US ETFs are the best ETFs for Swiss investors

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

I mostly invest in US ETFs, and I have recommended these ETFs many times on this blog. I consider US ETFs to be the best available ETFs. I have talked several times about what makes them great in various articles. But since I still get many questions, I will go into all the details of these US ETFs.

I am talking about Exchanged Traded Funds (ETFs) that invest in the United States. I talk specifically about ETFs from the United States. What matters here is the domicile of the ETF. This is more important than many people realize.

So, here is what makes these US ETFs great.

Availability of US ETFs

First, we need to address the issue of the availability of US ETFs, or lack thereof.

If you are in the United States, you will not have any issues. However, if you are in Europe, this is another story. Indeed, due to European regulations, many countries lost access to US ETFs.

In fact, in 2018, all the countries part of the European Union lost access to US ETFs. This is due to the PRIIPS regulations. These regulations are part of a bigger package known as MiFID II. These laws force the fund providers to provide a Key Investor Document (KID) in the investor’s language. And so far, US fund providers have not provided them, and they are unlikely to do it. So, for now, European investors cannot invest in US ETFs.

In theory, these laws protect investors by providing them more information on the instruments they are using. However, in practice, they are only here to force people to invest in European funds.

However, Switzerland is not part of the European Union. Therefore, Swiss investors still have access to US ETFs. However, this may change when the Swiss equivalent of the European laws enters into effect. Now, it is not entirely clear if this will apply to foreign brokers (like Interactive Brokers) or not. But for now, we are free to use these ETFs.

I believe these restrictions will not apply to execution-only brokers like Interactive Brokers. So, they should still be available in the future.

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

Furthermore, not every broker provides us with access to these ETFs, even though they could do it by law. For now, only foreign brokers, like Interactive Brokers, give access to these ETFs. This is good since Interactive Brokers is the best broker for Swiss investors.

If you want more information on these regulations, you can read my article on the availability of US ETFs.

US ETFs have lower fees

The first advantage of US ETFs is that they have lower fees than their European alternatives.

What matters to us is the Total Expense Ratio (TER) of the ETFs. The TER is the total fee you pay for holding the money. This fee is expressed in percentage and is removed from your money over the year. So, if you have a TER of 0.1% and 100,000 CHF in the fund, you will lose 100 CHF each year to fees.

Since you will pay the fees each year, it is important to optimize them. If you are a passive investor, ongoing fees are the most important cost you can optimize. So, it is important to do it well. And the more money you have in the funds, the more fees you will pay.

We can compare a few ETFs to see the difference in fees:

- Vanguard S&P 500: The US ETF (VOO) has a TER of 0.03%, while the European ETF (VUSA) has a TER of 0.07%, twice as expensive

- Vanguard World: The US ETF (VT) has a TER of 0.06%, while the European ETF (VWRL) has a TER of 0.14%, more than two times more expensive

- iShares S&P 500: The US ETF (IVV) has a TER of 0.03%, while the European ETF (IUSA) has a TER of 0.07%, twice as expensive

- iShares World: The US ETF (URTH) has a TER of 0.24%, while the European ETF (IWRD) has a TER of 0.50%, twice as expensive

As you can see, the TER of European funds is significantly higher than US ETFs. Over the long term, this will make a significant difference in your returns.

When you are investing in ETFs, investing fees are not to be ignored. And this is especially true if you want to retire early based on your portfolio.

US ETFs are more tax-efficient

The second advantage is even more significant, but it is also a bit more complicated and is only for Swiss investors. Indeed, US ETFs are more tax-efficient for Swiss investors.

This tax efficiency is based on the way dividends are taxed. Especially how the US taxes dividends of US companies.

By default, the US government will tax 30% of the dividends emitted by US companies to foreign investors. Now, Switzerland has a tax treaty that reduces this withholding to 15% for Swiss investors, the same amount withheld for US investors. And moreover, we can reclaim the 15% left on our tax declaration.

But when we use an ETF in Europe, the dividends will be withheld before reaching the fund. For instance, if you invest in an ETF from Ireland with Coca-Cola shares, you will lose 15% of these dividends directly. But if these dividends are paid to a US fund, there is no loss!

This advantage is essential since US stocks make up 50% of the entire world stock market. Saving on the dividends of these stocks is very important.

The second-best domicile for ETFs after the US is Ireland. So, if you do not have access to US ETFs, Ireland (IE) ETFs are the next best thing.

Overall, how much you save will depend on the yield of the ETFs you are using. For a 2% yield, you will save 15% of 2%, which is 0.3%. So, by using US ETFs, you can save up to 0.3% in fees every year! On a 100’000 CHF portfolio, you can save 300 CHF per year!

However, it is critical to know that this deduction can only be claimed when it reaches 100 CHF. Below 100 CHF, taxes will reject this deduction. So you will need about 33’000 CHF in US ETFs before you can claim it.

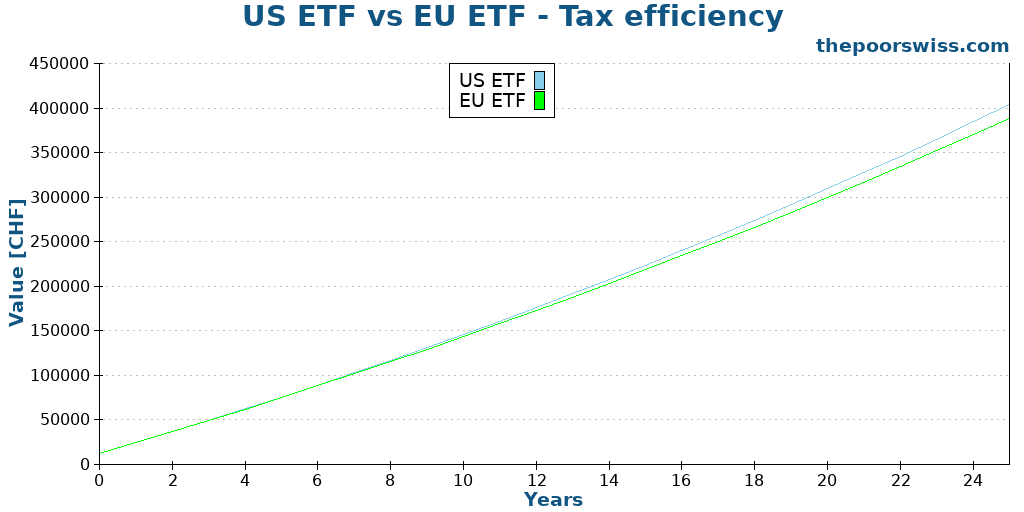

If you are wondering whether this is significant, you can take a look at the following graph. In this example, we are investing 1000 CHF per month over 25 years and the only difference is that we lose 15% of the dividends with

US ETFs are larger

A small advantage is that US ETFs are larger and more liquid. By large, I mean that they are managing more money. Generally, this is exposed as the Assets Under Management (AUM) metric.

A larger ETF has a few advantages over a smaller one:

- It shows more popularity. Larger funds are generally large because they are very popular (people put their money in them).

- It has a lower chance of being closed.

- A larger ETF has a higher trading volume. This has the advantage of the ETF being easier to sell. Generally, they also have a lower spread, which gives you better buying and selling prices.

- A larger ETF can better replicate the index since it will include more small companies than a smaller ETF.

For these reasons, large ETFs are generally better than small ETFs. But this should not be the primary argument in choosing an ETF.

US ETFs are cheaper to trade

The last advantage is that US ETFs are cheaper to trade (with a good broker) than European ETFs.

This is not directly due to the fund itself, but rather to the stock exchange they use.

For instance, my primary ETF, Vanguard Total World (VT), is traded on the New York Stock Exchange (NYSE). To buy or sell shares with Interactive Brokers costs me about 0.35 USD. I can buy many shares and still pay less than a dollar for the transaction.

On the other hand, buying 10’000 CHF of my Swiss ETF, iShares Core SPI ETF (CHSPI) on the Swiss Stock Exchange (SWX), cost me 10 CHF! That is about 30 times more expensive than my US ETFs.

And European ETFs are about in the middle of Swiss ETFs and US ETFs. To my knowledge, US ETFs are the cheapest to trade. Now, this may change if you use a service with free transactions. But there are very few good services like this available in Switzerland yet.

Risks: What about the US Estate Tax?

Many believe we should not invest in US ETFs because of the US Estate Tax. And in some cases, this is true. But in practice, for Swiss investors, there is almost no extra risk in investing in US ETFs.

The US estate tax law states that the inheritance of US ETFs is subject to a 40% inheritance tax. Nonresident aliens (basically, foreigners outside the United States) are exempted from this tax for assets up to 60,000 USD. After this, foreigners will have to pay a 40% tax.

This means that if you have many US assets, they could lose much value when you pass away, and your assets go through inheritance. You do not want this to happen to your estate.

However, many people miss that Switzerland has an estate tax treaty with the United States. And this treaty greatly increases the part exempted from this estate tax!

With this estate tax treaty, Swiss investors are exempted from the US estate tax for up to 11.18 million dollars, prorated to the proportion of US assets in your net worth. For instance, if US ETFs represent 10% of your estate, 1.118 million dollars (10% * 11.18 million) will be exempted from US Estate Tax!

So, in most cases, Swiss investors do not have to worry about the US estate tax! However, it is true that it may complicate your estate. If you have US ETFs, you will need to deal with the IRS.

If you want all the details and many more examples, you can read my in-depth article about the US Estate Tax law. This article also explains how to deal with US estate tax, in the specific case of Interactive Brokers.

What if you cannot use US ETFs?

Unfortunately, many people do not have access to these great US ETFs.

For these people, investing in European ETFs is still an excellent option. Using US ETFs is the best way to invest. However, it is an optimization over European ETFs. There is nothing wrong with investing in European ETFs!

If you want to be optimal, you must go with US ETFs. Now, it could be difficult (or even impossible) to use these ETFs. Even for Swiss investors, few brokers let us access them. If you do not want to go the extra mile and want to invest in good ETFs with lower effort, European ETFs are great!

What matters most is investing, not investing optimally!

What about mutual funds?

In this article, I have talked very specifically about US ETFs, but what about funds?

US mutual funds are also great. But it is interesting to know that Swiss mutual funds can also save you dividends. Indeed, funds are very different from ETFs in how they are held.

With a fund, each investor goes indirectly. With an ETF, you go through a broker who holds the shares in your name.

This allows the fund to be more efficient, directly depending on the treaty. So, a Swiss-domiciled mutual fund is as tax-efficient as a US-domiciled ETF. Of course, the Swiss mutual funds will likely have some other disadvantages (smaller and more expensive, mostly), but it is good to know that the main tax disadvantage of European ETFs is not present in Swiss mutual funds.

Conclusion

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

As you can see, there are many strong reasons to invest in US ETFs instead of European ETFs! These ETFs will let you save a significant amount of money in fees and taxes.

80% of my portfolio is invested in Vanguard Total World (VT), a US ETF. The rest is invested in a Swiss ETF for my home bias portion. So, I invest a considerable portion of my money into US ETFs. This is because I consider these ETFs to be the best available for Swiss investors.

However, these ETFs are more difficult to use. Investors from the European Union cannot invest in them anymore, and in Switzerland, only a few brokers let you use them.

As I mentioned, US ETFs are an optimization over European ETFs, but they are not a revolution. If you cannot (or do not want to) invest in US ETFs, investing in European ETFs will be a great way to invest!

If you want to start trading US ETFs, I recommend using Interactive Brokers. It is an excellent broker that lets you trade US ETFs with very low transaction fees. I have a guide on investing with Interactive Brokers.

Are you investing in US ETFs?

More reading

How I Made $2’000’000 on the Stock Market – Book Review

Can you time the market? Read our review of "How I Made $2,000,000 in the Stock Market" and learn the lessons from this classic trading book.

Mutual Funds and Index Investing

Now that we talked about stocks and bonds, it is time to talk about Mutual Funds. Find out about active funds and passive funds.

Yield Curve Inversion: Should we Panic?

Predicting a recession? Learn what a yield curve inversion is, why it scares investors, and what it actually means for your portfolio.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste, thanks for the article!

I would like to clarify the tax on dividends comparison between the US and European ETFs as I did not fully understand where the 15% are left.

For the ETFs domiciled in Europe, is it the case that the US withholding rate is 30% because of the US-EU treaty but you can only get 15% back? In other words, a Swiss resident can claim back at most 15%, but US withholds 30% because the money are paid to a fund that is neither in US or in Switzerland.

It’s slightly more complicated than that because it also depends on where there ETF comes from in the EU :)

And we are only talking about dividends coming from US companies.

If the country has a treaty with US, like Ireland, the US will take 15% of the dividends, before they reach the ETF. So you will never claim back these 15%.

If the country does not have a treaty, the US will take 30% of the dividends. Again, these 30% are lost.

If you own a US ETF directly, the withholding is done to you (not to the fund holder). Therefore, in Switzerland, 15% are taken but we can claim them back.

Does that make sense?

I understand, thanks! So the difference is not because of a different US withholding rate between Switzerland and Ireland, but because as a Swiss resident the withholding is done to you and you can claim it back.

I am assuming that IRS treats the US funds differently and goes a step further and does the withholding at the asset owner level, instead of at the fund level, as it is for Ireland.

That’s exactly it, it’s really the difference in ownership that matters.

Hi Baptiste,

Thanks for the excellent blog.

I have a question related to this:

“By default, the U.S. government will tax 30% of the dividends emitted by U.S. companies to foreign investors. Now, Switzerland has a tax treaty that reduces this withholding to 15% for Swiss investors, the same amount withheld for U.S. investors. And on top of that, we can reclaim the 15% left on our tax declaration.”

Do I understand correctly that dividends on US ETF are tax free for CH residents (if you reclaim the 15% in the tax declaration that IB applies)?

Hi Gian,

They are not really tax-free because they still get added to your taxable income. So, they are taxed at your marginal tax rate, which may be high.

But they are, in a sense, withholding-free since there is no withholding from Switzerland, and the withholding from the US can be claimed back.

Hi Baptiste,

If I understand the comments correctly, I need to send the Form W8BEN-1 completed to the broker and Form DA-1 with the tax return to the Swiss tax authorities to reclaim the 30% withholding tax in total. Is this correct?

Are there any instructions on how to fill out the documents or can I do it with my tax advisor?

Regarding the DA-1 form, I have read that the Swiss tax authorities only take this into account if the value is higher than 100 CHF. For this value to be higher than CHF 100, my portfolio must distribute over CHF 600 in dividends from foreign stocks.

Regards

Marco

Yes, your broker should give you access to a W8BEN form (but not all brokers support that). And DA-1, you will have to fill it every year.

I have an article about reclaiming this, you definitely don’t need a tax advisor: How to file your taxes with Swiss and foreign securities in 2023

You are correct, there is a minimum of 100 CHF in most cantons.

Hey there,

Thanks for this great website!

It looks like that as of today I cannot buy US ETFs anymore on IB. I get a notice linking to https://ibkr.info/article/4718.

Anyone having the same issues?

Hi

That’s a current problem that seems to touch every Swiss investor. There are many discussions about it, and it’s unclear whether this will stay.

I will try to post an update about this if this stays the case. But currently, I would say there is a 50/50 chance of getting back US ETFs.

It looks like we can buy these ETFs again.

Some communication from IB:

> The warnings, order cancellations or rejections for instruments without Key Information Documents (KIDs) are related to a temporary technical issue on our side which will be resolved soon. We are sorry for any inconvenience.

Indeed, it’s been fortunately restored for every Swiss investor!

Hi Baptiste,

Many thanks for the all the info you add on this blog.

What would you recommend for people currently residing in Switzerland but that will move to an EU country in the short term (3-5 years)?

Should they buy US ETFs or rather opt for the European ones? I am not sure whether you will be allowed to hold your position or will have to sell, in addition to the tax implications.

Thank you in advance for the answer!

Hi Elizabeth,

I would still recommend US ETFs while in Switzeralnd and then switch to IE ETFs once in the EU.

When this happened in the EU, people were not forced to sell, but they could not buy anymore.

Thank you Baptiste. The way I understand it:

1. Holding US domiciled ETFs in Europe is problematic because you could end up paying 30% dividend tax (instead of 15% if ETF were domiciled in Ireland)

2. You could be subject to the US Estate Law and pay up to 40% tax if you die (depending on whether country has treaty or not)

3. Therefore it makes sense to hold IE domiciled ETFs if you are based in Europe.

Now if someone were to hold a lot of US domiciled ETFs in Switzerland and moved to Europe, they would have to swap them for IE domiciled ETFs. This in turn means:

a) You would incur some transaction costs when swapping such large number of ETFs from US to IE

b) Both US domiciled and IE domiciled ETFs should have similar prices therefore you do not incur significant costs when swapping one for the other

c) The benefits of holding US domiciled ETFs in Switzerland for ~3 years outweigh the costs incurred in a) and b) together, therefore it still makes sense

Is my understanding correct? Many thanks in advance!

Your point 3) is correct but it depends on the treaty. As such, it does not apply to Switzerland.

Yes, your understanding is correct. And even for 3 years, I think it’s worth it.

Hi Baptiste

First of all congratulations on a really excellent website. Have you considered a YouTube channel?

I currently invest using IB and Swissquote. On the latter I notice I get taxed 30% US withholding tax on my US domiciled ETFs. I’m a resident of Switzerland and never lived in the U.S. How can I reclaim the 15% excess tax back?

Thanks in advance, Tim

Hi Tim,

I thought about it, but for now, decided against it. I simply don’t have the time to start any new large project with my son, my job and this blog :) And I do not think I will make a good job on a visual media.

You will have to contact Swissquote to fill a W8BEN-1 to get the 15% deduction instead of 30%. Why aren’t you holding your US ETFs at IB? The difference in transaction fees is really major.

Hi Baptiste,

What happens if I invest in U.S. ETFs now and later on Switzerland disables access to U.S. ETFs?

Would I need to sell everything I have or loose control over my shares?

Does the threat that Switzerland might disable access to U.S. ETFs mean that investing in an U.S. ETF, like VOO, is not a good long term investment (30+ years) for a Swiss person?

Hi Raquel,

We would simply be unable to buy more, but we could still sell or keep the shares we have.

I would not consider this a big threat, and I would definitely not stop investing in US ETFs because of that.

Dear Baptiste,

Thank you so much for all the info. I was wondering if you could provide me with some advice.

I am currently in the process of moving with my wife to Switzerland.

My initial plan was to open a joint account together with her utilising the UBS family pack.

After reading your blog I am now unsure of this decision. Now I am more leaning towards opening an online bank for myself (such as Neon), using another digital service for my 3rd pillar, using IB for our investments, and using Revolut or Wise for our joint account.

Now, the only nuisance is that she is a US citizen. My question is: would you know what are the implications of her sending a monthly amount to both Revolut (in my name) and Interactive brokers (possibility to open a joint account- worth it?)?

Thank you so much again for all the info provided!!

Hi Jaime,

Ideally, I would recommend opening joint accounts when possible, but it all depends on how you manage your money as a couple.

Being a US citizen makes it difficult to find a great bank because the best banks avoid them. You could get Neon bank for you and maybe Migros Bank for her. Or a joint account at Migros Bank for both of you and then a Neon on the side if you want a better account.

I don’t know the implications of sending that, but it should be fine as long as it’s disclosed. But I would be careful about trusting Revolut with much money.

Hi Baptiste,

As this is very important topic, maybe my question is stupid but let’s clarify this – when you say “Swiss investor” – is this related only to Swiss citizens or also includes Swiss residents (holding B/C permits)

Best

Hi

In that case, I am talking about investors that pay their taxes in Switzerland, no need to be a citizen :)

Hi!

Thanks amazing article!

Can you recommend an ETF Search Tool that also includes US domiciled ETFs (ExtraETF for example only shows ETFs available in EU, not the US ETF like VOO).

Also are US ETFs more distributing than accumulating? I have a hard time finding acc. US ETFs. Again Exra ETFs offers one glimpse whether an ETF is acc. or distr. Is there an US version of ExtraETF?

Thank you for your help?

Julia

Hi Julia,

I don’t know any good search tool that includes US ETFs.

Yes, US ETFs are not accumulating because funds are restricted by law to distribute at least 90% of the income. So they could only accumulate 10% at most which makes no sense.

Hi Baptiste

As far as I know, distributing (US) ETFs are not optimal for investors who are in accummulation phase as this results in higher transaction costs for reinvestments, requires manual reinvestments etc. (https://gerd-kommer.de/ausschuettende-vs-thesaurierende-fonds/#:~:text=Der%20Wert%20eines%20Fondsanteils%20vermindert,thesauriert%E2%80%9C)%20sie%20ins%20Fondsverm%C3%B6gen.).

Do you think the advantages of U.S. ETFs still outweigh the disadvantages associated with distributing ETFs for invenstors in the accumulation phase?

hi Chris,

That’s not correct in Switzerland in my opinion, for several reasons:

* Accumulating and distributing will result in the same taxes, so no advantages for accumulating here

* During the accumulation phase, you are investing every month. So, it does not matter if you invest 1000 CHF or 1000 CHF + a small amount of dividends, the fees will be the same, so again not disadvantage for distributing

* Same for manual, since you are investing anyway, it makes no difference.

So, I would say the advantages of US ETFs far outweigh the fact that there are no accumulating US ETF. In fact, I would even prefer distributing ETFs over accumulating ETFs in any case.

Thanks Baptiste!

I plan to automate my investments with IB as described on https://thepoorswiss.com/automate-your-investments-interactive-brokers/. It means a FIXED amount will invested every month. Consequence: dividends will NOT be reinvested automatically. I could invest them manually but I want to avoid manual work as I prefer automation and want to profit from compound interest as much as possible. Furthermore, an additional manual reinvestment of dividends would require another transaction and result in higher fees.

Therefore I am still uncertain if the accummulating Ireland domiciled ETF IE00BK5BQT80 fits better to my case. What do you think?

Would you even prefer distributing ETFs over accumulating ETFs if you have no access to US ETFs? And if so, why?

Hi Chris,

I think it’s a bad idea :)

For me, distributing ETFs have significant advantages, especially in retirement. Even without US ETFs, I would not use accumulating ETFs.

On top of that, the extra efficiency of US ETFs is worth significantly more than the small time you will gain.

Since most ETFs pay dividends quarterly, you only have to log in to IB once a quarter to reinvest them yourself. You could even create a second automated investment rule quarterly to reinvest your dividends, but it’s difficult to set that one properly in terms of value.

IB also supports dividend reinvesting for some ETFs. I have never tried it, but it’s likely that US ETFs are working.

Hello Baptiste,

Many thanks for this great article, very interesting. One naive question regarding US ETFs, isn’t there a big risk in investing in them given that there are talks of the US defaulting on their currency and causing yet another Global recession?

Hi,

If the US defaults on its currency, the risk will be across the entire world. Most large companies in the world, including Swiss ones, would be impacted.

And if this starts a major global recession, all stock market exchanges will be impacted.

If you are afraid about the currency risk, you should invest more in the Swiss ETFs, but be aware that big companies are exposed themselves to the currency risk and as such their stocks are exposed as well.

Thankyou for this great explanation.

At the moment I am a foreigner working in Switzerland (3,5 years now) and have a B-Permit. I am investing Monthly already via deGiro in VWRL. Maybe in a few years I will go back to the Netherlands. I want to open an IB account, due to the fact that my deGIRO account is in CHF and that will not be optimal when I live somewhere else and do not have CHF as my main currency anymore.

In this case the possibility of investing in U.S ETF’s will also be a possibility as long as l will stay here in Switzerland.

Due to the fact that I am still automatically paying tax by ‘Quellensteuer’ I am currently not declaring to get the 35% tax over my dividends back.

When investing in U.S Etf’s and paying the U.S Tax, I will ‘only’ pay 30% – 15% = 15% U.S tax over my dividends and don’t have to worry about getting taxed in Switzerland anymore?

I am not planning doing the tax declaration to get the other 15% back due to the Quellensteuer system.

You are correct:

* IB is better if you plan to move around since DEGIRO accounts are local

* With IB, you will be able to invest in US ETFs and only pay 15% withholding tax as a Swiss resident