Second Pillar: All you need to know to retire in Switzerland

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

We have studied the first pillar in the previous post in the series. Now, it is time to study the second pillar. The second pillar is an occupational pension for people working in Switzerland.

While the first pillar covers everybody’s basic needs, the second pillar covers a larger part of your salary. It is an occupational pension. If you never worked, you will never pay anything for this, and you will never receive anything from this. It is significantly more complicated than the first pillar.

In this article, I give you all the important details on the second pillar. I will also help you understand what you can do to improve it.

The Second Pillar

The second pillar is your work pension.

In French, it is called Loi fédérale sur la prévoyance professionnelle vieillesse, survivants et invalidité (LPP). In German, it is Bundesgesetz über die berufliche Alters-, Hinterlassenen- und Invalidenvorsorge (BVG). As you can see, the Swiss government is very good to make short names… But, we will simply call it second pillar in this article.

This second pillar is a pension for every people who worked in Switzerland and paid into the LPP. Every Swiss employee of at least 24 years with an annual salary of more than 21’150 CHF contributes to the second pillar. It is directly deducted from your salary and transferred to your pension fund. The contribution is a percentage of your salary.

Interestingly, your employer will at least match your contribution. Some employers contribute more than this. As an independent, you must pay both the employee and employer parts.

How much you pay for the second pillar depends on your age:

- 25 to 34 years old: 7%

- 35 to 44 years old: 10%

- 45 to 54 years old: 15%

- 55 to 65 years old: 18%

The percentage deducted from your salary depends on the part your employer is paying. All the contributions to the second pillar are pre-tax. It is an essential fact. You will pay the taxes when you withdraw your second pillar.

As you get older, you put more and more into your second pillar. It means that the last years matter a lot in the calculations of your second pillar pension. It is a bit dumb because the first years are the ones that are the most important for compound interest. So, we should actually contribute more in the early years.

The first pillar was global insurance. You are paying for other people. But the second pillar is a physical account, in your pension fund, with your name. So this is your money.

There is another big difference. Your pension fund is related to your current employer. Each employer chooses its pension fund provider. It means that when you change company, you will likely change pension fund as well.

Some companies will have a better option for the second pillar than others. Most second pillar providers are extremely conservative. But there are a few good ones that allow investing your money in stocks.

Vested Benefits

If you change employers, you must transfer your contributions to the new pension fund. But if you do not directly switch to a new job, you will transfer the funds into a vested benefits account.

If you lose or quit your job, you must transfer the funds into a vested benefits account. This account will be locked until you get a new job (and a new pension fund) or reach retirement age. Even if it is in your name, there is not much you can do with it. In some cases, you can choose how the money is invested. But, you cannot move money in or out.

If you become unemployed, you can also choose to continue contributing to the pension fund. In that case, you can transfer your assets to the Substitute Occupational Benefit Institution. This could be an option to avoid a gap in your pension fund.

If you retire early, you will keep the money in a vested benefits account as soon as you quit your job. It will stay there until the official retirement age. Vested benefits accounts can be withdrawn up to five years before retirement age.

If you leave Switzerland, you will have the choice to withdraw the money or keep it until retirement. Depending on the country you are leaving to, different conditions may apply.

Vested benefits accounts are generally much better than pension funds. For instance, you can take a look at finpension. They offer excellent vested benefits accounts.

If you want to know more, I have an article about all you should know about vested benefits.

Mandatory vs. Extra Mandatory

Now starts the complicated part about the second pillar. We have to distinguish between the mandatory insured salary and the extra-mandatory salary.

We will only be talking about the yearly salary here. The mandatory insured salary is the salary between MIN and MAX. These numbers are valid as of 2024 and usually change every two years.

- MIN is 7/8 of the maximum of the first pillar, 25’725 CHF.

- MAX is three times the maximum of the first pillar, 88’200 CHF.

If your salary is between 22’050 CHF and 29’250 CHF, your mandatory insured salary will be 3’525 CHF. Everything higher than MAX is the extra-mandatory salary. So, the maximum mandatory insured salary is 62’475CHF (MAX-MIN).

Here are a few examples with different yearly salaries:

- 20’000 CHF: Not eligible for the second pillar (less than 22’050 CHF)

- 25’000 CHF: Mandatory insured salary of 3’525 CHF (less than 29’250 CHF)

- 30’000 CHF: Mandatory insured salary of 4’275 CHF

- 50’000 CHF: Mandatory insured salary of 24’275 CHF

- 88’200 CHF: Mandatory insured salary of 62’475CHF

- 100’000 CHF: Mandatory insured salary of 62’475CHF CHF and Extra-mandatory salary of 11’800.

So what is the difference between these two parts?

I mentioned the contribution rate for the second pillar. These were the contributions to the mandatory part. The contributions for the extra-mandatory part depend on your pension fund and your company.

Another difference is the interest rate. The law sets a minimum interest rate of 1% on your mandatory contributions. But there is no minimum for the extra-mandatory portion. Your pension fund can offer better (or worse) interest on it. It is generally a bit better on the extra-mandatory portion. This interest is the only way your second pillar account money will grow. It is not a great interest rate. But there is nothing you can do about it. It still beats Swiss banks currently.

The last difference is the conversion rate. This rate will define how much pension you can get from the capital. The law sets a minimum conversion rate of 6.8% for the mandatory portion of your capital. Again, there is no minimum for the extra-mandatory part. Your pension fund will set the conversion rate. Generally, it is significantly worse than the conversion rate on the mandatory part.

1e pension plans

There is a third component for the second pillar, the 1e pension plan. This plan offers better investments for persons with very large salaries. It is not well-known because very few employers have such a plan.

If you want to know more, read my article about the 1e pension plan.

Insurance for death and disability

The second pillar also acts as insurance in two cases.

In the case of disability, the insured person will get a disability pension. The basis for the pension is all the assets accumulated and the sum of all the future credits. But they will not take interest into account for future credits. It is great insurance in case of a serious accident.

In the case of death, the surviving spouse will get 60% of the deceased’s full disability pension. However, there are some conditions for eligibility. There should be either the duty to provide for children or be at least 45 years old and the marriage lasted at least five years. If these conditions are not met, the surviving spouse will only get three years of pension.

In both cases, the government will review the pension every two or three years based on the beneficiary’s cost of living.

If you want more details, I have an entire article explaining what would happen to your retirement benefits if you died. And if you want to protect against becoming disabled, you can learn about the disability insurance in Switzerland.

How much will I get from the second pillar?

Once you reach retirement age (65 for both men and women), you can get your second pillar. You have three options:

- An annuity

- A lump sum

- A lump and an annuity

Here is where the conversion rate becomes important. The annuity will be computed using the conversion rate. If you convert 200,000 CHF with a conversion rate of 6.8%, you will get a 13,200 CHF pension each year.

If you take a lump sum, you will pay capital taxes, and if you take an annuity, you will pay income tax on top of it. For the extra-mandatory part, the conversion rate will depend on your pension fund.

Whether you should choose between these options is discussed below.

Should I take an annuity or a lump sum?

There is no definite answer to this question.

It will depend on the conversion rate at the age of your retirement. And how much do you expect to get out of the capital each year if you manage it yourself? Generally, if you were to invest the amount into stocks, you would do, on average, better than the current conversion rates. However, there is a risk with stocks, whereas the conversion rate is guaranteed. In the end, you will have to do the math yourself, depending on your situation.

If you do not invest your money or get lower returns than the conversion rate, you should probably opt for the annuity. It also depends on how much you need that money. Maybe you have planned to use that large sum for something specific. But be careful about considering the taxes.

If you want more details, you can read our article on choosing between a pension or a lump sum.

Inheritance and second pillar

Now, I said that the second pillar was your money. This is true. But there is a case where you could lose this money. Or, at least, your family could lose this money.

If you die before retirement, the inheritance of the second pillar depends on whether you have it in a vested benefits account or pension account.

First, if you have it in a standard pension account and if you die, this money can be passed to your spouse or your legal heirs. This is the standard way of inheritance.

However, if you do not have heirs or a spouse, this will not be distributed according to the inheritance law. For instance, your parents will not be eligible. And this money will get back to the canton. So, if you have no heir or spouse, you may consider your second pillar differently.

For a vested benefits account, it is simpler. It is based on the standard inheritance procedure.

How to optimize your second pillar?

Compared to the first pillar, there are a few things you can do to optimize your second pillar.

Voluntary contributions to the second pillar

You can make voluntary contributions to the second pillar to fill contribution gaps.

Like for the first pillar, you can have holes in your second pillar. Contribution holes (or gaps) can happen in several cases. For instance, if you started contributing late due to your studies or were unemployed for some years. If you leave Switzerland, you will stop contributing too. Finally, it generally happens because your salary is higher now than before. Therefore, you could contribute more now because your salary would have allowed you to contribute more.

You can fill these holes (or contribution gaps) by voluntary contributions. These contributions are pre-tax, too, so this will reduce your taxes. However, your employer will not match them. Moreover, voluntary contributions are always extra-mandatory. Finally, these contributions are locked for three years. It means there is no way to withdraw them before. You can ask your pension fund how much you can contribute to filling the gaps. There is an annual limit on how much you can contribute. They will also give you directions on how to perform these voluntary contributions.

If you can do it, I think it is a good way to increase your pension and lower your taxes. However, you need to be sure whether you should contribute to your second pillar or not. Be sure of your actions because this money will be locked for years. It is also money that will not return a lot of interest. But it is a safe investment. You can think of it as a long-term bond investment.

If you compare the second pillar to investing in the stock market, the second pillar will only be interesting in the short term. It will provide nice tax savings, but the interests are so low it will not return much after that.

If you want more details on the subject, you can read whether you should contribute to your second pillar or not.

Taxes

When you withdraw the second pillar, you will pay taxes on the withdrawal. This is at a better rate than if you had been taxed in the first place. But this is still a non-negligible part.

One essential thing is where you live when you withdraw your second pillar. This is what will matter for the second pillar. There can be a huge difference between different cantons. Moreover, you will also pay a wealth tax that can vary from canton to canton.

When you do the calculation, you need to take taxes into account. This could help you decide between a lump sum and a pension. And you may want to consider this when you move to a new place.

Change employer

Another thing you can do is choose a company with a better pension fund.

Of course, this is impractical, and the pension fund should probably not be the main argument for choosing a company over another. But this could make a significant difference in your retirement. You can also ask your company if there is an option for investing more in the second pillar. Indeed, at some companies, they give you the choice of how much to invest in it. And some companies can even match your extra contributions.

Increase your income

As for the first pillar, increasing your salary will increase your contributions to the second pillar.

Then, it will increase your final pension. Do not forget that contributions to the second pillar are pre-tax. But of course, increasing the salary is not always possible or even what you want. And increasing your salary is an obvious choice if you can do it in good condition.

Withdraw the second pillar before retirement

You can withdraw money from your second pillar before retirement (early withdrawal).

The main reason for early withdrawal is to buy a house. Indeed, you can withdraw your second pillar money to build or buy a house. It will reduce your pension accordingly. But it can help you to have the funds for the down payment on your house.

However, this will only work for your primary residence and the place where you live! You cannot use your second pillar for a secondary residence. If you work in Switzerland and live in a neighboring country, you can use this money to buy a house abroad. But again, you will have to live on this property.

The same applies if you want to start your own company. You can also withdraw the money if you are leaving Switzerland. The other reason is early retirement. You can withdraw your second pillar five years before retirement age.

The case of leaving Switzerland is the most complicated. It will depend on where you are going. If you leave for an EU country, you will only be able to withdraw the extra-mandatory part of your second pillar. But that will depend on exactly the country where you are going.

There are some limitations and rules to these early withdrawals. The minimum withdrawal is 20’000 CHF. If you sell the house you bought with the second pillar, you must repay what you withdrew.

Voluntary contributions into your second pillar after early withdrawal will not be tax-free. After you have reached the same amount as before the withdrawal, they will be tax-free again.

Be careful that after 50 years old, you are limited in what you can withdraw. After 50, you can only withdraw the amount when you are 50 or half of what is available. The limit is the maximum of these two numbers. Finally, withdrawals are only possible every five years.

Reporting

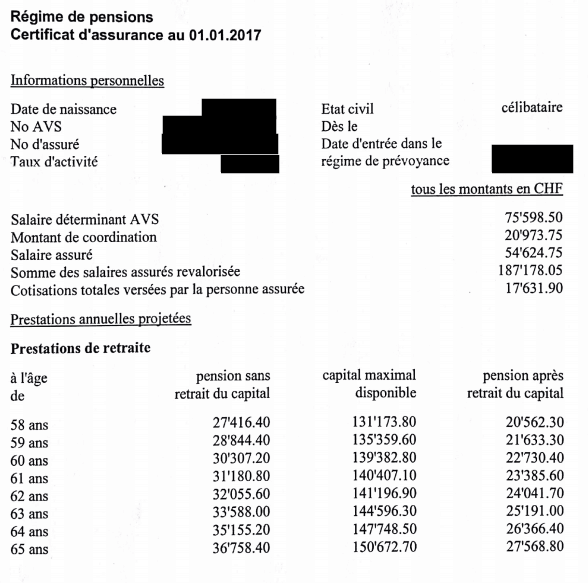

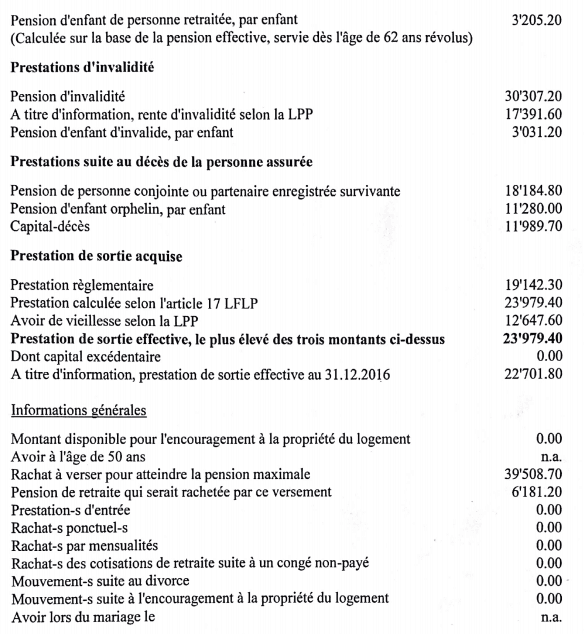

Every year, you should receive a report from your pension fund telling you many things. It will give you information about how much you contributed, the mandatory and extra-mandatory parts… It also predicts how much you will have by retirement. You should not bother too much about the predictions. But it is interesting, nonetheless.

This report differs for each pension fund, but most information will be the same. For instance, here is my redacted report from 2017:

As you can see, there are tons of numbers here. It will also cover things like death or pension in case of handicaps. If you are married or divorced, you will have more information than me.

If you are lucky, you will receive reports more often. And if you are fortunate, your pension fund will have a web portal where you can see this information online. It will depend on your pension fund. My new second pillar company updates its online portal monthly. I can track it much better now.

You should always keep these reports if you receive them in the mail (I scan them). They contain important information for your financial future.

Accounting for your second pillar

If you are tracking your net worth (and you should!), you may consider the second pillar inside it.

I integrate my second pillar in my net worth and count it as bonds. Since it is a very safe and conservative investment, counting it as bonds in my net worth makes sense. Adding your second pillar to your net worth will give you a better picture of your assets.

FAQ

What is the second pillar in Switzerland?

The second pillar is an occupational pension. Every person who works in Switzerland and receives a salary of more than 22,050 CHF per year is eligible for this pension.

How much will I receive from the second pillar?

How much you will receive will depend on how much you contributed. It will also depend on your last salary. Finally, some second pillars have better conditions than others. You can ask your second pillar provider to estimate how much you will receive at retirement.

How can I optimize my second pillar?

You can make some voluntary contributions to your second pillar. But remember that these contributions will be locked in your second pillar until you can withdraw them. You can also increase your salary to increase your second pillar contributions.

Conclusion

The second pillar is the second part of the retirement system in Switzerland. It will cover a larger portion of your salary in retirement than the first pillar. While the first pillar is for everybody, the second pillar is only for employed people.

How much you get at retirement will mostly depend on your salary. Under normal circumstances, with your first and second pillars together, you should gain a pension of about 70 to 80 percent of your salary. If you want to complete this, you must use the third pillar. I will cover the third pillar in the next post of this series. It is an optional part of the retirement system but has many advantages.

To continue learning about the retirement system in Switzerland, read about The Third and Final Pillar.

What do you think about the second pillar? Do you have tips to optimize it? Do you have any questions regarding the second pillar?

More reading

First Pillar: All you need to know to retire in Switzerland

Understand the First Pillar (AVS). Learn how the Swiss state pension works, how much you contribute, and what retirement benefits you can expect.

What should you do with a life insurance 3a?

Life insurance 3a is a poor investment for retirement. What should you do with an existing life insurance 3a? I compare 3 strategies to deal with it.

How Much Will You Spend in Retirement?

To reach Financial Independence, you need to know how much you are going to spend in retirement and it is not as simple as it seems!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste, thanks thanks thanks! :)

so if I correctly understood, the 2 pillar is good to save taxes and as long as you are more or less 15 years to your pension. and we should see it as bond.

In my case, I’m lucky to earn good money and I’m also 25 years far from the pension.

should I lodge something like 20K a year and invest the tax saving into stocks as you suggest?

do you have a way so that I can calculate how much money I should lodge considering the 2pillar ROI? I have 300k of possible voluntary lodgment (I started late in CH) and I was planning to fill it in 6 years, but after this article I’m thinking I should lower a lot the voluntary contributions or just start them when i will be 55-60 yo…

thanks again!

Hi,

Yes, you understood correctly. If you are 25 years away, you should only invest if you have very marginal tax rate and if you want some bonds. Because over 25 years, stocks will always outperform the second pillar even with the savings reinvested.

I would indeed not put 300k in 6 years. Also keep in mind that the more you put in a single year, the less each extra CHF inside is interesting (marginal tax rate lowers).

Without knowing your full situation, I think that 20-30 a year is more reasonable. But for some people 50K a year is also fine.

Hi Baptise,

Always great content, many thanks!

I’ve recently gone self-employed, although 2nd pillar is not mandatory for self-employed person, what’s your opinion about it? Is it sensible to buy myself the 2nd pillar, or more smartly investing the fund? I do max out my 3rd pillar payment.

Thanks so much for shedding some light :)

Vanessa

Hi Vanessa,

It’s difficutl to say exactly for which situation. If you have a a very large income, the second pillar may be interesting for the tax deductions. But over the long-term, stocks will beat the second pillar. Should You Contribute to Your Second Pillar in 2023?

Hi, thanks for such amazing posts.

Imagine I do an early withdrawal of Pilar 2 for buying a home. After that, all my Pilar 2 contributions will go to cover the gap of my early withdrawal. Does that mean they will not be tax deductible anymore until the gap is covered?

If that’s the case, does it still make sense to make additional contributions if I’m planning to buy a house in 3 years?

Thank you

Hi Nic,

You are correct. As long as you have a hole for early withdrawal, contributions to fill that hole are not tax-deductible.

If you are planning to buy a house in the next years, it can still make sense if you want to keep that money in the second pillar since it will be deductible. But in most cases, if you plan to withdraw most of your second pillar, voluntary contributions are not that great 3 years before. Although, they are better before than after since after , you will first need to fill the hole.

Hi Baptiste,

I’m trying to figure out if one could voluntarily increase the LPP contribution (i.e. by law set to minimum 7% for under 34). My employer has set the 7%, but I know that there are employers who allow the employees to choose a higher contribution rate.

Do you know if I would choose voluntarily to contribute 10%, the employer would be forced to pay the 5% and myself the other 5%?

Thanks in advance,

Adrian N

Hi Adrian,

You can do that only if your pension fund allows it. If the pension fund does not allow it, you cannot raise it yourself.

Also, you have no way to force the employer to pay more, and you cannot pay more than the employer. So, you are very limited in what you can do.

Dear Baptiste

Thanks for the clear, concise and informative information about the 2nd pillar. Super helpful!

I have ca 461k in a vested benefits account plus about twice that in a U.S. 401k. I’m above 65 years old and want to start spending my savings! I’m still working part-time, self-employed; I work enough to cover my monthly expenses but want to access my savings to fund travel, artwork, and similar indulgences.

Based on your article and the PostFinance tax calculator you linked to, my idea is to withdraw 10% annually from the 2nd pillar account annually. The taxes for that amount look to be 4.5%, which seems ok. I plan to keep the US 401k in reserve and start tapping into that when I stop working.

Does this plan make sense to you? Any downsides that I should be aware of?

Also, the 2nd pillar funds are in CS Mixta-LOB 45 Index fund. It does ok-ish. I’m not inclined to transfer it elsewhere mostly due to the hassle factor. Any comments about that?

Thanks so much for any tips/insights you might have!

Hi Veloman,

Thanks for your kind words.

Unfortunately, there is a large flaw with your plan. You cannot partially withdraw from a vested benefits account. You will have to withdraw it in full, and with that amount, you will pay large taxes on the withdrawal.

Also, remember that you cannot keep your vested benefits account forever. Before, we used to be able to keep them 5 years after the official retirement age. Starting in 2024, this will only be possible if working. So you may only have a few years left to withdraw it.

Now may not be the best time to withdraw, but you should probably plan for a withdrawal in the next few years and transfer that into either a broker or a robo-advisor, whichever suits you best.

Indeed, its unfortunate that Switzerland insists on totally clearing out pension accounts rather than doing it little-by-little as is the case with the 401k in the US. One idea, however, if the money is still in a 2nd pillar, is to transfer it to two vested benefit accounts and close each of them down sequentially.

Here’s what finpension has to say on the issue:

https://finpension.ch/en/how-to-split-your-pension-fund/

Of course, whether this is worthwhile, or even possible, depends on your personal circumstances.

There are some inaccuracies in this article that should be corrected. Specifically, the section on vested benefits has two errors. If you retire early, you can access the funds before 65 for a man and 64 for a woman — you can access the funds up to five years before the official retirement date. And, if you leave Switzerland, you can take the vested benefit funds with you at any age, subject to withholding tax.

So, the following is untrue:

The same is true if you leave Switzerland. Until the age of retirement, you will have to keep the money in a vested benefits account.

If you retire early, you will also keep the money in a vested benefits account as soon as you quit your job. It will stay there until the official retirement age.

Thanks, I will refresh that section.

hi Baptiste,

Do you know if it is possible to compare the historical effective interest rates for different 2nd pillar pension funds in Switzerland? I could find only one from Credit Suisse Pension Fund:

https://pensionskasse.credit-suisse.com/en/our-service-for-you/media-and-news/translate-to-english-news-detail/interest-rate-for-the-pension-fund-in-2022/

Maybe most of them are in German that don’t appear in my search.

Hi YYY,

I never found comprehensive data on the subject either. It’s relatively easy to find information for the last year because it gets announced in newspapers or things like VZ, but something with more than a few years is much more difficult to find.

So you’re telling me I can retire early/quit my job and move my 2nd pillar savings to a Vested Benefits and then invest it via finpension just like my 3a account? So I get actually decent returns from 99% stocks as opposed to the savings getting eaten by inflation or barely beating it in traditional 2nd pillar accounts, plus lower fees?

And then on top of that I can choose to get still get an annuity of (currently) 6.8% when I reach the actual retirement age?

This is a big game changer for people looking to retire early and I’m very surprised that this is the first time I’m hearing about it.

Yes, you can transfer your 2nd pillar to a vested benefits account and invest it nicely when you stop working.

However, most vested benefits accounts won’t allow you to get an annuity. With Finpension 3a, you can’t get an annuity, only a lump sum.

Thanks for the info Mr. Swiss! Fascinating stuff.

Well detailed article. Thanks!

I’ve some questions:

1) Will the 2nd pillar contribution be separated after marriage (and not manipulated like the 1st pillar at 150%)?

2) If so, at retirement age (e.g. both in the couple at 65), if we take our 2nd pillars contribution with annuity mode, how can we calculated the net amount? Shall I sum future couple 1st pillar annuity + future 2nd pillar annuity and then use a common net salary calculator?

Thanks!

Luigi

Hi Luigi,

1) It won’t be manipulated, you will get two individual pensions.

2) You should check out how much deductions you will get after retirement and then indeed, you can add the two pensions + the 150% first pillar and adds them and remove the deductions and that should give you a good estimate. Keep in mind that this may change until you are retired.

Hi Baptiste,

Can you elaborate please on the scenario when one makes their salary by working for more than one employer with a salary paid by each of them lower than the required 21K but the combined total of all salaries being above the 21K.

Can the 2nd pillar be claimed in such a case and how?

Obviously the different employers would not know on their own that payments for 2nd pillar need to be initiated. And, each employer may deal with a different pension fund. What should the employee do?

Hi Stoyan,

That’s an excellent question and not a well known subject.

If you have two salaries and none of them amount to the minimum but the total is higher than the minimum require, you have two options

* You can ask one of your two companie’s pension fund it they could take you in considering both of your salaries (I don’t know the conditions of the pension fund for that)

* You can get affiliated directly at the Fondation d’institution supplétive (more information in English here) and they should take anyone that has the two conditions fulfilled.

I should definitely write more about that.