doing every month.

It is great to have a routine. It helps you get more efficient, and like this, you do not forget to do anything. And once you start doing it routinely, it becomes automatic, and you will save time. And time is your most important resource. And following a personal finance routine will help you avoid mistakes and save money in the process!

Of course, you do not need to follow the same steps as me. You should probably not have the same steps. Every people can have different things to do based on the way they are investing or based on their situation.

But I would encourage you to define at least a monthly routine clearly. You can use mine as a base template if you want. And why not even a weekly routine?

So, here are the 13 steps of my monthly personal finance routine.

1. Pay my monthly bills (after salary)

All the services you need to pay, save and invest, in a neat package, with extremely good prices!

Use code tpsummer to get one year of Neon Plus and your debit card for free!

- Invest with great fees

Once I receive my salary, the first of my personal finance routine steps is to pay my monthly bills for the next month. I do this with the Neon mobile app.

These bills are my mortgage interests, taxes, insurance, credit card bills, and sometimes exceptional bills like Billag or some bi-annual bills. My salary goes into my checking account. I also receive some bills in my mailbox that I pay at the end of the month.

Why am I doing this first?

For the simple reason that I want to know how much I have left for next month. And I want to know how much money I can invest this month. I do not believe in the “Pay Yourself First” philosophy. It does not make any sense. If you save as much as you can, there will be something left to pay yourself. Pay yourself first makes you complacent, thinking you cannot save more.

2. Check my emergency fund

I always keep about two months of monthly expenses in my emergency fund. My emergency fund holds about 10’000 CHF.

I directly keep my emergency fund in my checking account. If you have access to high-interest savings accounts, you should use them instead. But in Switzerland, we do not get any interest in bank accounts.

So, once I have paid my monthly bills, I check how much I can move to my broker. I always keep about 10’000 CHF in my checking account. I invest everything higher than that. So, if I have 16’700 CHF left, I will invest 6’700 CHF this month. It cannot get simpler than that!

3. Invest my extra savings

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Once I know how much I can invest, I transfer this money to my broker account. It generally takes one working day for the money to arrive at Interactive Brokers. After I receive the money in my broker account, I directly invest it. For instance, I can invest all the money in my VT ETF.

I am using the new amount to rebalance my portfolio. I am investing in the fund that is the most below its allocation. It is how I am balancing month by month. I never rebalance my portfolio. It is in check with my overall investment strategy.

Currently, the stock market is my only investment. But if I were to make other investments, I would split the money between the stock market and the alternatives.

4. Check my spending and budget

At the beginning of each month, I look back at the budget of the past month. I try to do this as early as possible, ideally on the first day of the month. I check every expense and earning for mistakes. Once I am sure of my expenses, I take note of my savings rate (which can still change with the next two steps).

I am doing my budget in a straightforward way with multiple categories and an amount per category. What matters to me is that I have an accurate view of all our expenses.

And most importantly, I take a look at how much we spend on every category. I try to understand what went well and what did not go well. It will help me improve month after month.

If you aim to improve your budget a little each month, your budget will be much better after a year!

5. Check my credit cards

I am also checking that all the expenses from my credit cards are in my budget. I also check every credit card expense for possible mistakes. Several times I forgot to add small expenses to my budget from my credit card. The biggest benefit is making sure that there are no errors or frauds on my credit card statements.

It is also an excellent time to check if I can buy more things with my credit card. Now that I have several credit cards, it is good to check if some expenses are not using the correct credit card. I want to minimize my fees as much as possible. And maximize the small bonus I get for spending with my credit card.

But if you want to keep it simple, you can also not bother with credit cards and use your bank cards! It will not make a huge difference and it will make it easier to track your expenses.

6. Check all my accounts

After my credit cards, I check all my accounts. My goal is to get the current value of each of them.

Fortunately, I do not have many accounts. I have a checking account, one at Migros Bank and another one at Neon Bank. For each of my checking accounts, I verify all the transactions. I also make sure I have put each of these transactions in my budget. It is generally the only account that is moving significantly.

Finpension 3a is the best third pillar in Switzerland.

Use the FEYKV5 code to get a fee credit of 25 CHF!

- Invest 99% in stocks

I also check my third pillar accounts at Finpension 3a. I check the value of each of my investments. Once I have all these values, I can carry on to my next step.

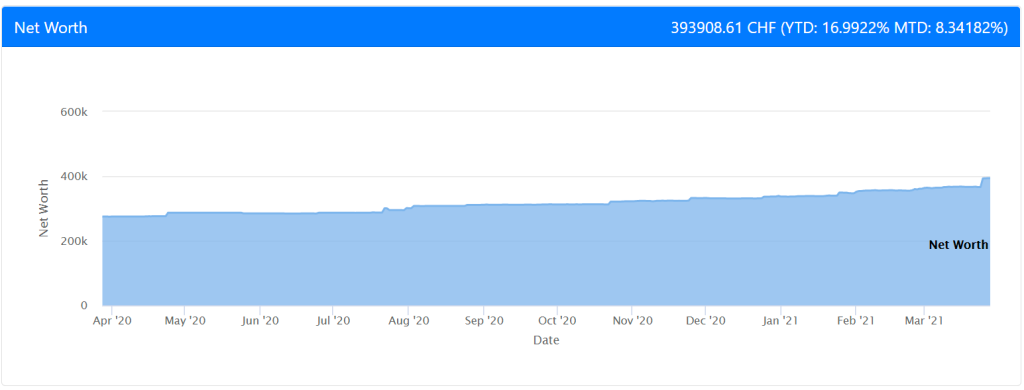

7. Update my net worth

Now, I got the values of all my accounts and all my investments. It is time to put them together in my net worth tracking application. Once it is done, I get my new net worth!

I can see how much the net worth increased (or decreased) compared to last month. I also track how much my net worth grew from the beginning of the year.

For me, these are important personal finance metrics to keep in mind.

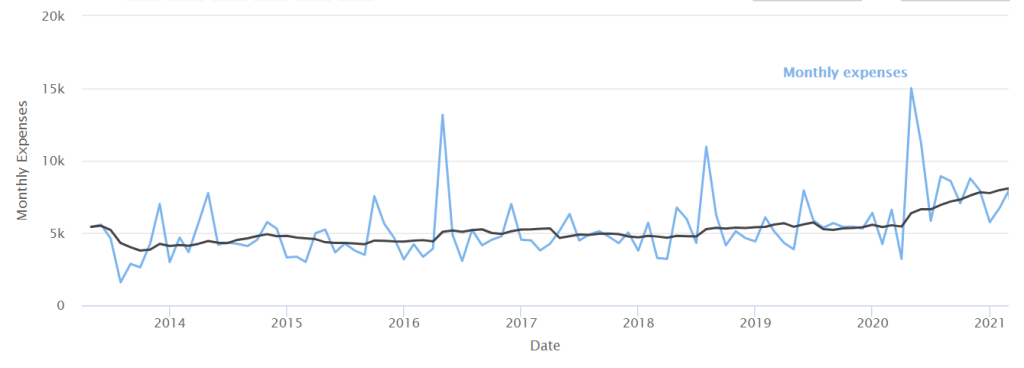

8. Keep track of the trends

One thing I also like is to compare the trend of several things. In the previous step, I can compare the direction of my net worth. It should, of course, go up. But it should ideally accelerate its ascent.

I also check the trend of my expenses. For instance, I keep track of the pattern of my expenses over time. One thing that is very important for me is the 12-month average. For example, for my expenses (in black):

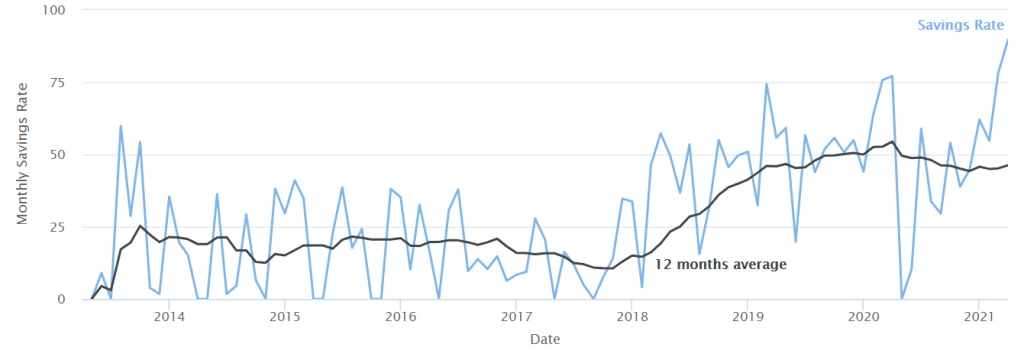

Ideally, I would like the average to go down to 4500 CHF. But these days it is not great. I cannot even keep it below 5000 CHF. The average is more important than the value of each month. Because you may have some lousy and perfect months, but the average should stabilize. I am also checking the trend of my income. And very importantly, I am reviewing the trend of my savings rate. It is the most important trend for me.

Since I started to improve my finances in 2017, my average savings rate has been consistently going up. It is an excellent sign.

I also check the rate of my income and earnings. Most of my income is very regular since it is my salary. But I also get a little income from this blog. And I like to check how earnings are going.

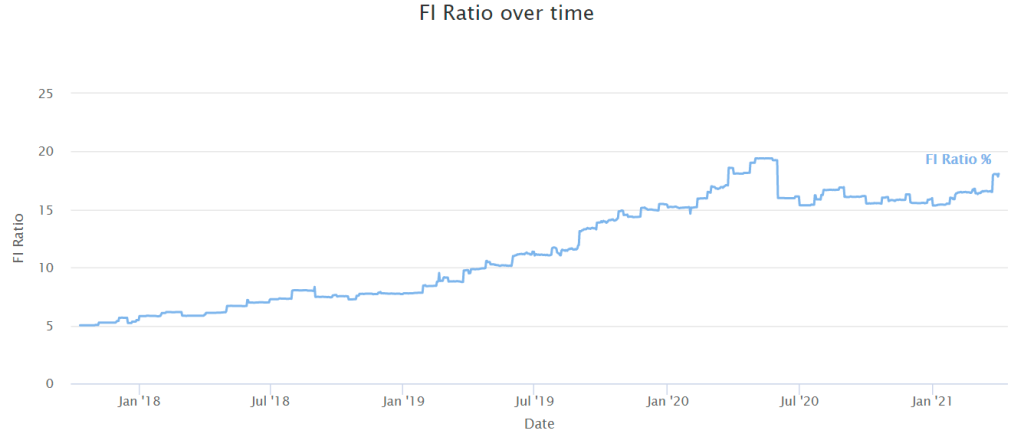

9. Check my Financial Independence (FI) Ratio

After I finish all the data, I will get the final numbers out. I can check my savings rate, of course. And its trend is seen in the previous section. But the last value I am checking is my Financial Independence (FI) Ratio. This metric tells me how far away I am from being Financially Independent. I can also check the trend:

My FI ratio should always go up. For now, it is increasing quite slowly. I am working on making it grow faster. But I am not stressed as to when I will be able to retire.

Currently, our expenses are not yet very stable, so this causes our FI ratio to jump all over the place.

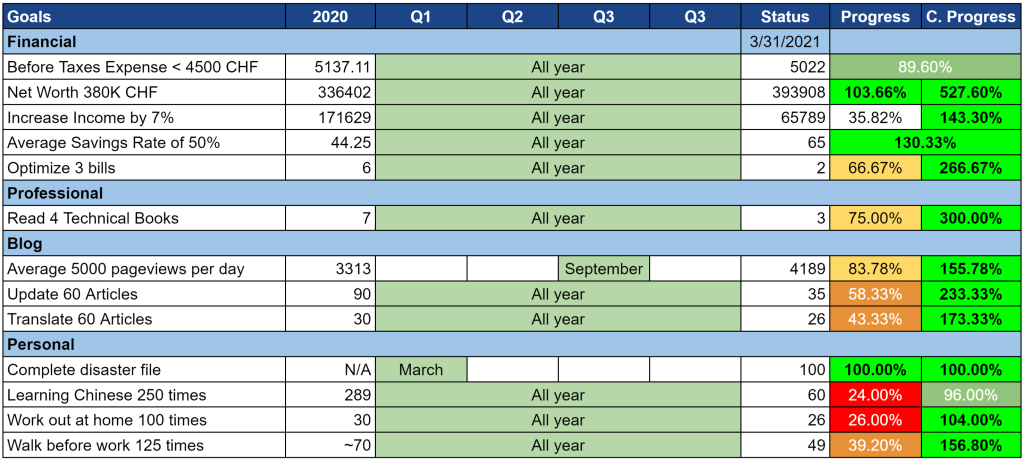

10. Update our goals

Finally, I now have all my numbers. It is time for me to check the current status of my goals. Every year, I try to set a few goals for the entire year. And every month, I check how the goals are going.

For instance, here is one recent update on my goals.

It helps me to have a good idea of where I am. It also helps me see what to do better to reach my goals.

11. Set next month’s goals

Once I have finished inspecting my yearly goals, I set a few goals for the next month. For instance, if I have spent too much in one month, I set a very strict limit on spending in the following. I am also setting soft goals such as:

- Research credit cards to find a better one

- Research bank accounts to find a better one

And so on. I try to put 4-5 goals for each month. I do not always report them on the blog. Generally, I write them down on a piece of paper.

And once I have my goals completed, I try to make a small plan of what I can do to improve my goals.

12. Study the analytics of the blog

This blog is my only side hustle. So, I am incorporating it into my monthly personal finance routine. If you have other side hustles, it would be good to check them every month as well.

I am checking how much traffic this blog got and comparing this to the previous month. I am using Google Analytics for this. If some pages get more traffic than usual, I am trying to understand why. And if the traffic is going down, I am also trying to understand why.

I am also checking if my blog consumes too much power on my hosting plan. I am using SiteGround to host this blog. Since I use one of their cheap plans, I must ensure I do not use too much. If I use too much, the decreased performance will impact the readers’ experience negatively. If it is too high, it is time to go to a higher hosting plan.

I also checked the income I got during the month. But this is currently not my focus on the blog.

13. Post on the blog

Finally, my personal finance routine’s last item is to post my monthly report on this blog. If you do not have a blog, you may write a small report on your computer. Or you could keep track of the numbers for the next month.

For instance, you can check out the most recent monthly report. This post has the details of my expenses and income. It also contains the current status of my goals. And, of course, some information about things that happened during the month. And my expectations for next month.

Why am I doing this?

I am mostly doing this for myself. I want to keep track of my financial status. I also believe it makes me more accountable. And it helps to keep me motivated. And since I like reading monthly reports, maybe some people will enjoy mine!

What I do not do

You may have seen that there are also some things I do not do.

First, even though I check the value of my funds, I do not plan any action for them. I do not want to sell or buy based on the price of the funds. I buy as soon as the money reaches my broker account. And I do not sell as long as I do not need the money. It is essential for long-term passive investing.

You have also seen that my personal finance routine is entirely manual. I do not automate any of my money things. I think that automating your personal finances is a mistake. I much prefer to be in control.

Conclusion

Here you have it! My 13-step monthly personal finance routine system!

Following this system helps me be very aware of what is going on with my finances. What is good and what is bad? I want to have as much information as possible with my budget. And I want to avoid missing a step. I very rarely make a money mistake with my personal finance routine. And since I do the same steps every month, I save time.

These steps are personal. Of course, not everybody will have the same. However, I believe everyone should have a bit of a personal finance routine. Even with you have only a few steps, it helps to do them regularly and each month.

Enough about me! What about you? Do you have a personal finance routine? How many financial steps do you do each month?

More reading

I Will Teach You To Be Rich – Book Review

I Will Teach You To Be Rich is a book about getting rich by automating your finances and investing. But how good is it really? Let's find out!

My 8 Biggest Budgeting Mistakes – How to fix them!

I have made many budgeting mistakes, learn about them and avoid doing the budgeting mistakes I have done!

Cars are not always bad for finance

Are cars really money pits? I argue why owning a car in Switzerland is not always a financial mistake and how to minimize the costs of driving.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

i’ve seen you on tv and i know how much you earn, not everyone will ever reach that level.

and most of your net worth increase come from that.

don’t you have fear you may be jobless suddenly one day and find no new job for several months/years, outside RAV coverage? i’ve been through that and for personal reasons which i prefer not to disclose i can’t take an aggressive approach on the job market either.

my salary is about 30% lower than yours, no bonuses.

my net worth grows steadily only of about 35k per year and i don’t have a partner.

i think you have a solid approach but on the other hand you’ve been pretty lucky as well :)

It’s true that my income is quite high, I have never hidden that fact. And it’s entirely true that about 95% of our net worth growth is due to savings, not investing.

I am not very afraid about that. In software programming, there currently are a ton of job. And I am quite qualified. But, I would have two years of unemployment benefits if I was laid off and I could live two more years our of our net worth. So, for now, I have enough security.

I would not put that on luck too much. I have studied software programming for more than 10 years, worked countless hours on personal coding projects, read countless books, and experimented with many things. The luck may come from some of my capacity at work, but most of my little success comes from hard work and dedication.

Sorry if I did not express myself clear. With luck I mean that you have chosen the right path (IT) at the right time, like several other people nowadays. I studied a couple of years before you and back then IT was not so in, and today’s salaries were just crazy. What I studied had potential back then but then the market shrunk. Nothing to argue on your experience, compétence, passion, efforts or dedication :-)

Oh, then I get it :) Yes, I am lucky to be passionate about software programming and not something much less lucrative. It’s true, I did not work hard on becoming passionate :)

It’s entirely true that if you are passionate about hairstyling (just an example), you are less likely to have a very high salary than a person passionate about software programming or any other high-paying career.

Congrats to your disciplined approach. I believe that discipline is a big contributor to reaching fi.

I suggest you add an additional step to number 4. It‘s something I did for a few years that helped me on my way: each month you pick one recurring bill (e.g. mobile plan, newspaper subscription, electric bill, …) and you set the goal to lower it as much as you can without reducing the value of what you get. Of course the higher the bill you try to reduce the better but I think that‘s not even the main point. The important thing here is that over time all the improvments on your reccuring costs really add up and are also creating a double effect: you increase your savings and lower your spending target at the same time.

This adds an active element to your budget tracking and by doing it each month you achieve more than just reacting to movements in your spending.

Hi Mark,

Thanks :) I agree that discipline helps a lot :)

This is a good idea! I am doing that with my yearly goals where I have to reduce three bills. I do not think I could reduce one per month, they are pretty well optimized at this time. But it’s a great step to add to a routine indeed!

Do you have a routine yourself?

I broke my routine after a couple of years, there was nothing left to improve :) I guess I could start again since after some time the bills start to increase again.

Yes, it makes sense :)

Hi TPS,

Thanks for the detailed info.

I read that you use a dedicated app, but by any chance is there any spreadsheet that you would recommend for this routine and for the 11 metrics you wrote about on your other article?

Thanks again!

Apologies, by spreadsheet, I meant spreadsheet template

Hi Henry,

I am afraid I do not have such a spreadsheet, no.

It’s on my task list to either provide a template for my readers or to provide access to my dedicated app. In the meantime, I am afraid that you will have to crunch the numbers yourself.

Thanks for stopping by!

Thank you, I look forward to it

Please could you do a post on Mintos?

Hi Doods,

I have written a bit about Mintos in my post about P2P lending in the past. I plan to update this post soon. I may do a full review of Mintos next year if there is enough people interested.

Let me know if you have a specific question.

Thanks for stopping by!

OK, thanks, I will read your P2P lending post.

I am having trouble setting up payment from Revolut to Mintos

I’ve done a number of transfers to Mintos from Revolut without any problems, so it should be possible.

Hi TPS

Do you pay your taxes monthly? The payment slips I get are end of March, June, Sep etc

So its a bit tricky for me, as I have to keep some cash back for future months as well.

Interested to know if you pay on account monthly to make it easier to budget.

Thanks

Hi Gavin,

Yes, I pay my taxes monthly. I am basically paying the taxes for the next year. At the beginning of each year, they compute how much I paid and how much I should have paid and send me a bill with the difference.

I do not pay monthly to make it easier. I am just using the payment slips they are giving me :)

I would not mind paying quarterly. Since it’s not a huge amount of money, you can keep some extra cash at all times for this.

If this is an issue, simply ask the tax office to let you pay monthly instead. This should be possible to arrange.

Thanks for stopping by

I don’t any of that, sounds like too much work! I don’t do any budgeting, hate those :-)

Once a month I spend 10 to 20 minutes by checking and taking note in a gsheet the money I currently have on, separated by item (accountA, accountB, AccountC, Degiro,Etc ETc)

– My several bank accounts

– Retirement funds

– Brokers

– P2P

– Crypto

– Revolut,etc

– Any other financial product

And thats it, did some % calcs on the sheet to see how much it grew from last month, how much each item accounts from total NW, and last column is the best, total NW & % that it grew :)

Over time you start to get an idea on how much you are growing every month which is nice.

I have automated deposits every month to the several financial services, and many are automated inside, if not, just go and buy more stock/fund/ETF etc.

Low hassle and I get most of the benefits, the progress and total NW

Hi Johny,

It sounds like a lot, but it does not take me a lot of time! Except for writing the monthly update, but most people won’t have to do that ;)

I do not really budget, but I think that tracking expenses is really important and I would not want to stop doing it. This is also a good way to see if our expenses are increasing or decreasing. I really like having metrics over time.

I also have metrics on how much my net worth grew from last month, last year, … All this is automated in the budget application, I just have to fill a few things.

As for automation of the deposits. I do not do that. I think automating money is a bad idea.

Thanks a lot for sharing!

I like that you have such a robust monthly routine in place. As for me, I’m embarrassed to say that i don’t have one. It’s been working out for me becuz I “programmed” my brain to naturally spend less, save more and invest systematically. I truly follow these methods here: https://mamabearfinance.com/save-money-without-using-a-budget/

But now that this blog is born, I’m learning a lot from other bloggers like you on how to analyze my traffic trends. It’s still at a young stage so the data is immaterial but I made it a goal to be more pragmatic about monitoring it. By the way, how do you check your power consumption on your hosting site?

Hi Mama Bear,

If you can program your brain enough, you will not need a routine indeed. But having one could still save you some time instead of saving you money :) And time is great!

It’s not really about power consumption (my wording was not great!) but about processor consumption. If you use a host with Cpanel (like SiteGround), they will tell you on the sidebar how much you use these last few hours. That is for shared hosting. If you use a dedicated hosting, you need to connect to the server and check the CPU consumption directly.

Thanks for stopping by!

Coming to this post after reading your top 5 post for 2018 blog, loving all of them!

It’s very good that you’re so systematic going about things, that is something I can learn from, a lot! Saving this article for future reference, as I’m planning to start tracking my budget & goals more closely :)

Hi M @ Radical Fire,

Thanks a lot. I am really happy that my posts are helping people. I am bit crazy about routines, so this is really easy for me. On the other hand, it is more difficult for me to go out of the routine. This is something I need to learn from other people!

Thanks for stopping by!

Thanks for the blog. You are amazingly systematic. Just had a few questions.

What application do you use for budget tracking ?

Also how much time does step 3 to 10 take for you per month ?

Hello Arun :)

Thanks!

I’m using budgetwarrior to track my budget, it’s a very geeky budget application.

It probably takes me around 2 hours per month. That’s a rough estimate, I never really counted my time doing that :)

Thanks for stopping by!

Hey!

Nice to see your routine! I am filling out my Excel sheet every 1st of the Month to track my progress. The Excel looks like this https://ibb.co/jZk6Wd it changed quite a lot since I started 3 years ago. I have some small statistics as well but I am more the numbers guy so I like to look at these hard facts rather than some graphics :-P – By the way I changed the numbers.

From your routine I skip steps 3 and 7 – 11. But to be honest I think I check my Excel file approximately 10 times a month and think about what I could change or do better and what goals are possible.

Cheers,

Mascap

Hi :)

Before I had my application for budget and tracking, I was also using a Google Sheets. I was adding so much formulas to it that it was starting to be a mess. So I changed. But Excel and Google Sheets are very good way of managing budget and net worth!

I also like hard facts, the visualization are more here for the trends and the blog! And for the people I’m discussing my finances with.

Why do you skip 3 ? It is an important step to me.

To be honest, this is only the main routine. I’m checking my budget many times a month too ;) I think it’s natural. I’m also checking my investment account in a regular basis.

Thanks for stopping by and sharing!