How to Open an Interactive Brokers Account in 2026?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Interactive Brokers is an excellent broker from the United States. It is known for its cheap fees and unique investment product range. It is being used by many personal finance bloggers, for instance.

It is currently the best broker that allows access to U.S. ETFs. And U.S. ETFs are the most efficient ETFs for Swiss investors.

In this guide, I review how to open an Interactive Brokers account. It is not very difficult, but there are a few things you need to know before you start your application. And I also teach you how to optimize your account to save money!

Interactive Brokers

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

So what is Interactive Brokers (IB)?

IB is a brokerage firm from the United States. It was created in 1978 in New York, more than 40 years ago! IB is the largest brokerage firm in the United States and the leading foreign exchange (forex) broker. Interactive Brokers offers access to many instruments, such as stocks, bonds, options, futures, and more.

Interactive Brokers is a very well-known broker with an excellent reputation. It is known to be cheap compared to its competitors. I have already compared IB and DEGIRO in the past. This comparison showed that it is even less expensive than DEGIRO, the broker I used before.

An essential thing with IB is that, by default, they do not lend your shares to other people, such as DEGIRO does by default. But you have the choice, which is good! Indeed, you also can lend shares, and you will get some of the money from the lending.

If you want more information on IB, read my review of Interactive Brokers.

Why open an IB account?

So, why did I open an IB account? It is currently the best broker available to Swiss investors.

There are many reasons to prefer Interactive Brokers over other brokers.

- IB offers access to U.S. ETFs to Swiss investors, while many brokers are not.

- IB has excellent prices.

- IB offers access to many investing instruments.

- IB offers foreign exchanges at an excellent price.

- IB has an excellent reputation.

- IB has good financial strength.

So, we will see how one can create an account on IB.

Create an Interactive Brokers account

First, prepare some time in front of you. The account creation process on Interactive Brokers is not difficult, but it will take some time. You will need to answer a few questions, and you will need to wait a day for your account to be funded.

Interactive Brokers has several entities in Europe. The primary entity is IB UK, but one is in Luxembourg, and one is in Ireland, for instance. For Swiss investors, the best entity is IB UK because they offer access to a Swiss IBAN and give you access to US ETFs. For European investors, it does not make much of a difference.

First, go to the account creation page and click “Open account”.

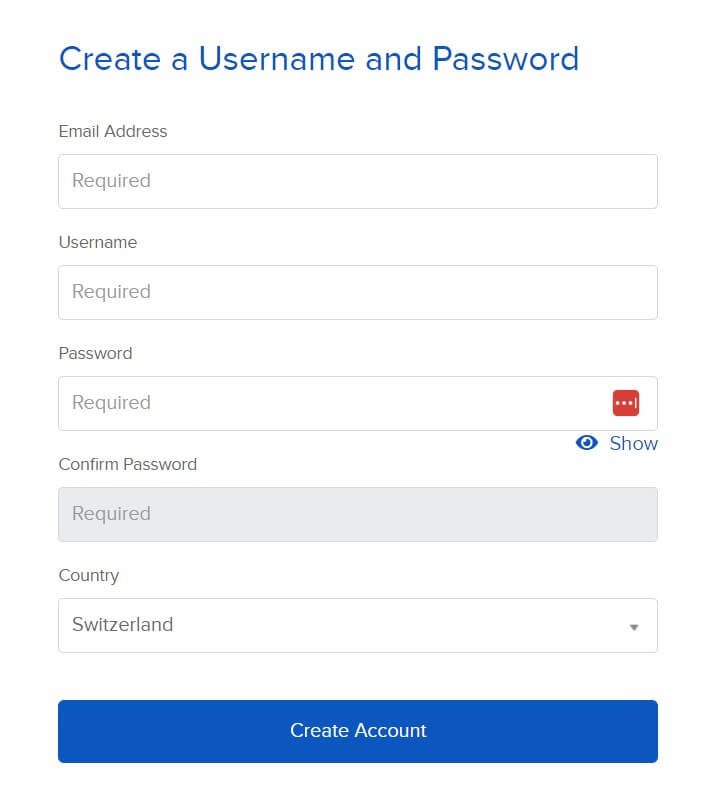

On the first page, you must enter your email, user name, and password for the account. Make sure to choose a good password and user name.

I would recommend making your password at least 20 characters long. A long password is essential to secure your online accounts! Make sure to remember it correctly as well!

You also need to enter your country of residence. If your country of legal residence differs, you must also enter it. You can then confirm the first page.

At this point, they will email you to confirm your email address. Just check your mail and choose to continue the application.

Personal information

On the second page, you will have to set your account type. I put it to Individual for this example. You can check the kinds of accounts to ensure you choose the one according to your needs. But most people will want either an individual or a joint account.

Then, you will have to enter the general kind of personal information. Nothing is special here, only what you are used to entering on each website. You will have to set your addresses as well.

Since this will be related to your taxes, it is essential to enter them correctly. You will also need to enter a valid phone number. IB will use this phone number authentication, so once again, enter it correctly.

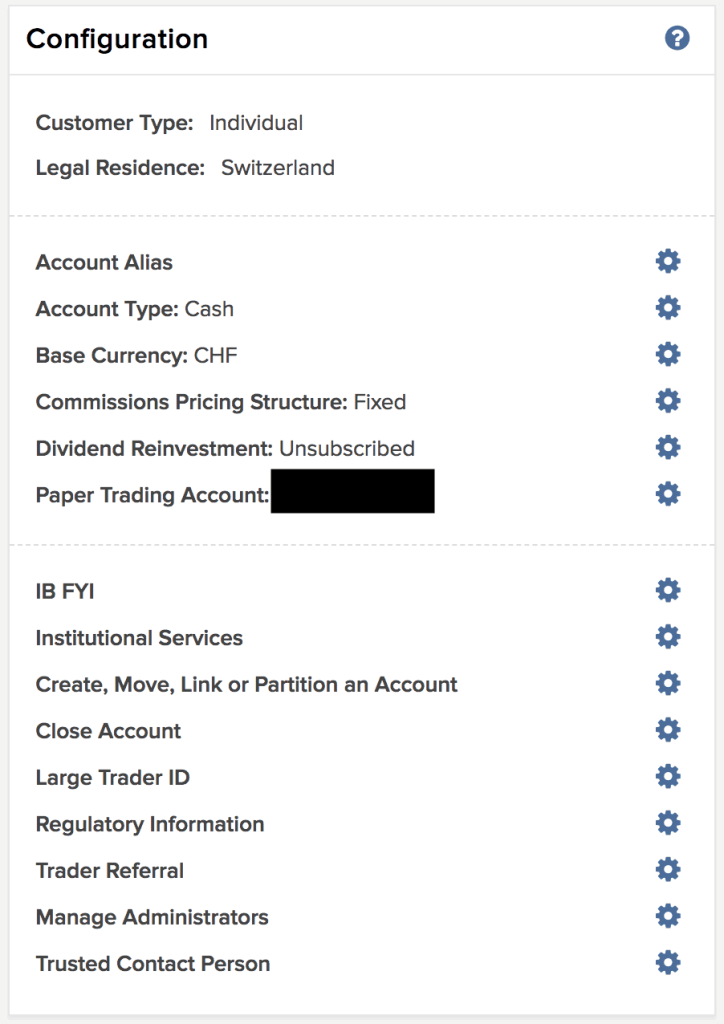

IB has several types of accounts. You will need to select the type you want. The primary type of account is a Cash account, which is the type you probably need. A cash account means you must have the money before each trade.

There are also Margin accounts (IB has some good information about margin accounts). Margin means you can use leverage for investing with money you do not have. Unless you know what you are doing, I recommend a Cash account.

Another thing you need to configure when you create an IB account is the base currency. Since I make most of my payments in Swiss Francs (CHF) and live in Switzerland, I chose CHF as my base currency.

You can always convert money from your base currency to any other currency. The base currency only matters for the interface’s display. If you select CHF, you can still transfer USD and buy shares in EUR, for instance.

Currently, the CHF balance has a positive interest rate. If it becomes negative again, you will see a warning about the negative interest rate on CHF balances. You can get the current negative interest rate and limit here.

Now, you will also have to set up three security questions. You will need these questions if you ever need to recover your account. Make sure you select questions from which the answer is not ambiguous (but challenging to find)! This procedure is, once again, a standard procedure.

Investment Questions

After this, you need to answer questions about your finances.

You need to tell how much your net worth is and how much income you have. You also must say what your objectives are for your investments. For instance, you may want to invest for capital appreciation or fixed income. All this information is here for regulatory reasons.

You also have to set which instruments you want to invest in. For instance, if you intend to invest in stocks and bonds, you must select these options. I only selected stocks. Stocks, bonds, options, and futures are among many other choices. You must also select which country (stock market exchange) you would like to invest in.

For each of the instrument you intend to trade in, IB will ask you how much experience you have with it. I would not recommend lying, but I would recommend overestimating your experience. The reason is that if you put zero experience, you will likely not be allowed to trade. So, add a few more trades per year and a few more years of experience if necessary.

In some cases, these questions will be followed by a short investment test for some instruments. You can do it multiple time, so do not be stressed out, this is normal. If you do not know, do not hesitate to use the internet to pass it (or even ChatGPT).

You also need to confirm your phone number with a code.

Confirmations

At this point, you must agree to all the rules IB has for trading. Ideally, you may want to read them. But you probably will not!

If you want, you can also join the Stock Yield Enhancement Program. This program will allow IB to lend your shares to other people. With that, you will receive half of the profits.

Of course, there is a slight risk to that, and you may also be unable to sell your shares when you want or need to. I am not using that feature now. But I have tested this feature recently, and it works well.

At this point, Interactive Brokers will want proof of your identification. For this, you can upload a driving license, an ID card, a passport, or an alien ID card for IB to confirm your identity. You will also have to enter information about your tax status on the same page.

You will also have to fill in information about your employer and job. Usually, you also need to submit something as proof of address.

Fund your IBKR account

IB will fully activate your account once they receive funding.

You need to deposit the first amount for IB to validate your account. First, you have to declare how much money you will deposit. Then, IB will give you all the information necessary for the payment.

Make sure you correctly copy the IBAN. With banking transactions, you should always double-check all banking information before transferring. The transfer will be free since they have a bank account in Switzerland!

And do not forget to include the line indicated by IB with your account number in it. Otherwise, the money will not go directly to your account, and you must contact them to resolve the issue. You must do that for all future deposits to your Interactive Brokers account.

Finalize your account

After you have funded your account, you can still do a few more things.

First, you can configure the market data. You should set your market data status to non-professional. And you should check that you are not buying any market data. Unless you plan to day trade, you do not need this data. You do not want to pay for it.

One great thing is that you have to use two-factor authentication (2FA). You have no choice. You must configure your mobile phone to use it as 2FA.

2FA is an essential part of online security. First, you need to install IBKR Mobile on your phone. This application is available for Android and iOS.

Once you have installed the application, you can register it as a two-factor authentication for your account. You will have to log in with your username and password, and you need to enter the code you received by SMS.

Finally, you can then choose a PIN for your future two-factor authentication. Remember that PIN since you must use it for each connection to Interactive Brokers.

If you do not know about 2FA and why it is necessary, read my article about online personal finance and security.

Wait for your account

At this point, you only need to wait for IB to create and fund your account.

It should not take too long. It only took one day for my account to be created and funded. It is pretty fast. The next day, I could directly make my first trade.

Optimize your IBKR account

Now that you have access to your account, there are two more things to finalize in your account.

The first thing remaining at this point is configuring the Pricing System. I recommend you use the tiered pricing system. IB is cheaper than DEGIRO when you use the Tiered Pricing system.

You can make the change in your Account Settings. If you prefer the more predictable fixed pricing, you can also opt for it. There are some cases where fixed pricing is cheaper than tiered pricing.

Here are my settings just before I made the change to Tiered pricing:

The second thing applies if you are a Swiss investor and will invest in U.S. ETFs. In that case, you need to fill out the W-8BEN form. That is pretty simple. You can go into your Account Settings. There, you can click on Profile next to your name. Then, you must click the (i) blue button next to your name below Profiles. Then, you can click on “Update Tax Forms”.

They will then take you through the process, and you can fill out the W-8BEN tax form. This form will halve the dividend withholding from your American stocks and ETFs. This step is essential if you want to profit from the great tax efficiency of U.S. ETFs.

Some people have told me that it sometimes takes about one day for the account currency to be changed on the interface. You have to wait one day, and the issue should disappear. In the meantime, you may see some numbers in other currencies (likely GBP).

Another thing you can choose to do is to allow IB to lend your shares. By doing so, you will get 50% of the profits. This feature is called the Stock Yield Enhancement Program. However, there are some risks. I have tried it on and off over the last few years, but whether you think it is worth it is up to you.

Conclusion

The broker you need to buy stocks and ETFs reliably and at extremely affordable prices. Trade U.S. stocks for as little as 0.5 USD!

- Extremely affordable

- Wide range of investing instruments

The procedure is now complete! If you followed this guide, you now have an Interactive Brokers account.

With this great broker, we have access to U.S. Exchange Traded Funds such as VT, which makes the most significant part of my portfolio.

I have now been using IB for more than two years. And I am delighted with IB. Interactive Brokers is the best broker available to Swiss investors.

The next step is now to buy an ETF from Interactive Brokers. It is also relatively simple and only takes a little time.

What do you think about Interactive Brokers? Do you already have an account? If not, which broker are you using?

More reading

Zak Invest Review 2026 – Pros & Cons

Zak Invest is a new service by Bank Cler. Is this broker worth it? I analyze its features and fees and compare it with alternatives like Saxo and Neon.

What is the best Swiss broker in 2026?

Top Swiss Brokers. We compare the best brokers in Switzerland for 2026. Find the safest and cheapest option to trade stocks and ETFs locally.

Cornèrtrader Review 2026 – Cheap Swiss broker

Honest review of Cornèrtrader, a very affordable Swiss broker: how good is it really? Is it really affordable? We will find out!

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Mr. Poor Swiss,

Thanks for these articles about brokers.

I start to follow you and I made the same decision opening an DEGIRO account first… But what intrigues me is why you decide opening an account in IB.

I know about the “DEGIRO cut access to U.S. funds from Swiss investors! Since my portfolio is made of about 80% of U.S. Exchange Traded Funds (ETFs)”.

DEGIRO also have ETFs like S&P500 from Vanguard an so on in different exchanges you can see in this link(https://www.degiro.ch/data/pdf/ch-en/Free_ETFs.pdf) and without any fees.

My question is, you cannot have the same investments using these ETFs?

BTW I invest into:

IE00B3XXRP09 VANGUARD S&P500

IE00B3RBWM25 VANGUARD FTSE AW

IE00BYYR0C64 VANGUARD GLBLMINVO

IE00B4L5Y983 ISHARES MSCI WOR A

What do you think?

thanks once again

Hi Ricardo,

The problem is not ETF with U.S. securities, as you found out, there are plenty in Europe. The problem is with U.S. ETF (literally, an ETF from the United States). These have better tax advantages than ETF from Europe.

I would recommend you read my post about the lack of U.S. ETF, it should help with more detail.

Thanks for stopping by!

imaginary scenario :

1.investor ABC has 300.000 CHF invested in Novartis , Roche , Nestle

2.investor Rick invest in Nasdaq futures and need cash for collateral just in case of a posible margin call .

3. a correction is coming in the next 6 months .

4. investor ABC decide to move in cash until the “storm” will go away so he will have 300.000 CHF in cash and he will pay/lose 1,238 % for 200.000 CHF for the next 6 months .

5.investor Rick decide not to sell but stick to his investments through the “storm”.Because he will maybe need extra cash just in case of a posible margin call , investor Rick will like to borrow some cash if is necessary . And he is willing to pay , lets say 3 % .

6. the benefit for investor ABC = he will not have to pay 1,238 % for those 200.000 CHF

7.the benefit for IB = IB will get 3 % from investor Rick

8.the benefit for Rick = will get through the “storm”

everybody wins

The idea is coming from this: IB has a “Stock Yield Enhancement Program ”

https://www.interactivebrokers.com/en/index.php?f=14527

Lets say investor ABC has shares in Novartis . He can lend those shares to IB and IB will further lend those share to an investor who will sell short those shares .

Investor ABC will still own those shares , he will still get the Novartis dividend and in top of that investor ABC will receive an extra yield from the Short seller .

Example :

1.investor XXX want to short 1000 shares Novartis

2.he will borrow those 1000 shares from IB and IB will borrow those shares from investor ABC with his approval of course .

3.investor XXX ( the short seller ) will pay 4 % interest for the value of those borrowed shares

4. IB will split the 4 % and IB will retain 2 % and investor ABC will get the other 2%

5.During that period , investor ABC will still own the shares and he will still get the dividend ,plus an extra yield .

Can be done the same with cash too ?

Of course does not make sense if the investor ABC has US $ because IB pays interest for cash in US $ ( or change his CHF in US $ ) but in future it is possible that IB will not pay interest for US $ either .

How much a Swiss bank will pay in interest ?

Hi rick,

I guess this makes sense indeed. It’s still market timing and it could end badly.

Stock Yield Enhancement Program is really to yield shares, not cash. I did a little research, but I didn’t find anyway to lend cash in IB. The best thing you could do is transfer it to USD to get some interests and avoid negative interests. However, there is a currency risk of course.

A Swiss bank will basically not pay any interest. The best right now are around 0.03% and they often do not pay interests after 100’000 CHF.

You should probably ask IB about that.

Thanks for commenting :)

Hi Mr. The Poor Swiss,

Is not more easy to send money by Revolut to the IB, in USD money currency?

I mean, using Revolut to change currency and trade in BI in USD currency.

Thanks.

Hi,

That’s a good point. You can indeed send CHF to Revolut, exchange it to USD and then transfer it to IB.

I don’t think it is simpler since it adds a new step and also adds at least one more day delay. But it will save you about 2 CHF on each exchange indeed.

Moreover, this can be rather large transfers. I feel a bit more comfortable with the large transfer going from my bank to IB directly.

But this is a very good alternative indeed.

Thanks for stopping by :)

I just started my journey with IB and I think if you can wait (which usually you can, if you buy monthly/quarterly for the long term) and the conversion is below 10k/month (revolut limit) then imo it’s better to go with revolut.

Over the long term if each month you will save 2 USD, it will compound

Hi Trebor,

Do you mean to say that it’s better to do the transfer each month with Revolut instead of sending CHF to IB and then using to do the transfer?

It’s possible indeed if you never transfer more than 10K in one month. I would not do it for 2 CHF per month though. I do not to transfer such amounts with Revolut.

But yes, even 2 CHF per month will compound nicely if invest in the stock market.

Thanks for stopping by!

Hi,

I find that funding IB with Revolut can be a very good idea in some situations. For instance if you want to invest on a monthly basis.

Did anyone managed to do it? I tried, but I’m stucked because of the following: If you open a notification for a wire deposit in USD on IB, IB provides you with a virtual bank account number that contains your username (it is therefore alphanumerical, but does not have an IBAN format). This does not fit the format expected when you do a transfer on Revolut (IBAN expected for transfer to UK).

I would be super glad if someone can help. Thanks!

Hi Donovan,

Yes, it can be practical to use Revolut.

I am at work right now with no access to IB. But I do not think it would be an issue. You need to enter directly the IBAN into Revolut and then you can use your account number/name as the reference number.

I am always using IB CH IBAN to send money to, I do not use a virtual bank account.

You should check on IB if you have several options for deposit. I can check again tonight if you want.

I hope that helps!

Hi Mr. The Poor Swiss,

Thanks a lot for your answer! I had a look at my account again. If I want to transfer CHF to IB, it happens exactly how you described, and I can provide a CH IBAN with the correct format to Revolut.

But if I select USD as currency and select Bank Wire Deposit as the transfer method, IB does not provide me an IBAN that I could use for Revolut. I only get the virtual account number, an ABA Routing Number (no idea what that is…), and the SWIFT/BIC Code. Since the whole point of using Revolut is to transfer USD, I’m still stucked.

If you have an idea I would be pleased. I will keep looking for the solution anyway. ;)

(I don’t know why, I couldn’t publish below your comment…)

Hi Donovan,

Oh, that sucks!

ABA Routing Number is for U.S. banks. But if you do not get a regular IBAN, I do not see how you can transfer money from Revolut.

You could still transfer CHF and then convert the CHF on IB. IB is really good at foreign currency exchange. But it’s starting to be a lot of steps.

(Don’t worry about the order of comments :) )

Thanks for stopping by!

Hi The Poor Swiss

Thanks a lot for your informative blog!

Concerning the issue of transferring and exchanging money: The forex commission of IB is at least 2 USD per transaction, which seems pretty steep (compared with the commission for buying shares/ETFs). Especially if you want to invest small amounts each month (eg. 500 CHF).

Alternatively, one could try to exchange elsewhere and then transfer USD to IB. But in my experience, transfers in USD usually use SWIFT, an archaic payment system with uncontrollable fees from intermediary banks… a transfer of USD from Revolut to a Swiss bank account recently costed me 20 USD (even with IBAN).

Have you (or anyone) managed to transfer USD to IB from an European bank or from Revolut for free? Is this possible?

Transfers from US banks to IB seems to be free, as they can avoid the “international wire transfer” of SWIFT.

Thank you.

Hi Sam,

This is a good point. I should mention that the conversion fee on IB is bad for small amounts. 2 USD for 1000 USD transfer is 0.2%, so it’s still worse than DEGIRO 0.1%. But for large sums, it is really good to have such a small fee.

In theory, you could use Revolut to do the transfer. It’s easy to transfer CHF to Revolut for free. The problem is transferring USD from Revolut to IB. I know people who tried this and fail to find a way to do it for free. You could transfer USD to their European bank accounts, but it would be too expensive.

I do not know any other way to do it for free. Maybe you could do it with TransferWise for 0.3% too. But I do not know if that’s possible or not.

Yes, transfers from US banks to IB is fine because they have an American bank account.

Now, IB is indeed not the best for small sums. Personally, I have never converted less than a few thousand CHF into USD. So the fee is really good.

One solution could be to wait a while to accumulate the CHF before you convert it. But that’s not optimal indeed.

Thanks for stopping by!

What is the minimum amount needed to put into the account? Im new to this..if i was to buy shares and leave the account dormant for a while, do they charge for inactivity?

Hi Sair,

There used to be a minimum of 10’000 USD, but that is not the case anymore. You can now open a Cash account with 0$.

However, they have inactivity fees of 10 USD per month if you have less than 100’000 USD in assets.

Let me know if that helps :)

Hi,

is it still the same minimum? I heard IB changed it in Mars… thanks

Hi Jean-Pierre,

It is still 100K USD for waiving inactivity fees. They may have changed other things, but this minimum is still here.

Thanks for stopping by!

Hi Mr. The Poor Swiss.

Thank you for the article (contains a lot of useful information) and apologize for the large number of questions I’m asking:

1. “Another thing you need to configure when you create an IB account is the base currency of your account. I am going to make most of my payments in Swiss Francs (CHF), therefore I went with CHF as my base currency. You can always convert money from your base currency to any other currency.”

Does it mean that when you transfer your money from your Swiss bank to IB account through IBAN to CH2089095000010569674, there is no fee for that at all? In other words, if let’s say you send 1000 CHF, you will get exactly 1000 CHF in your IB account, right?

The second question: since US ETFs are sold in USD, how do you buy them? You mentioned: “You can always convert money from your base currency to any other currency”. Is the currency exhcnage rate between CHF and USD good enough? Do you have to pay any commission for this conversion? What is IDEALPRO and FXCONV?

2. “You need to set how much your net worth is and how much income you have.”

Does IB check it some how? Do they require any supporting documents? May I simply answer “it’s none of your business, guys”?

3. “You also need to select from which country (stock market exchange), you want to invest in.”

If I want to buy US ETFs like VT, SPY or IVV then should I select NYSE? If next year (2020) I lose access to US-domiciled ETFs and will decide to continue with European domiciled ETFs, should I select SWX? May I add another stock exchange later?

4. “On the same page, you will also have to enter information about your tax status”

What does it mean?

5. “Once we are done replenishing our cash fund, I will move more funds to my new IB account. At this point, I will make sure to write an article on how to buy an ETF on Interactive Brokers.”

Since I am about to create an account in IB and make my first purchase of ETFs, I look forward to reading this article.

Hi,

You’re welcome :)

I am glad to answer your questions!

1. Yes, that is totally correct. I never paid any fee to transfer CHF to my IB account :)

2. You have to convert the currency. In Interactive Brokers, you can make a trade for almost any currency. The exchange rates are extremely good at IB. Some people use IB only to make currency conversion. You have to pay a small fee indeed. I have paid about 3 dollars last time I converted 10’000 CHF into USD. IDEALPRO and FXCONV are different exchanges for making currency conversions. In practice, for simple users like us, there is no difference.

3. I do not think they check how much you got, no. They do not require any supporting document. I do not think you can answer that, no.

4. You can add other exchanges later on yes. I have selected U.S. and all of Europe as my countries to invest in.

5. It’s simply in which country you pay tax and your tax number (social security number, AVS)

6. The article is coming and in the pipeline. It should be published by the end of the month!

I hope that helps!

Hi Mr. The Poor Swiss.

Thank you for the information.

Let me ask you some more questions.

I’ve just opened my IB account and I am about to fund it (bank wire). So, first of all I see the following message: “CHF carries a negative interest rate as imposed by the relevant central bank. This means that you will actually pay interest to keep this currency with the broker rather than earning interest (this is because the broker, in turn, must pay interest to the banks in which it keeps client funds denominated in this currency).” Does it mean that I have extra fees just because I selected CHF for my base currency? What do you think abot this?

Second question: I am requested to fill the following fields: Sending Institution (Required), Account Number (Optional), Nickname (Required). What is this? Where can I find this information? I want to send money from my PostFinance account. Does acount number equal to the last 9 digits of my IBAN?

Thank you.

Hi Aleksei,

You are welcome.

a) It is not extra fees, no. However, your balance in CHF at Interactive Brokers will have a negative interest. If the current interest is -0.5%, you will lose 0.5% of your CHF cash every year. Since you should generally not carry a large balance in cash in your broker account, this should not make a big difference in the long-term.

b) The Institution should be PostFinance. You can let the Account Number empty, this is what I did with my Migros account. And the Nickname, you can put what you want, this is the just the name inside IB.

I hope that helps

Thanks for stopping by!

Hi Mr. The Poor Swiss

If an investor will have in his account 150.000 CHF in cash , he will pay 1,238 % for the balance above 100.000 = 50.000 CHF in this example .(negative interest !)

Is it possible for the investor to lend that amount (50.000 CHF) through IB and the borrower ( another investor ) to pay that negative interest ? instead of the owner ?

Hi Rick,

I do not know if you can lend cash on IB. I would think you cannot.

However, why would you have so much cash on IB? I am not sure it is a great place to store cash, especially in CHF. You could store it in USD in order to make some profit.

If I had so much cash, I would store it in my bank account.

Thanks for stopping by :)

Hello Mr. The Poor Swiss

Your articles on Interactive Brokers are extremely valuable. I’d like to open a bank account here with my base currency being CHF, however I am concerned about the exchange rates which You find extremely good, as You mentioned. At the moment how much is 1 CHF in USD? I am just curious about how it is relative to the interbank exchange rate.

Many thanks for Your answer in advance.

Hi Richard,

Thanks for your kind words on my article :)

The rate should be the interbank exchange rate in real-time. IBKR has no markup, margin, or spread, or thing of that sort on top of the rate.

I am afraid it is Saturday, so the exchange will be closed until Monday.

If you ask again on Monday, I’ll give you the last rate ;)

After the exchange, regardless of the rate, you will pay a fee of 0.002% of the trade value, with a minimum of 2 USD. So, unless you convert more than 100K USD, you will pay 2 USD.

Thanks for stopping by!

I am sorry, but I am a bit puzzled by your explanation: “They have weird conditions for the user name, it needs to be between 8 and 9 characters in length. And it needs to contain at least three numbers. I think it is a bit dumb, but it is only a password”. Are you talking about name or password here?

Hi Aleksei,

You’re right to be puzzled. There is a mistake in this paragraph. I edited the post to fix it.

I was speaking of the user name, not the password.

Thanks for letting me know!

Hi the Poor Swiss,

Did you make up your mind yet as to how to transfer your capital from Degiro to IB?

I am exactly in the same situation as you…

Cheers from Genf!

Jean-Pierre

Hi Jean-Pierre,

Yes, I did. I started selling my funds and buying them back. However, I do not think it is a good idea anymore. There is really too much risk of market price change between the time you sell and the time you have the money again to buy them back.

Unless you have a very small portfolio, I would not advise to sell and buy back.

Good luck with your transfer!

Great Post,

just a question what will happen after 2020. Will we need to sell all our US based ETF? Or can we keep them until we want to sell them?

Hi JUinZH,

We won’t need to sell US-based ETFs. We can keep them until we want to sell them. We just may not be able to buy more of them.

Thanks for stopping by :)

I did not find the way of using FXCONV on the TWS “android” app but only on the PC desktop version. If anyone can share an idea on that it would be highly appreciated. Cashflow is right, use the FXCONV for currency converting. The IDEALPRO also works but it ends up in a currency position instead of cash balance. It does not harm but gives a headache by reading out balances.

Thanks for sharing this!

I really need to get more information about the differences between FXCONV and IDEALPRO.

Hey mate,

You should find what you look for in this post I wrote last year: https://www.mustachianpost.com/2017/02/21/how-to-buy-the-vt-etf-in-usd-on-interactive-brokers/ (I had the same questioning ^^)

Hi Marc,

Thanks for the link. It is very helpful indeed!

My only problem is that I do not use the TWS app most of the time. I prefer to use the WebTrader or even simpler the Account Management interface. And from these two interfaces, only IDEALPRO is available.

Thanks for stopping by :)

Indeed IB hasn’t the most “human” user-interface out there…

Yes, I’ve rarely seen interfaces with so little ergonomy.

Nice. Glad you made the switch! Welcome on IB! A real broker! ;-)

When I opened my account, it took me something like almost 1 hour, between all the questions and the documents needed. It was a real pain in the ass as we say. I’ve never done a registration like that before haha.

I hope you will consider using their TWS (Trader Workstation) app for investing. It’s a scary Java app, at first sight, but much more feature complete than the rest, there is more informations and honestly, not hard to use and much better looking than their WebTrader. In fact, I find the last one quite scarier…

The only thing I suggest, is double checking how to convert currency correctly, you need to use FXCONV instead of IDEALPRO when converting USD to CHF on the forex. Not sure if you can do it with the WebTrader. Else you can end with virtual negative balances… Maybe you can do some tests with your paper trading account.

Also I couldn’t say it better so I’m quoting someone from internet : “And really you want to learn how to use TWS anyway – it’s a hell of a lot better.”

Good luck.

@Cashfl0w: can you please explain the fx conversion. YOu kinda’ scared me sicne I always used IDEALPRO.

Hi Cashflow,

As you said, it’s a bit a pain in the ass. I’ve never seen any registration so complete. But it’s pretty straightforward overall.

I will definitely test TWS. So far, the only things I have seen from it is pretty overwhelming. But I am going to give it a try.

Thanks for the tip about conversion. I will take a closer look at this the next time I do a currency conversion!

Thanks a lot of sharing