Revolut Review in Switzerland 2026: Pros & Cons

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

A major issue with many payment cards is their tendency to impose high fees on foreign currency transactions. For instance, if your currency is Swiss Francs and you make a purchase in dollars, you’ll be required to pay a certain percentage of the transaction cost. Often, card issuers charge over 2% in fees for such transactions. Fortunately, Revolut offers a solution to this problem.

Saving money on foreign transaction fees is made easy with Revolut. Unlike banks that typically offer unfavorable exchange rates, Revolut provides you with the best available exchange rates. If you frequently purchase items in other currencies or from different countries, having a Revolut card is essential to keep your expenses in check.

On top of that, Revolut has many other services.

| Monthly fee | 0 CHF |

|---|---|

| Users | 15’000’000 |

| Card | Mastercard prepaid |

| Currencies | CHF and more than 20 |

| Currency exchange fee | Small markup for small amounts, then extra on weekends and large amounts |

| Top-up CHF | Free with Swiss IBAN |

| Languages | English, French, German, and Italian |

| Other features | Stocks, cryptos, … |

| Depositor protection | 0 CHF |

| Established | 2015 |

| Headquarters | London, United Kingdom |

Revolut

Revolut is a company from the United Kingdom. They are pretty young. They started in 2015. They offer a prepaid debit card. Except in a few cases, there is little difference between both (unless you want to go into debt).

With Revolut, both MasterCard and Visa are available. They are almost the same for most usages. You can use it online and even withdraw money at an ATM. They offer two types of cards:

- Virtual Debit Card: You can generate it in your Revolut account. You can use it online with its number.

- Physical Card: You can order a physical debit card for a small fee.

But the interesting thing about Revolut is that foreign exchange transactions are cheap! There are no foreign exchange fees. However, while Revolut used to provide the interbank exchange rate, they do not anymore. Since 2023, they have provided the Revolut Exchange Rate, which means nothing, except that they can now add their own surcharge.

So, foreign exchange transactions with Revolut are not free anymore. On average, users are reporting about a 0.4% surcharge.

This surcharge is still better than many banks. But there are some interesting alternatives at this level.

It is entirely worth having a new card for these savings. Moreover, since my employer’s headquarters is in the United States, I may travel more than usual, which means I will save even more money.

Since its inception, Revolut has started offering many new features:

- Support for cryptocurrencies directly from the application.

- Premium and metal plans for users that need even more features

- Saving vaults for your money with saving goals

In 2019, Revolut got a European Specialized Bank License! It is a big deal for the company. They operate as banks in EU countries, but not yet in Switzerland. When operating as a bank, your deposits are protected by the European Deposit Insurance Scheme (EDIS) up to 100,000 EUR.

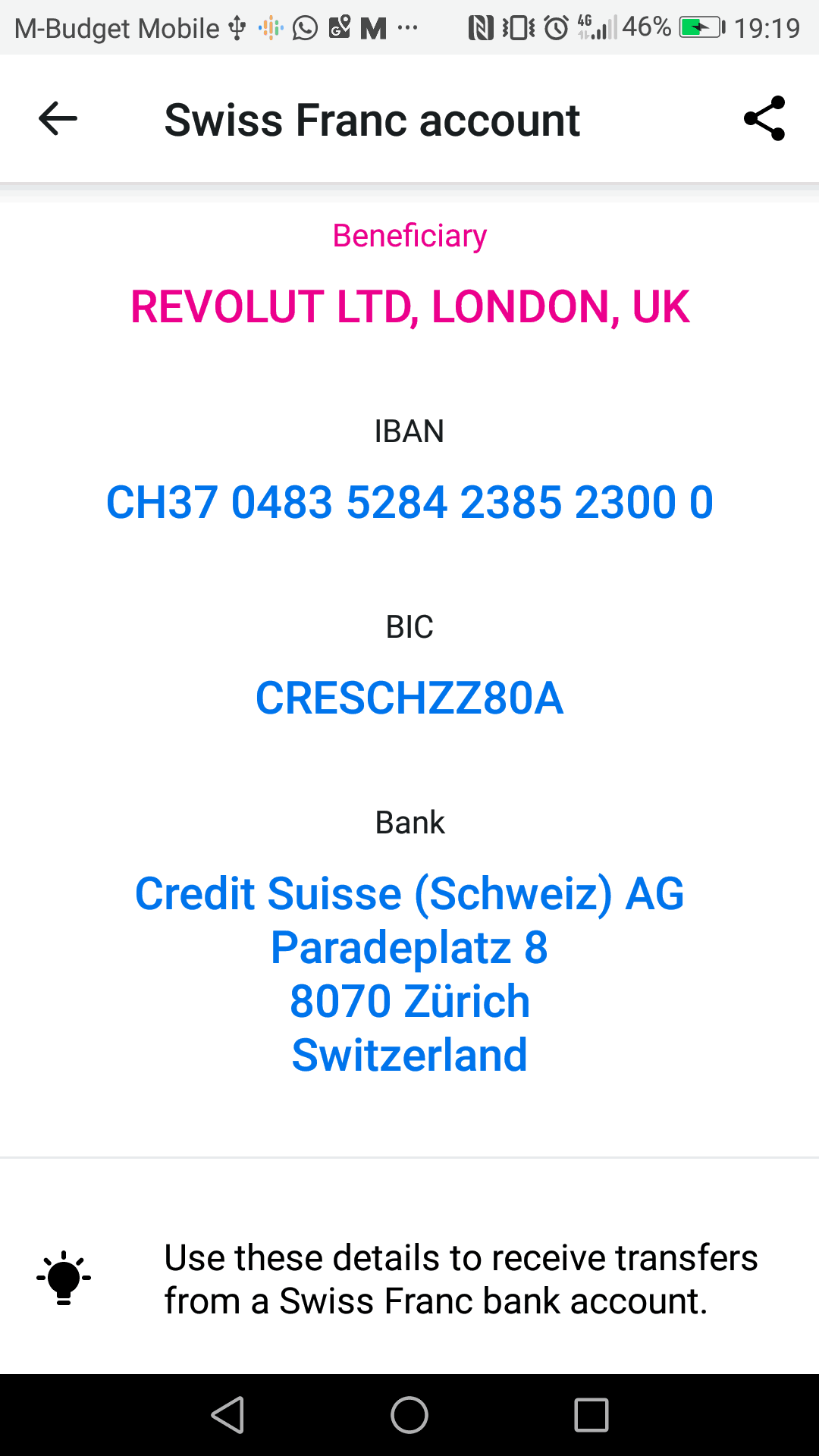

At the same time, Revolut obtained a Swiss IBAN. This is an essential point for Swiss users since it allows them to easily top up their accounts for free.

If you plan to use Revolut to save money on foreign fees, you will be okay with the free Standard plan! You can always upgrade to another plan later.

2025 changes and individual Swiss IBAN

Start in late 2024, Revolut stated implementing some changes for Swiss customers of Revolut. After the migration, users are now working with the Revolut UAB entity.

Each user now has what they call an individual Swiss IBAN that is unique for each customer. Unfortunately, these IBANs are not in the name of the customer name, but instead in the name of Revolut UAB. This means that Revolut still operates as a wallet. And this means that any transfer to these accounts still needs to add the beneficiary in the changes.

In theory, this gives us deposit insurance since the accounts are managed by PostFinance. However, since the accounts are in not in our names directly, I am not convinced there is much protection to be had on our CHF balance. Additionally, the fact that accounts are not in our name means it is not convenient for inbound transfers.

Overall, the 2025 changes did not bring much improvement.

Sign up for Revolut

Now you are ready to sign up for Revolut. You have to install the application on your smartphone. There is no way around it. It is excellent for most people. But for people like me who dislike phones, it is not perfect. But I guess I have to live with mobile apps now!

Nevertheless, it is pretty straightforward. You can go to the Revolut website to get a direct link to the application to download. You can also search for Revolut in your phone application store (Google Play or App Store).

Once you have installed the application, you can go through the registration process. You will have to enter standard information about yourself. You will also have to scan your ID. At some point, you will have to top up Revolut for authentication. You can use your Wise card now to top it up. And this will be free!

Once you have done this, you can start using a virtual card or order a physical card. You must pay 6.99 CHF for the delivery if you order a physical card. It should be the only time you pay anything to Revolut. My card arrived quite quickly, four working days, I think.

How to Top Up Revolut for Free

Since the Revolut card is a prepaid debit card, you must top it up. You cannot use it if you do not have any money on your card. You have several choices to top it up:

- A debit card issue in your country: Free!

- A credit card issued in your country: Expensive!

- Another debit or credit card: Expensive!

- A bank transfer: Generally free!

You should only use free options to top up your account. Anything else does not make sense. There is no point in spending more money than what you will save on foreign exchange fees. So, two options make sense:

- a top-up from a debit card from your country

- a bank transfer

Top Up Revolut with Swiss IBAN

You can directly transfer money to your bank account.

Revolut offers a Swiss IBAN in Swiss francs. You can transfer money directly from your Swiss bank account into Revolut. And this is a real CH IBAN from a Swiss bank! You will not pay any fee for the transfer!

Revolut offers bank accounts for most European countries, making it straightforward to transfer money from most countries.

You can now transfer money for free to your Revolut account directly from your bank account. You only need to wire money from one account to another to top up your account.

To do this, go into the app and click on Add Money (The big button is like a plus sign). Then, you can select “Transfer to your Revolut account”. They will give you all the information necessary for a bank transfer to their account. Be careful when you enter the reference number because this is how they will identify you.

Once you have sent the payment, the money usually takes one working day to appear in your account.

Detailed Revolut Fees

I said foreign transactions are cheap with Revolut. Unfortunately, this is not always true, even with Revolut. There are a few details that are important to know.

First, not all currencies are treated equally by Revolut. There is a 1% fee for Thai Baht, Russian Rubles, and Ukrainian Hryvnia, while all other currencies are free.

However, there is a monthly limit of 1000 GBP for free transactions. It is equivalent to 1000 GBP (1250 CHF) for other currencies. You will pay a 1.0% fee if you exchange more than this.

Furthermore, the rates are different during the weekend. Revolut will charge a 1.0% extra fee on each exchange transaction during the weekend. You can find more details on the official Revolut price explanation.

In the best case, an exchange costs about 0.40% with Revolut. In the worst case, it can be expensive, with a 2.5% fee. You need to be careful when doing your exchanges during the week. Be aware that some currencies will charge you more. And you should avoid using Revolut for large transfers as well!

Finally, it is worth restating that Revolut no longer offers interbank exchange rates.

Alternatives

We can quickly compare Revolut with some alternatives.

Revolut vs Neon

All the services you need to pay, save and invest, in a neat package, with extremely good prices!

Use code tpsummer to get one year of Neon Plus and your debit card for free!

- Invest with great fees

In Switzerland, Neon is a big contender to Revolut.

When you pay with the card, all currency exchanges are cheap with Neon. Revolut has some limits on cheap exchanges. However, Neon uses the Mastercard exchange rate plus a surcharge, which is about 0.75% worse than the interbank rate. Revolut provides the so-called Revolut Exchange Rate, which is also about 0.4% pricier than the interbank rate. So, in some cases, Revolut is cheaper than Neon, but in others (weekend for instance), Neon will be cheaper. However, the Revolut Exchange Rate is less transparent than the Mastercard Exchange Rate.

On the other hand, bank transfers in other currencies are not free with Neon. These transfers are generally cheaper with Revolut. Also, Revolut is a multi-currency account. Neon only lets you hold Swiss Francs.

As for reputation, Revolut has a poor reputation with many issues. Neon is currently free of controversies and has a good reputation in Switzerland.

Since I started using Neon, I have not used my Revolut account. I prefer Neon to Revolut for their safety and professionalism.

To learn more, read my comparison of Neon vs Revolut.

Revolut vs Wise

Wise is probably Revolut’s biggest competitor.

Revolut and Wise are digital bank accounts focusing on currency exchanges at a fair price.

Overall, Wise has a much better reputation. Many controversies tarnished Revolut reputation.

Both services are on the same price level.

- Wise has fees on each currency conversion, which is very transparent.

- Revolut has a surcharge of 0.40%, which is not transparent and not visible in the app.

- Revolut has free conversions for up to 1250 CHF per month.

- Wise prices are simpler than Revolut fees. Indeed, Revolut has different fees during the week and weekend. Revolut also has different fees for different currencies (called exotic prices).

While Wise focuses on its core business, Revolut tries to do everything from its app. Indeed, Revolut offers crypto, stocks, and commodities from within the app. You can even book stays using the app. I do not see this as an advantage. I prefer having a few apps doing a good thing than a single app trying to do everything.

I should also mention that Wise has been profitable for a while Revolut only had a single profitable year since its creation.

Overall, I prefer Wise over Revolut for its reputation and for not trying to do too much. But both apps are interesting. Since the latest changes in 2023, Revolut is no longer cheaper than Wise.

For more information, you can read my detailed comparison of Revolut vs Wise.

Revolut vs N26

Of the main competitors of Revolut in Europe is N26.

Both Revolut and N26 are digital bank accounts. Both have a bank license, but Revolut has not yet implemented it. So, N26 has a slight advantage in terms of regulations and safety.

Interestingly, both companies have a poor reputation, which has generated several significant controversies.

N26 is cheaper than Revolut since all primary services are free. Indeed, payments in other currencies are always free with N26. However, Revolut has some substantial limitations. Also, N26 allows you to withdraw EUR for free in your country five times a month, while Revolut only allows 200 EUR per month.

When it comes to Switzerland, N26 has very poor support of Switzerland. Indeed, they have no Swiss IBAN. So you have to deposit EUR into your account, which is inconvenient for people.

Also, N26 does not support CHF in the app. This means that you cannot have a balance in CHF and that any payment in CHF will go through a currency conversion with the card provider, which is not free.

So, N26 is probably better in Europe, but Revolut is much better in Switzerland.

To learn more about these two, read my detailed comparison of N26 and Revolut. Or, you can read my review of N26.

Revolut FAQ

Is Revolut a bank?

Revolut has a digital banking license, that makes it a digital bank. However, since they got that license after getting started, many of their accounts are not under the license.

Is Revolut free?

It depends on how you use it. There are limits under which it is free. For instance, you can convert 1250 CHF per month for free, during weekdays, but you would have to pay a fee during the weekend. So, make sure you check their fee schedule in advance.

Who is Revolut good for?

Revolut is good for people that want to use this card to travel and pay relatively low fees abroad and in foreign currencies. These people should not hold too much money on their accounts.

Who is Revolut not good for?

Revolut is not good as primary bank account. It is not good if you a transparent exchange rate or want to hold a lot of money on your account.

Revolut Summary

Revolut offers a debit card without any fees for currency exchange. On top of that main feature, they have plenty of advanced features such as stock trading, cryptocurrencies and sub-accounts.

Product Brand: Revolut

3

Revolut Pros

Let's summarize the main advantages of Revolut:

- Cheap currency exchanges during the week.

- Can hold many currencies in the account.

- Very fast transfers to other users.

- Fast transfers to other bank accounts.

Revolut Cons

Let's summarize the main disadvantages of Revolut:

- Very poor transparency on exchange rates

- Expensive during the weekends.

- Free exchanges are limited to 1250 CHF per month.

- Expensive for some exotic currencies.

- Revolut has a poor reputation.

- There are reports of many people getting their accounts blocked and losing access to their money.

Conclusion

I like using a travel card. It is free and saves me a lot of money each year. Every time I travel to another country, I use my travel card to pay for everything! I have never had any issue getting it accepted anywhere.

I am also using it to pay online on foreign websites. For instance, I often have to pay in EUR or USD if I order something on eBay. With my Revolut, the conversion is free at an excellent exchange rate!

A travel card is a perfect companion to your local payment card.

However, many people had issues with Revolut and got their accounts blocked without proper communication. There are also many negative online reviews about Revolut. So, you should still be careful not to trust Revolut with too much money.

I never had a lot of money in my account. My rule is not to have more than 500 CHF on my Revolut account.

All the services you need to pay, save and invest, in a neat package, with extremely good prices!

Use code tpsummer to get one year of Neon Plus and your debit card for free!

- Invest with great fees

If you do not want to trust your money with a foreign bank, you could use Neon bank for your purchases abroad. They also have free transactions in foreign currencies and abroad. This means you can have the advantages of Revolut with the benefits of a local bank. For more details about how I use cards, read about my entire payment card strategy.

Although I still have my Revolut card, I mainly use my Neon card now. It is more practical, more transparent and about the same level of fees.

Finally, if you do not know what to choose between Revolut and Wise, I have written an entire article about Revolut vs Wise.

Have you ever tried a Revolut card? Which payment card do you use?

More reading

7 Simple Steps to Change Bank Account in 2026

Switch banks easily. Follow these 7 simple steps to change your bank account in Switzerland without stress and start saving on banking fees.

wiLLBe Review 2026 – Pros & Cons

wiLLBe is an account by the LLB, in Liechtenstein, with a nice interest rate, low fees and good withdrawal limits. We review it in details.

N26 in Switzerland Review 2026 – Pros & Cons

N26 is a European digital bank account that offers free international conversions! Learn everything about N26 in my full unbiased review!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

What do you think about Revolut Invest? Especially when it offers 5 free commission trades right now on premium accounts.

Hi Matteo

On paper, it’s not bad, but I still have some doubts about putting much money on Revolut. I am not entirely convinced by their security. But I have not done a full review of their services.

The summary is not up-to-date:

> Currency exchange fee Free for small amounts, then 1.0% and weekend 1%

It’s not free for small amounts now that Revolut uses a made-up currency exchange rate.

You are right, I forgot to update the summary, will do it now! Thanks!

Note that they removed the fees when topping up the account with a Swiss credit card, as long as you moved your account to Revolut Switzerland

Payments AG (which they nag you to do):

> Stored card: free. […] If you are using a non-commercial card that

has been issued in Switzerland and you have been onboarded to Revolut Switzerland

Payments AG, no additional fee will be charged.

Source: https://cdn.revolut.com/terms_and_conditions/pdf/personal_fees_standard_for_swiss_clients_of_revolut_bank_uab_59eb6320_1.1.0_1744275460_en.pdf

Hi Paul

Have you tried it yourself?

That could be convenient indeed. But what do they mean by a non-commercial card?

I tried the other day and it worked without issues. I didn’t have any fees whatsoever when I topped the account in CHF using my Swiss credit card.

With “non-commercial card” I think that they mean that you are not allowed to use your professional credit/debit card to top-up your account. I don’t know if it is actually enforced or if they even have a way to know if you do.

Thanks for sharing, Paul. This is good indeed. I will update the article accordingly.

That’s a fair interpretation.

My 2cents on this. The new Iban works flawless, I am using it for a couple of months. I top it up the Revolut for monthly expenses in €, either when i go to germany/france or to top up my Bank Account in Portugal, and online Shopping with virtual cards.

It is Perfect for Holidays in particular with Apple/Google pay.

So, in the end I don’t have “life changing money” there that I should worry about protection. I would choose a Swiss bank app for that.

Thanks for sharing, Hugo.

I agree that for temporary money, it’s fine.

What bothers me is that they brand this as individual IBAN, but it’s not individual if it’s in their name, not ours. So, I would still not trust it as a main or even secondary account.

I fully agree, it’s even more disingenuous considering that even with your “personal” IBAN you are still required to put a special string in the remarks field of all transfers or you won’t receive the money.

So for CHF it’s literally the same status quo as before, just that the IBAN is from Die Post instead of Crédit Suisse/UBS.

Exactly, despite all the marketing buzz, the status quo remains.

I’ve used the old account these days to tranfer some money. This is what Revolut sent:

“We’ve noticed that you’re using your Swiss IBAN (provided by Credit Suisse/UBS) to receive payments to your account. Please note that this IBAN will be deactivated by 30 June 2025.

After this date, any payments sent to this IBAN will be rejected and returned to the sender’s bank.”

Sounds to me like the rest should continue working. With the above experience of the new account and my similar concerns, will see if the switch will be forced at some point.

Hi AG,

Thanks for sharing this. It seems indeed like only the Swiss IBAN will be impacted in the end.

But then how are you going to top up your account? If you do it by card, you will pay fees.

All other currencies, except CHF, can be transferred to a UK acount (at least for me as I started using Revolut in the UK). So I will use my UK account to transfer GBP (or EUR) to Revolut for free.

Fully aware that not everyone might have that option via a “spare” UK account.

That is, if I will keep using it, as the currency conversion from CHF to EUR/GBP within the monthly free limit is/was my main usage. And virtual cards, but Wise has those as well.

And going off-topic for a bit, I recently signed up for a Bank Wir Top account which sounds very good to me. If this works out the way I imagine, I might use that one for most foreign payments (no conversion fees and Interbank rate). And it’s a more reliable brick-and-mortar bank. As I do agree with some comments/concerns, I also never put much money on Revolut.

Hi AG,

That’s a fair point, some people may have extra accounts to feed their Revolut account.

Yes, WIR Bank top should be a strong alternative for paying with the card. But the interbank rate does not apply to bank transfers in other currencies.

Hello,

We use Revolut frequently, my wife and son (Junior account) with the free plan and i have a paid plan.

My wife wants a simple place to invest a monthly amount in ETF’s (I use Interactive Brokers, but she does want something more easy to use), and Revolut seems preety smooth. As example, clicking in Invest and selecting ETF’s, and then the Vanguard SP500, tha app shows all the details of the ETF, and even an estimation of potential gains over 20 years according to a selected monthly investment amount (549k in 2045 for a 200/month amount). In my case it is even “commission free”.

She finds that awesome and very user friendly, however I would like to talk her in to an alternative, because I will sleep better if she has several hundred thousands francs on a different bank than Revolut.

I love Revolut, don’t get me wrong, we use it often as a payment system. I am just not sure it is the place where I want to place a big part of life savings/investments. Do you find it too paranoid?

I have seen your reviews, especially the Swissquote vs Yuh, but I did not got into a conclusion:

for single/two transactions of a few hundred francs monthly, eg 300-500, what would be the best in terms of:

– fees (mainly US ETF)?

– simplicity/easy to use?

Thank you and have a nice day,

Hugo

Hi Hugo

I think that’s a totally fair point. Revolut is a great payment system, but I still have doubts about holding large sums of money with them. Until very recently, they even had no bank deposit protection for Swiss customers.

I would add that an estimation of 549k with 200 CHF / month is not realistic, it requires a 19% yearly return. Even the S&P500 does not provide such returns.

If your wife wants something really simple, either Neon or Yuh would be great. They are both very simple, on the level of Revolut and are relatively cheap.

Hi Batiste,

Thanks for your reply. I found it also not so realistic, but did not do the math :) 19% average return/year is indeed a long shot. Additionally to your valid points, I read several reports of a less than satisfactory customer support, and in an era of full digitalization, where we can do almost everything without a face to face contact, one of the things I value the most is how a service provider reacts when I need their support.

Yuh seems very easy to use, intuitive interface. I think we will go for it.

Have a great day,

KR,

Hugo

Neon just added a surcharge cost on exchange rate of 0.35%. This will lead to a 0.75% cost for each transaction abroad. Still the best?

Hi Giulio

Yes, as of today, new plans have changed. Current users are being migrated (me included) until mid-May where the new plans will become the norm for all users.

And correct, adding 0.35% to 0.40% for Mastercard makes a total fee abroad of 0.75%. There is the option to pay 2 CHF per month to get back this fee and get a free withdrawal.

I will update my articles in May to reflect these changes. I still do not know exactly what I will do with my own account, other accounts are becoming interesting now but I probably don’t want to go to the trouble of changing.

I am a big fun of this website, so I felt obliged to share my opinion. This particular article sounds like bashing Revolut and promoting Neon. It is very biased, which is totally unlike other articles. Also, the arguments why one should use Neon are not compelling, and not complete.

Could you expand on what you feel is biased in this article?

This article was likely written before any Neon content, so I do not feel like Neon had any influence over it.

As of this time, not all Revolut users have any deposit guarantee (this is starting to come for new accounts, but not all older accounts, like mine) and the cheap usage is much more limited at Revolut. It looks like all my comparisons still stand today.

Hi

what about revising this article, taking into account the not any more so recent offer of a “swiss iban”, which seems to mean having an account with a lithuanian bank and using for payments and banking services the Revolut Bank UAB?

I really do not know what to think about this offer, which is being resubmitted again and again to the client from Revolut.

Good thing, bad thing, what is your opinion?

https://www.lb.lt/en/sfi-financial-market-participants/revolut-bank-uab

Hi Giacomo

The problem is that previous accounts have not been transferred to the new structure. So I cannot really test it.

On paper, it looks good. Once (if?) my account is transferred from Revolut Ltd to Revolut UAB, I will do a more thorough update and review of this article.

Hi

I think it is about time to decide if abandon Revolut or accept the Swiss Iban policy (We rely on the infrastructure of PostFinance to give you a unique Swiss IBAN. However, your Swiss Francs will be held by Revolut Bank UAB, not by PostFinance. Similarly, we do not provide you with an account by PostFinance.), switching to Revolut Bank UAB (meaning too that “Governing law: Lithuanian law will apply after your migration date.” and “Complaints handling: after the migration date, most of your complaints can be addressed to the Bank of Lithuania.”).

The frequency of the msg and email from Revolut ist escalating, they are now somewhat menacing, telling us “Time is running out to get your individual Swiss IBAN, so you can enjoy an even more seamless banking experience. Find out how to access your Swiss IBAN to avoid any account disruptions, and what you’ll get with your new Revolut bank account.”

What would be the meaning of “account disruption”?

Hi gig,

I would personally switch to the new structure when possible since it offers more guarantee for your money.

But they have not offered yet to transfer my account.

As for the disruptions, I have no idea what this means. They may have to close accounts that are not transferred in the end.

My account was finally transferred, and I am not overjoyed with the changes. With the new entity, we can get an individual Swiss IBAN, unique to each customer. But this IBAN is still in the name of Revolut UAB, which makes it as inconvenient as before for any inbound transfer. And since the account is not even really in our name, I am not sure the money is really protected anyway.

So, quite disappointed by these changes.