How much we spent in 2024 – Full Expense Report

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

We keep track of all our expenses (or at least most of them). Each month, I publish a monthly update on this blog. And once a year, I also analyze the costs for the entire year. This yearly view helps me have a global view of what we spend.

I should mention that we do not really budget. What we do is really expense tracking in different categories. But having all our expenses in the same place really helps have a good picture of what is really going on.

In this article, we detail the expenses of our family of three for 2024, in the canton of Fribourg.

2024 Expenses

Before we get started, you can take a look at our 2023 expense report if you want a baseline.

For context, we are a married couple in the canton of Fribourg, with a three-year-old and one and a half income for 2024 (my wife stopped working this during the year). Be careful that you do not compare too much against others. It is better to try to improve yourself, rather than compare with others. It is also important to note that our internet bill is paid by the blog and since September 2024, our car is also owned by the blog.

Here are the totals of our expenses for 2024:

| Category | Total CHF | Difference | What is it? |

|---|---|---|---|

| State | 79’460 | +31144 | All taxes |

| Personal | 34’133 | +2739 | Everything else, for us, is not mandatory |

| Food | 13’297 | +1112 | Groceries and eating out |

| Insurances | 10’342 | +828 | All our insurance, primarily health insurance |

| Housing | 8’806 | -14198 | Mortgage, house fees, new windows, new boiler |

| Transportation | 3’275 | +833 | Car and public transportation |

| Communication | 574 | -601 | Phone and internet bills |

In total we spent 149’887 CHF. This is a 13’735 CHF more than in 2023 (a 9.1% increase). Without taxes, this amounts to 70427 CHF. This is 9290 CHF less than in 2023 (a 11.6% decrease).

The number without taxes is to take with a pinch of salt. Indeed, we did some expensive work on the house in 2023, which we did not do in 2024. So, we did not really spend less in 2024 than we did in 2023, we simply did less work on the house. Other categories actually increased significantly.

But the major change of the year is the insane amount of taxes we paid. The main reason is that we did not pay enough in 2023 (because of the delayed computation that that the tax office is doing) and this comes back at us. Fortunately, this should go down again in 2025 because the blog income is now in the LLC and we only withdraw a small salary from it.

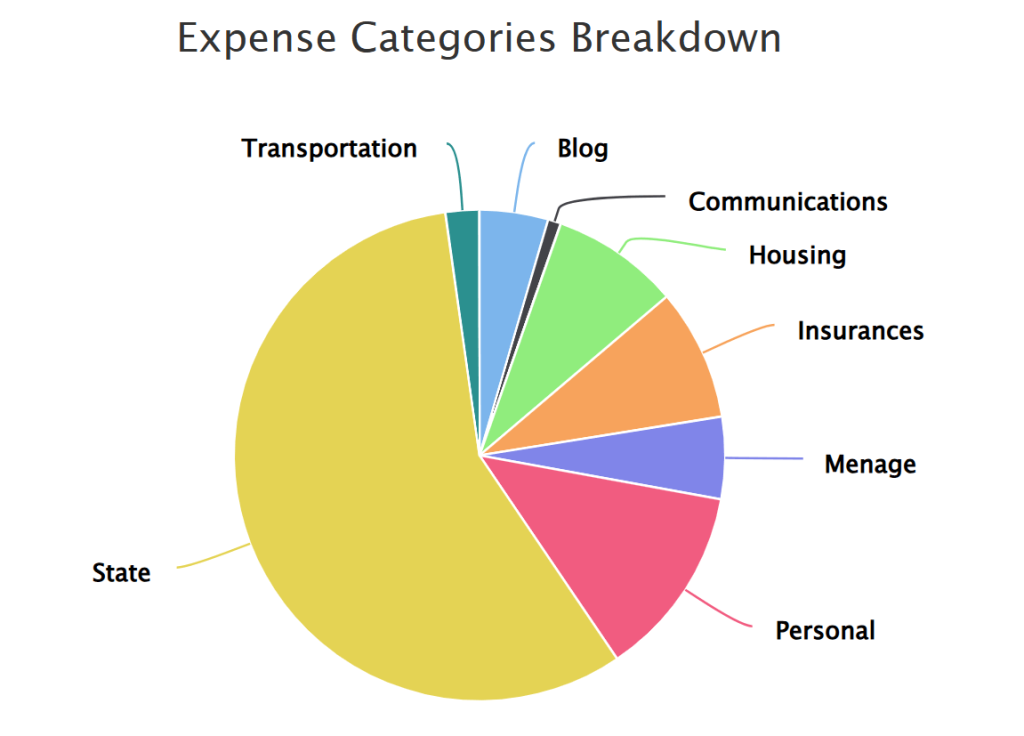

Here is a breakdown of our expenses per category for 2024:

Some of the main categories are making a huge part of our budget:

- Taxes are 51.9% of our total expenses

- Personal expenses are 22.3% of our total expenses

- Groceries and food represent 8.7% of our total expenses

In 2025, our taxes will go down (unless something really weird happen). And we need to work on our personal expenses which are often unjustified and very short-term expenses that we should avoid.

Biggest 2024 Mandatory Expenses

We can start quickly with the big mandatory expenses:

- Taxes: 79460 CHF

- Health insurance: 9376 CHF

- Groceries: 7971 CHF

- Daycare: 7407 CHF

- Mortgage: 3661 CHF

Together, these expenses make up a large part of our entire expenses. The only one of these expenses we could get rid of is the daycare. However, it currently fits well our lifestyle to have our son two days a week in the kindergarten and we do not plan to change that.

Our taxes should go down in 2025. Health insurance will of course go up even higher in 2025, as it does every. In 2023, we changed our health insurance, but did not change in 2024 (I was lazy). But we will probably change in 2025. We could lower our mortgage fees by amortizing more, but this does not make much sense from a financial point of view. And our groceries have increased, but mostly following inflation, so it is not too bad.

We can then take a look at some individual expenses.

Holidays 3775 CHF

We did not spend much in holidays in 2024. We only went for a short holiday in Germany. Then, my wife went to Amsterdam with friends. And then, my wife and son went a few days to Lucerne while I was working. I feel like we should have done more holidays together, but we did not have enough days of leave on my end unfortunately.

And the main part of the expenses is actually the plane tickets for China for 2025. So, we really did not spend much in 2024 for our holidays. I feel like this was a lost opportunity. I would rather spend money on something we would remember rather than on some unnecessary things.

New expenses

One new expense in 2024 is that I bought myself a large espresso machine and an espresso grinder. This total 2477 CHF plus about 1000 CHF of coupons. This is definitely a very significant expense, but I think it is entirely worth it. I am very happy about this expenses. I now do excellent espresso with my machine and I am really happy about this machine and grinder.

Things we improved in 2024

I do not feel like we improved a lot in 2024.

We reduced again our heating expenses. I think we have reached a good level and we are managing the heating system properly now. We also offset some of it by doing more wood fires.

This did not change anything for 2024, but I have finally canceled my usenet subscription. I used to download many things over newsgroups, but I have not done so in multiple years now. So it was high time I finally gave up. So, we will save 85 CHF in 2025.

Things that will change in 2025

There are a few things that will change in 2025.

Since our son is really fond of kindergarten (not so much of daycare), we will try to put him a second half-day in a second kindergarten that looks amazing. If we do and he likes, this will add 120 CHF to our budget.

Since we have created our LLC, the new car is now owned by the LLC instead of owned by us. This means that the car insurance, the car maintenance and the fuel will now be paid by the company instead of by us. On the other hand, since we also use the car for private trips, we have to declare extra virtual income in our taxes.

Other than that, I do not see any major change in 2025.

Things to improve in 2025

There are two things we should improve in 2025.

First, we need to be more careful about miscellaneous expenses. Often, we buy small things without thinking too much and then we do not use them as much as we thought we would. Or it was simply not as necessary as we thought. This is a pattern we have started these last two years. It is not totally out of control, but it is getting there. I would rather we think more about each of our expenses rather than simply go on Galaxus (for me) or Zalando (for my wife) whenever we think we need something. Unfortunately, this was also the case last year, so I do not know exactly how to break the trend.

The second thing is that we should be more careful about snacks when we are out on a small trip. We often buy a small drink here, a small thing to eat there and finally a lunch or dinner there. It is not a huge amount at the end, but it is probably not a great example for our son. We should get into the habit of having a healthy snack with us and then doing a real meal out rather than multiple small things.

There are probably other small things we could do, but I prefer to focus on a few things.

Conclusion

In 2024, we spent much more than in 2023. Most of this increase is due to taxes being much higher than previously. On the other hand, we spent much less on the house (having no renovation project in 2024), but we spent more on almost every other category.

As a result, our spending is more significant than it was before. So, we will have to be more careful in 2025 with our spending. Our main issue is our lack of control for small to medium expenses that we buy without really needing them. For large expenses, we are better because we think and discuss them through. But when you buy something for around 100 CHF or less, it is more difficult to really think through because it feels like not much on the grand scale of things. But they quickly add up to 1000 CHF and become a large expense. But anyway, we are not too deep in this trap, so we can still exit it.

What about you? How was 2024 for your expenses?

More reading

September 2025 – We moved in

In September 2025, we moved into our new house! We are thrilled about that. We also spent too much money, but we will get back to saving later.

January 2021 – Starting the new year in force

In January 2021, we managed to save 62% of our income and enjoyed living in our new house! Find out all the details!

October 2021 – Tiring but rewarding

In October 2021, we saved a large portion of our income, but got very tired because of the uneasy sleep of our baby.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

After 3.5 years of owning the machine and a steep learning curve (grind sizes, coffee beans, tools like WDT and spraying for minimal retention in its grinder) I can say it does very good espressos, on par with what I get in speciality coffee shops. So I will say I am happy with it, but I am looking for something more.

Thanks for sharing. It does take a while to adjust indeed. Even recently, after about one year, I am still improving my process.

Hi Baptiste, how do you manage to keep your yearly transportation costs so low? If I look at car tax, car insurance, fuel, possible repairs/service + perhaps public transport for your partner, it’s super low. How do you achieve it? Looks like you rarely quit your home (or mainly walk / use a bike?).

Hi Curious

We indeed do not drive much (less than 10’000 km per year) and my wife has a half-price plan that shes uses regularly. Our son is currently below 6 and gets public transportation for free. As for me, I rarely use public transportation. I also work from home, so even lower costs.

Until September, we got an old car, very cheap. In September 2024, we switched to a new car, but the LLC of the blog is now paying for it. So, in the future, it will go down even more. I will mention this in the article.

Morgen, i love your blog.

I am an expat and it`s has been super useful, since i moved to switzerland.

I am interested in understand why you pay so much in taxes. because i live in Zug with a salary over 100K and i am paying 21% of taxes from My income.

Hi Jean Pierre

Thanks, I am glad this is useful.

The reason I pay so much taxes is because I live in Fribourg, which pretty much sucks in that regard, especially compared to Zug which is considered a low-tax canton.

Hi Baptiste,

Thanks for the article, would be grateful to understand in more detail the Insurance breakdown, how you achieve this number as ours seems to be much more :).

We are a family of 4 (2 adults, 2 kids), and we pay around

– 14k: health

– 410: personal liability & contents

– 600: Legal

– 160: Travel

– 1’300: Life Insurance

Do you have all these, how do you manage the risk. Any input would be great :)

Thank you

Hi Tyrone

Sure, here are our details:

* Health: 9376 CHF

* RC and contents: 333

* Legal: 332

Your health insurance is indeed higher, but you have one more kid. This can vary a lot per canton (we are in Fribourg) and on your complimentary insurance (we have very few of these).

We don’t have pure risk life insurance or travel insurance. There is not much risk that would be covered by these two in our case I think.

Besides coffee machine : ) One thing I didn’t see in your budget are proper investments. Why are they not factored in? I would imagine – and I think I have read on this blog, that when you receive your salary you are investing a a variety of stocks using IBKR. Is this not correct? THx..

An investment is not an expense :)

For me, an investment is anything that leaves an account in my name for another account that is not in my name. An investment is a transfer from two of my accounts.

I agree, but I think there’s a distinction to be made. Although it is not a traditional expense like rent/groceries, it’s still money that leaves your cash flow and affects your overall budget. Collins defines investing as putting your money to work for long-term growth, suggesting that it is an intentional financial decision that should be accounted for – even though the money is still ‘yours’ in an investment account, it’s no longer available for immediate use.

I mention this because i’m curious to see its impact overall.. like what portion of overall spending is allocated to investments.

I am not saying savings are not important, I am only saying they have nothing to do with expenses :)

We track our income and we track our expenses. Then, savings are simply income-expenses. If you are curious, we saved/invested about 130k in 2024.

I see what you’re saying—you’re separating expenses from savings/investments conceptually. Makes sense! My point was more about how investments still impact cash flow, even if they aren’t ‘expenses’ in the traditional sense. Since investing redirects money from spendable income into long-term assets, some people (like me) prefer to include it in budgeting to get a clearer picture of financial priorities.

Either way, saving/investing $130K in 2024 is great—nice work!

It’s entirely true that you can also budget for cash flow and some people track each cash flow in their tracker. But personally, I never track from where money goes. But of course, this is only what works for me, it may not work for everybody :)

Thanks, that was indeed a good result!

What exactly to you mean when you write “..rather than simply go on Galaxus”? Is this a complaint about the convenience of these services?

The convenience of online ordering often removes the thinking out of a purchase. When you have to go to a shop to buy something, you think much more about something than if you simply go to a website, order it. There is a cost to convenience.

I am not saying that Galaxus is bad, far from it. But we should be careful about not being trapped by convenience.

Yes I totally agree, thanks for the clarification..

Really interesting to see your personal expenses over a year in such a detail. Would you say it helps you to improve your budget? And the end of the day it gives you transparency but is this enough to change your habits e.g buying snacks on trips?

Would be interesting to hear on how you try to implement your improvement opportunities in your everyday life.

Hi,

That’s a very good question. I believe it helps in maintaining a healthy level of expenses. But you are entirely right that it is difficult to break “bad” habits of spending.

Overall, we are able to keep our total expenses without expenses under control and I believe that this kind of thing helps. But on the other hand, in the 2023 reports, I had already noted that small expenses were a problem and we did not really manage to “solve” it.

I think you’re being way too hard on yourself. For a family of three in Switzerland, your expenses are already incredibly low, and you’re doing a fantastic job managing your finances. Most people in your situation spend way more without even thinking about it, so you should give yourself some credit.

I get that you’re focused on reaching your financial goals, but don’t forget to actually enjoy life along the way. You mentioned feeling like you should have traveled more, and I completely agree. The time with your family now is priceless—you don’t want to look back in 10 years and realize you were too strict for no real reason.

You’re clearly on the right track, and honestly, you’ll reach your financial goals no matter what. But if you don’t allow yourself to enjoy the journey, it might not feel as rewarding when you get there. Just some food for thought—keep up the great work, but don’t be afraid to live a little!

You are probably right :)

My main issue with our expenses is that we are often spending on small things that do not really matter in the long-term and these things pile up. I do not think this is good. However, we probably do not spend enough on things that matter like taking some time out, having a dinner out with the family and stuff like this. We will need to do better in 2025.

Thanks for your feedback!

It would be easier for putting things into context if you would at least give a range of how much you earn. Or we need to dig around and make ballpark calculations.

It only matters for taxes, right? We have an income of about 260k per year.

I find it quite odd to consider taxes as expenses. These are not really much dependent on you, but mainly proportional to your gross income and wealth. The more your income and wealth will grow, the more every other expenses will be negligible and comparing yoy expenses won’t be much useful.

I don’t find it odd at all :) For me, an expense is everything that leave my bank account to go to a bank account that is not mine.

But I know that some people tend to “ignore” taxes.

Hi,

Just curious, what espresso machine and grinder have you got? I am also into this hobby :D

Hi Robert

Nice :)

I have a Profitec Pro 700 with Flow Control and a Niche Zero grinder. What about you?

Wow really nice.

I have a Breville Barrista Express, looking to upgrade to something like Niche Zero and something like Lelit Elizabeth.

I almost went for a Lelit myself.

Are you happy about the espressos on the Breville?

Stovetop not good enough for you guys? : )

Can’t do espresso on a stovetop :)

congrats on the new coffee machine! i would recommend Mame in geneva or la gazette in morgues for your bean supply.

once you start experimenting with specialty cofee i can expect your expenses to soar…also look into normcore for additional tools to make your life easier.

I currently buy my beans at Pausa Caffe, very happy with their coffee. I want to try something more local.

I haven’t used any normcore tools yet, but I bought quite a few MHW 3Bomber accessories on Galaxus.