Should you have a home bias in your portfolio in 2026?

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Many people use a home bias in their investing portfolio. These investors are allocating a large portion of their portfolio to domestic stocks. And this portion is not based on the size of their local stock market. But not every investor agrees with that strategy. And some people do not know what a home bias is.

So, in this article, we discuss whether investors should have a home bias in their portfolios. We also look at existing research on the subject.

Home Bias in investing

So: what is a home bias in investing?

You have a home bias when you dedicate a large portion of your portfolio to stocks of your home country. For instance, you could say that you are allocating 25% of your portfolio to Swiss Stocks if you live in Switzerland.

One important thing is that your home bias does not have to be in the country you are living in right now. If you plan to retire in another country, your preference should be toward this other country. For instance, if you live in Switzerland now but want to retire in England, you may want English stocks as your home bias.

In general, people should invest in a diversified way. If you believe in the efficiency of the market, you want to invest according to stock market valuations. So if your country represents 10% of the entire stock market, you should invest 10% of your portfolio in your country’s stocks.

So, if you invest more than this 10% in your country’s stocks, you have a bias (sometimes called a tilt) towards this municipality. This country bias is your home bias.

We will take the example of Switzerland. Switzerland is about 3% of the world’s stock market. I allocate 20% of my portfolio to Swiss Stocks. So, I have a substantial home bias towards Switzerland.

Benefits of Home Bias

There are two benefits of adding a home bias to your portfolio.

The first advantage is that if something gets bad in other parts of the world, it could reduce the volatility in your portfolio. A home country bias could greatly help you if you need the money at this time of trouble.

This first advantage also helps with currencies. If your bias is in CHF and the USD loses a lot of value, your shares in CHF will be safe from this devaluation. Again, this protection could help if you need to sell at the wrong time.

Research showed that a reasonable home bias (lower than 40%) could decrease volatility in local currency. If you want to retire by withdrawing your portfolio, it is essential to consider volatility.

The second advantage is that you know more about what you invest in. Investors will likely know a lot more about companies in their own countries. And investors are more likely to invest in what they know. So, if you need a home bias to start investing, you should have one, by all means.

Home bias hurts your diversification

Now, an investing home bias also has some disadvantages.

Since it is a bias, it will hurt your diversification and returns. Now, this will highly depend on how biased you are. Diversification is critical for reducing volatility by spreading your investment over multiple countries and different kinds of companies. With good diversification, you will have fewer risks of something happening in a country and ruining your portfolio.

How much such a bias will hurt your diversification will depend on its size. For instance, if your home bias is 80% of your portfolio, you are losing on a lot of diversification. On the other hand, if it is only 20%, it may help you in times of need, and the impact on diversification may not be that high.

While diversification is excellent, it also suffers from diminishing returns. When you have 60% of foreign stocks in your portfolio, the benefits of more diversification get lower. So going from 60% to 70% of diversification has less impact than going from 10% to 20%. Research from Vanguard confirmed these results.

Therefore, if you keep your home bias reasonable, you will not pay a higher price for diversification.

Home bias can be achieved with currencies

In practice, it is unlikely that a global event does not impact your home stocks. On the other hand, a large currency event in some countries could spare your home currency if it is strong.

So, in some cases, it does not have to be in the same country as your home bias, but it needs to be in the same currency. If you plan to retire in France, you could have a home bias with European stocks in Euro. Of course, if you plan to retire in Switzerland, you will be limited to Swiss stocks, which are the only ones in Swiss Francs.

But, you do not have to invest in Swiss stocks to get Swiss Francs in the stock market. You could get some cash, but it would lose value to inflation.

Something that would work instead is to have foreign stocks hedged in your local currency. With this technique, you would not lose on foreign diversification. And you would still benefit from having stocks protected from variations in other currencies.

Now, there are some disadvantages to currency hedging. It could be more expensive in the long term. And no conclusive data shows that currency hedging will yield better performance. And currency hedging will reduce your currency diversification.

Nevertheless, currency hedging instead of a pure home bias could be a good solution for many investors if they worry more about currency fluctuations than local events.

Home bias ETF may be cheaper

Are you ready to take control of your financial future? “Invest Your Money in the Stock Market” is your ultimate guide to building wealth through smart investing in Switzerland.

This step-by-step manual demystifies the world of stocks and ETFs, empowering you to invest confidently on your terms.

Sometimes, an investor may save money by adding a home bias ETF to his portfolio.

In some countries, it is more efficient to invest in domestic stocks than in foreign stocks. In that case, having a home bias will reduce your overall fees. And since we saw that investing fees were very important, doing so may help your overall returns.

It is not the case in every country. For instance, in Switzerland, you do not have lower taxes for Swiss Stocks than for foreign stocks. On the other hand, ETFs for Swiss Stocks generally have higher Total Expense Ratios (TERs) than foreign stocks ETFs. And the Swiss Stock Exchange itself is much more expensive than American Stock exchanges.

But there is one thing where they will differ: currency exchange fees. When you buy a U.S. ETF, you will need dollars. If the dollar is not your base currency, you must buy dollars with your local currency. Foreign exchange conversions are not free. If you have a good broker like Interactive Brokers, these transactions will not be expensive. But for many other brokers, like DEGIRO, currency conversion can be expensive. So, this adds a fee that buying Swiss Stocks will not have.

Consider the big picture

One problem with home bias is that many investors are bad at considering the entire picture.

If you have a home bias in your primary investing portfolio but have a lot of home stocks in your retirement accounts, you are likely to have too large of a bias. As we saw before, a home bias that is too large will hurt diversification. In turn, a lower diversification will reduce your returns and increase the volatility of your portfolio.

So, you should consider your entire net worth and decide how much home country bias you want in this net worth. You should not consider only your investing portfolio. It is always essential to have a good view of where you are standing and what your assets are.

For instance, in Switzerland, you should consider your second and third pillars as well. You probably have more Swiss Stocks than you think. It is always a good idea for your asset allocation to represent your total assets, not a small portion of them.

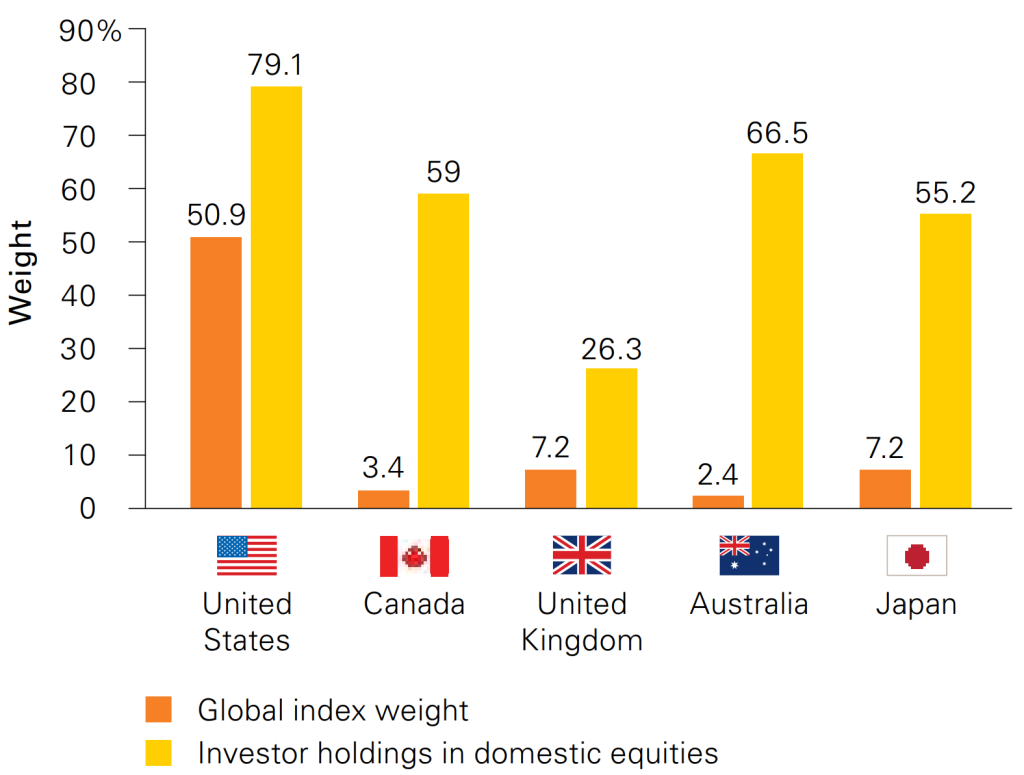

How much home bias do people have?

To understand what investors are doing, we can look at how much home country bias investors from different countries have in their portfolios.

I have found the results for five countries in a research paper by Vanguard.

As we can see, most investors have a strong bias toward domestic stocks. The most extreme example is Australia, where the domestic stock market is only 2.4% of the world, and Australian investors are allocated 66.5% to domestic stocks.

In the United States, investors have an extensive bias toward domestic stocks. On the other hand, the American stock market is half of the world’s stock market. So these investors are making themselves less of a disservice than Australian investors.

In the United Kingdom, the results are better. On average, English investors have 26.3% invested in domestic stocks. So, English investors are doing a better job at diversification than most.

I also found some interesting results from Vanguard for Switzerland. Here is what Swiss investors have in their portfolios on average:

- 43.79% of Swiss Stocks

- 36.97% of European Stocks

- 19.24% of Other Stocks

Two things are interesting in these results for Swiss investors. First, Swiss investors have a strong home country bias. They allocate more than 43% to domestic stocks. Also, Swiss investors have a second bias toward European Stocks.

Overall, Swiss investors invest more than 80% in European and Swiss Stocks. However, these stocks only represent about 25% of the world stock market. It means that Swiss investors have an extreme European bias.

These results are fascinating. I did not think that Swiss investors had such a bias. I would not recommend such a high bias towards Swiss or European Stocks. If you want both biases in your portfolio, you could do 20% in each and then keep 60% fully diversified globally. But I prefer having only a Swiss home bias.

Conclusion

While it is a bias, I still believe a home bias makes sense. However, it is not strictly necessary, and it should not be too large. Home bias in 10-40% may help you invest and protect yourself against some foreign events. But a more considerable home bias will hurt your diversification.

I like having a home bias in my portfolio. I want at least 20% Swiss stocks in Swiss Francs in my portfolio. Since I consider my allocation on my entire net worth, my allocation in Swiss Stocks ETF may be lower. But overall, I try to stick to this 20%. I want to have such a bias in Swiss Francs to hedge against foreign currencies getting deflated.

If you do not know what to do with your home bias, I recommend adding a small home bias to your portfolio. Doing so will likely reduce the volatility of your portfolio. And it could help if you need to sell when it is the wrong time for foreign stocks.

Continue to learn more about portfolios by reading about currency hedging and whether you should use it in your portfolio.

What about you? Do you have a home bias in your portfolio?

More reading

How to invest with high inflation?

Many people are wondering how to invest now that inflation is high again. We find out what we should do! And what we should not do!

Financial advisors – Do not get ripped off

Do you need advice? Learn the difference between fee-only and commission-based financial advisors and how to spot a salesperson in disguise.

Should Swiss investors worry about the US Estate Tax in 2026?

Avoid the tax trap. Learn about the US Estate Tax for Swiss investors and how holding US assets could expose your heirs to high taxes.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hello Baptiste,

Considering that I’m an expat in Switzerland, I’ve just arrived, and I’ll likely be here for a few years—not permanently (let’s say around 5 years, for example)… would it make sense to apply a home bias in CHF? I’m originally from Spain, so my home currency would be the EUR

Thanks,

Hi Juan,

No, I don’t think it makes sense in this case. If you are planning to go back to a EUR country, you can either prepare a home bias in EUR now, keep it for later or simply not have one.

You write, that there is no tax advantage in Swiss stocks. Maybe I’m missing something, but you get your withholding tax back on dividends on Swiss stocks when paying your taxes, while you “loose” 15% to the US government since you only get parts back with the double taxation treatment. This would be a strong argument for a Swiss home bias

Hi Gre

You are missing one detail indeed: we have a tax treaty with the US that reduces the effective withholding to 0%.

I have more details in this article: US ETFs are the best ETFs for Swiss investors

Thanks for the good article.

Before I put money into CHSPI (for example), I should know how my 3rd pillar is invested – am I right? That means that if my 3rd pillar is already strongly invested in Swiss stocks, I could consider that CHF amount to be my “home bias” and calculate its percentage weight in relation to my total wealth – right?

Do I have also to consider my 2nd pillar as “home bias”?

Thanks!

Hi FunMachine

Yes, it makes sense to consider the full picture. If your 3a is 100% in Swiss stocks, it may be an important enough to be your entire home bias (or a part of it). And same for your second pillar indeed. Depending on your asset allocation, your second pillar could be both your bonds and your home bias.

Hi Baptiste, thanks for your reply.

On the 3A I can decide how to invest it (it’ll be at Finpension soon). But I thought I can’t decide anything about how the 2nd pillar is invested – correct? Is there any way to know if it’s only bonds or how it is invested at all?

Thanks.

Correct, the second pillar is invested by the pension fund (except for the 1e plan but most people don’t have that).

Normally, each pension fund will report their investments quarterly (sometimes more and sometimes but at least annually). You can usually find them on their website.

Hello,

Thanks for this breakdown. I think an article would be helpful that would describe the scenario of “what would happen to my assets if I was living and earning in Switzerland, 80% my portfolio was in USD and USD lost 40% value with respect to CHF”. Do you accept the challenge? ;)

Hi Bambosz

I am not sure I understand. What would happen to my assets is obvious: They would lose 32% of their value (80% of 40%).

Over time, it is expected that the USD would lose value against the CHF. However, in the long-term the added returns of investing globally should make up for this.

I understand that this would be the case if the value dropped overnight and there would be no impact on the US stock prices (ETF share price would remain identical). I was thinking about a process taking some time (e.g. 1-2 years). My understanding is that, if USD was depreciated comparing to CHF, it would also lose value to other currencies and this would somehow affect the US-based ETF value (although not clear to me what would be the effect) beyond the simple currency exchange rate, but maybe I am wrong?

I have an unrelated question that I did not find a clear answer to (considering Alixis´post below): if I have CHF, does it matter which exchange I buy a given ETF at, beyond the spread/liquidity at a given exchange? I.e. if I was to buy at ETF X that is traded at SIX, Xetra or London Exchange, does the currency (or something else) matter if I buy through IB?

Thanks!

Hi

You are not wrong. It could cause indeed some changes to USD stocks because of import and export. And it depends whether this is caused by a weakened dollar globally or a strengthened Swiss franc. But it’s extremely difficult to predict how much USD/CHF woudl impact global stocks.

In the next 10-20 years, I would not be surprised if the dollar was 40% lower compared to the CHF. But in this time, the returns on the portfolio should have been enough to balance this.

The same ETF can be traded in different currencies indeed, on different exchanges. But it is still the same ETF. It does not protect at all against currency risk. You already mentioned spread and liquidity which is important.

The other difference would be in transaction costs since these are different for each exchange. Also, based on your broker, it may be cheaper to use the broker to do the currency conversion on a good exchange than let an expensive exchange do the conversion.

Hi Baptiste,

Thank you for this article. You write “If your bias is in CHF and the USD loses a lot of value, your shares in CHF will be safe from this devaluation”, which can’t be true in an efficient market, as the value of a share doesn’t depend on the currency it’s quoted in. For example, VWRL is traded in SIX, Euronext, and LSE, in three different currencies, but it makes 0 difference where you buy it (ignoring fees). When there is a movement in the CHF/USD exchange rate, stock prices will move to compensate for it.

Hi Alexis

The trading currency makes no difference whatsoever indeed. However, the holding currency makes a difference. I am talking about the difference between CHSPI (holding in CHF) and VWRL (holding in USD).

Hi Baptiste,

Thank you for the quick reply! I’m not sure I understand what you call “holding currency”. (Unless we start discussing bonds, in that context I agree with that you said)

Assume Nestlé moved their seat to France and their stock listing to Euronext, are you saying that this would make their stock price react differently to a EUR/CHF exchange rate change?

Or consider a Swiss company, listed in SIX, that only has customers in the US. Don’t you think that a devaluation of USD would cause their stock to drop?

Obviously, a USD crash would also impact Swis stocks, but not in the same way it would impact USD stocks. A USD ETF would be impacted based on the deprecionat, with a 1:1 ratio. An ETF holding Swiss stocks in CHF, would not impacted 1:1.

No, the USD ETF price would go up, compensating in part the USD devaluation. Similar to how CHSPI went down on January 15 2015.

Why would an USD ETF go up in CHF if if the value of the USD went down?

It would go up in USD. It could go up or down in CHF, it depends on many factors.

Look at VWRL vs CHSPI on Jan 15-16 2015. They dropped as much. This was an event where viewed from Switzerland, the USD lost a lot of value, and the shares in CHF were not safe from that devaluation (contrary to your assertion in the article).

Hey Baptiste,

I am reasoning on Swiss stock vs CHF cash as home bias for a Swiss resident having some US ETFs.

I’d tend to say that Swiss stocks would be a better option than cash, not only bc. cash loses value with inflation as you pointed out, but also because should the USD crash, then probably the Swiss stocks would go up more as a consequence of the fact that Swiss companies do business with the US and they would profit from the USD crash. Whereas if I kept cash, the CHF would be way stronger than USD but it would be always the same amount of CHF as I had earlier, it would not increase proportionally to the Swiss companies growth.

Does it make any sense?

Thanks

Hi Eva

Your assumption about the USD crash is unlikely to be true. The problem with a strong Swiss francs is that Swiss goods are too expensive for export and it makes it difficult for many companies to do business internationally. They won’t increase proportionally to the decline.

Having CHF cash would protect you against a USD crash more than Swiss stocks in my opinion.

Hi Baptiste,

right, it makes sense.

You wrote in the article: “I want to have such a bias in Swiss Francs to hedge against foreign currencies getting deflated.” and in your answer said the CHF cash would protect more than Swiss stocks in case of USD crash.

So, is inflation the reason why you still opted for Swiss stocks over keeping crash? Do you believe that inflation penalises more than what a USD or global market crash would do to Swiss stocks? Otherwise what’s your rationale (I know you wrote several other reasons why to keep home stocks, but what yours – if you don’t mind to share :)?

Thanks

Hi Eva,

Okay, I was not clear. CHF stocks will still protect you against some (but not all, my point!) of the USD crash since they are priced in CHF. But the stocks themselves will suffer as well.

There is no way to fully protect against a very strong USD crash because it’s the leading currency in the international markets. I believe that the best we can do is have a home bias in our portfolio.