Wealth Tax in Switzerland in 2026

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

In Switzerland, we have something that very few countries have: a wealth tax. This means that we get taxed on the amount of our net worth. So, the more wealth we accumulate, the more we pay taxes.

This tax is often not properly considered when estimating taxes paid in retirement.

In this article, we see all there is to know about the wealth tax in Switzerland.

Wealth Tax

In our guide to Swiss taxes, we have briefly touched on wealth tax, but we have mostly focused on income tax. In this article, I will focus solely on the wealth tax.

In Switzerland, the wealth tax is levied by the cantons and municipalities. There is no federal wealth tax. This means you are entirely dependent on your canton for how much wealth you will pay.

The wealth tax is usually much lower than the income tax. Many people do not even pay wealth tax because their taxable net worth is lower than the deductions. However, as soon as you accumulate money (for retirement, for instance), you must pay significant wealth taxes.

Most cantons have a simple progressive system where you pay a higher tax rate on higher net worth. Since it is progressive, you pay different taxes on each tranche of your taxable net worth.

But some cantons have more complex systems with several wealth tax components. We will run a few examples later.

Taxable net worth

It is important to know that your wealth tax will be based on your taxable net worth, which is slightly different from your net worth.

The basis is the same as your net worth. The taxable net worth is the sum of all your taxable assets minus your deductible debts.

The main difference is that some of your assets are not included in the taxable net worth. The taxable net worth excludes assets tied to the second pillar, such as vested benefits accounts or funds in your pension fund. The taxable net worth excludes assets tied to the third pillar in a bank account or life insurance.

The second difference is how the value of some assets is calculated, especially real estate. The taxable value of your real estate is estimated by a basic value by the canton. For us, the taxable value of our house is about twice lower as what we paid. This is not the value you will have in your net worth.

Finally, depreciating assets like cars are also included in the taxable net worth. I generally do not recommend including them in your net worth because they will end up worth nothing. In the taxable net worth, they use formulas to compute the value of a vehicle based on its years. However, this should not contribute much to your taxable net worth.

Examples

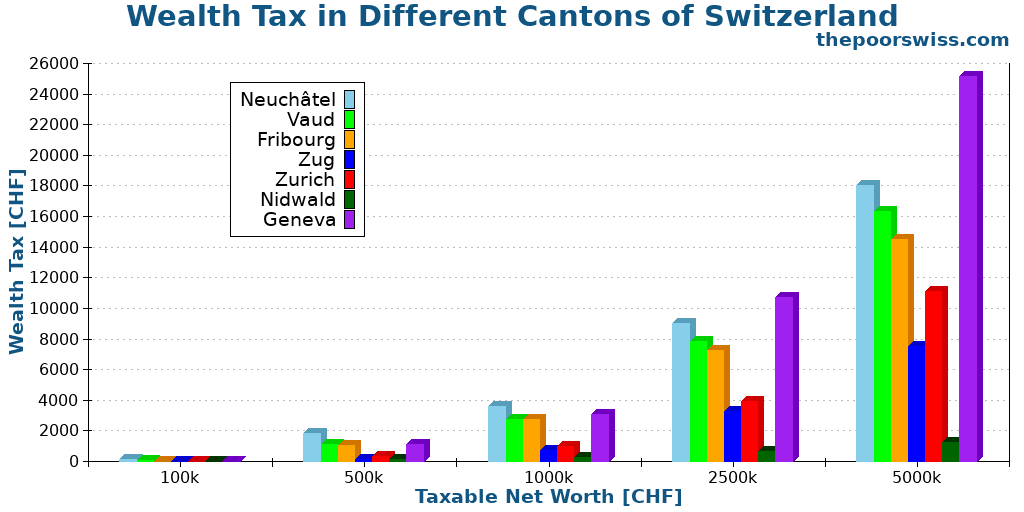

We will take a few examples of cantons. I use single-person examples because this can vary slightly for couples. I also only consider the cantonal tax. In practice, you would have to pay a tax for the municipality (a percentage of the cantonal tax). You can expect to pay about double these numbers once you consider the canton and municipality.

Nidwald has the simplest system. They have a deduction of 35’000 CHF and a tax rate of 0.025% on the taxable net worth.

Neuchatel has a simple system. The first 50’000 CHF are free. Then, from 50’0001 to 200’000 CHF, you will pay 0.3% of your taxable net worth, 0.4% up to 350’000 CHF, and 0.5% up to 500’000 CHF. Anything above will be taxed at 0.36%.

Vaud has a more complex system. You also get the first 50’000 CHF for free. But then, the rate increases from 0.048% to 0.3082% from 50’001 CHF to 2’000’000 CHF. Anything above that will be taxed at 0.339%.

Fribourg has a relatively simple system but with complex deductions. The tax rate grows from 0.05% to 0.37% between 50’000 CHF and 1’200’000 CHF. And anything above will be taxed at 0.29%. Deductions are different for couples and singles. For instance, singles get a 55’000 CHF deduction for a net worth below 75’000 CHF. But the deduction is reduced by 10’000 CHF for each extra 25’000 CHF of net worth.

Zug has a simple system. The first 200’000 CHF are free for single persons. Then, the first taxable 250’000 CHF are taxed at 0.0425%, the 250’000 at 0.085%, and then at 0.1275% for the third tranche. Anything above 750’000 CHF is taxed at 0.17%.

Geneva has a complex system. They are using two different progressive tax rates. The difference between the two rates is that the second tax rate is not counted for municipalities. Only the first is. In our case, we simply add the two values. Geneva is offering an 83398 CHF deduction on the taxable net worth.

Finally, Zurich has a slightly different system. You don’t pay taxes on wealth below 77’000 CHF. Then, from 77’000 you pay 0.50 CHF for each 1000 CHF extra. Starting from 308’000 CHF, you pay 1 CHF for each 1000 CHF. And this increases to 3 CHF for each 1000 CHF after 3’158’000 CHF.

We can compare these seven cantons based on a few taxable net worths.

It is clear from this graph that there are huge differences between cantons.

Neuchâtel is always very expensive. Geneva is also very expensive, especially when we reach high numbers. Vaud and Fribourg are mostly the same, after Geneva and Neuchâtel. Zurich is good and and Zug is great, both are much cheaper than the first four cantons. Finally, Nidwald is on a different plane with a very cheap wealth tax.

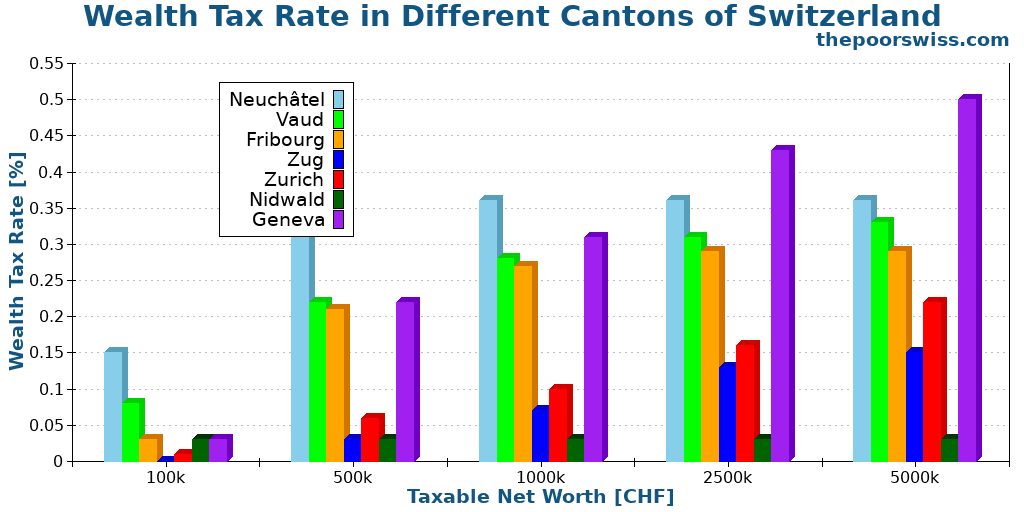

We can also present the results as the total wealth tax rate to compare better.

On this scale, it is easier to see the huge difference between the cantons.

When we think this number will be multiplied by the municipality tax rate, wealth tax can significantly affect your expenses.

Wealth tax and early retirement

If you plan to retire early, you must amass significant money. This amount of money means you will pay a significant wealth tax. So, how does this tax impact your retirement?

There are two ways to plan for wealth tax in early retirement.

The first way is simply to consider this as an extra expense. If your FI target is 2’500’000 CHF, you can estimate your wealth tax based on the canton you live in. For instance, for us, in Fribourg, it would be 7250 CHF for the canton and 6235 CHF for the municipality. But in Nidwald, it would be ten times cheaper.

Once you have estimated this number, you simply add it to your projected expenses in retirement. Since this will increase your FI number, you may have to do some math to get it right, but it is not very complicated.

The second way is to consider this wealth tax rate as a wealth management fee. When investing, we are trying to minimize investing fees. Any management fee will reduce your success rate in retirement if you follow Trinity Study withdrawal rates.

In that case, you will likely need to offset that extra fee with a reduced withdrawal rate. The result is again that this will increase your FI target.

Overall, planning for the wealth tax for early retirement is important. You will likely have to accumulate more money if you want t

Optimize your wealth tax

There are a few options to optimize our wealth tax. But these options are limited.

The first option is to move to a canton with a lower wealth tax. Since there are huge differences between cantons, geo arbitrage works well. Of course, this is not a simple solution, but this is likely the best way to optimize your taxes.

The second option is to decrease your taxable net worth. There are a few options to achieve that. The first option is real estate. In general, the taxable value of a real estate property is much lower than its real value. This means that your debt will often be higher than the taxable value, reducing the taxable net worth. Obviously, this may have a consequence on your income tax.

Another way to reduce your taxable net worth is to transfer money to non-taxable assets such as your second and third pillar.

Conclusion

The wealth tax is a relatively simple concept but with massive differences between the cantons. There is not much we can do to reduce this wealth tax.

The wealth tax is a form of double taxation. We are taxed on our income and then again on our savings when we accumulate money. I do not think this is a great way to tax people since this does not incentivize saving but spending.

For most people, the wealth tax will be negligible. It starts to matter when considering early retirement and the need to accumulate a lot of money.

In our case, we plan for the wealth tax as an extra expense for financial freedom. This wealth tax will increase over time until we can be financially free.

What about you? How do you account for the wealth tax?

More reading

9 Reasons to Live in a Small Village

City or Countryside? Discover the advantages of living in a Swiss village, from lower taxes and cheaper rent to a quieter lifestyle.

How to Get Swiss Marriage Visa for a Chinese

Getting married in Switzerland? A complete guide to the Swiss Marriage Visa process for Chinese citizens, including required documents and timelines.

The Poor Swiss versus the Average Swiss Household

How do we compare? See how our expenses and savings rate compare to the average Swiss household and discover where we save the most money.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Besides topping up our Pillar 2 with a recent inheritance from an American relative, can gifting some of the funds to children (into their accounts) to pay for college, lower our wealth tax? What would be the implication for our children when they are under age (we are on their accounts) and when they turn 18 (our son will turn 18 next year)? Thanks! Your info has been helpful re IBKR. :-)

Hi Deborah

Until your children are of age, you are liable for the wealth tax on their accounts. So, until that point, there is not much you can do.

After that, you can do gift to your children (normally gifts to children are tax-free for them, but you may want to double-check that for your canton). In this case, they will then start paying for the wealth tax on their account.

Great post as always, Baptiste!

You suggest that buying property might be a good way to reduce wealth tax but with property you get the imputed rental income tax. Wouldn’t that be higher than the potential tax on the money if you say, kept in bonds?

Yes, you are right. This is only a way to reduce wealth but it is not without consequences on income tax. Bonds would not lower your wealth tax.

I am not advising to buy property to reduce the wealth tax, only mentioning that it probably would reduce it. I will make this clearer.

Learn from Baptiste, folks …

By the end of 2020 I had gained significant wealth by investing in various EMFs when COVID hit, since I knew it would rebound.

I was, of course, taxed on that wealth. I left the wealth in those EMFs and by March 2021, when COVID lockdowns started to end, their value had dropped. A LOT!

When I got my tax bill (for my wealth in Dec 2020) it was almost the total amount of my (March 2021 hugely reduced) wealth! I was shocked and it wiped out my entire savings.

I now know that real estate or third pillar would have helped greatly but I didn’t realise it at the time (bad tax advisor).

So, take heed readers. Baptiste is doing you a great service by sharing what he learns here; learn from him.

Best wishes

Hi,

I am not sure I understand how this is possible. To get a wealth tax equivalent to your wealth, you would need an insane amount of return and then a huge drop, like significantly more than 10x, no?

I do not have any legal ownership of the bank accounts owned by my two brothers who are asking me to be a joint depositor. My two brothers, both in their seventies and both with health/ medical issues. The want me to be able to withdraw the money in the joint bank accounts when they pass away.

Hi Gabriel,

Do you have a question? Normally, if you are your brother’s heir, you should get everything when they pass away and you should not need to be a joint depositor.

My question is if I agree to be a joint depositor to their bank accounts, must I declare these bank accounts as part of wealth when I file my 2024 income and wealth in Switzerland. My brothers are Philippines citizens and lives in the Philippines. Thank you.

I would say yes, but that’s more a question for an estate lawyer rather than for me, that’s too specific.

I understand from my bank that I could move my retirement capital of my second pillar in a private pension into a disinvestment plan. This means monthly payments over a fixed period (eg. 20 years) until the capital is exhausted. In addition I would be paid a small interest on the capital. The monthly payments are not taxed, the interest is. What do you think?

Hi JG

I have never heard of that. It sounds reasonable that the monthly payments are not taxed since you already got a tax on the capital withdrawal.

I would be surprised if this came with reasonable fees, so be very careful about those. If they can do better than 6.8%, it is interesting, but otherwise, it will be strictly worse than than simply getting a pension, no?

Great article! You missed a case of a geo-arbitrage by moving to a place that has no wealth tax (such as Madrid or Italy). Typically these places have a comparable “wealth appreciasion tax” (aka capital gains tax), but you can at least reset the “tax base” by selling everything while you are still a Swiss resident.

Hi Alex

True, but the title of the article being wealth tax in Switzerland, I did not want to delve in other countries :)

Great article, thank you.

This double taxation, *annually* for the rest of my life and retirement really infuriates me. Tax me fairly on my income when I earn it please, but don’t tax me yearly if I choose to save it and not spend it! It’s a harsh penalty for saving & minimizing debt.

As Petronius mentioned above, I expect it incents people to leave Switzerland at retirement age. And in my opinion, the benefit of no capital gains tax does not offset this wealth tax, as capital gains is a one-time tax at the time of the sale, not annually.

I am surprised more people don’t complain about this.

Hi Jason,

I also think this is not a very fair taxation, but there is not much we can do about it except for leaving like you said.

You could start a popular initiative to lift this tax. However, it may not be that popular because it mostly impact high capital people, which are unlikely to be the majority.

I have a contrarian view on that, actually. While I agree that it’s a case of double taxation, I find the wealth tax better than the income tax. It insentivises people to put money in the real economy (either by spending or investing) because idly sitting money would be eaten away. Income tax, on the other hand, is not discriminating (much) between people spending their salary away on, say, daycare and those who are just “getting richer” (assuming the same salary). So the income tax can also be perceived as less fair.

But what you about investing the stock market? Aren’t you investing in the economy?

Are foreign properties that was bought before arrival to Switzerland, as well as during our stay in Switzerland, are treated in the same way based on the taxation as Swiss real estate?

It depends on the country they are in and of tax treaties. But in general, real estate is taxed in each country and not only in the country you are living in.

It’ll probably bump your tax progression still (unless it’s Nidwalden with a flat rate).

It may, yes, but don’t forget about the mortgage, you are only owning a small portion of the real estate.

as always: excellent

Thanks, Frankie!

My two elderly brothers, who are non-Swiss Citizens and non-Swiss residents are requesting me to be added as a joint depositor to a bank savings account they currently maintain. If I agree, will 100% or 33% of the balance of the joint savings account be added to my wealth? Thank you for your attention.

Each of the three should be taxes on 33.33% only, otherwise the amount would be taxed three times.

By the way, I never contributed any funds to the savings account currently joined by my two brothers.

That should not change anything, I think.