Inyova Review 2026 – Pros and Cons

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Inyova is a Swiss robo-advisor that focuses on impact investing. You may know it under the name Yova which was its previous name until June 2021.

The main idea is to invest in improving the world. This way, you will not only get good returns on your investment but also use your money to improve the world.

But how does Inyova compare with other robo-advisors, and how much does it cost? This complete Inyova review will reveal the answers.

By the end of this Inyova review, you will understand all the advantages and disadvantages of investing with Inyova and whether this service fits your personal investing needs.

Disclaimer: I am not investing with robo-advisors. DIY investing is better for people willing to invest time and effort, and it will save you money. But DIY investing takes time and knowledge. For people unwilling to invest their time and effort, investing with robo-advisors is the next best thing.

| Management fee | 1.20% – 0.90% (degressive) |

|---|---|

| Product Costs | 0% |

| Withholding Costs | 0% |

| Total Costs | 1.20% – 0.90% |

| Investing strategy | Active |

| Investing products | Stocks |

| Minimum investment | 2000 CHF |

| Currency conversion | Included in management fees |

| Customization | None |

| Sustainable | Very sustainable |

| Languages | French, German, and English |

| Custody bank | Saxo Bank |

| Users | Unknown |

| Established | 2017 |

| Headquarters | Zürich, Switzerland |

Inyova

Inyova is a robo-advisor that focuses uniquely on impact investing. They target people who want to make the world a better place with their money. Of course, since it is an investment platform, they try to invest in profitable companies.

Inyova was launched in 2017 under the name Yova. Even though they are a young platform, they have been growing quickly and are already managing several million CHF. In June 2021, Yova changed its name to Inyova. This new name means “Invest in your values”.

It is important to note that you need at least 2000 CHF to invest with them. This minimum is because, below that level, good diversification would not be possible.

They started with a web application but have also added a mobile one. This is interesting because most robo-advisors in Switzerland lack mobile applications.

So, we now delve into the details of this Inyova review.

Inyova Investing Strategy – Impact Investing

We start this Inyova review by going over their investing strategy.

Inyova has a very different investment strategy from that of other robo-advisors. Indeed, while most robo-advisors invest in Exchange Traded Funds (ETFs), Inyova will directly invest in stocks and bonds.

Another way they differ is that they only invest in sustainable companies, following the impact investing philosophy. Other robo-advisors offer sustainable investing options, but it is not their primary focus. With Inyova, you cannot invest in other companies. So, they are only for investors who want to invest in this fashion.

In the past, the portfolio was highly customizable, but now they have a unique investment fund managed by Inyova. This fund is optimized for sustainability and returns.

In the end, you will have about 1000 stocks in your portfolio. Inyova will diversify these stocks across various sectors and countries. This means a great diversification overall.

Your asset allocation will be based on your risk profile: how long you want to invest the money and how old you are. For instance, a young investor like me could have 100% invested in stocks. On the other hand, an investor close to retirement may have only 60% of stocks (or even less). So the minimum is 20% invested in stocks, and the maximum is 100%, which is great.

Overall, Inyova offers an impact investing strategy that is good if you focus on sustainable investing. They are the best robo-advisor for impact investing and sustainable investing. I like to invest in wider ETFs to avoid stock picking. Nevertheless, I understand the appeal of sustainable investing. You cannot invest in all stocks in the world if you want to invest sustainably.

Inyova Fees

When reviewing an investing service, it is paramount to review the fees. Inyova is different from other services in that there are no fixed fees. The fees you pay depend on how much money you invest with them.

If you have strong financial goals, investing fees are extremely important.

The investing fees at Inyova are all-inclusive annual fees. So, you will pay a portion of your assets as management fees. Here are the fees based on the amount of money invested:

- Below 50,000 CHF: 1.2% annual fee

- Between 50,000 and 150,000 CHF: 1.1% annual fee

- Between 150,000 and 500,000 CHF: 1.0% annual fee

- Above 500,000 CHF: 0.9% annual fee

Overall, these fees are expensive. With a huge amount of money invested, you can get decent fees compared. However, if you do not invest much (like most people), the fees at Inyova are high. For me, a 1.2% annual fee is not acceptable. Of course, you will have to decide for yourself if you are comfortable with this level of fee.

It is good to note that currency conversion fees are included in the fees. This is good to know because most robo-advisors will not include it in the management fees.

The fees you pay depend on how much your account is worth. So this also includes capital gains. This is great since a good performance can also make your account cheaper.

Finally, you will also pay Swiss stamp duty on the operations that Inyova makes for you. This tax should not be huge, but it is still not negligible.

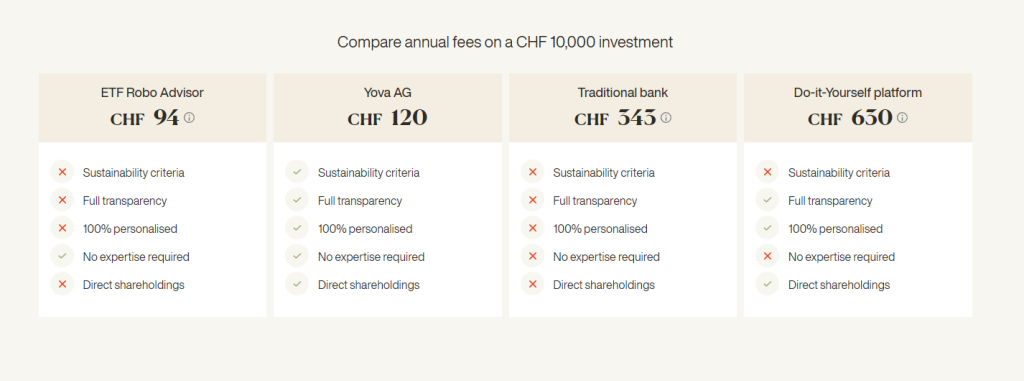

Now, there is something else I dislike about their pricing: their comparison with other pricing. Here is how they compare themselves with other alternatives:

The first thing that irks me is that they compare themselves against a robo-advisor with a 0.94% fee, which is already high for Switzerland. The cheapest I know would have a fee of 0.64%, almost half as expensive as Inyova. This is a common marketing strategy, i.e., to not compare against the best.

On the other hand, it irks me that they compared themselves with an expensive DIY platform (Swissquote). There are two major problems with this comparison.

First, they use a costly platform (Swissquote) instead of a cheaper and better one, like Interactive Brokers. Using a better broker would dramatically reduce this.

The second problem is that they are comparing against ETF robo-advisors but not comparing against ETF DIY investing. If we take my case, I pay about a 0.2% annual fee, all-inclusive. My fees would come down to being four times cheaper than Inyova. Since I have more than 100,000 CHF invested, the fee would be down to 1.0% for me (still three times more expensive than my fees!).

I am not saying that to show off that my strategy is cheaper than Inyova. I am saying that because it does not help customers! People should know that investing by themselves is less expensive than what Inyova tries to show. If you want more details about such a comparison, read my article about the different levels of investing.

Overall, I think that Inyova’s fees are not great. For small invested amounts, the fees are too high compared to a cheaper robo-advisor. If you have a considerable amount of money invested in Inyova, the fees will be better (but still not great). Finally, their comparison with other alternatives could be more transparent.

Is investing in Inyova safe?

An essential part of an investing service is its online security. So we will see if investing with Inyova is safe.

First, since they are not a bank, they cannot hold your assets. All your shares will be held, in your name, by SAXO Bank. Inyova is only considered the asset manager. So, they can execute trades in your name, but they cannot access your funds. The cash is still protected by the general Swiss deposit protection, up to 100,000 CHF. Therefore, the portion of your assets that is not yet invested is also safe.

If Inyova goes bankrupt, all your funds will be accessible in your name at SAXO Bank. It is a good level of safety for your assets. It is the same strategy used by almost all robo-advisors in Switzerland.

From a technical perspective, all communication is encrypted, which is the standard minimum these days. You can also use a second factor of authentication (2FA). This will significantly increase the security of your account. If you care about online security, you should always use 2FA.

So, overall, investing with Inyova will be safe since it uses asset segregation. However, technical security would be much better if they had second-factor authentication support.

Inyova Grow

In addition to the investments, Inyova also proposes projects. This feature is called Inyova Grow. These projects are sustainable projects like:

- Large solar plants

- Wind farms

- Greehouses

These projects give some fixed interest rate. They are mostly paying interest on an annual basis, but some are using a different schedule, and the capital is repaid after a few years. Most of these projects have been in EUR, but Inyova is planning to have CHF projects as well in the future.

These projects are a nice way to allocate money to sustainable projects. However, keep in mind that Inyova will charge a 0.95% fee per year, so keep this fee in mind when computing your returns.

Inyova Third Pillar (Inyova 3a)

From December 2021, Inyova also offers a third pillar account: Inyova 3a

The principle is the same as Inyova. You can invest sustainably according to your values. Inyova 3a is the first fully sustainable third pillar in Switzerland.

You can start investing from 100 CHF since they allow fractional shares. This is great to get started! You will have to choose our values, which are just like the standard Inyova account.

The third pillar costs 0.80% per year. Moreover, depending on your strategy, you will pay between 0% and 0.24% for the product costs. Since the bonds are the most expensive, the most aggressive strategies are cheaper. If you have no bonds, you will not get any extra fee, so only 0.80% total. And this will get simpler later with an all-inclusive fee.

You can get more information on Invoya’s website.

User Reviews

I wanted to see what people were saying online about Inyova. Unfortunately, there are very few online reviews about this service. My favorite source of reviews, TrustPilot, has zero reviews for it. However, there are a few reviews on Google. Based on 28 reviews, they got an average grade of 4.7 stars out of 5.

Of course, there are not enough reviews to draw proper conclusions, but it is still interesting. I also looked at forums to find people’s opinions on Inyova.

Overall, the positive points in the reviews are mostly about the team itself. Indeed, the team seems easily approachable and very helpful. People also greatly appreciate the level of customization that is possible in their portfolios.

On the other hand, the negative reviews were about two things:

- The very high fees of the service.

- Their heavy advertising campaign.

Overall, Inyova users have excellent reviews of the service. People not using Inyova mostly complain about the high fees and that we can invest elsewhere for much cheaper.

Alternatives

When evaluating a service, comparing it with some alternatives is essential. So, we will compare Inyova with two Swiss robo-advisor alternatives.

Inyova vs Finpension Invest

An excellent and innovative Robo-advisor by Finpension.

- Most tax-efficient Robo-advisor

- Access to private markets

A great alternative is Finpension Invest, with an option for sustainable investing. Both options are simple to use.

Finpension Invest uses ETFs, unlike Inyova which uses a fund of stocks selected by them. It will have much lower sustainability.

But the advantage of Finpension Invest will be that it will be much cheaper. In fact, it will be more than twice as cheap. It is also more customizable.

For more details, you can read our review of Finpension Invest.

Inyova vs Selma

Selma is another good robo-advisor in Switzerland. Selma also has an option for sustainable investing.

There are some major differences between these two robo-advisors. Indeed, Selma will invest in Exchange Traded Funds (ETFs) picked up by another provider instead of an active fund picked up by Inyova .

Selma will invest in sustainable versions of its ETFs when you select sustainable investing.

Now, these two versions of sustainable investing are different. Inyova’s sustainable strategy goes much further than Selma‘s. With Selma, you only have the bare minimum of sustainability. If you care about impact investing, Selma will probably not be enough for you.

On the other hand, Selma’s fees are better than Inyova’s. With Selma, you will only pay about 0.98% in fees for your portfolio. Selma is cheaper than Inyova.

From an ease-of-use point of view, both solutions are good.

For more details, I have an in-depth comparison of Inyova vs Selma.

Inyova vs True Wealth

|

Cheapest Swiss Robo-Advisor

|

Very Sustainable

|

|

Primary Rating:

4.5

|

Primary Rating:

4.0

|

|

Pros:

|

Pros:

|

|

Cons:

|

Cons:

|

|

Security:

Good

|

Security:

Good

|

- Very customizable

- Excellent fees

- Passive investing

- Great diversification

- Not highly sustainable

- Great customization

- Very sustainable

- Degressive Fees

- Stock-Picking Strategy

- Lack of diversification

- High fees

Another serious alternative is True Wealth, which has an option for sustainable investing.

True Wealth uses the same strategy as Selma in that it invests in the ETF, so it has the same sustainability quality as Selma. However, regarding sustainability only, Inyova is better than TrueWealth.

On the other hand, True Wealth is even cheaper than Selma and much cheaper than Inyova. With sustainable investing, True Wealth only costs 0.8% per year, so it will always be cheaper than Inyova.

Finally, True Wealth is slightly less user-friendly, but not by a huge margin.

Inyova FAQ

What is the minimum you can invest with Inyova?

You need to invest at least 2000 CHF to open an account with Inyova.

How much will you pay in fees for Inyova?

You will pay 1.2% of your portfolio to get it managed. If your portfolio gets bigger than 50’000 CHF, your fees will go down.

Who can invest with Inyova?

Every Swiss resident that is at least 18 years old can open an Inyova account.

What happens if Inyova goes bankrupt?

Your shares are stored in your name, in Saxo Bank. So if the service goes bankrupt, you can get back your assets.

Who is Inyova good for?

Inyova is great for people that want to invest in the most sustainable way.

Who is Inyova not good for?

Inyova is not great for people wanting to optimize their costs because of its relatively high fees (especially for small portfolios). Inyova is also not great for investors that want the option to invest sustainably or not since Inyova only offers sustainable investing.

Inyova Summary

A very good Robo-Advisor, with a strong focus on impact investing and sustainable investments.

Product Brand: Inyova

4

Inyova Pros

Let's summarize the main advantages of Inyova:

- Good focus on impact investing and sustainability.

- You can invest up to 100% in stocks.

- Easy account creation.

- Web & Mobile applications.

- Good diversification.

Inyova Cons

Let's summarize the main disadvantages of Inyova:

- High fees.

- Not possible to customize the portfolio.

Conclusion

This Inyova review should contain everything you need to know about their offer. Overall, Inyova is a good robo-advisor for investing sustainably in the future. It will let you invest very simply in the stocks and bonds of companies that positively impact the future.

However, this highly sustainable investment comes at a price. Inyova’s fees start at a very steep price. Below 50,000 CHF, you will pay a 1.2% fee on your assets. For me, this fee is too high.

Other alternatives allow you to invest sustainably in the robo-advisor world, and you will save on fees. Both Selma and True Wealth are significantly cheaper. Overall, I prefer passive investing, while Inyova is more active investing. But they provide a good diversification with over 1000 stocks.

Inyova is the only robo-advisor focusing on impact investing. Other robo-advisors have straightforward sustainable investing options but no strong impact investing options.

You can save even more fees by investing yourself. Most people overestimate the complexity of investing by themselves. Investing fees are very important, and there are significant differences between different investing levels.

What about you? What do you think of Inyova?

More reading

Selma vs Inyova 2026 – Best robo-Advisor for Sustainable Investing?

Impact or Simplicity? We compare Selma and Inyova, two popular Swiss Robo-Advisors, to help you choose between ease of use and sustainable investing.

Finpension Invest Review 2026 – Pros & Cons

Wealth management for all? Read our review of Finpension Invest. We analyze the fees and strategies of this private investment solution.

clevercircles Review 2026 – Pros & Cons

clevercirlcles is a new Swiss Robo-advisor, with a twist. They add a community feature to the system. Is that enough to shine? Let's find out.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Inyova changed their portfolio to have a unique portfolio. So customization of the portfolio per value is not possible anymore.

Dear Poor Swiss,

Thank you for sharing your experience, tips, and opinions! Your blog is one of the first places that come up whenever I search for my Swiss-related financial questions =) I learned about Inyova from you (and from Neon bank), and I decided to try it. Unfortunately, I didn’t have a positive experience, and now I doubt the company very much.

I hold a Russin passport but legally reside in Switzerland, working for a Swiss employer. Inyova is not opening an account for me because of my passport. Their main investment partner, Saxo bank, has forbidden opening accounts for holders of Russian passports soon after the escalation of Russian aggression in Ukraine a year ago. Inyova and Saxo claim that the policies are to follow EU sanctions, even though none of the sanctions forbid working with non-sanctioned Russian individuals, and most of the banks and brokers do not put forward such discriminatory policies. To me, it looks like Inyova is putting all the money of their clients into the bank that enforces discrimination, and it does not look aligned with their advertised promises of supporting only conscious businesses.

To make matters worse, they are not upfront about the issue. I learned about the problem only after I filled out all the forms for account opening — the customer service representative contacted me individually a few days later (after our chat they put a little note in their FAQ in one of the questions, but that’s all). As I understand, most of their clients do not know that their money goes to the bank which allows itself to discriminate against some people, hence cannot make a decision whether such a decision aligns with their investment values or not. This point also casts a shadow on Inyova as a conscious value-oriented company.

I would appreciate it if you consider adding a note on this story in your blog posts. At this point, I do not look for having an account with them, but I believe that their potential customers that look for sustainable and conscious investments should know about this situation.

Hi Maria,

Sorry to hear about your experience. I know a few Russians in Switzerland who have had some issues with their Russian passport, but not on that scale.

Remember that changing custody bank is a huge effort for an investment platform, so they cannot simply change in a few days. This may not align anymore, but I would not consider this a fault of Inyova since they have chosen SAXO much before the war.

Have you tried other platforms? Are there other examples of refusing Russians?

Thank you for your kind support 💙

It’s been a year since the policy was put in place. I do not consider the original Saxo policy (and backfire to the companies dependent on them) of Inyova, but I cannot appreciate how they are handling the situation now. So, I thought to share my experience for their potential customers to be informed =)

Selma is also dependent on Saxo bank, so their investment offer is not available to Russians as well. I know that Interactive Brokers are working just fine for us, so I assume services that depend on them (Investart, e.g.) would also work, although I haven’t tried them yet.