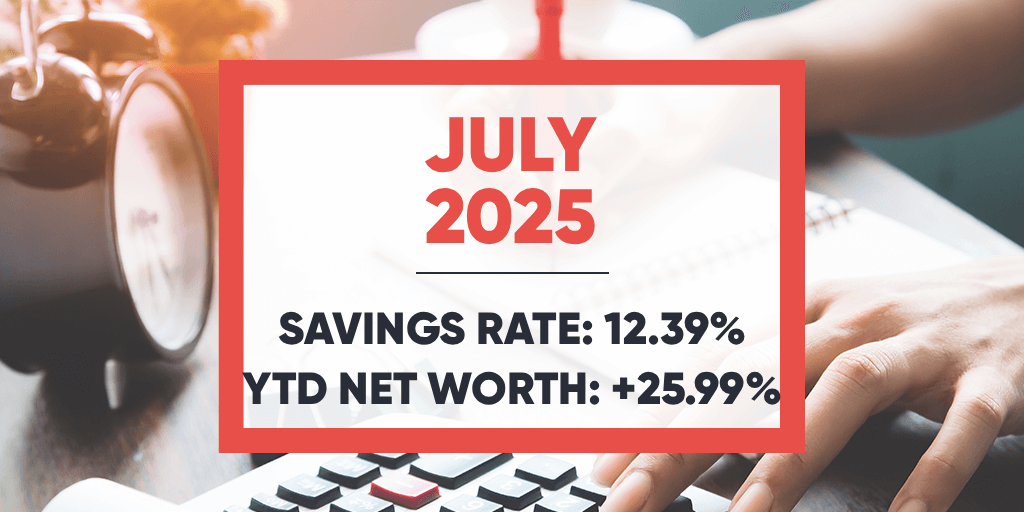

July 2025 – Buying a new house

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Last month, I mentioned there may be something big coming in July, and here it is: we are buying a new house. And before you ask: no, it is not a great financial decision, but we are prepared to live with it.

We are thrilled about buying our new house. But this will be a tiring period since we have to juggle between daycare holidays, buying a house, selling a house, and a new German course.

Financially, it was not a great month, but we still managed to save a little money.

July 2025

Let’s address the elephant in the room first: we are buying a new house. And you may ask why we are buying a new house when we bought the last one five years ago. Our current house is a semi-detached house, and we have always wanted an individual house but could not afford it in the past. Now that we can afford it, we have been looking around for the last six months or so. And we have finally found something we both like.

From a financial standpoint, this will likely take us back a few years on our path to financial independence. The new house is twice the price of the previous one. The mortgage will cost more, and so will maintenance. And we also have a few projects for the new house. However, we hope to stay in this new house until the end of our lives (or at least until our health permits it).

One big decision we had to make was whether we would sell the current house or rent it out. And we hesitated quite a lot. At the beginning, we were thinking of renting it out. But we then realized that conditions for investment mortgages are worse than we expected. And when we added the taxes this would incur along with the added work, we decided it was not worth it. Additionally, the value of our current house increased quite nicely in 5 years. So we can put back a significant amount of equity into the new house. It means we are reducing our opportunity cost.

That is not to say real estate is a bad investment. But a house is not a great investment in Switzerland. An apartment is a better investment if you want cash flow.

Of course, we will keep you informed about the financial implications of this new house and of selling the current house. I did not want to talk about it last month because we had not yet signed anything. Now, we have signed the contract at the notary and are preparing the move. We have also started the process of selling the old house, with pictures taken.

Another smaller event this month is that my wife started an intensive German course to increase her chances of finding a job. The opportunity is good, but the timing is not great since the course falls during the holiday season (daycare and kindergarten are closed). So, we have to juggle between buying a house, selling a house, and finding a solution for our son. As a result, I took all my days off between now and September already. I may have to take some unpaid leave as well depending on the house.

As a result, this month was a bit tiring, and the next one will be really exhausting. But we are very much looking forward to the new house. Once things are settled, we plan to really lay low and recharge the batteries.

Financially, the month was not great since we had to pay an advance to the real estate agency and are back to paying full taxes. But we still managed to save a little money, which will be allocated to the second half of the down payment.

Expenses

Here are the details of our expenses in July 2025:

| Category | Total | Details |

|---|---|---|

| Insurances | 831 | Health insurance for three |

| Transportation | 41 | A few buses and parking |

| Personal | 1202 | Many small events |

| Food | 1084 | Multiple meals out of the house and groceries |

| Housing | 3969 | Water, mortgage, heating, a few bills, and a deposit for selling the house |

| Taxes | 7757 | Taxes at the three levels |

In total, we spent 14886 CHF during the month. Without taxes, this amounts to 7129 CHF. If we do not count the deposit for selling the house, we only spent 3886 CHF, which is much lower than our goal.

We had to pay federal taxes again this month. So, we are back to paying full taxes until the end of the year. In theory, our payments should go down, but we have not yet received the final tax summary, so we are still paying based on our 2023 taxes.

So far, we have only had to pay a few expenses related to the house. The main expense is that we had to pay for the deposit on the real estate agency (we chose Neho). We also had to pay for a few official documents. Larger expenses will likely come in the following months.

Our food expenses are slightly high, but we had multiple meals out of the house. So I am fine with this extra budget this month.

Overall, considering that half of our expenses are in taxes and another quarter in the deposit, we have spent a very reasonable amount of money this month.

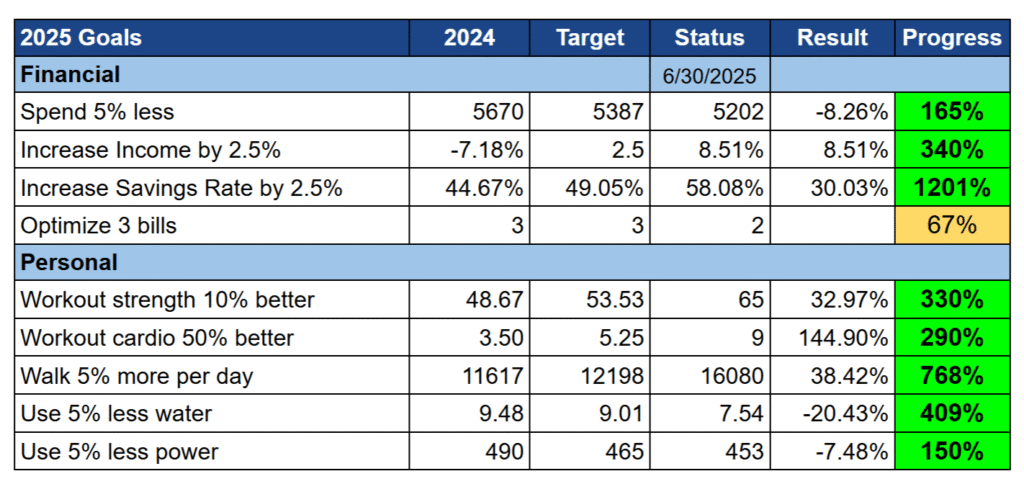

2025 Goals

Here is the status of our goals by the end of July 2025:

Overall, our goals are still doing well.

We managed to spend very little this month (if we do not count the deposit for selling our house). This reduces our average expenses significantly. This is great because this is usually the goal we are struggling the most with. On the other hand, our income was average, and our savings rate was bad.

This month was quite hectic in our schedule between buying a new house and preparing to sell the current one and the German courses. As a result, I did not do as many workouts as I would have wanted. This trend will continue in August and likely in September with the return to the office. I plan to go back to a full routine in October. But I will not give up during this time and will still do what I can but accept that there are limits. In any case, the status is much better than last year, so even if it goes down in the following months, I will be happy with it.

Our water and power goals are doing fine. But as soon as we are in the new house, this will be quite irrelevant. Indeed, we have a heat pump in the new house, which will replace the heating with a higher power bill. Furthermore, we will have a swimming pool, so our water bill will likely increase significantly.

Overall, I am entirely happy with our goals. We will have to revisit our goals once we are in the new house.

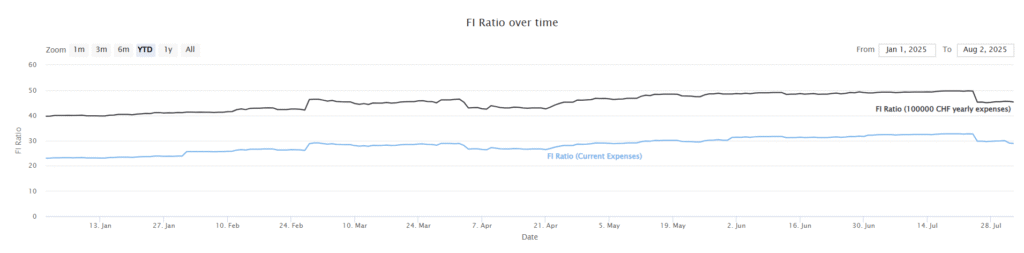

FI Ratio

Here is the progress of our FI ratio as of July 2025:

Our FI ratio has taken a big hit this month.

We have started piling up on cash since we had to do the first 10% prepayment this month. And we are getting ready for the second 10% in August. We think we should not stay out of markets for long since we plan to refill our accounts once the current house is sold.

Currently, our net worth did not go down much because of the house. On the other hand, our FI net worth is down significantly. This makes sense since the 10% of the down payment is moved out of the FI net worth since it is now locked in real estate.

Additionally, our expenses went up in July, lowering sligthtly our FI ratio based on current expenses.

Overall, this large drop was expected. This will go down again next month. And then, once we sell our current house, this will go up again. But it will take a few years to get back to the level of last month.

The Blog

Not much happened on the blog this month, the home projects took up most of our time.

We are continuing to increase our presence on social media. I am not sure if it makes a difference yet, but I think it will pay off in the long term. Once things have settled on the house side (likely early next year), I want to get back to doing some videos, either on YouTube or on TikTok.

On an entirely different note, I would like to mention the Free By 40 book by Mustachian Post. This year, the book reached 3000 copies sold, making it officially a bestseller. I reviewed this book a few years ago. If you are interested, you can also check out the official book page.

Next month, I have no specific plan, but I want to continue on writing my usual weekly articles, answering all comments and emails. I would like to go back to do some extra projects in October once we are fully settled in the new house.

Next Month – August 2025

In August, we will have more things to prepare for the move to the new house. We currently plan to move in early September. So, August will likely be spent about sorting things out and maybe making a few boxes already. We also hope to get a few visits for our current house. Additionally, my wife will continue her morning German courses, so we will not have much time overall.

Financially, August should be a fairly standard month. We probably will not have to pay any large expenses yet for the house. These will come starting in September. So, we should be able to save a little money. On the other hand, we will transfer the second half of the down payment and will therefore reduce our FI net worth even more.

What about you? How was July 2025?

More reading

June 2021 – A warm and quiet month

In June 2021, we went on a small vacation to Thun and spent too much money, but we still managed to save more than 50% of our income!

Why I Will Never Recommend Bluehost Again!

Bluehost terrible hosting quality made my website unavailable for more than one day. And the support keep making it worse. I don't recommend them anymore.

August 2018 – Wedding and honeymoon

In August, we had a second wedding ceremony with more friends and family and went on our honeymoon, in Egypt.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Yes, before the end of the year the tax office sends the calculation with tax credit split into 12 payments. You can then ask for adjustment if your situation has changed or will change in the new year. Ialso think that the payments can be done on bigger portions if preferred.

Thanks for the details, Lubo. I wish we would get 12 payments in Fribourg as well.

Hi Baptiste, question about the income taxes in FR canton. I live in VD and your income taxes and payment frequency are confusing to me. Could you share what are the key elements of the personal income tax payments that you use in FR? Or feel free to point me to an internet resource where I can get some education. Thanks

Hi Lubo

In Fribourg, we pay taxes in advance for the year. So, in 2025, we are paying advance payments for 2025 taxes, but we will only know the final amount sometimes in 2026.

For some reason, we receive 10 bills for the cantonal taxes, 9 bills for the municipality taxes, and 6 bills for the federal taxes. This means that our monthly taxes are pretty inconsistent.

Does that answer your question? Is it different in VD?

Hi Baptiste,

Thank you for the answer. In VD we also pay advanced credits every month based on your last year tax. What got me to ask you about it is the fact that you have mentioned that you pay taxes on an off and not monthly which also results in unusually high tax amounts but than again this depends also on the income and tax optimization that you manage to do. So not comparable. Generally personal income tax as well as compulsory health insurance is supposed to be lower in FR than here in VD.

Hi Lubo

Do you pay every month (as in 12 bills per year)?

If you are interested, we also publish a final expense report each year: How much we spent in 2024 – Full Expense Report. This makes it easier to compare maybe.