Dollar Cost Averaging is more risky than you think

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

When you have a large sum of money to invest, you have two choices. Either you invest it at once or cut it in smaller sums and you invest it over a longer period. The latter option is called Dollar Cost Averaging (DCA).

Most people will tell you you should always use Dollar Cost Averaging for your investments. But, in practice, investing in a lump sum is better than using DCA.

In this article, we will see what DCA is and its advantages and downsides. By the end of the article, you will know how to invest a lump sum.

We will also talk about Continuous Investing. Continuous Investing is when you invest your monthly savings as soon as it is available. Some people call this DCA, but it is not accurate. These are two different things. One is excellent, but the other is not.

Dollar Cost Averaging (DCA)

Dollar Cost Averaging (DCA) invests much money over an extended period. DCA will effectively average the price of what you buy over a longer period. Hence the name of dollar cost averaging your purchase.

We can take an example where you got 60’000 USD to invest. You want to invest it in the Vanguard Total World ETF (VT).

You could invest it at once today in the stock market. But you are afraid that the market will suddenly drop. And indeed, the market can quickly lose a few percent in one day. And can drop up to 50% in a few months (or even weeks). Such a significant drop does not happen often, but it can happen. And you are afraid that just after you invested your big sum, the market will drop a lot.

So, instead of investing it at once, you decide to Dollar Cost Average your VT purchase. You cut your lump sum into 12 parts of 5000 USD. And you choose to invest one part every month for one year.

So if the price of VT goes down significantly shortly after you made your first investment, you will have saved a lot of money since the average price of your investments will be lower than it would have been.

So, the main advantage of DCA is to protect you against a drop shortly after your investment.

DCA introduces another risk

You have eliminated one significant risk. However, you have just introduced a new significant risk. If the market is going up during the time you are dollar cost averaging, the average price will significantly increase. You have traded one risk for another.

It remains to see which risk is more significant.

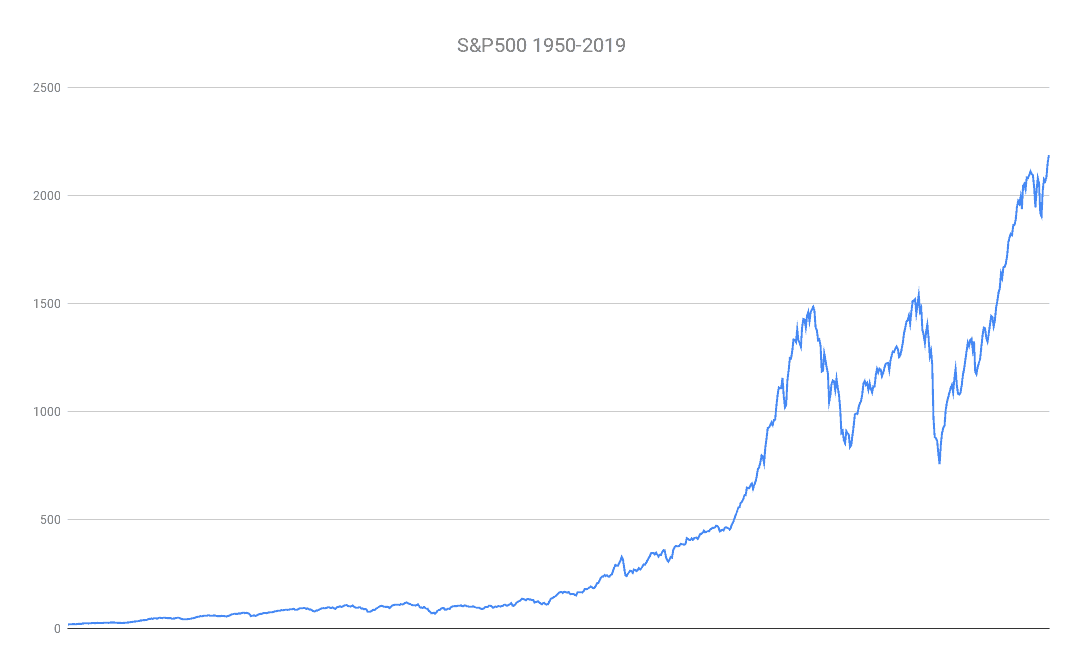

In practice, the second risk is greater. The stock market, on average, is going up. You can easily see that on the graph of the S&P 500 over more than half a decade. So, every year, the stock market has more chances to go up than down. From a probability standpoint, the risk introduced by DCA has more effect than the risk it fixes.

For instance, in the past 100 years, the Dow Jones Industrial Average (DJIA) was up 70% of the last 100 years. So, the DJIA is twice more likely to go up than to go down. Thus, you are increasing the risks in your portfolio by using DCA.

Indeed, it is better to protect against a risk of 70% rather than a risk of 30%.

Downsides of DCA

Here is a summary of the multiple downsides of DCA.

First, when you dollar-cost average your purchase, you are betting against the market. However, there is a higher probability that the market will go up rather than down. By dollar cost averaging, you are increasing your risks.

All the cash waiting to be invested is incurring some opportunity costs. First, it will not generate any dividends. On average, a good stock market index will have a dividend yield of about 2%. You are missing the dividends. And you are also increasing the risk of inflation.

One small disadvantage of DCA is that you will likely increase the transaction fees for your investment. Generally, most brokers have a small flat fee and a percentage fee. If you invest twelve times instead of once, you will pay 12 times the transaction fees. These fees should not be a lot of money, but this is still some wasted money.

DCA will only protect you from the risk of the stock going down during the period of DCA. Nothing prevents the market from plunging the day after you have finished your DCA investment. So, it is short-term protection.

DCA is a short-term strategy! If you want to invest for the long term, it is not a good strategy. Generally, it will not work.

And talking about the investing period, you still have to choose the period during which you want to dollar cost average your investment. A typical time frame is one year. But you could choose to invest for two years or only six months. Choosing the optimal period for DCA is impossible. Trying to do so is market timing.

The entire idea of DCA is very close to market timing. If you doubt whether the market will increase, you are already timing the market. And we have discussed market timing previously. Timing the market is a loser’s game. There is no way to predict the market. We can only base our decisions on the facts that we already have. These facts are more than one hundred years of stock market data. And these have shown that generally, the stock market is going up. Therefore, you should bet on the market going up, not down.

Finally, by holding a lot of cash, you are also messing with your asset allocation. When you started investing, you decided on an asset allocation that suited you. For instance, you may have decided to invest 80% in stocks and 20% in bonds. But now, you have a large amount of cash. Maybe you have 40% in stocks, 10% in bonds, and 50% in cash now. And your asset allocation will only be balanced once you are done investing it.

Value Averaging

Value Averaging is an alternative to dollar-cost averaging. Instead of investing the same monthly amount, you will invest based on your shares’ current value.

We can take the same example as before. You want to invest 60’000 USD in 12 months. In the first month, you will invest 5000 USD as with DCA. However, in the second month, you will invest an amount so that the value of your shares reaches 10’000 USD. For example, if the shares went down in value to 4500, you will buy 5500 USD to bring it back to 10’000. If the shares increase the next month and reach 11’000 USD, you must invest 4000 USD.

So instead of having a fixed investment each month, you have a fixed goal.

Some people like Value Averaging because it avoids investing too much when the market is going up and more when it is going down.

However, it has some important downsides. If the market drops significantly during the year, you must invest more than planned. If you invested during the financial crisis of 2008, you would have had to invest more than 80’000 USD in bringing back the value to 60’000 USD. So where will you find the extra 20’000 USD?

And on the contrary, if the market is going very well, you may have to invest less than you wanted. Then, what will you do with the extra money?

Value Averaging is strictly worse than DCA. It has fewer advantages and more disadvantages. It is too complicated and incurs too many risks.

How to invest a Lump Sum?

Now that we have seen that DCA is mostly a bad idea, it is straightforward to know how to invest a lump sum.

You should invest a lump as soon as possible and at once. You need to know your target allocation and use the lump sum to ensure your portfolio is balanced. If you need bonds, buy bonds. If you need stocks, buy stocks. And if you need both, buy both! It is an excellent time to balance your portfolio correctly.

Continuous Investing is not DCA

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

Now, you may be thinking: what am I supposed to do with my savings every month?

You need to invest it as soon as you get it! Investing your monthly savings could be considered some form of Dollar Cost Averaging. However, it is unavoidable. And there are a lot of posts talking about that and saying this is Dollar Cost Averaging. Both concepts should be separated. We can call this Continuous Investing.

If you do not invest it directly but wait, for instance, until you have one year or even one-quarter of savings, you will increase your risks significantly and have zero advantages.

You cannot reduce the risks of your monthly investing. Once a month, you should invest your savings. You should do that regardless of the price. Over a very long period, this will save you money to invest frequently since you will buy when the price is high and you will also buy when the price is low, giving you a better average than if you invest only once a year.

This form of DCA is unavoidable and is the recommended way of investing! It is great to invest your savings each month. You need to invest continuously.

I have actually simulated how often you should be investing. It turns out that monthly investing is the best frequency. You should not try to delay your investments.

Why are people recommending DCA?

All over the internet, almost everybody is recommending Dollar-Cost-Averaging over Lump Sum Investing.

The main reason is that DCA makes people feel better. If you invest over several months and the market is going down, you will feel better that you did not invest too much the first time. Moreover, you will also feel better about buying shares at a discount.

It all comes down to the fact that people are much more afraid of a loss than they are happy with a return. Most people will feel a bigger impact with a loss of 10% than a profit of 10%. This fact has been shown many times already.

People prefer avoiding a small loss than staying for the long term and taking a more significant return. Therefore, people recommend DCA not feel bad about investments.

But I think this is wrong. Most people are investing for the long term. And therefore, it is better to maximize long-term gains. Even if you feel bad for one year or two years, you should be able to weather it. And people advocating for DCA should also point out the disadvantages!

FAQ

What is Dollar-Cost Averaging (DCA)?

Dollar-Cost Averaging (DCA) is an investing technique where you invest a sum of money over a longer period. The larger sum is split into smaller portions and invested as such.

What is Value Averaging?

Value Averaging is an alternative to Dollar-Cost Averaging (DCA). Instead of investing the same amount every time, you invest based on the current value of your shares.

What are the downsides of Dollar-Cost Averaging (DCA)?

When you dollar-cost average an investment, you are betting against the market. But on average, the market is going up. This means you are likely making the wrong bet.

What are the advantages of Dollar-Cost Averaging (DCA)?

Dollar-Cost Averaging (DCA) protects you against a drop in the market happening shortly after you start investing.

Conclusion

I do not advise Dollar Cost Averaging for any of your investments. You should stick to your asset allocation and invest money when you have it. It is part of my Investor Policy Statement not to use DCA.

If you invest for the long term and have a large sum of money, the best course of action is to invest it now. Dollar Cost Averaging the investment will increase your risk of losing out on returns. And do not forget to invest according to your asset allocation.

Now, if you want to invest using DCA, do it if it makes you feel more comfortable. It is an excellent technique to cut some emotions out of investing. But do not let your emotions choose your investing strategy.

But you should still invest your savings monthly. Continuous Investing is not the same as Dollar Cost Averaging. There are too many articles on the internet that mix the two concepts. Continuous Investing is great, DCA is not great!

While it is not a very popular opinion, I am not the only one who thinks like this. For instance, JL Collins talked about why he does not like DCA.

What about you? What do you think of DCA? Do you use it?

More reading

How to Change Broker and Transfer Your Portfolio

Find out how to change broker and how to transfer your investment portfolio from the old broker to the new broker account.

What Makes Vanguard Unique?

Vanguard is an awesome mutual fund company. Find out several reasons that makes Vanguard unique as a mutual fund provider.

Mutual Funds and Index Investing

Now that we talked about stocks and bonds, it is time to talk about Mutual Funds. Find out about active funds and passive funds.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hello the Poor Swiss,

Love reading your articles and blogs that share your personal insights. I am only starting to learn about investing (at the age of 40) and have a lump sum of cash for investment (200k). The stock market is in a crazy all-time high. Would you still consider investing the lump sum under the current condition?

Thanks

JC

Hi JC,

If it were me, yes I would still invest a lump sum.

In your case, it depends on two things:

* How long do you have in front of you?

* What would you do if the market drops 50% one year after you started investing?

Based on these questions, you can decide whether you want to invest as a lump or as DCA.

Thanks for stopping by!

Hi there

How about now, in these times? Would you DCA or Lumpsum invest?

Hi IronM,

Even in these times, I would still invest a lump sum unless it was really huge (>100’000). After this, I would probably DCA it a little even though mathematically it should not matter.

Thanks for stopping by

Hello!

thanks for the article. I have been reading a lot on your blog in the last months and I am well aware you against DCA and you stick to your IPS :)

what would you suggest for a beginner investor like me starting now investing (IB with ETF basically)?

A lot of articles are talking about recessions, I do not want to bet on the market going down but maybe a DCA strategy could be reasonable during these following years.

(FYI, I have long term goal and being 29 yrs old I would invest 89-90% stock vs 10% bond)

have a good day

Hi Pol,

I would say that it depends on how long you plan to invest and if you have a large amount of money to invest or you plan to invest every month.

If you invest for some time in 10 years or more, I would simply invest now. You should not bother with prices. And then continue investing every month.

Now, if you have a large amount of money ready to invest or you do not have much time before you need your money, it *may* be different. You could wait for the market to drop. But you may have to wait years and it may never drop lower than now (it will drop but if it drops in 5 years, it may not come back to current levels). So it’s up to you.

I hope this helps a bit

Thanks for stopping by!

Great article. Made me think. I am doing DCA on a sun on a fund account at the moment. I have no fees related to this so I do it just to reduce risk. I am not sure I agree that what you introduce with DCA is a risk. But I see what you mean.

I am a very statistic-oriented person, not just for investing but in general, but statistics need to be analyzed and interpreted properly to be useful, otherwise they may lead to wrong conclusions or not be precise enough.

In this case, I can see the point of them being totally against DCA, and I’m all about not trying to time the market as a long term investor, but I can’t help but wonder what a statistical analysis would say about DCA vs lump sum specifically on all previous contexts of 10+ years of continuous market growth and all time highs, as opposed to just DCA vs lump on average..

In other words, what I mean is that, while I know that timing the market is a losers game, intuitively, I feel like that the longer we have been from a recession, and the closer we are to the next one, the better it has to work DCA over lump sum, as the chances of the market not growing more than it declines are supposed to be higher..

That said, I can easily be completely wrong and this might be my brain resisting to accept the best course of action.

Hi Carlos,

I can see where this make sense. I would also think that if we were to analyze the differences in returns between DCA and lump sum, there would be times where DCA is better. And indeed, it’s just before the end of a bull market and during a bear market. As long as the market is going down, DCA should win.

I may try to do this analysis in the future, it could be interesting.

However, even with that, it does not really help us since we never know how far (or close) we are from a bear market.

That’s a very interesting post!

Thanks for stopping by

I believe the DCA is a misunderstood thing.

From my understanding DCA has a clear purpose. Lowering the risk. Which is not equal to increasing the return. You do not use this technique for rising your return but you use it in order to lower your risk. Naturally you want both at once but this toy does not support that.

In case you have a lump sum to invest, you have to decide what way you go with it and it depends on you risk profile.

If you are ok to take more risk then you will shorten the time you invest the whole money and it will result in P/L according to the market goes.

If you risk profile is less brave then you go slow and your P/L will be again, according to the market goes but your money will be at risk in a completely different structure.

What is kind of decisive is that after a certain time you will not optimize the risk picture anymore by prolonging the investment, but you will lose more than you can be protected against risk. That is pure playing with probability so mathematics at the end of the day.

In practice it is not really worth to make it longer than 1 to 2 years in case you have a larger lump sum.

Or vice versa, in case your money is too few, then the DCA does not support too much even if you brake it in to even smaller. So it only works if you have a larger amount of money to put in risk. Don’t DCA a fraction of your weekly wage.

I kind of agree with the statement that DCA is not as good as you think but you have to put it in to context. Challenging the DCA in the subject of return optimization is not really fair I would say.

You can’t just say that the not received return after not invested money is also a risk of not earning enough :)

Hi baseldon,

It is true that the main purpose of DCA is to lower the risk. To be precise, it is to lower the risk of the stock market crashing just after you invest. And it does that since it will average down (in that case), the price of your shares. And in down-market, it will even increase your returns compared to lump sump.

And it’s also true that I am mostly compared a risk against returns. But for me, lowering the returns is a risk. It put your plan at risk.

But you are entirely right in that I am mostly focused on the long-term and DCA is obviously not long-term.

Thanks a lot for sharing your point of view!

I agree that DCA is bad, when money is just sitting in your savings account.

Again, I agree completely, that invest immediately when you get paid.

But, what I think people seem to seldom consider are the alternatives to stock market (and savings account).

I agree timing the market will not work, but, I’m hoping being heavily invested in p2p now (which can yield similar average returns) and waiting for cheaper times to shift back to stocks will result in higher overall returns than being all-in in stocks today.

It’s risky of course. Very much so. I’m pretty sure I don’t _know_ for absolute certainty what I’m doing, but who does? ;)

But yeah, DCA is not very great. But I wish people considered other high return assets to stocks, too.

Hi Eelis,

That’s a good point. The stock market is not everything. I have talked about P2P Lending already. And there is also real estate.

When people are getting scared of the stock market, they could indeed pivot some of their investments into alternative investments. This would diversify as well.

Of course, it’s all market timing :) Even though the stock market is at an all-time high, it could well go higher for 10 more years. It’s unlikely, but who I am to know!

But I agree that some people should also consider other assets. I also wish that some heavy P2P lending adopters would also recognize the risks.

Thanks for stopping by!

Oh man. What a post! I wrote something similar when I was analyzing the pros and cons.

DCA is 100% timing the market. Which is usually not a good idea.

I understand if you have a short term need for the money to DCA, but if you are investing for the long haul, the lump sum approach is statistically the best way to go.

Hi Kevin,

Nice to see more people that like statistical approaches! As you said, it’s just statistically better to use a lump sum in the long-term.

For the short-term, the stock market is not that great anyway.

Thanks for stopping by!

Investing is a matter of putting your money at risk in order to reap some return. Often your money is risked at a specific AA say 60/40. If you have 1M invested and 200K in cash to invest your AA IS not 60/40 but more like 50/33/17. This is why DCA is not smart for lump sum. You lose a whole year to being under risked and therefore a whole year to the extra return. Market timing is noise. Over 40 years timing will be infinitesimal change on return compared to what you lose by waiting for an entry.

The opposite is true of weekly investing. Clearly you can’t invest what you don’t yet have but need to risk it ASAP The people that say DCA a lump sum don’t understand DCA. Good article

Hi Gasem,

That’s a very good point about the asset allocation. Once you have a large sum to invest and you are waiting for DCA, your cash allocation is way out of your AA! Many people do not consider their cash in their asset allocation. But this is an important part because of inflation. If there was no inflation, we would have much less incentive to invest.

It would be cool to receive a salary once a week in order to invest it more often. However, that’s probably not going to happen!

Are you also investing as soon as you can?

Thanks for stopping by!

I certainly wouldn’t invest a lump sum now, with markets at all time highs. I expect better entry prices in the next six months. At most, you could invest maybe 25% now, then wait and see for the rest.

Hi Carl,

I understand why you would think like that. But people were already saying that in 2015 and in 2017 and in 2018. The problem is that you never know how long to wait.

Of course, that depends if you invest for the really-long-term or for the short term.

But for the long-term, I would still invest a lump sum now.

Thanks for stopping by!