US ETFs are the best ETFs for Swiss investors

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

I mostly invest in US ETFs, and I have recommended these ETFs many times on this blog. I consider US ETFs to be the best available ETFs. I have talked several times about what makes them great in various articles. But since I still get many questions, I will go into all the details of these US ETFs.

I am talking about Exchanged Traded Funds (ETFs) that invest in the United States. I talk specifically about ETFs from the United States. What matters here is the domicile of the ETF. This is more important than many people realize.

So, here is what makes these US ETFs great.

Availability of US ETFs

First, we need to address the issue of the availability of US ETFs, or lack thereof.

If you are in the United States, you will not have any issues. However, if you are in Europe, this is another story. Indeed, due to European regulations, many countries lost access to US ETFs.

In fact, in 2018, all the countries part of the European Union lost access to US ETFs. This is due to the PRIIPS regulations. These regulations are part of a bigger package known as MiFID II. These laws force the fund providers to provide a Key Investor Document (KID) in the investor’s language. And so far, US fund providers have not provided them, and they are unlikely to do it. So, for now, European investors cannot invest in US ETFs.

In theory, these laws protect investors by providing them more information on the instruments they are using. However, in practice, they are only here to force people to invest in European funds.

However, Switzerland is not part of the European Union. Therefore, Swiss investors still have access to US ETFs. However, this may change when the Swiss equivalent of the European laws enters into effect. Now, it is not entirely clear if this will apply to foreign brokers (like Interactive Brokers) or not. But for now, we are free to use these ETFs.

I believe these restrictions will not apply to execution-only brokers like Interactive Brokers. So, they should still be available in the future.

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Furthermore, not every broker provides us with access to these ETFs, even though they could do it by law. For now, only foreign brokers, like Interactive Brokers, give access to these ETFs. This is good since Interactive Brokers is the best broker for Swiss investors.

If you want more information on these regulations, you can read my article on the availability of US ETFs.

US ETFs have lower fees

The first advantage of US ETFs is that they have lower fees than their European alternatives.

What matters to us is the Total Expense Ratio (TER) of the ETFs. The TER is the total fee you pay for holding the money. This fee is expressed in percentage and is removed from your money over the year. So, if you have a TER of 0.1% and 100,000 CHF in the fund, you will lose 100 CHF each year to fees.

Since you will pay the fees each year, it is important to optimize them. If you are a passive investor, ongoing fees are the most important cost you can optimize. So, it is important to do it well. And the more money you have in the funds, the more fees you will pay.

We can compare a few ETFs to see the difference in fees:

- Vanguard S&P 500: The US ETF (VOO) has a TER of 0.03%, while the European ETF (VUSA) has a TER of 0.07%, twice as expensive

- Vanguard World: The US ETF (VT) has a TER of 0.06%, while the European ETF (VWRL) has a TER of 0.14%, more than two times more expensive

- iShares S&P 500: The US ETF (IVV) has a TER of 0.03%, while the European ETF (IUSA) has a TER of 0.07%, twice as expensive

- iShares World: The US ETF (URTH) has a TER of 0.24%, while the European ETF (IWRD) has a TER of 0.50%, twice as expensive

As you can see, the TER of European funds is significantly higher than US ETFs. Over the long term, this will make a significant difference in your returns.

When you are investing in ETFs, investing fees are not to be ignored. And this is especially true if you want to retire early based on your portfolio.

US ETFs are more tax-efficient

The second advantage is even more significant, but it is also a bit more complicated and is only for Swiss investors. Indeed, US ETFs are more tax-efficient for Swiss investors.

This tax efficiency is based on the way dividends are taxed. Especially how the US taxes dividends of US companies.

By default, the US government will tax 30% of the dividends emitted by US companies to foreign investors. Now, Switzerland has a tax treaty that reduces this withholding to 15% for Swiss investors, the same amount withheld for US investors. And moreover, we can reclaim the 15% left on our tax declaration.

But when we use an ETF in Europe, the dividends will be withheld before reaching the fund. For instance, if you invest in an ETF from Ireland with Coca-Cola shares, you will lose 15% of these dividends directly. But if these dividends are paid to a US fund, there is no loss!

This advantage is essential since US stocks make up 50% of the entire world stock market. Saving on the dividends of these stocks is very important.

The second-best domicile for ETFs after the US is Ireland. So, if you do not have access to US ETFs, Ireland (IE) ETFs are the next best thing.

Overall, how much you save will depend on the yield of the ETFs you are using. For a 2% yield, you will save 15% of 2%, which is 0.3%. So, by using US ETFs, you can save up to 0.3% in fees every year! On a 100’000 CHF portfolio, you can save 300 CHF per year!

However, it is critical to know that this deduction can only be claimed when it reaches 100 CHF. Below 100 CHF, taxes will reject this deduction. So you will need about 33’000 CHF in US ETFs before you can claim it.

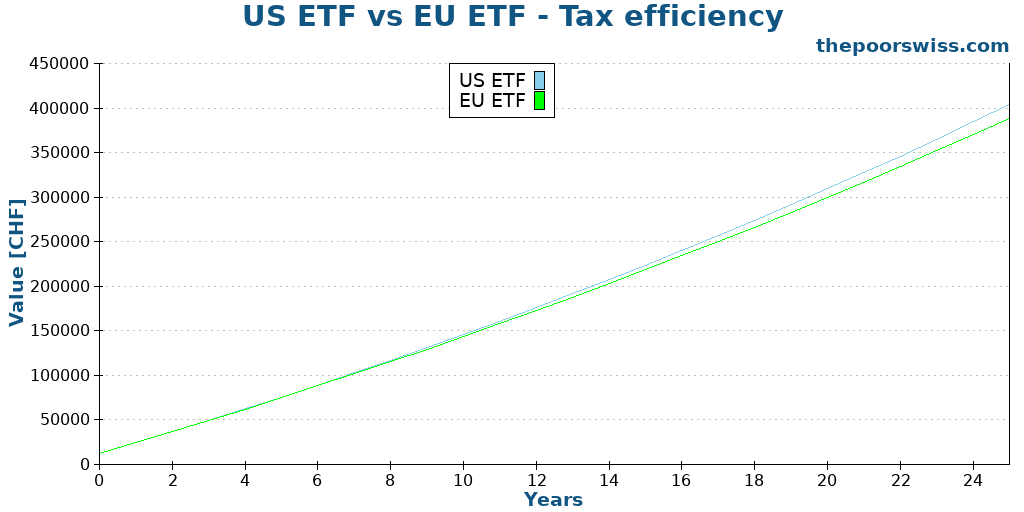

If you are wondering whether this is significant, you can take a look at the following graph. In this example, we are investing 1000 CHF per month over 25 years and the only difference is that we lose 15% of the dividends with

US ETFs are larger

A small advantage is that US ETFs are larger and more liquid. By large, I mean that they are managing more money. Generally, this is exposed as the Assets Under Management (AUM) metric.

A larger ETF has a few advantages over a smaller one:

- It shows more popularity. Larger funds are generally large because they are very popular (people put their money in them).

- It has a lower chance of being closed.

- A larger ETF has a higher trading volume. This has the advantage of the ETF being easier to sell. Generally, they also have a lower spread, which gives you better buying and selling prices.

- A larger ETF can better replicate the index since it will include more small companies than a smaller ETF.

For these reasons, large ETFs are generally better than small ETFs. But this should not be the primary argument in choosing an ETF.

US ETFs are cheaper to trade

The last advantage is that US ETFs are cheaper to trade (with a good broker) than European ETFs.

This is not directly due to the fund itself, but rather to the stock exchange they use.

For instance, my primary ETF, Vanguard Total World (VT), is traded on the New York Stock Exchange (NYSE). To buy or sell shares with Interactive Brokers costs me about 0.35 USD. I can buy many shares and still pay less than a dollar for the transaction.

On the other hand, buying 10’000 CHF of my Swiss ETF, iShares Core SPI ETF (CHSPI) on the Swiss Stock Exchange (SWX), cost me 10 CHF! That is about 30 times more expensive than my US ETFs.

And European ETFs are about in the middle of Swiss ETFs and US ETFs. To my knowledge, US ETFs are the cheapest to trade. Now, this may change if you use a service with free transactions. But there are very few good services like this available in Switzerland yet.

Risks: What about the US Estate Tax?

Many believe we should not invest in US ETFs because of the US Estate Tax. And in some cases, this is true. But in practice, for Swiss investors, there is almost no extra risk in investing in US ETFs.

The US estate tax law states that the inheritance of US ETFs is subject to a 40% inheritance tax. Nonresident aliens (basically, foreigners outside the United States) are exempted from this tax for assets up to 60,000 USD. After this, foreigners will have to pay a 40% tax.

This means that if you have many US assets, they could lose much value when you pass away, and your assets go through inheritance. You do not want this to happen to your estate.

However, many people miss that Switzerland has an estate tax treaty with the United States. And this treaty greatly increases the part exempted from this estate tax!

With this estate tax treaty, Swiss investors are exempted from the US estate tax for up to 11.18 million dollars, prorated to the proportion of US assets in your net worth. For instance, if US ETFs represent 10% of your estate, 1.118 million dollars (10% * 11.18 million) will be exempted from US Estate Tax!

So, in most cases, Swiss investors do not have to worry about the US estate tax! However, it is true that it may complicate your estate. If you have US ETFs, you will need to deal with the IRS.

If you want all the details and many more examples, you can read my in-depth article about the US Estate Tax law. This article also explains how to deal with US estate tax, in the specific case of Interactive Brokers.

What if you cannot use US ETFs?

Unfortunately, many people do not have access to these great US ETFs.

For these people, investing in European ETFs is still an excellent option. Using US ETFs is the best way to invest. However, it is an optimization over European ETFs. There is nothing wrong with investing in European ETFs!

If you want to be optimal, you must go with US ETFs. Now, it could be difficult (or even impossible) to use these ETFs. Even for Swiss investors, few brokers let us access them. If you do not want to go the extra mile and want to invest in good ETFs with lower effort, European ETFs are great!

What matters most is investing, not investing optimally!

What about mutual funds?

In this article, I have talked very specifically about US ETFs, but what about funds?

US mutual funds are also great. But it is interesting to know that Swiss mutual funds can also save you dividends. Indeed, funds are very different from ETFs in how they are held.

With a fund, each investor goes indirectly. With an ETF, you go through a broker who holds the shares in your name.

This allows the fund to be more efficient, directly depending on the treaty. So, a Swiss-domiciled mutual fund is as tax-efficient as a US-domiciled ETF. Of course, the Swiss mutual funds will likely have some other disadvantages (smaller and more expensive, mostly), but it is good to know that the main tax disadvantage of European ETFs is not present in Swiss mutual funds.

Conclusion

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

As you can see, there are many strong reasons to invest in US ETFs instead of European ETFs! These ETFs will let you save a significant amount of money in fees and taxes.

80% of my portfolio is invested in Vanguard Total World (VT), a US ETF. The rest is invested in a Swiss ETF for my home bias portion. So, I invest a considerable portion of my money into US ETFs. This is because I consider these ETFs to be the best available for Swiss investors.

However, these ETFs are more difficult to use. Investors from the European Union cannot invest in them anymore, and in Switzerland, only a few brokers let you use them.

As I mentioned, US ETFs are an optimization over European ETFs, but they are not a revolution. If you cannot (or do not want to) invest in US ETFs, investing in European ETFs will be a great way to invest!

If you want to start trading US ETFs, I recommend using Interactive Brokers. It is an excellent broker that lets you trade US ETFs with very low transaction fees. I have a guide on investing with Interactive Brokers.

Are you investing in US ETFs?

More reading

Think and Grow Rich – Book Review

Think and Grow Rich will help you on your way to success and wealth. Learn how to master your emotions and fears to reach your goals.

The Complete Guide to Asset Allocation

Stocks vs Bonds. Learn what asset allocation is, why it determines 90% of your investment returns, and how to choose the right mix for your goals.

Protect yourself from a recession – Be prepared for the worst!

Prepare for a crash. Discover practical strategies to protect your finances and portfolio during a recession and come out stronger on the other side.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi ,

I read in one of your blogs on which broker to choose and I remember when it came to some brokers that were only dealing in USD , you mentioned that it doesn’t make sense to hold in usd as currency conversion will offset gains or isn’t that desirable – so only invest using those platforms if you have USD lying around , so I’m confused in terms of investing in US ETFs would be in USD and you’d have to convert being a Swiss.

Are you saying or considering that we convert every time or are you referring brokers that let you hold in chf but still convert @ the time of purchase or are these etfs being sold in chf ? ( last one is wrong I guess )

If you could shed some light there it’d be great !

I have account with etoro- and now opened recently with Degiro.

Thanks a lot

Hi ATS

If you need to transfer CHF, you should not use a broker that does not handle CHF, like eToro, because every deposit you do would cost you mmoney.

With IB, you can transfer CHF and then either use it in CHF or convert it (for onyl 2 USD) to USD to buy US ETFs.

I send mostly CHF to IB, convert it to USD for a very small fee at an excellent rate and then buy US ETFs.

Thanks for the great article Baptiste!

“Swiss investors are exempted from the U.S. estate for up to 11.18 million dollars”: Do you know how a “Swiss investors” is defined in this context? Is it a Swiss citizen? A Swiss tax resident? Does it depend on the location or citizenship of the beneficiary?

Cheers & thank you very much

Hi Berni,

I don’t think the citizenship matters. What matters is residence and exclusive tax-paying. You must be living in Switzerland and paying taxes solely in Switzerland.

Thanks Baptiste!

Do you mean the “residence and exclusive tax-paying” of the deceased or the heir?

cheers & thanks :)

Of the deceased. But I would imagine that the residence of the heirs also matters. In my case, I assume both the deceased and heirs are in Switzerland since this is what interests us in this article.

ack, thanks Baptiste! :)

Hi Baptiste,

Thanks for the article, I’ve been investing in IB for the last few months and received my first dividends this month from SCHD and VT.

I filled out the W8-BEN form on interactive brokers but when I download my dividend report I see the following:

Ex Date Quantity Tax Fee Gross Rate Gross Amount Net Amount Code

Starting Dividend Accruals in CHF 0.00

Stocks

USD

Symbol Date Ex Date Pay Date Qty Tax Fee Gross Rate Gross Net Code

SCHD 2023-09-19 2023-09-20 2023-09-25 237 46.54 0.00 0.65 155.12 108.58 Po

SCHD 2023-09-25 2023-09-20 2023-09-25 237 -46.54 0.00 0.65 -155.12 -108.58 Re

I don’t know if its legible, but basically it seems I’ve been withheld 35% (“gross rate” (1-0.35)). But actually its 30%=46.54/155.12.

In any case I was expecting this to be 15%, do you have any idea why its not? Thanks!

Jaime

Hi Baptiste,

I cried wolf too early! I spoke to customer support in Interactive brokers, and apparently it had something to do with a US indicia check… Anyway they checked and all is good, they will do a reversal of the 30% WHT and apply a reduced rate!

Good to hear that :)

Hi,

I don’t know what the 0.65 there. But it seems indeed that you have been withheld 30%. Did you fill the W8-BEN before the dividend was received? Maybe it’s a timing issue and it must be before the ex-dividend date.

Hi Baptiste,

Great post and your overall website is outstandingly helpful. I recently stumbled upon it and now reading regularly.

Questions- 1) Why do you have the main ETF as Vanguard Total World (VT), and not the Vanguard S&P 500 VOO? It has much better returns with all other parameters similar. Am I missing something?

2) I thought in Switzerland, it doesn’t make a difference from tax perspective whether it’s accumulating or distributive? Rather Distributive may be cleaner as you will know exactly how much dividend to declare in tax returns?

I am a B permit holder in Switzerland, and just opened an IB account to make my first investment in ETFs using US ETFs. But just getting a bit confused on the above aspects. Thanks very much !

Hi,

1) VT covers the entire world while VOO only covers the US.

2) Correct. Tax-efficiency is the same but distributing ETFs are more convenient for me since I can do what I want with the dividends and it makes more sense to fill up the tax declaration.

Thanks for your interesting blog, Baptiste! I am a former Swiss citizen, but now living in Italy. What I find puzzling though, is that you say that EU-based citizens will not be given access on the IBKR platform to US ETFs. So does that not deprive the main reason for them to use IBKR?

Hi Enrico

It’s not IBKR blocking US ETFs, it’s the law. Any broker should block access to US ETFs for EU residents.

So, IBKR is still a great broker with a lot of features and fair prices, so should be a good candidate for EU residents as well.

Hi, thank you for the great article. I am a Swiss resident and have an Interactive Brokers account. The Swiss tax authority have refused to refund the 15% withholding tax on my US ETF dividends. My tax advisor says that Switzerland only does this if the bank holding your account is a Swiss bank. I think in the case of my interactive brokers account it is a UK bank. Does this sound correct to you, or should I dispute this with the tax authority? Many thanks!

Hi Paul,

That’s weird. What is the reason the tax authorities gave you? I know there are some limits (you need to reach a minimum of 100 USD I believe and sometimes there are some other limits based on mortgage interests).

I don’t think this is correct, but you should make sure this is the proper reason. I know many people got back the 15% as a DA-1 when using IB.

Hi Baptiste,

First of all, many thanks for the great blog.

In the post, you talked about “Swiss” investors. Does the tax treaty apply for the non-Swiss residents of Switzerland as well? I am not a member of EU if this matters.

Best,

Kaan

Hi Kaan,

Yes, it applies to Swiss residents who pay their taxes in Switzerland, not only Swiss citizens.

Hi Baptiste,

I don’t if I read it on your blog or somewhere else, but remember advice, that as Swiss residents investing in US ETFs we shouldn’t choose ETF focused on high dividends (like Vanguard VYM), because we don’t pay taxes on capital gains, but we pay them on dividends.

Did I state it properly? Do you agree, that we should avoid dividend-focused ETFs?

Cheers

Maciej

What is also still not clear for me is the final taxation on dividends:

1. US puts 15% withheld (special deal with Switzerland) which you can fully take back.

2. Does Switzerland from its side put 35% tax on the dividends of US ETFs? And these you cannot take back?

If the second point is true, then I understand why we shouldn’t focus on dividend-ETFs. 35% taxation is crazy high.

Cheers

Maciej

For your second point, this is actually doubly wrong.

a) This 35% is whitholding only. This means that this counts towards your already paid taxes.

b) There is no extra withholding on US ETFs dividends. However, you will be taxed as income, like any other dividend in Switzerland.

Hi Maciej,

You stated it properly, but it’s not only for US ETFs, it’s for any stock and ETFs with dividends.

It makes little sense to focus on dividends in Switzerland compared to focus on capital gains.

Hi Baptiste,

Like Jakub, I am a currently a permit B holder. Do I have to declare my investments at the end of the year (I have them with a foreign broker)? My total income is lower than 120K per year.

On a completely different matter, do the 35% swiss withholding tax on dividends apply only through swiss banks/brokers or to all people resident in Switzerland even though they invest with a foreign broker?

Thank you.

Hi John,

Normally not. If you don’t have to do a full tax declaration, you don’t have to declare all the assets.

I believe the withholding should be done with any broker as long as you are eligible to taxes in Switzerland.

Hi Baptiste,

First of all, many thanks for all your work, this blog is amazing!

I was going thourgh different sections and comments to find and answer but could not find it so I thought I will ask myself ;)

I am currently permit B holder, taxed at source, bascailly on the verge of exceeding the limit 120k per year. Do you know how I can claim those 15% tax from dividens if I am not submitting my tax return the same way as Permit C and Swiss passport holders?

Hi Jakub

Thanks for your kind words.

Unfortunately, you can’t get these back if you don’t do a full tax declaration.