US ETFs are the best ETFs for Swiss investors

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

I mostly invest in US ETFs, and I have recommended these ETFs many times on this blog. I consider US ETFs to be the best available ETFs. I have talked several times about what makes them great in various articles. But since I still get many questions, I will go into all the details of these US ETFs.

I am talking about Exchanged Traded Funds (ETFs) that invest in the United States. I talk specifically about ETFs from the United States. What matters here is the domicile of the ETF. This is more important than many people realize.

So, here is what makes these US ETFs great.

Availability of US ETFs

First, we need to address the issue of the availability of US ETFs, or lack thereof.

If you are in the United States, you will not have any issues. However, if you are in Europe, this is another story. Indeed, due to European regulations, many countries lost access to US ETFs.

In fact, in 2018, all the countries part of the European Union lost access to US ETFs. This is due to the PRIIPS regulations. These regulations are part of a bigger package known as MiFID II. These laws force the fund providers to provide a Key Investor Document (KID) in the investor’s language. And so far, US fund providers have not provided them, and they are unlikely to do it. So, for now, European investors cannot invest in US ETFs.

In theory, these laws protect investors by providing them more information on the instruments they are using. However, in practice, they are only here to force people to invest in European funds.

However, Switzerland is not part of the European Union. Therefore, Swiss investors still have access to US ETFs. However, this may change when the Swiss equivalent of the European laws enters into effect. Now, it is not entirely clear if this will apply to foreign brokers (like Interactive Brokers) or not. But for now, we are free to use these ETFs.

I believe these restrictions will not apply to execution-only brokers like Interactive Brokers. So, they should still be available in the future.

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Furthermore, not every broker provides us with access to these ETFs, even though they could do it by law. For now, only foreign brokers, like Interactive Brokers, give access to these ETFs. This is good since Interactive Brokers is the best broker for Swiss investors.

If you want more information on these regulations, you can read my article on the availability of US ETFs.

US ETFs have lower fees

The first advantage of US ETFs is that they have lower fees than their European alternatives.

What matters to us is the Total Expense Ratio (TER) of the ETFs. The TER is the total fee you pay for holding the money. This fee is expressed in percentage and is removed from your money over the year. So, if you have a TER of 0.1% and 100,000 CHF in the fund, you will lose 100 CHF each year to fees.

Since you will pay the fees each year, it is important to optimize them. If you are a passive investor, ongoing fees are the most important cost you can optimize. So, it is important to do it well. And the more money you have in the funds, the more fees you will pay.

We can compare a few ETFs to see the difference in fees:

- Vanguard S&P 500: The US ETF (VOO) has a TER of 0.03%, while the European ETF (VUSA) has a TER of 0.07%, twice as expensive

- Vanguard World: The US ETF (VT) has a TER of 0.06%, while the European ETF (VWRL) has a TER of 0.14%, more than two times more expensive

- iShares S&P 500: The US ETF (IVV) has a TER of 0.03%, while the European ETF (IUSA) has a TER of 0.07%, twice as expensive

- iShares World: The US ETF (URTH) has a TER of 0.24%, while the European ETF (IWRD) has a TER of 0.50%, twice as expensive

As you can see, the TER of European funds is significantly higher than US ETFs. Over the long term, this will make a significant difference in your returns.

When you are investing in ETFs, investing fees are not to be ignored. And this is especially true if you want to retire early based on your portfolio.

US ETFs are more tax-efficient

The second advantage is even more significant, but it is also a bit more complicated and is only for Swiss investors. Indeed, US ETFs are more tax-efficient for Swiss investors.

This tax efficiency is based on the way dividends are taxed. Especially how the US taxes dividends of US companies.

By default, the US government will tax 30% of the dividends emitted by US companies to foreign investors. Now, Switzerland has a tax treaty that reduces this withholding to 15% for Swiss investors, the same amount withheld for US investors. And moreover, we can reclaim the 15% left on our tax declaration.

But when we use an ETF in Europe, the dividends will be withheld before reaching the fund. For instance, if you invest in an ETF from Ireland with Coca-Cola shares, you will lose 15% of these dividends directly. But if these dividends are paid to a US fund, there is no loss!

This advantage is essential since US stocks make up 50% of the entire world stock market. Saving on the dividends of these stocks is very important.

The second-best domicile for ETFs after the US is Ireland. So, if you do not have access to US ETFs, Ireland (IE) ETFs are the next best thing.

Overall, how much you save will depend on the yield of the ETFs you are using. For a 2% yield, you will save 15% of 2%, which is 0.3%. So, by using US ETFs, you can save up to 0.3% in fees every year! On a 100’000 CHF portfolio, you can save 300 CHF per year!

However, it is critical to know that this deduction can only be claimed when it reaches 100 CHF. Below 100 CHF, taxes will reject this deduction. So you will need about 33’000 CHF in US ETFs before you can claim it.

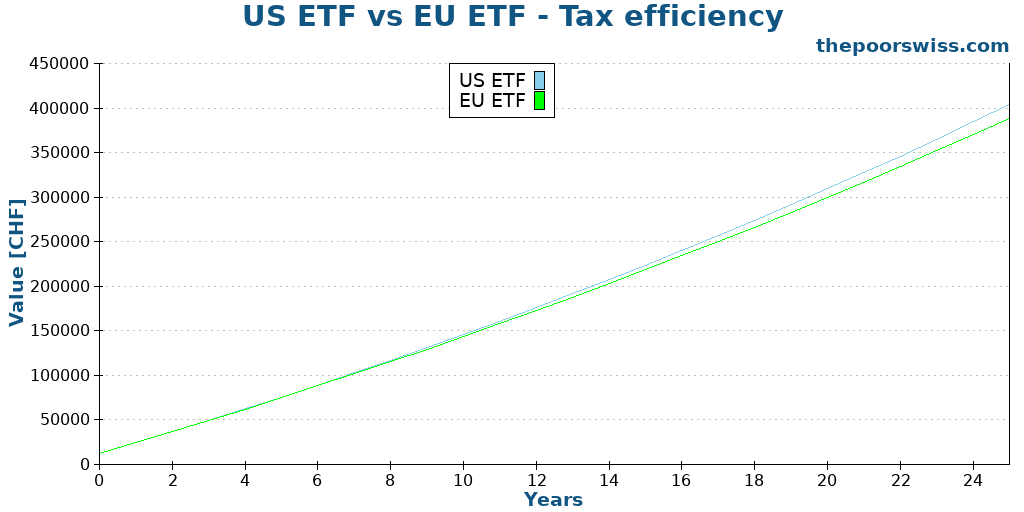

If you are wondering whether this is significant, you can take a look at the following graph. In this example, we are investing 1000 CHF per month over 25 years and the only difference is that we lose 15% of the dividends with

US ETFs are larger

A small advantage is that US ETFs are larger and more liquid. By large, I mean that they are managing more money. Generally, this is exposed as the Assets Under Management (AUM) metric.

A larger ETF has a few advantages over a smaller one:

- It shows more popularity. Larger funds are generally large because they are very popular (people put their money in them).

- It has a lower chance of being closed.

- A larger ETF has a higher trading volume. This has the advantage of the ETF being easier to sell. Generally, they also have a lower spread, which gives you better buying and selling prices.

- A larger ETF can better replicate the index since it will include more small companies than a smaller ETF.

For these reasons, large ETFs are generally better than small ETFs. But this should not be the primary argument in choosing an ETF.

US ETFs are cheaper to trade

The last advantage is that US ETFs are cheaper to trade (with a good broker) than European ETFs.

This is not directly due to the fund itself, but rather to the stock exchange they use.

For instance, my primary ETF, Vanguard Total World (VT), is traded on the New York Stock Exchange (NYSE). To buy or sell shares with Interactive Brokers costs me about 0.35 USD. I can buy many shares and still pay less than a dollar for the transaction.

On the other hand, buying 10’000 CHF of my Swiss ETF, iShares Core SPI ETF (CHSPI) on the Swiss Stock Exchange (SWX), cost me 10 CHF! That is about 30 times more expensive than my US ETFs.

And European ETFs are about in the middle of Swiss ETFs and US ETFs. To my knowledge, US ETFs are the cheapest to trade. Now, this may change if you use a service with free transactions. But there are very few good services like this available in Switzerland yet.

Risks: What about the US Estate Tax?

Many believe we should not invest in US ETFs because of the US Estate Tax. And in some cases, this is true. But in practice, for Swiss investors, there is almost no extra risk in investing in US ETFs.

The US estate tax law states that the inheritance of US ETFs is subject to a 40% inheritance tax. Nonresident aliens (basically, foreigners outside the United States) are exempted from this tax for assets up to 60,000 USD. After this, foreigners will have to pay a 40% tax.

This means that if you have many US assets, they could lose much value when you pass away, and your assets go through inheritance. You do not want this to happen to your estate.

However, many people miss that Switzerland has an estate tax treaty with the United States. And this treaty greatly increases the part exempted from this estate tax!

With this estate tax treaty, Swiss investors are exempted from the US estate tax for up to 11.18 million dollars, prorated to the proportion of US assets in your net worth. For instance, if US ETFs represent 10% of your estate, 1.118 million dollars (10% * 11.18 million) will be exempted from US Estate Tax!

So, in most cases, Swiss investors do not have to worry about the US estate tax! However, it is true that it may complicate your estate. If you have US ETFs, you will need to deal with the IRS.

If you want all the details and many more examples, you can read my in-depth article about the US Estate Tax law. This article also explains how to deal with US estate tax, in the specific case of Interactive Brokers.

What if you cannot use US ETFs?

Unfortunately, many people do not have access to these great US ETFs.

For these people, investing in European ETFs is still an excellent option. Using US ETFs is the best way to invest. However, it is an optimization over European ETFs. There is nothing wrong with investing in European ETFs!

If you want to be optimal, you must go with US ETFs. Now, it could be difficult (or even impossible) to use these ETFs. Even for Swiss investors, few brokers let us access them. If you do not want to go the extra mile and want to invest in good ETFs with lower effort, European ETFs are great!

What matters most is investing, not investing optimally!

What about mutual funds?

In this article, I have talked very specifically about US ETFs, but what about funds?

US mutual funds are also great. But it is interesting to know that Swiss mutual funds can also save you dividends. Indeed, funds are very different from ETFs in how they are held.

With a fund, each investor goes indirectly. With an ETF, you go through a broker who holds the shares in your name.

This allows the fund to be more efficient, directly depending on the treaty. So, a Swiss-domiciled mutual fund is as tax-efficient as a US-domiciled ETF. Of course, the Swiss mutual funds will likely have some other disadvantages (smaller and more expensive, mostly), but it is good to know that the main tax disadvantage of European ETFs is not present in Swiss mutual funds.

Conclusion

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

As you can see, there are many strong reasons to invest in US ETFs instead of European ETFs! These ETFs will let you save a significant amount of money in fees and taxes.

80% of my portfolio is invested in Vanguard Total World (VT), a US ETF. The rest is invested in a Swiss ETF for my home bias portion. So, I invest a considerable portion of my money into US ETFs. This is because I consider these ETFs to be the best available for Swiss investors.

However, these ETFs are more difficult to use. Investors from the European Union cannot invest in them anymore, and in Switzerland, only a few brokers let you use them.

As I mentioned, US ETFs are an optimization over European ETFs, but they are not a revolution. If you cannot (or do not want to) invest in US ETFs, investing in European ETFs will be a great way to invest!

If you want to start trading US ETFs, I recommend using Interactive Brokers. It is an excellent broker that lets you trade US ETFs with very low transaction fees. I have a guide on investing with Interactive Brokers.

Are you investing in US ETFs?

More reading

Swiss Investors almost lost Access to US-Domiciled ETFs

Starting in 2022, U.S. domiciled funds will not be available to Swiss investors. DEGIRO decided to enforce this early, in 2019. What can we do?

Exchange Traded Funds (ETFs) – Best for passive investors

Master the basics of investing. Learn exactly what Exchange Traded Funds (ETFs) are, how they work, and why they are the best tool for building wealth.How to Change Broker and Transfer Your Portfolio

Find out how to change broker and how to transfer your investment portfolio from the old broker to the new broker account.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste

The article is a great write-up, however I have a couple of questions:

While the performance of the VT (world) and VOO (S&P 500) US-products are very similar to the European iShares MSCI World and iShares S&P 500, there is a stark difference when taking the EUR/USD conversion into account. At first I didn’t understand where the difference between the reported numbers came from. The 10-year return for iShares World is 142.54% in USD and 211.40% in EUR. The 10-year return for the iShares S&P 500 is 219.54% in USD and 310.28% in EUR. This comparison indicates that EUR investments had a very big currency advantage over the last 10 years. This is of course based on the historical exchange rate of EUR and USD, but just something to keep in mind.

The other question is, how long Swiss residents will be allowed to buy US ETFs. Since Switzerland often implements EU regulations a couple years later and behaves much in the same way and interests as the European Union does, I don’t see how it’s feasible to keep buying US ETFs when the writing is already on the wall that trading them will not be possible anymore someday. Wouldn’t that be very bad for a product that we want to hold for as long as possible (10/20/30 years)?

Hi Christian

Thanks!

Yes, we have to keep currencies in mind. That’s a problem for Swiss investors that have to use either USD or EUR investments. I believe that in the long term, this will balance out and no tool can make it better in the long term. But we should definitely not forget about that. What matters in the performance in CHF.

Switzerland is implementing similar regulations indeed, but they are not exactly the same. We have equivalent regulations making Swiss brokers unable to recommend/advertise US ETFs. Currently, the CH regulations are different in that execution-only is allowed.

I don’t think it will change in the future. But even if it does, it’s not a big deal. Once this happens, we will still be able to keep these shares, we will just have to switch to something else.

Hi Baptiste,

Thanks for the highly informative article! As a complete novice I just have one question about currency risk. How much attention should I pay to that? For context I exchanged 30k to dollars already on IB and plan to do a lump sum investment in VT (or split into 10k over 3 months).

Thanks in advance for any advice!

Anna

Hi Anna

I would say it depends on two factors:

1) For how far away are you investing? In the very long term, currency risk should almost not matter. But in the short to medium term, it is indeed important.

2) How risk-averse you are? If you can’t handle the extra volatility, you should probably reduce the currency risk.

Hello

If you hold a US-domiciled ETF with non-US stocks and non-US bonds, aren’t you being double taxed on these dividends, ie, the US taxes you 15% on the dividends + the country where the stocks or bonds originate also withhold dividend tax? Wouldn’t this double taxation of non US stocks and bonds be avoided by holding an Irish UCITS because you would avoid the 15% withheld by the US and only have to deal with whatever the originating country withholds?

Best

Jordan

Hi Jordan

As far as I know, there is no extra tax holding non-US stocks in an US ETF.

But if you have a fund with only non-US securities, there is also no advantage in holding it in a US ETF.

I am seeing to apps for IB on the Apple App Store:

https://apps.apple.com/ch/app/ibkr-mobile-invest-worldwide/id454558592?l=en-GB

https://apps.apple.com/ch/app/ibkr-globaltrader/id1604776354?l=en-GB

Have you tried them and seeing your preference for IB, can you comment on them?

Much appreciated, Robert

Hi Robert

I almost never use the mobile apps.

I have a slight preference for the Mobile Invest. You can see it here: How to buy an ETF from IBKR Mobile

IBKR Global Trader is slightly more modern and more polished. I have a review of it: IBKR Global Trader Review 2024 – Simple stock trading

Hey Baptise,

Thanks for all your great articles!

Assuming one can’t invest in US ETFs, or has reached a limit that she/he is comfortable investing with IB, could it make sense to directly buy a small quantity of stocks to counter balance the disadvantages of European ETFs? I am thinking of having one European ETF + replacing a portion of it with eg the top X holdings of that ETF.

Of course this would be riskier than having the ETF itself but accepting this and assuming a small allocation could that compensate for the tax-inneficiency of European ETFs?

Hi Eric

As long as you are talking about US companies and that your broker let’s you fill a W8BEN form, yes, that could be an idea.

Be careful that means you will have to balance yourself the different companies and it will be more expensive in transaction fees (Swiss broker ain’t cheap).

It would more tax efficient, but unless you have a high amount to invest, it may not be that efficient given the downsides.

I suggest to review VWRL. It is not so bad as you might think. I agree that tax inefficiency for US dividends is a disadvantage for VWRL vs VT. But it you look at performance of these two ETFs from 2012 to 2024 since launch of VWRL, they had similar performance. Reason being VWRL doesn’t have small caps which compensated for US dividend disadvantage. And the TER difference is not really impactful because tracking difference of VWRL is very low and hence effective costs are not that high.

In real terms the disadvantage of US dividend tax can be about 0.1% for VWRL vs VT.

Having said that, if you really don’t want to have disadvantage for US dividends, another approach could be following -:

– buy US ETF for US exposure (like VTI)

– buy IRISH ETFs for rest of the world (VEUR, VFEM, VPAX, VJPN). You need 4 ETFs instead of one

– ignore Canada or buy a Canadian ETF also via US

For me personally, I also don’t want 100% IB and 100% US ETFs. So my alternate is SSAC (ishares) if I want accumulation or VWRL (vanguard) if I want distributing.

Thanks a lot both for the detailed answers!

Have you considered the new FWRA or a combination of VEVE/VFEM eg 90/10% as an alternative to VWRL?

I understand that all can be bought directly in CHF on SIX, although the volumes are lower there. Would you be concerned by that?

Following is from Swiss resident perspective-:

Just trying to understand. I have seen many comparisons of US domicile ETF and Irish domicile ETFs.

But what about CH domiciled global funds like ones offered by CS. Let‘s assume the TER is same. Would CH domicile funds be same as US domicile ETFs or they would suffer same disadvantage like IE ETfs?

I am a bit confused why there are not a lot of CH domicile global funds or ETFs.

Hi Abhiney

That’s a good question. Normally, it should suffer the same fate because anybody can use these funds. So, I would expect the US dividends to be withdrawn at source (at 15%) and we would not be able to reclaim that. Also, since it’s a CH ETF, we would have to pay CH dividend withholding (reclaimable).

And CH ETFs tend to be more expensive than US ones in terms of TER and significantly smaller.

Thanks. However I am wondering if an individual investor can claim back withholding taxes in US via Swiss tax returns using Double taxation treaty. Why the funds cannot do the same?

I would have expected that funds should get their withholding tax back and they should in turn deduct the reclaimable 35%

Seems funds don’t have same process like us individuals

Hi

Just to update.

I checked with UBS and it seems that 15% tax withheld in US can be claimed back by UBS and then this is reinvested into the fund. And of course 35% reclaimable Swiss WHT is charged to the investor.

This example is for UBS passive MSCI US Index fund. Valor 35655041

This basically means that for Swiss investors, Swiss domicile global finds might not be very bad.

Hi,

Yes, because this is a fund and not an ETF. This makes a difference.

I did not see in your original question that you were asking about funds and not ETFs, sorry.

It’s like many of the index funds for retirement, they can reclaim that and be more efficient.

I just want to update you. It seems at a later point UBS didn’t want to confirm their tax efficiency. They told me that they cannot give tax advise.

So now, I am not 100% sure if Swiss mutual funds can claim back tax from US or not. For pension funds for sure they can claim back but for non-pension funds the situation is not completely clear. Technically they should but I cannot confirm with proof that they do.

In an article from Finpension they recommend IE domicile as second best vs US

https://finpension.ch/de/das-beste-fondsdomizil-fuer-schweizer-anleger/

Thanks for the update Abhiney!

It seems indeed that IE is always the second recommendation after the US!

Hi Baptiste,

thanks for the article! Can you please explain in detail how taxation of dividends work? 30% is taxed by US and 15% is credited by Swiss authorities, and you indicate that 15% can be reclaimed. In this article I found that it is difficult to reclaim those 15% resting from US, did you have experience and how it is to be done? https://ajooda.ch/en/withholding-tax-on-dividends-in-switzerland-withholding-tax/

Hi Oleg,

The first part is not correct. If you sign a W8BEN, you only get a 15% tax from the US and you can reclaim that.

Saying it “requires enormous effort” is a huge overstatement. The effort is really low, I have detailed here: How to file your taxes with Swiss and foreign securities in 2024

Hi Baptiste, I see your site has info and many comments about U.S ETFs and access or not access to them. I have not yet opened an investment account with IBKR or other , but my intention is to do so and buy U.S ETFs based on advantages and research. However I’ve become quite confused if this is possible based on many comments by fellow followers. Add to that , Flowbank for example states purchasing US ETFs is possible . Suisse is not part of EU Ucits law as you stated in another post but there seems to be issues with some buying . In a nutshell what is the latest or confirmed availability for those starting out now? Thanks for your blog and efforts

Hi Marc,

Legally, it’s possible. And normally, it’s possible with IB (I did that this year already).

However, it seems that some users of IB have lost this access (I don’t yet know why).

Hello Baptiste,

I have no access to US ETF as I need to sick to one Swiss broker for professional reason and I was wondering if in this situation the use of a synthetic swap based IE ETF would allow to avoid completely US withholding taxes if this ETF complies with the Hire Act Section 871m regulations? It seems to be the case for instance of Invesco D500 which significantly outperforms the physical replication Vanguard VUSA maybe for that reason but I didn’t found any clear confirmation in the fund description.

If that’s true this could be an interesting addition to your very good article.

You wrote in an other article that you recommend to stay with physical ETF which makes sense for US based ones but if you need IE based ETF like me I was wondering if swap ETF would not be a better alternative.

Moreover most physical ETF practice securities lending which could expose them to the same level of conterparty risk as swap replication, isn’t it?

Many thanks for your insight!

Hi Julien,

It may be a way indeed, but for me, I still feel that a replication-based ETF is best. I want to know what my ETF holds.

If I could not invest in US ETF, I would invest in full replication EU ETFs.

Also, I would not call 3% difference in 5 years a significant outperformance, this is only a slight outperformance that may be within margin of errors.

It’s true that securities lending in ETF could create some risks, I did not take this into account in my choices yet. I will have to see whether we can find good ETFs without it. But from what I have read, Vanguard is quite conservative in its lending.

Thank you for the advice.

I agree that 3% over 5 years might not be a lot and if I understand well it becomes 1.5% over 5 years after reclaim in the Swiss taxation : exactly the 0.3% annual gain of the 15% withholding tax on an average 2% annual dividend as in your example.

I am not questioning the overall advantage of US ETF, just trying to find a better use of EU ETF…

This ETF is fine if you don’t mind synthetic ETFs. It’s probably among the best you can find in that category. So, if you are fine with these kinds of ETFs, go for it :)

Hey Baptiste

Thanks for this article. What happens if I would move back to the EU? I would assume it’s possible to hold and sell the US ETFs but not buy any new ones?

Thanks

Yes, Henrik, you are right. In this case, you would be able to keep your ETFs in your account but not buy more of them.

Thanks, the additional question might be more important; are you forced to sell them at market rate when you move or are you able to keep them and sell (not buy) them at the time of your choosing. Thanks again

Didn’t I answer already? You normally can keep your ETFs when you move. You can then sell them like your other ETFs, using any kind of orders you want.