DEGIRO vs Interactive Brokers for European Portfolio: Who is cheaper in 2026?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

DEGIRO and Interactive Brokers are great brokers for European investors. But how do they compare exactly? Which one should you choose?

In this article, I compare DEGIRO vs Interactive Brokers in terms of price for a European ETF portfolio. I compare different scenarios that should cover the needs of most long-term investors.

We only compare the costs of both brokers, not the features and usability. If you are interested in the features, I have written reviews of both brokers.

And remember: Investing involves the risk of loss. Always do your research before you invest and know why you invest and what you invest in.

|

Great broker for Europe

|

My top pick

|

|

4.5

|

5.0

|

Our investment portfolios

For this comparison of brokers, we consider two different portfolios.

Since the fees do not change, we are not interested in the exact ETFs used. We are only interested in which exchange you purchase the ETFs.

For a choice of ETFs, I wrote about possible portfolios with European ETFs. To know why we must invest in European ETFs, you can read why we may lose access to superior U.S. ETFs. Swiss investors still have access to US ETFs, but European investors have already lost access.

The first portfolio is for a Swiss investor. This investor has 25% of his portfolio in a Swiss ETF (from the SIX stock exchange). The rest of the portfolio is from a European ETF (from the Euronext Paris stock exchange).

Our second portfolio, for a European investor, is even more straightforward. This investor has 100% of his portfolio in European ETFs (from the Euronext Paris Stock Exchange).

In both cases, each investor only invests once a month in one ETF. It is a perfect way to invest with low fees. Some people are investing every quarter. But it barely reduces fees, and it makes you keep more cash. Investing every month is also an excellent way to build an investment habit. So monthly investments make more sense.

For these two investors, we compare the prices of two brokers: DEGIRO vs Interactive Brokers. These two brokers are among the cheapest available in Europe. But which is more affordable for each scenario?

DEGIRO Fees

First, we study the fees for each service, starting with DEGIRO.

With DEGIRO, you pay a connectivity fee of 2.5 EUR (2.68 CHF) per year and per stock exchange on which you own shares. If you have an ETF on SIX and one on Euronext Paris, you pay 5 EUR per year. However, your local stock exchange is free. So, if you are a Swiss investor, you get SIX for free.

If you convert currency on your account, you pay a fee of 0.25%. It can quickly become expensive once you invest a large amount of money. A currency exchange happens if your base currency is CHF and you buy an ETF in EUR.

The fee system of DEGIRO is pretty simple. Unfortunately, it is slightly different for each country. I wish DEGIRO had the same prices regardless of which country you come from.

A collection of Core ETFs is also cheaper with DEGIRO. It used to be free, but the service fee still applies. You also still have to pay currency exchange fees if necessary, but the other expenses are waived. We do not use that for this comparison since that would significantly restrain our choice. But if you choose ETFs in the core selection, you can make it cheaper.

With DEGIRO, a Swiss investor pays 3 EUR (3 CHF) for each purchase of a Swiss ETF. The price is also the same (3 EUR (3 CHF)) for a European ETF. 2 EUR goes to DEGIRO while the other 1 EUR covers the third-party (the stock exchange) costs.

Now, for the European investor case, I take the example of DEGIRO France. The fees are a bit different from country to country. So, if you are not in France, you can check out the prices on your DEGIRO website.

Interestingly, this investor only pays 2 EUR (2 CHF) for each purchase of a European ETF. DEGIRO gets 1 EUR, and 1 EUR is for the third-party costs. It would be the same price for a Swiss ETF. However, European investors are unlikely to invest in Swiss ETFs. Interestingly, this is significantly cheaper than investing for a Swiss investor.

In the past, another account type was the DEGIRO custody account. But as of 2022, this account is not offered anymore to new customers.

Interactive Brokers Fees

Now, we also have to study the fees for Interactive Brokers. They do not have two account types but have two fee systems: Fixed and Tiered. So we compare these two. Other than the prices, there are no differences between the two pricing systems.

Regardless of where you live, you pay the same fees, which simplifies them a bit. In both cases, there are no custody or inactivity fees!

For both account types, you pay 2 USD (2 CHF) for currency exchange. The Swiss investor must exchange some CHF into EUR to buy European ETFs.

Fixed Pricing

The Interactive Brokers Fixed pricing is straightforward.

For buying an ETF on the Swiss Stock Exchange, you pay 0.05% of the total transaction. The minimum fee is 5 CHF, and there is no maximum fee.

For purchasing an ETF on the European Stock Exchange, you pay 0.05% as well. But the minimum fee is only 3 EUR (2.84 CHF), and there is no maximum.

I assume that you use the Smart Routing orders, which is the default. Only experienced investors should opt for Direct Routing which is more flexible but also more expensive.

Tiered Pricing

The Interactive Brokers Tiered system is more complicated.

First, you must pay some transaction fees to IB for each region. Then, based on the stock exchange, you must pay some extra fees. And they are entirely different based on the exchange.

For buying an ETF on the Swiss Stock Exchange (I took EBS), you pay 0.05% in transaction fees to IB (with a minimum of 1.50 CHF and a maximum of 49 CHF). You then pay a flat fee of 1.5 CHF for the exchange and an exchange fee of 0.015%. On top of that, you pay a 0.38 CHF clearing fee and a 1 CHF trade reporting fee.

For buying an ETF on the European Stock Exchange (Euronext Paris), you pay 0.05% in IB transaction fees with a minimum of 1.25 EUR and a maximum of 29 EUR. You pay a 0.01% exchange fee (with a minimum of 0.8 EUR). And the clearing fee is 0.10 EUR.

We can observe that it is much cheaper to trade on Euronext than on SIX. Switzerland has a reputation for being expensive!

As you can see, this is much more complicated than the Fixed system. But you do not have to worry about this; I do all the math for you!

Swiss Investor

We can start with our Swiss portfolio, with 25% of a Swiss ETF and 75% of a European ETF.

In this case, our example investor invests once every four months in the Swiss ETF and the other months in the European ETF. The Swiss Investor has CHF as its base currency. It means that buying the European ETF incurs a currency conversion.

It is the kind of portfolio that most Swiss invest in. If you do not want a Swiss ETF, skip to the next section for a complete Europe ETF Portfolio. However, the following section uses EUR as a base currency.

We compare DEGIRO vs Interactive Brokers for this Swiss investor for several scenarios.

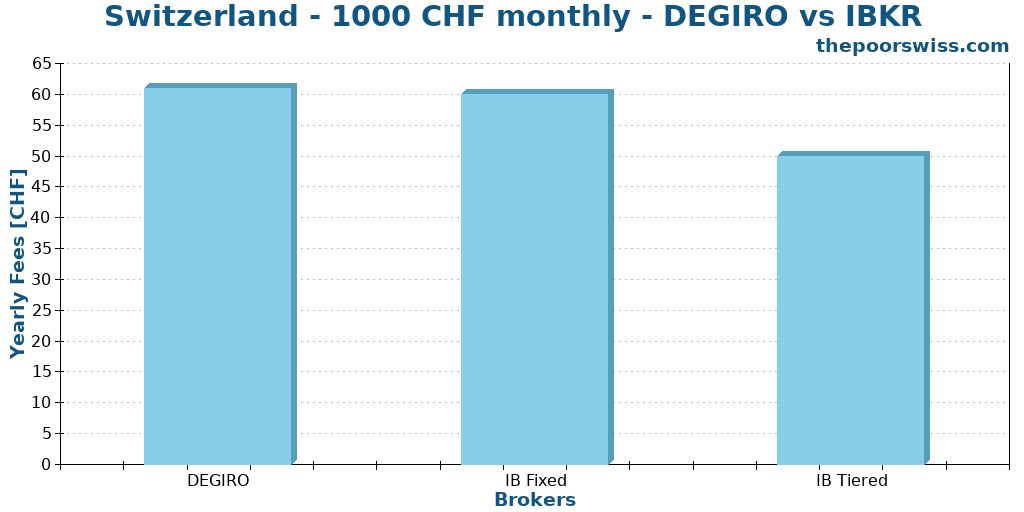

Starting investor

Our first scenario is with a person starting to invest.

The investor begins with 25’000 CHF and invests 1000 CHF every month. It is a typical scenario for someone just investing in the stock market. But this is only an example. There is no problem starting with zero CHF.

Here are the total fees for each broker account:

In this case, Interactive Brokers Tiered and Fixed are slightly cheaper than DEGIRO, but it is not significantly different. We can see that the Tiered pricing of IB is more affordable than Fixed for small investments.

So, in this particular case, Interactive Brokers Fixed and Tiered are the best choices.

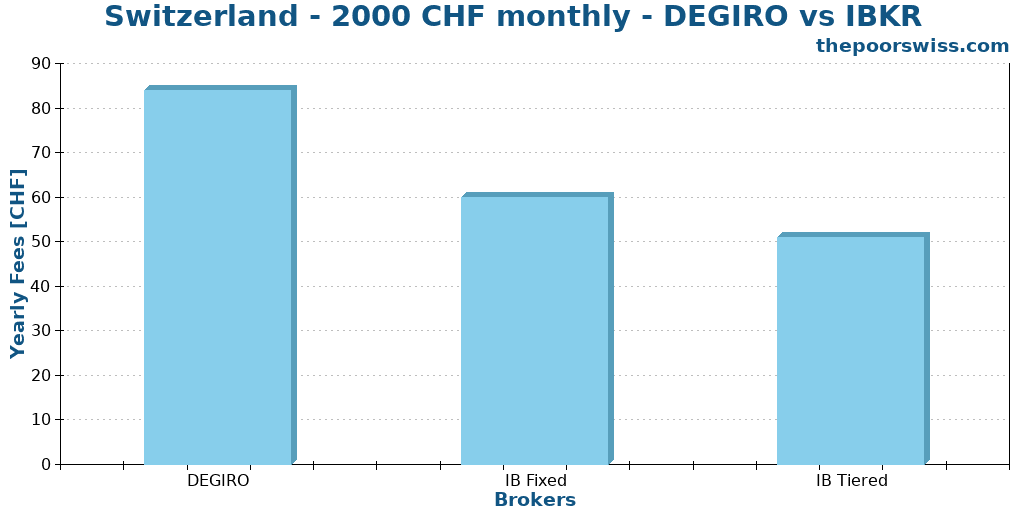

Standard Investor I

For the second scenario, we can take an investor who has 100’000 CHF and invests 2000 CHF monthly. After a few years of investing, this is the state that many investors can reach.

Here are again the total fees for each broker account:

Both Interactive Brokers Tiered accounts are now significantly cheaper than DEGIRO.

So, in this particular case, Interactive Brokers Tiered is the best choice. However, it is only marginally cheaper than Interactive Brokers Fixed. Both are excellent choices for this scenario.

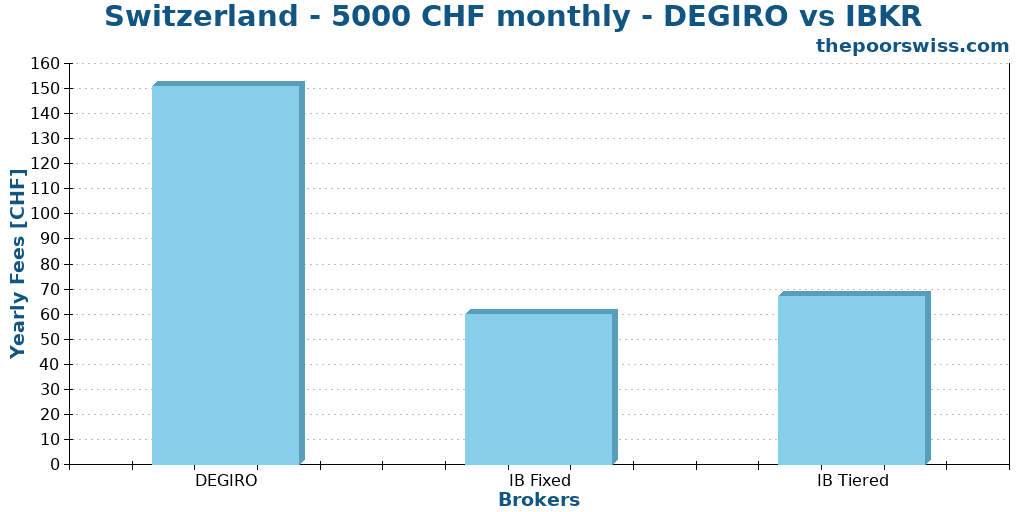

Standard Investor II

Here is what happens if we invest 5000 CHF monthly instead of 2000 CHF. It is still a typical investing case.

This scenario would give us the following totals:

We can see that Interactive Brokers Fixed is the best option here. Interestingly, Fixed is now cheaper than Tiered. And Interactive Brokers is now twice as cheap as DEGIRO.

Once again, in this particular case, Interactive Brokers Tiered would be the best choice.

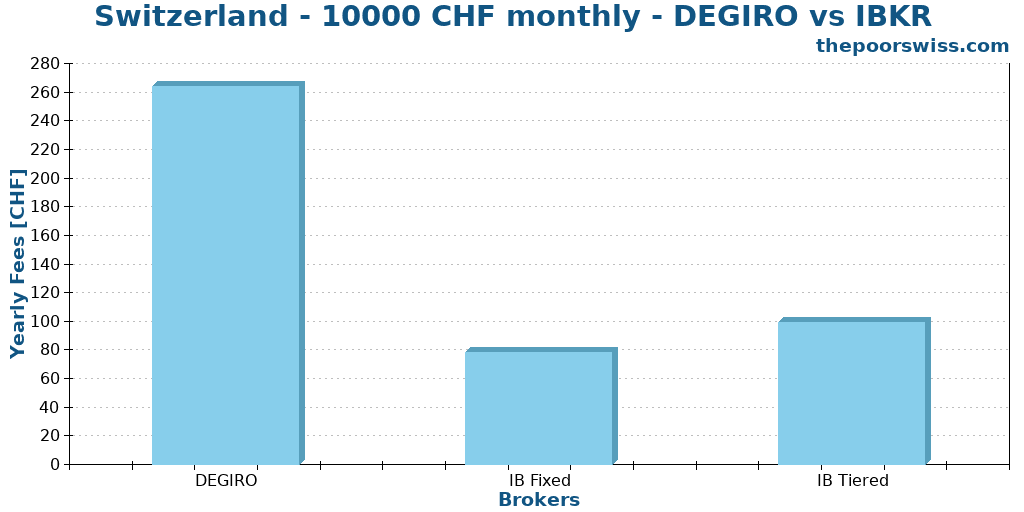

Advanced Investor

We should check the last scenario for our Swiss investor. This time, our investor has 500’000 CHF and is investing 10’000 CHF every month. This scenario is not typical since this is a lot of money. But this is still possible.

We get the following totals from this case:

Not many things have changed in this scenario. We can note that the gaps between the different options are increasing. The Fixed account is still the best option. Tiered is still relatively cheap as well. However, Interactive Brokers is now more than three times cheaper than DEGIRO!

In this case, Interactive Brokers Tiered is the cheapest option.

Conclusion Swiss Investor

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

We can draw several conclusions for Swiss investors:

- Interactive Brokers Tiered is the cheapest account for small investors

- Interactive Brokers Fixed becomes cheaper for the higher amount invested per month.

- The difference between Interactive Brokers Tiered and Interactive Brokers Fixed is relatively small.

- DEGIRO can become several times more expensive than Interactive Brokers

- Most of the fees of DEGIRO come from currency exchanges.

For Swiss investors, I recommend using Interactive Brokers.

It does not mean that DEGIRO is a bad broker for Swiss investors. In the worst scenario, you would pay 264 CHF more per year. This is not a considerable amount. DEGIRO is still a great broker, not just as cheap as IB. If you do not want a broker from the United States, go with DEGIRO!

European Investor

If you live in Europe, you likely have a portfolio with only European ETFs.

In this case, the example investor invests monthly in a European ETF. It is a simple scenario. Since a European investor has euros, there will be no currency conversion in this scenario. It makes a significant difference!

This should be the case for most European Investors except for Swiss investors. It could also be different for people from the United Kingdom since they do not have euros.

Some of the prices from DEGIRO vary from country to country. For this example, I took the prices from France. Interactive Brokers has no difference based on where you come from.

We compare DEGIRO vs Interactive Brokers for the same scenarios for this European investor.

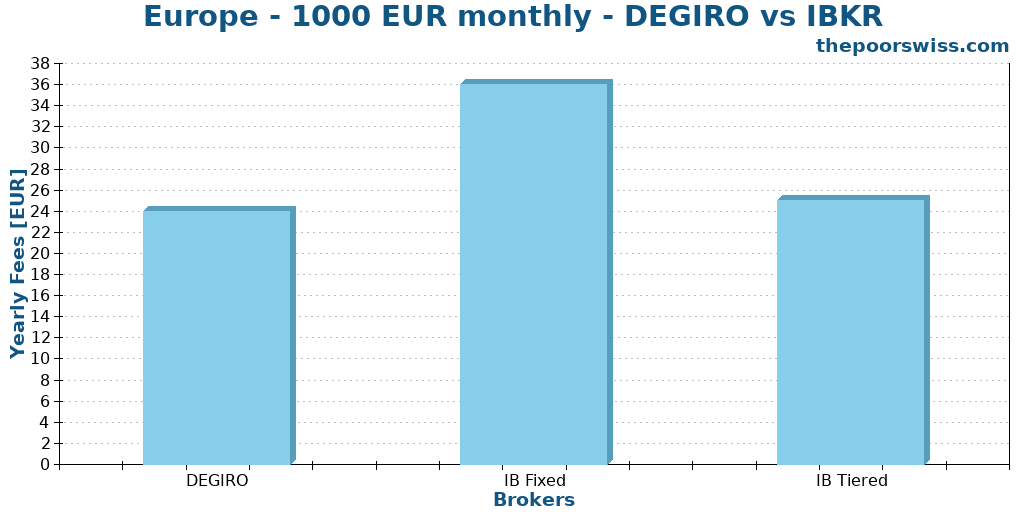

Starting investor

Our first scenario is for a person that is starting to invest. The investor begins with 25’000 EUR and invests 1000 EUR every month. This scenario is typical for a European investor just starting to invest in the stock market.

Here are the total fees for each broker account:

In this case, DEGIRO is very slightly cheaper than Interactive Brokers. But both are affordable in this case. Interactive Brokers Tiered is better than Interactive Brokers Fixed.

So, in this case, DEGIRO is the best option. But IB is also very cheap.

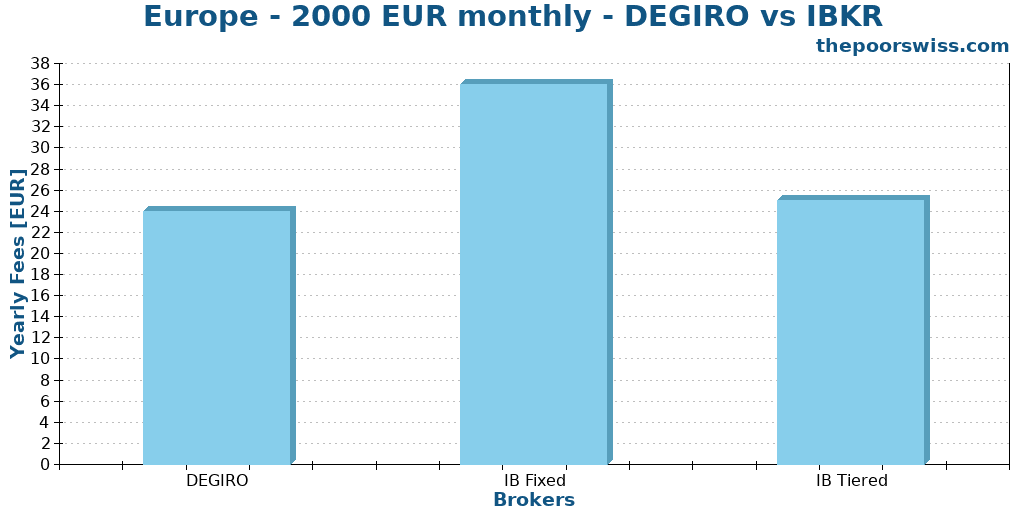

Standard investor I

Our second scenario is with a person in the second stage of investing. The investor already has a portfolio of 100’000 EUR. This standard investor invests 2000 EUR each month.

Here are the total fees for each broker account:

Nothing changed in this scenario. So, in this case, DEGIRO remains the cheapest option by a small margin. But IB is also very cheap.

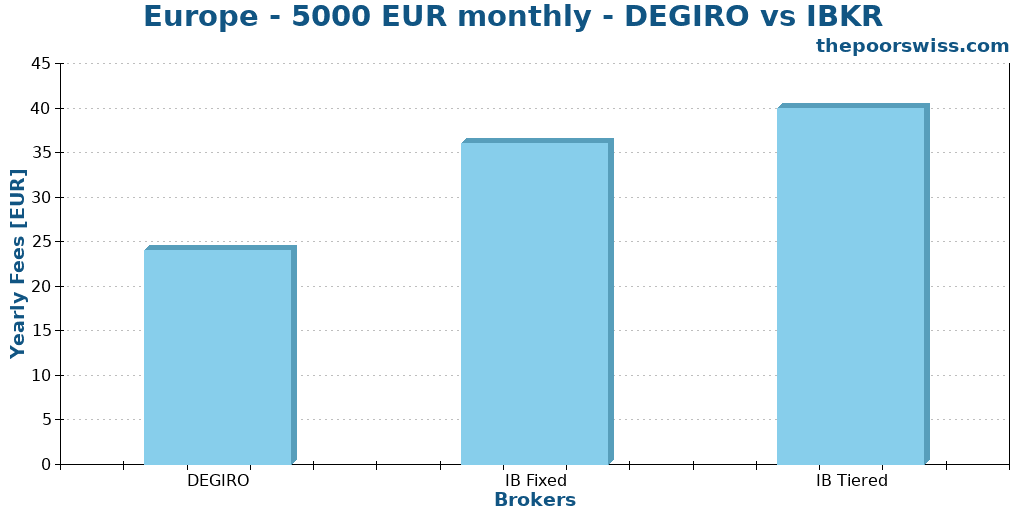

Standard Investor II

Here is what would happen if this standard investor invested 5000 EUR per month instead of 1000 EUR.

This scenario would give us the following fees per broker account:

Now that the investments increase, IB becomes more expensive while the prices for DEGIRO do not change. The gap is starting to be more significant here. Interactive Brokers Fixed is now cheaper than Interactive Brokers Tiered.

For this particular case, DEGIRO is the best option.

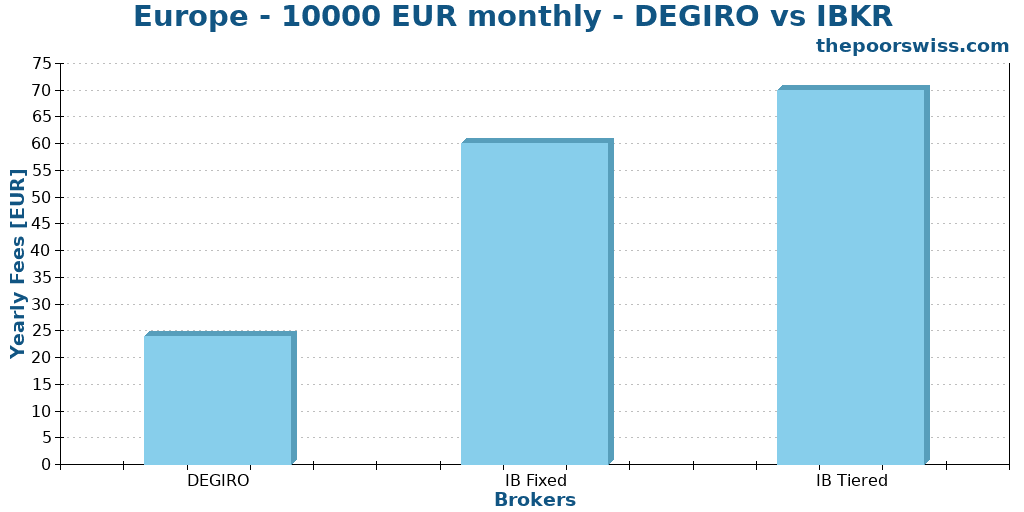

Advanced Investor

Finally, we also check the final scenario for our European investor. Our last investor has 500’000 EUR and is investing 10’000 EUR every month. It is not a typical scenario since this is a lot of money. However, this is still possible for dedicated investors or high-income earners.

Here are the prices for each broker account:

Once again, DEGIRO is the best option, twice cheaper than Interactive Brokers Fixed.

Conclusion European Investor

We can draw several conclusions for European investors:

- DEGIRO is the cheapest account

- Interactive Brokers Tiered is a good option for small investors

- Interactive Brokers Fixed is a good option for investors with more money

- Investing without currency exchanges can save a lot of money.

Most European Investors should go with DEGIRO.

One advantage of IB is that you can move from country to country without changing your account to a new entity. With DEGIRO, the entity you use depends on where you live. So, if you move abroad, you may have to switch your account, which is not free. So, if you plan to move abroad or be a nomad, I recommend Interactive Brokers.

Conclusion – DEGIRO vs Interactive Brokers

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

There you have it! We now know the cheaper option between DEGIRO vs Interactive Brokers for several scenarios. Interestingly, both broker accounts are competitive. There is no bad option between these two brokers.

We can draw some conclusions from this comparison:

- For a Swiss Investor, Interactive Brokers Tiered should be the most affordable broker unless you invest a lot, in which Interactive Brokers Fixed becomes interesting.

- DEGIRO should be the most affordable broker option for a European investor.

- There is very little difference in prices between DEGIRO and Interactive Brokers. Both brokers are very affordable.

So which should you choose? Swiss investors should probably go with Interactive Brokers Account. If they do not want a US broker, they should go with DEGIRO.

European investors, on the other hand, should probably go with DEGIRO. It is significantly cheaper for beginner investors.

If you need further instructions on these brokers, you can read my reviews:

What about you? Which broker do you use?

More reading

Neon Invest vs Swissquote 2026 – Which is the best broker?

Neon Invest vs Swissquote. We compare the fees, ETF limits, and features to help you choose between the low-cost app and the established bank.

Step-by-Step Guide: How to buy an ETF with Swissquote in 2026

All you need to know about buying ETFs and converting currencies on Swissquote. This guide will make your experience straightforward.

How does cash settle with Interactive Brokers?

Where is my money? Learn how cash settlement works at Interactive Brokers (T+2) and why you cannot withdraw your funds immediately after selling.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi, I am in Switzerland at the moment but will be moving to Italy middle of next year. If I were to open an account now with IBKR do you know what would happen when I move? Would I just be able to transfer the same account across without closing and opening up a new one? And regarding funds, can I invest in Euro-denominated UCITS EU funds while in Switzerland on IBKR? If so then when I move country next year that should mean I don’t have to sell and re-buy the funds?

Thanks

Hi Luca,

I don’t know for sure, but I would expect you would be able to change your address, likely having to provide proof. You will have to ask the support to make sure, but as long as you use an entity that is available in both countries, that should be fine.

You can invest in UCITS fund while in Switzerland.

Hi Babtiste,

First of all, thank you for your review and the work you are doing with your blog. It has so much useful information, it is almost hard to believe. I have recently moved to CH and I have Degiro account. Would you know if I have to sell all my US ETFs or it is that I just can not invest in them moving forward?

Thank you beforehand

Hi Nastia,

Normally you don’t have to sell US ETFs. The rules for DEGIRO are the same in the entire EU I believe and they applied the same rule (unnecessary, but they did it anyway) to Switzerland.

Thank you Babtiste!

Hi Baptiste,

Thanks for the great work as usual. In the past you suggested CHSPI as swiss etf and VT as us etf. Having still Euros lying in an old account, what etf EUR based could you recommend?

Hi Andrea,

If you are using IB, currency conversions are very cheap (2 USD), so I would not choose ETFs based on the currency you have but based on the best available ETF.

Hello,

Me again. I’m interested to know your opinion on the following.

After my bills and savings for tax etc, I will have approx. 1,000CHF per month to invest, this is in addition to the money I pay into my 3a each month (In the process of moving from UBS to Finpension, 100% global).

I’m keen to achieve the 80/20 split for international exposure and home bias however, when investing a relatively modest amount, the commission is going to be proportionally much larger (2*shares in CHSPI= 272CHF+ between 1.5 and 3CHF of commission (I believe the commission would be approximately the same for 20 of the same shares?)) this would add up over the course of a year if I did the same purchase each month.

In this case would I be better off doing the following, every month for 3 months, buying exclusively VT. Then in month 4 buying only CHSPI?

Or is it indeed the case that I shouldn’t be too concerned about the commission as above?

Thanks,

Jordan.

OR indeed (just had a thought but not sure if it’s stupid), choose the Finpension 3a Switzerland 100 and only use IB to purchase VT? Then I will have home bias/ exposure in my pillar 3a and international exposure in IB.

Your thoughts are much appreciated!

Thanks.

That’s another good strategy. You should always consider the big picture. If you want an 80/20 split and have your 3a only in Swiss stocks, you will need to have a portfolio at IB four times larger than your 3a. It may be slightly more difficult to keep a balance that way, but that’s a good strategy as well.

Hi jordan,

You are right that investing a few shares in the Swiss stock exchange is relatively expensive. It would be slightly more expensive for 20 shares, but only slightly so.

You should do a rotation of 5 months (20% each = 80/20) and not four months (25% each = 75/25), but that’s exactly what I would do: buy VT, VT, VT, VT, CHSPI. I think it’s a great strategy to buy a single ETF each month.

Thanks for this review! I lived in Germany until last year and I was using DEGIRO. Now I am living in Switzerland and want to open an IB account. I still have a lot of expenses in EUR and I wanted to ask about using IB as an exchange. Can I deposit CH to my IB account, exchange them for EUR and then send them to my EUR account? Thoughts?

Hi Daniel,

Yes, you can as long as your EUR account is in your own name.

Shouldnt you take into account the stock lending program revenue for IB?

Degiro forces you to lend stocks and does not share the revenue if you do not take the custodity account.

Anyone has a answer?

Hi

That’s a good point. However, it’s very difficult to estimate how much you are going to make with the SYEP from IB. I did about 3-5 USD per month on my portfolio when I tried it. It would offset the costs of IB compared to DEGIRO, but how much will highly depend on the stocks you have.

Hi Baptiste,

Why don’t you convert CHF to USD/EUR BEFORE you send it to IB? For ex. I convert CHF to USD with my Revolut account and then send USD directly from Revolut to trade with US ETFs

Hi,

Conversion is MUCH cheaper on IB than on Revolut when you send significant amounts per month. If I convert 10’000 CHF to USD on IB, it cost me 2 USD. I would pay 50 USD with Revolut.

Thanks for the excellent article.

As for the the Custody account – is it still possible to open one? Anyone had some luck recently?

I tried it a few weeks ago, but during registration it gives me no option, only the free Basic account (and its derivatives). I also sound some info on the internet that the Custody accounts are no longer being offered to new clients (people who already got them get to keep them).

Hi Veja,

You are right, they have removed the Custody account since late last year it seems. This is weird. There are still several references in the doc about the custody account, but it seems like not available anymore. And there has been no communications by DEGIRO about this.

I will update my DEGIRO articles to reflect that.

Hey man!

Excellent blog my friend. Thanks a ton for all this info. That really helped a lot! Can I leave a tip, you really deserve it.

What I wanted to annotate is that the fixed pricing on interactive brokers has changed. It is not at 0.10% anymore but at a rate of 0.05%.

https://www.interactivebrokers.co.uk/en/index.php?f=39753&p=stocks1

I understand that all these changes constantly happening make this stuff nightmareish to maintina. Still, it would be great if you could update the article for the ones coming after me.

Hi Andreas

Currently, there is no way to give me a tip, but thanks :)

I just took a look at the updated fees and It’s actually more complicated than you outline. The new fixed fees are only with IB SmartRouting. And the fee is 5 CHF for trades up to CHF 10,000. So below 5000 CHF, it’s actually more expensive than before.

I will have to look at what SmartRouting exactly entails. But once I do, I will plan another update of this article, which is indeed a nightmare to update.

Hi just a comment, how can it be more expensive than before? If before there was a 0.1% fee with min of 10CHF and now its 0.05% fee with min of 5CHF.

Before at 5000 CHF you would pay 10CHF, now 5CHF.

However, if you go down to Switzerland, then the price becomes 6CHF and 0.1% if its “direct routed order”… This is getting complicated.

I can tell you that my account is set to fixed and all things I have tested seem to be at 0.05%.

I have changed my account to tiered to see If i can do some comparisons (since the best way is to really do some buy order tests). However, even though I did the change and the web shows I have tiered, it seems to not apply (maybe it takes some more time?).

Kind regards,

Richard

Thanks, Richard! I forgot about the min 10 CHF fee ;)

You are right, it’s always cheaper now!

Hi, no problem!

The only thing I dont know what to do now is….

– Pay high fees and worse TERs for EU ETFS

– Buy the superior US-ETFs..

After reading numerous of your (and mustachian) blog posts I can not still be convinced of what is the best.

– Is it even legal? Can we have problems?

– What happens if you own those ETFs and rules change?

By the way, thanks for this very useful blog!

hi Richard,

We should not pay these fees too much. I recommend using US ETFs for the most part and a Swiss ETF for the home bias.

It’s still allowed at IB and legal :)

I have an article about US ETFs.

If the rules change, we just won’t be permitted to buy more, but we will keep our shares and only be able to sell them.

Hi, I saw that in your example you have different options with the starting value and then monthly investments. Would it be a good idea to start investing even if we start with 0 chf deposit and then 200 chf per month? Or is it not worth it? Sorry for the beginner question. Thank you

Hi Kennyster

I believe it’s always interesting to start investing. But it’s true that the fees of both DEGIRO and IB will not be that great if you invest only 200 CHF per month.

Maybe to invest 200 CHF per month, a Robo-advisor is slightly better. On the other hand, with IB, you have no minimum, while most Robo-advisors services in Switzerland have a minimum.

Thank you a lot for the explaining! Do you know if would be a better choice Raiffeisen Rio over IB? I mean as I understood, with IB the fixed fee of 10 chf in case of low investments for each month has dropped. So why should not be good to use IB? Is it because the ~4 chf over 200 chf? Many thanks and sorry for the beginner question

I have not yet reviewed Raiffeisen Rio, so I can’t speak of that one particularly.

But regarding robo-advisors against IB, it’s indeed about transaction fees, especially on CH ETFs. If you purchase 200 CHF of a CH ETF, you will pay about a 3 CHF fee, which is 1.5%. On the other hand, with a US ETF, you will pay 0.35 USD fee which is a good fee even on that amount.

So, even with 200 CHF, I would recommend investing with IB, but only in US ETFs and start using CH ETFs once you have more per month. For CH ETFs to make sense, we should either not invest monthly or invest about 500 CHF monthly I would say.