Wealth Tax in Switzerland in 2026

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

In Switzerland, we have something that very few countries have: a wealth tax. This means that we get taxed on the amount of our net worth. So, the more wealth we accumulate, the more we pay taxes.

This tax is often not properly considered when estimating taxes paid in retirement.

In this article, we see all there is to know about the wealth tax in Switzerland.

Wealth Tax

In our guide to Swiss taxes, we have briefly touched on wealth tax, but we have mostly focused on income tax. In this article, I will focus solely on the wealth tax.

In Switzerland, the wealth tax is levied by the cantons and municipalities. There is no federal wealth tax. This means you are entirely dependent on your canton for how much wealth you will pay.

The wealth tax is usually much lower than the income tax. Many people do not even pay wealth tax because their taxable net worth is lower than the deductions. However, as soon as you accumulate money (for retirement, for instance), you must pay significant wealth taxes.

Most cantons have a simple progressive system where you pay a higher tax rate on higher net worth. Since it is progressive, you pay different taxes on each tranche of your taxable net worth.

But some cantons have more complex systems with several wealth tax components. We will run a few examples later.

Taxable net worth

It is important to know that your wealth tax will be based on your taxable net worth, which is slightly different from your net worth.

The basis is the same as your net worth. The taxable net worth is the sum of all your taxable assets minus your deductible debts.

The main difference is that some of your assets are not included in the taxable net worth. The taxable net worth excludes assets tied to the second pillar, such as vested benefits accounts or funds in your pension fund. The taxable net worth excludes assets tied to the third pillar in a bank account or life insurance.

The second difference is how the value of some assets is calculated, especially real estate. The taxable value of your real estate is estimated by a basic value by the canton. For us, the taxable value of our house is about twice lower as what we paid. This is not the value you will have in your net worth.

Finally, depreciating assets like cars are also included in the taxable net worth. I generally do not recommend including them in your net worth because they will end up worth nothing. In the taxable net worth, they use formulas to compute the value of a vehicle based on its years. However, this should not contribute much to your taxable net worth.

Examples

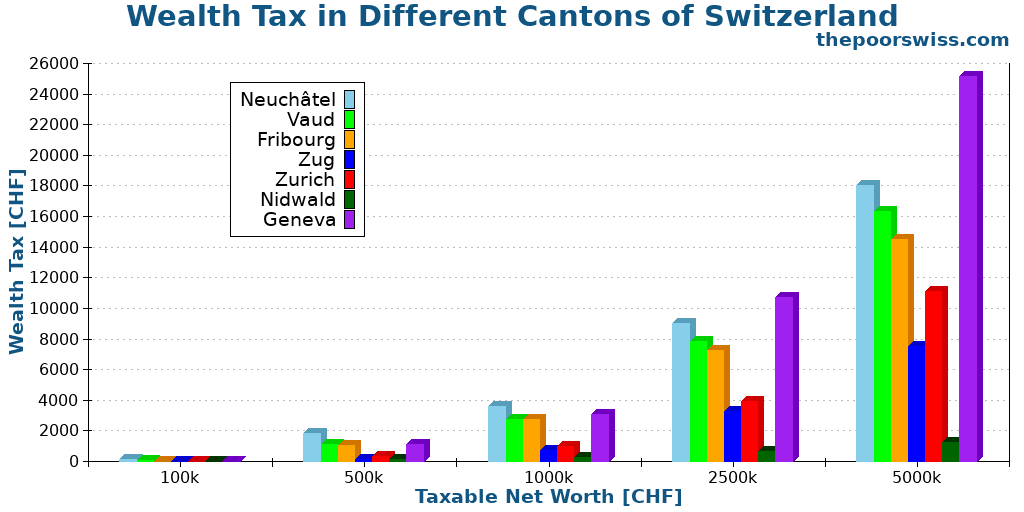

We will take a few examples of cantons. I use single-person examples because this can vary slightly for couples. I also only consider the cantonal tax. In practice, you would have to pay a tax for the municipality (a percentage of the cantonal tax). You can expect to pay about double these numbers once you consider the canton and municipality.

Nidwald has the simplest system. They have a deduction of 35’000 CHF and a tax rate of 0.025% on the taxable net worth.

Neuchatel has a simple system. The first 50’000 CHF are free. Then, from 50’0001 to 200’000 CHF, you will pay 0.3% of your taxable net worth, 0.4% up to 350’000 CHF, and 0.5% up to 500’000 CHF. Anything above will be taxed at 0.36%.

Vaud has a more complex system. You also get the first 50’000 CHF for free. But then, the rate increases from 0.048% to 0.3082% from 50’001 CHF to 2’000’000 CHF. Anything above that will be taxed at 0.339%.

Fribourg has a relatively simple system but with complex deductions. The tax rate grows from 0.05% to 0.37% between 50’000 CHF and 1’200’000 CHF. And anything above will be taxed at 0.29%. Deductions are different for couples and singles. For instance, singles get a 55’000 CHF deduction for a net worth below 75’000 CHF. But the deduction is reduced by 10’000 CHF for each extra 25’000 CHF of net worth.

Zug has a simple system. The first 200’000 CHF are free for single persons. Then, the first taxable 250’000 CHF are taxed at 0.0425%, the 250’000 at 0.085%, and then at 0.1275% for the third tranche. Anything above 750’000 CHF is taxed at 0.17%.

Geneva has a complex system. They are using two different progressive tax rates. The difference between the two rates is that the second tax rate is not counted for municipalities. Only the first is. In our case, we simply add the two values. Geneva is offering an 83398 CHF deduction on the taxable net worth.

Finally, Zurich has a slightly different system. You don’t pay taxes on wealth below 77’000 CHF. Then, from 77’000 you pay 0.50 CHF for each 1000 CHF extra. Starting from 308’000 CHF, you pay 1 CHF for each 1000 CHF. And this increases to 3 CHF for each 1000 CHF after 3’158’000 CHF.

We can compare these seven cantons based on a few taxable net worths.

It is clear from this graph that there are huge differences between cantons.

Neuchâtel is always very expensive. Geneva is also very expensive, especially when we reach high numbers. Vaud and Fribourg are mostly the same, after Geneva and Neuchâtel. Zurich is good and and Zug is great, both are much cheaper than the first four cantons. Finally, Nidwald is on a different plane with a very cheap wealth tax.

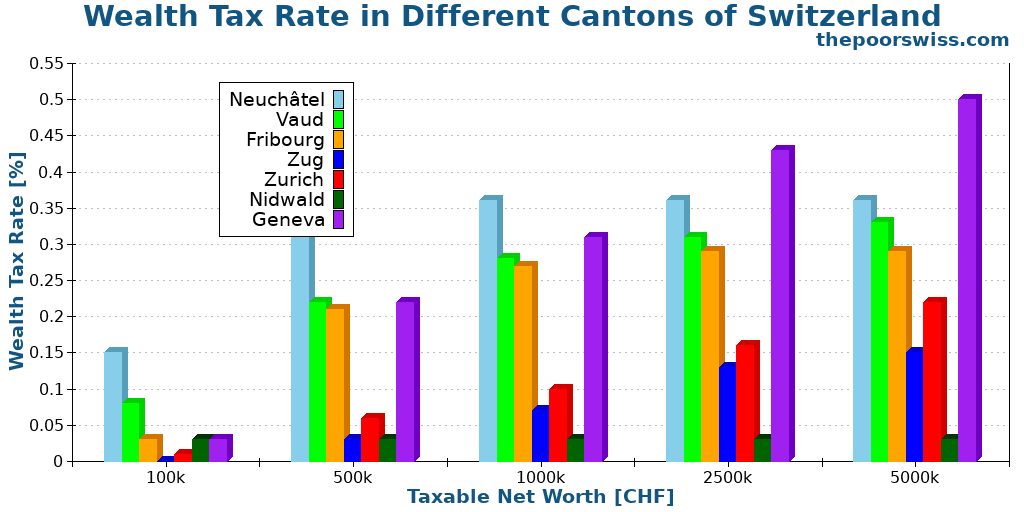

We can also present the results as the total wealth tax rate to compare better.

On this scale, it is easier to see the huge difference between the cantons.

When we think this number will be multiplied by the municipality tax rate, wealth tax can significantly affect your expenses.

Wealth tax and early retirement

If you plan to retire early, you must amass significant money. This amount of money means you will pay a significant wealth tax. So, how does this tax impact your retirement?

There are two ways to plan for wealth tax in early retirement.

The first way is simply to consider this as an extra expense. If your FI target is 2’500’000 CHF, you can estimate your wealth tax based on the canton you live in. For instance, for us, in Fribourg, it would be 7250 CHF for the canton and 6235 CHF for the municipality. But in Nidwald, it would be ten times cheaper.

Once you have estimated this number, you simply add it to your projected expenses in retirement. Since this will increase your FI number, you may have to do some math to get it right, but it is not very complicated.

The second way is to consider this wealth tax rate as a wealth management fee. When investing, we are trying to minimize investing fees. Any management fee will reduce your success rate in retirement if you follow Trinity Study withdrawal rates.

In that case, you will likely need to offset that extra fee with a reduced withdrawal rate. The result is again that this will increase your FI target.

Overall, planning for the wealth tax for early retirement is important. You will likely have to accumulate more money if you want t

Optimize your wealth tax

There are a few options to optimize our wealth tax. But these options are limited.

The first option is to move to a canton with a lower wealth tax. Since there are huge differences between cantons, geo arbitrage works well. Of course, this is not a simple solution, but this is likely the best way to optimize your taxes.

The second option is to decrease your taxable net worth. There are a few options to achieve that. The first option is real estate. In general, the taxable value of a real estate property is much lower than its real value. This means that your debt will often be higher than the taxable value, reducing the taxable net worth. Obviously, this may have a consequence on your income tax.

Another way to reduce your taxable net worth is to transfer money to non-taxable assets such as your second and third pillar.

Conclusion

The wealth tax is a relatively simple concept but with massive differences between the cantons. There is not much we can do to reduce this wealth tax.

The wealth tax is a form of double taxation. We are taxed on our income and then again on our savings when we accumulate money. I do not think this is a great way to tax people since this does not incentivize saving but spending.

For most people, the wealth tax will be negligible. It starts to matter when considering early retirement and the need to accumulate a lot of money.

In our case, we plan for the wealth tax as an extra expense for financial freedom. This wealth tax will increase over time until we can be financially free.

What about you? How do you account for the wealth tax?

More reading

How to Get Swiss Marriage Visa for a Chinese

Getting married in Switzerland? A complete guide to the Swiss Marriage Visa process for Chinese citizens, including required documents and timelines.

Is inflation in Switzerland really that low?

Recently, inflation in Switzerland has been very low, but is it really getting cheaper to live in Switzerland? Let's find out!

The costs of daycare in Switzerland

Daycare can be expensive in Switzerland! But how much does it cost really? We find out and devel into daycare costs.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

The main problem with wealth taxes is valuation, as the value of assets constantly rises and falls with market conditions and supply/demand. If you are wealthy and sell assets, realizing a gain, you have the money available to pay tax on the gain. In many countries if you subsequently sell assets whose value has fallen, and realize a loss, you may recover part of the tax you previously paid on the assets you sold. With wealth taxes this is not true. If you have become wealthy through your own efforts and have a high net worth, and in one year you pay wealth taxes on your wealth; then in the following year there is a global recession and the value of your assets drops drastically, you may still have to pay some wealth tax if your net worth still exceeds the threshold, but you get no taxes back from the prior year when the paper value of your assets was much higher. It is fair to tax wealth, even at substantial rates, but it should be on actual realized, proven wealth; either from sales in which you have actually received the cash value of the sale, and/or on the value of your estate at time of death, before it is distributed to your beneficiaries.

Hi phelan,

That’s a fair point. When we compare wealth tax with capital gains tax, there are two major differences:

* We cannot deduct wealth loss, but we can deduct capital losses

* We are taxed on our gains multiple times (each year) with wealth tax but only once with capital gains tax.

We are lucky to not have capital gains tax, but this is being compensated by wealth, which can be high in some cantons.

Good article.

I agree that it is double/ triple taxation (but most of the taxes are: you pay income taxes, then from your taxed income you pay municipal taxes, VAT on goods etc…), so I do not see why it should be perceived differently than any other tax.

Where I do have a fundamentally different point of view is whether it is a ‘good’ form of taxation, which I believe it is, as I see it as a much fairer/ socially beneficial tax than income tax.

In income tax you ‘penalize’ people who earn a lot (i.e., at least in theory, produce a lot of value), while with wealth tax, you ‘penalize’ people who own a lot (regardless of the source of this wealth, whether it is earned, inherited or received in any other way)

– Low/ no income tax rewards people who produce more value for society, which is the core for social mobility. Your economic situation is mostly driven by your performance that you more directly control

– Low/ no wealth tax (with low/ no capital gains) mostly rewards people with accumulated capital who often didn’t earn their wealth on their own, and is actually very bad for social mobility. Your economic situation is mostly driven by your ancestors’ (that you might even not know, unless you are first-generation rich) – that you had low/ no influence on

Hi Andy

That’s a fair point on income being taxed multiple times. However, wealth tax is taxed from income and is also taxed multiple times (canton, federal, and municipality).

The post says wealth tax is a form of double taxation. I found this article https://kof.ethz.ch/en/news-and-events/kof-bulletin/kof-bulletin/2024/07/wealth-tax-a-minimum-tax-on-the-rich.html which describes it more as a backup to income tax which is easier to work around.

Hi Hector

The problem with that approach is that everybody is impacted, even people who already pay a high income tax rate.

Unfortunately, the rich will always find ways around paying taxes and such taxes generally do not work well.

So, for standard people, it’s double taxation. But I agree that for rich people who manage to reduce their income tax rate to a low level, it’s a basic tax.

Every country has its own rules – and you can optimize around that.

E.g., afaik in GE you cannot escape wealth tax, but on 1-2 M CHF it is not the end of the world (especially compared to recent market returns). I checked with 2 tax advisors.

Now in GE what you can optimize is the income tax part. If you have kids, it is not hard to put it to zero even with 10K/month family income (which is plenty even in Geneva). Of course, you cannot get back then the withholding tax.

Example family #1: 2 jobs, but pays creche, deducts creche, but still high income tax

Example family #2: 1 job, or better, 2x 60% employment, more life, more time, 0% income tax

Of course, it is debatable whether the state should be supporting families like this – however, this is government policy and comes down to parties, elections etc. What we can do is to adapt. (On a sidenote we are internationals, and we are familiar with several countries’ benefit systems, and honestly Switzerland is one of the most kid-unfriendly European countries. But we are not here for the benefits, one job locks us here.).

I do not use a tax advisor, because their cannot save me anything. But if they can save you thousands, it is better to pay that 300-600 once.

Sorry for not taking my name publicly for this comment, but I do not want to get in the spotlight.

Yes, there are ways to optimize taxes.

But your second example family is a bit misleading in my opinion. They will have 120% income instead of 200%, so it makes a lot of sense that they have lower taxes. I am not sure I would call that an optimization on income tax, but rather a global optimization. I also not saying it’s a bad thing, but not always doable.

Hello, I think you might want to double check the numbers in this — I was surprised that Zug is higher than Zurich in your examples. When I use the online tax calculator, there’s a deduction of 204’000 CHF for single people in Zug, which means it works out much cheaper than Zurich. For a net worth of 400’000, Zurich gives 460 CHF per year tax burden (marginal wealth tax rate 0.22%) and Zug 111 CHF (marginal wealth tax rate 0.07%).

Hi boop

I will check it out. The numbers may have changed since I did the computations, a few years ago.

Indeed, they changed in 2024, will need to update that.

Hi Baptiste, I have been a long term follower of the blog.

As tax season is upon us some questions inevitably arise.

This one is regarding value thresholds to declare wealth. For example: physical cash, marketplaces balances (e.g. steam) or app account (Revolut).

I couldn’t find any information on this, but I am fairly certain declaring how much cash you had in your wallet is not expected (as opposed to a cabinet full of 1000CHF notes)

Hi Leonardo

That’s a very good question and I don’t think these thresholds exist.

As long as you don’t use this as tax evasion, I think there should be no issue.

I have never declared the few 100s in cash that I often at home. And if I have 50 CHF in my steam account or namecheap account, I would not declare it.

I think it comes down to good sense. Anything significant should be declared (let’s say 1000 CHF+) or anything that adds up (if you have 10 Revolut accounts, with each 100 CHF in it).

Thank you for great article Baptiste,

Using this imaginary numbers, did I got this correctly:

Say, I live in Zurich, and I have 100k invested in VT, plus I have 20k cash on my bank account.

120k – 77k = 43 * 0.5 = 21.5 CHF wealth tax

Hi Marko

Yes, I come to the same number in this example.

Thanks for your confirmation,

What bothers me here is they tax me on unrealised gains.

I can quite literally be losing money and would be forced to sell assets to pay wealth tax, assuming I’m not liquid.

This also mean ultra rich pay huge amount of money on their assets. I would be surprised if they havent find a way around this.

Yes, wealth tax will tax unrealized gains. For most people, this will not be a big issue because wealth tax is much lower than income tax. But if you are wealthy, this may become significant.

If you want to avoid it, you can take on debt or move to a cheaper canton. There is not much more we can do.

Hi Baptiste,

Great blog! Thank you for this post and the reminder e-mail! I have a question: do you know whether I can transfer more than the tax-deductible to the 3rd pillar, like the ETF part of my investment portfolio to avoid wealth tax?

Also I imagine for other currencies the govt. posts exchange rates we need to use to calculate, but what about crypto?

(Did not do it so far in case we buy real estate as getting the money out of 3rd pillar is also taxed and also the management fees on 3rd pillar investments are higher than on a standard IBKR account.)

Hi Lajos,

Normally, you can’t. The 3a provider will try to prevent this from happening.

About crypto, I have no idea. I would hope they do for biggest crypto coins, but I am not sure.

Thank you for the quick reply!

Hi Baptiste, Lajos,

Here is the link for the exchange rates including crypto, gold, foreign currencies, etc. I had it bookmarked from last year and just changed 2023 to 2024:

https://www.ictax.admin.ch/extern/en.html#/ratelist/2024

Hope it helps.

Thanks for sharing. I am very surprised (and glad) to see that they also share the crypto currencies values. This is very useful!

Hi Baptiste, I find your blog super helpful – especially as I’m new to Switzerland. In terms of the wealth tax, how is it calculated when it comes to investments (such as in index funds, gold, and crypto)? Is it whatever these numbers were on the 31st of December on the investment platform, or is it based on the initial investment made (since any loss/ win won’t be realised until sold), or something else? This info is hard to find online so I appreciate some details on how to calculate this. Thank you :)

Hi Martina

I am glad you find my blog helpful.

It’s based on the value at the 31st of December. So, to your point, it includes any unrealized capital gains.