Finpension Invest Review 2026 – Avantages et inconvénients

| Mis à jour: |

(Information: certains des liens ci-dessous peuvent être des liens d'affiliation)

Finpension gère déjà le meilleur troisième pilier et le meilleur compte de libre passage. Ils viennent de lancer Finpension Invest, leur service de robo-advisor. C’est une période très excitante.

Comme d’habitude, nous examinerons en détail les avantages et les inconvénients de ce nouveau service. Nous examinerons également les frais, les caractéristiques et la sécurité de Finpension Invest. À la fin de cet examen, vous saurez si vous devriez utiliser Finpension Invest et comment elle se compare à d’autres solutions.

| Frais de gestion | 0.39% |

|---|---|

| Coûts des produits | 0.10% |

| Coûts de retenue à la source | 0% – 0,15% (par canton) |

| Coûts totaux | 0,49% – 0,64% (par canton) |

| Stratégie d’investissement | Passif |

| Produits d’investissement | ETF et fonds indiciels |

| Investissement minimum | 0 CHF |

| Conversion de devises | Gratuit |

| Personnalisation | Très élevé |

| Durable | Pas par défaut |

| Langues | Français, allemand et anglais |

| Banque dépositaire | Finpension |

| Utilisateurs | 60 000 |

| Établi en | 2016 |

| Siège social | Lucerne, Suisse |

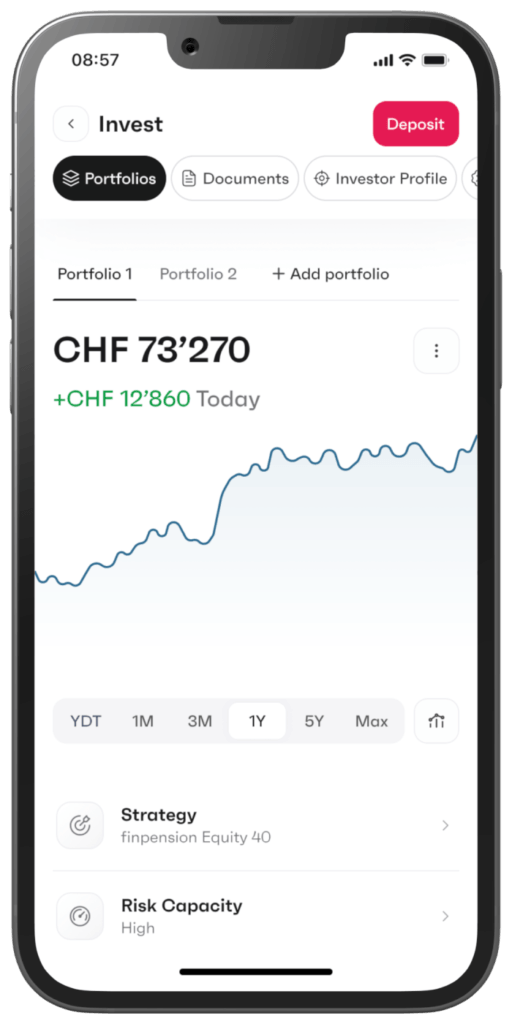

Finpension Invest

Un excellent Robo-advisor, optimisé au maximum, par Finpension.

- Optimisé pour les impôts

- Accès au marché privé

J’ai déjà longuement parlé de Finpension sur ce blog. À l’origine, il s’agissait d’un compte pilier 1e, puis ils ont commencé à offrir des prestations de libre passage parce que leurs clients voulaient garder leur argent avec eux lorsqu’ils quittaient leur emploi. Enfin, ils ont créé Finpension 3a.

Cette entreprise est fascinante parce que je considère son 3a comme le meilleur troisième pilier disponible à l’heure actuelle. Ils ont également réussi à obtenir le meilleur compte de libre passage.

Depuis leurs débuts, ils ont toujours eu une excellente réputation et ont été à l’avant-garde de plusieurs innovations. En 2026, ils gèrent plus de cinq milliards de CHF.

En 2024, ils ont introduit un nouveau produit dans leur gamme: Finpension Invest. Ce service est un robo-advisor en dehors du système de retraite. Ils avaient déjà fait allusion à ce projet en 2023, et c’est donc un plaisir de voir le produit final.

Il est important de noter que Finpension a été agréée comme maison de titres par la FINMA. Cela signifie qu’elles peuvent détenir elles-mêmes les titres et ne doivent pas faire appel à une banque dépositaire.

Pour des raisons réglementaires, Finpension Invest n’est proposé qu’aux résidents suisses.

Nous allons donc voir en détail ce qu’est Finpension Invest.

Stratégie d’investissement

Commençons par la stratégie d’investissement. Il est essentiel de voir comment un robo-advisor investit pour déterminer si nous devons l’utiliser ou non.

Finpension Invest utilise des fonds négociés en bourse (ETF) pour les actions. Pour les obligations, ils utilisent des fonds indiciels. L’utilisation d’ETF est la méthode standard de fonctionnement des robo-advisors suisses. La bonne nouvelle, c’est qu’ils n’utilisent que des ETF indiciels. Les ETF indiciels suivent un indice au lieu d’essayer de sélectionner des actions. Ils sont donc bon marché et, dans la pratique, ils battent même les fonds actifs.

L’utilisation d’ETF présente généralement un inconvénient en termes d’efficacité fiscale, mais comme nous le verrons dans le chapitre suivant, Finpension Invest ne souffre pas de cet inconvénient.

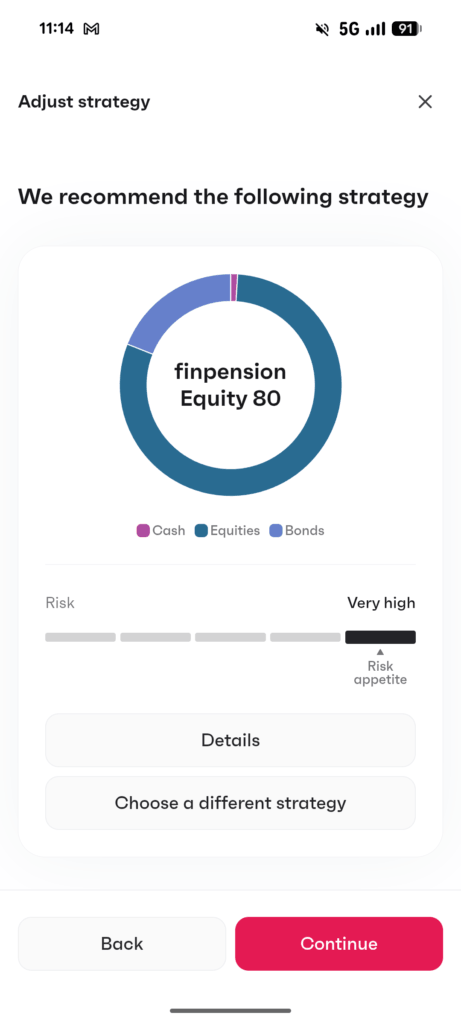

Il y a deux façons principales de mettre en place votre stratégie :

- Auto-Select : Préparera un portefeuille pour vous.

- Autosélection : Vous permet de préciser votre stratégie.

Dans tous les cas, vous pouvez atteindre jusqu’à 99 % d’investissement (en actions ou en obligations). Vous devrez conserver 1 % en espèces. Vous pouvez même conserver 99 % dans un fonds du marché monétaire si vous avez vraiment peur du risque.

La partie qui n’est pas investie en liquidités, en actions ou sur le marché monétaire sera investie en obligations suisses. C’est logique, car vos obligations sont là pour réduire les risques de votre portefeuille. Vous ne devez donc pas y introduire de risque de change. Et la couverture ne résoudrait pas le problème, car vous devriez payer les coûts de la couverture et payer un impôt sur le revenu plus élevé (en raison des rendements plus élevés des obligations étrangères).

Pour la sélection automatique, vous pouvez choisir entre trois axes pour les actions :

- Global : Entièrement diversifié au niveau international.

- Suisse : Investissez dans le monde entier, mais avec une forte préférence pour les actions suisses.

- Durable : Seulement investir dans des actions durables (à l’échelle mondiale).

Pour l’auto-sélection, vous disposez de quelques options supplémentaires :

- Global : Entièrement diversifié au niveau international.

- Europe : Investir dans le monde entier, mais avec une forte préférence pour les actions européennes.

- Suisse : Investissez dans le monde entier, mais avec une forte préférence pour les actions suisses.

- Broad Impact : L’investissement durable avec un impact global.

- Impact sur le climat : Investissements durables axés sur le climat.

- Impact social : Investissements durables à vocation sociale.

Enfin, comme c’est le cas avec Finpension, vous pouvez également créer un portefeuille sur mesure avec Finpension Invest. Cela signifie que vous pouvez choisir vous-même les fonds directement, parmi plus de 40 fonds disponibles. Vous êtes entièrement libre d’investir dans votre portefeuille.

Sur votre compte, vous pouvez avoir jusqu’à 10 portefeuilles différents. Chacun d’entre eux peut faire l’objet d’une stratégie différente.

Enfin, vous pouvez également investir sur les marchés privés. Les marchés privés sont des transactions effectuées en dehors du marché boursier public. Avec Finpension Invest, vous avez accès à deux fonds institutionnels pour l’investissement sur les marchés privés. C’est assez impressionnant, car aucun autre robo-advisor ne vous donne accès aux marchés privés.

Il est important de noter que les marchés privés ne seront proposés qu’aux personnes ayant un profil de risque très élevé (en fonction de vos réponses à l’évaluation des risques). Cette limitation a beaucoup de sens car les marchés privés peuvent être très volatils.

De plus, vous ne pouvez pas mélanger des fonds de marchés privés avec d’autres fonds dans le même portefeuille. Vous pouvez avoir plusieurs fonds de marchés privés (dans différents portefeuilles), mais chacun de ces portefeuilles doit être entièrement investi dans des marchés privés. Comme vous pouvez avoir 10 portefeuilles, ce n’est pas une grande limitation.

Dans l’ensemble, la stratégie d’investissement de Finpension Invest est excellente. Ils ont couvert toutes les bases, et ils offrent même un accès aux marchés privés, ce qu’aucun autre robo-advisor simple n’offre à ce jour. Ce service peut être un excellent outil pour l’investissement à long terme.

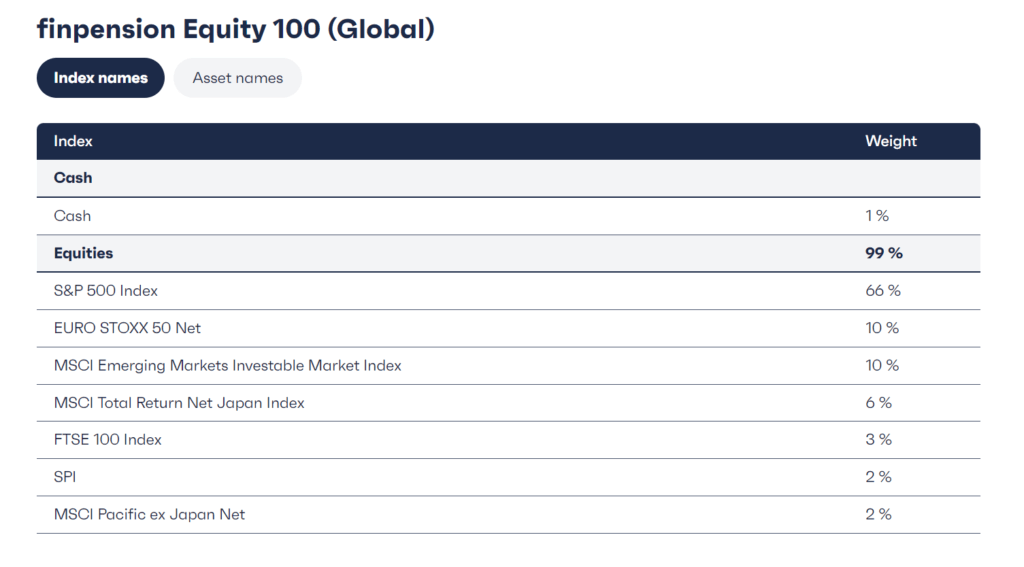

Exemple de portefeuille

Nous pouvons prendre un exemple pour examiner les détails des stratégies proposées par Finpension Invest. Pour moi, la stratégie Finpension actions 80 (Global) est un bon exemple à examiner.

Ce portefeuille est très bien diversifié puisqu’il couvre tous les marchés. Chaque pays et chaque région sont représentés en fonction de leur capitalisation boursière. Par exemple, la Suisse représente environ 2 % de l’ensemble du marché boursier mondial, alors que les États-Unis en représentent actuellement 66 %.

Vous serez peut-être surpris par le nombre de fonds. En théorie, il serait plus simple d’utiliser un fonds mondial et de laisser le fonds choisir les pays et effectuer le rééquilibrage. Cependant, comme Finpension Invest souhaite être particulièrement efficace sur le plan fiscal, elle doit choisir au moins un fonds pour les États-Unis afin de permettre à BlackRock d’effectuer pour elle le reporting complet des retenues à la source.

Ainsi, alors que je préférerais généralement ne pas avoir de pourcentages minuscules dans un portefeuille, dans ce cas-ci, c’est tout à fait logique et le portefeuille est très bien diversifié et équilibré.

Frais de Finpension Invest

En général, le meilleur critère pour distinguer deux robo-advisors est le prix. Pour maximiser votre rendement, vous devez minimiser vos frais. Il est donc essentiel d’analyser en détail les frais de Finpension Invest.

Finpension Invest a des frais de dépôt de 0,30 % et des frais de gestion de fortune de 0,09 %. Cela nous donne une commission totale de 0,39%. Ces frais incluent la TVA.

Il est important de noter que sur votre relevé annuel, ces deux frais seront indiqués séparément. Les frais de garde sont généralement déductibles de vos impôts dans la plupart des cantons. C’est donc une bonne chose qu’ils fournissent ces deux numéros séparément.

En plus des 0,39%, vous devrez payer le TER des fonds. En moyenne, il se situe entre 0,08 % et 0,10 %.

Enfin, le droit de timbre suisse est également dû sur les transactions (pour les ETF uniquement, pas pour les fonds indiciels) et n’est pas inclus dans la commission globale. En tant que gestionnaire de patrimoine, Finpension est tenu de facturer ces frais.

Comme ils utilisent des ETF, il n’y a pas de commission d’émission ou de rachat lorsque vous achetez ou vendez. Les frais de conversion de devises sont également inclus dans les frais.

Dans l’ensemble, les frais de Finpension Invest sont excellents. Des frais totaux d’environ 0,49 % sont vraiment parmi les meilleurs que l’on puisse trouver en Suisse.

Retenue à la source aux États-Unis

Nous avons dit précédemment que les ETF ont généralement un inconvénient en termes d’efficacité fiscale. En effet, les États-Unis imposent les dividendes à la source. Avec un ETF américain, vous pouvez éviter cela, mais pas avec un ETF européen, et aucun robo-advisor suisse ne propose d’ETF américains. Avec un ETF européen, vous perdriez 15 % des dividendes provenant des actions américaines.

Il est facile d’estimer ce coût. Les actions américaines représentent actuellement 66 % du marché boursier mondial et ont un rendement moyen de 1,50 %. Ainsi, en moyenne, la perte de ces dividendes équivaut à l’ajout de frais supplémentaires de 0,1485 % (arrondis à 0,15 %).

Normalement, ce n’est pas récupérable. Cependant, Finpension a mis au point une technique très innovante. Ils ont conclu un accord avec BlackRock (le fournisseur de fonds de l’ETF). BlackRock leur fournira toutes les informations nécessaires pour chacune des retenues de dividendes. Finpension peut ensuite les relier aux actions détenues par les utilisateurs. Et à partir de là, ils peuvent produire une déclaration qui peut être ajoutée à la déclaration d’impôts pour récupérer cette redevance !

Il est à noter que Finpension est actuellement en contact avec les différents services fiscaux pour valider cette technique. Mais nous savons déjà que Lucerne a accepté cette demande. Il y a donc de fortes chances que d’autres cantons suivent.

Les déductions DA-1 ne peuvent être demandées que si vous atteignez un minimum de 100 CHF. Le total comprendra les demandes de Finpension et éventuellement d’autres déductions que vous effectuez vous-même.

Cette fonction montre vraiment que Finpension connaît son métier. Cette fonctionnalité donne un avantage considérable à Finpension Invest par rapport aux autres robo-advisors suisses.

Ouvrir un compte Finpension Invest ?

Si vous avez déjà un compte Finpension (pour votre 3a, par exemple), vous pouvez directement créer un portefeuille Finpension Invest à partir de celui-ci. Sinon, vous pouvez commencer à créer un compte à partir de zéro, soit à partir du site web, soit à partir de l’application, et le processus devrait être assez rapide.

Comme pour tout onboarding de робо-conseiller, vous devrez répondre aux questions habituelles d’évaluation des risques. À partir de là, ils définiront votre capacité de risque. À partir de là, ils vous suggéreront des portefeuilles, mais vous pourrez passer outre ce choix.

Si vous ouvrez un compte Finpension 3a, veuillez utiliser mon code FEYKV5. Ce code vous donnera un crédit de frais de 25 CHF (si vous déposez 1000 CHF au cours des 12 premiers mois) et aidera également mon blog.

Dans l’ensemble, l’ouverture d’un compte chez Finpension Invest est assez standard.

Compte joint Finpension invest

Depuis juillet 2025, Finpension prend désormais en charge les comptes joints ! C’est une excellente nouvelle car très peu de comptes d’investissement joints existent en Suisse. Si l’une des deux personnes décède, l’autre personne peut toujours accéder au compte puisqu’il est à leurs deux noms.

Les deux personnes doivent résider en Suisse. Ensuite, elles doivent toutes les deux créer un compte chez Finpension. Ensuite, l’une d’entre elles peut convertir un portefeuille en portefeuille joint, et ce portefeuille appartiendra aux deux individus. Cela fonctionne avec un compte bancaire joint ou deux comptes bancaires individuels (dans ce cas, les deux comptes doivent être validés).

Il est excellent de voir cette fonctionnalité car elle peut être utile à de nombreux couples mariés.

Dépôts et retraits

Nous pouvons également voir comment déposer et retirer de l’argent de votre compte.

Tout d’abord, il convient de noter que vous pouvez commencer à investir avec seulement 1 CHF sur votre compte. C’est formidable, car de nombreux робо-conseillers ont des limites considérablement plus élevées.

Pour alimenter votre compte, vous pouvez effectuer un simple virement bancaire. Toutefois, vous devez déclarer vos comptes bancaires à l’avance. Cela signifie que vous ne pouvez transférer de l’argent qu’à partir d’un compte que vous avez déclaré, et ce compte doit être à votre nom. Vous pouvez enregistrer plusieurs comptes dans l’application.

Vous ne pouvez actuellement approvisionner votre compte qu’en CHF, comme la plupart des робо-conseillers.

En outre, vous pouvez également retirer de l’argent directement à partir des interfaces. Vous pouvez choisir vers quel compte enregistré vous souhaitez transférer de l’argent.

Dans l’ensemble, les dépôts et les retraits sont très pratiques chez Finpension Invest. Et nous verrons dans la section suivante que vous pouvez rendre les choses encore plus faciles en les automatisant.

Caractéristiques supplémentaires

En plus des fonctionnalités d’investissement de base, il existe également des fonctionnalités supplémentaires très intéressantes.

Tout d’abord, vous pouvez transférer de l’argent directement d’un portefeuille à l’autre. Cela peut être très pratique. Cela vous permet également de transférer de l’argent d’un portefeuille à un autre service, comme votre 3a. Je pense qu’ils ont fait un travail impressionnant en intégrant tous leurs services.

Vous pouvez entièrement automatiser votre investissement grâce à la réinvestissement hebdomadaire. Ainsi, les gens peuvent mettre en place un ordre permanent de leur banque vers leur compte Finpension, et tout sera investi au plus tard une semaine plus tard. Il s’agit en quelque sorte d’un plan d’épargne.

Et vous pouvez aussi faire le contraire avec un plan de désépargne. Cela vous permet d’établir un ordre permanent pour retirer de l’argent automatiquement et régulièrement. Par exemple, vous pourriez dire que vous voulez 1000 CHF par mois, et Finpension Invest vendra automatiquement suffisamment d’actions pour atteindre ce montant et l’envoyer à votre compte bancaire. Là encore, vous pouvez mettre en place plusieurs de ces plans pour chacun de vos portefeuilles.

Dans l’ensemble, il est excellent de voir que toutes ces fonctionnalités sont déjà présentes dans la première version de Finpension Invest. Dès le départ, ils disposent déjà de plus de fonctionnalités que la plupart de leurs concurrents.

Sécurité

Bien entendu, nous ne devons pas oublier la sécurité de notre argent. Vous ne voulez jamais envoyer votre argent à un service auquel vous ne pouvez pas faire confiance.

Contrairement à la plupart des робо-conseillers, Finpension Invest possède une licence d’entreprise de titres. Cela signifie qu’ils peuvent détenir directement des titres, sans dépendre d’une banque dépositaire tierce. Du point de vue de la réglementation, tout est en ordre.

Si Finpension devait faire faillite, les actions seraient en sécurité, car Finpension doit séparer les actifs des clients des siens. Cela prendra probablement un certain temps car il faudra le transférer à une nouvelle banque dépositaire, mais cela devrait bien fonctionner.

Il convient de mentionner que Finpension est rentable depuis 2019 (quelques années seulement après sa création). C’est important pour l’utilisation à long terme du service. De nombreux робо-conseillers en Suisse perdent de l’argent.

Je n’ai eu connaissance d’aucun problème technique de sécurité avec Finpension.

Le seul petit inconvénient est qu’il s’agit d’une nouvelle société de titres (depuis mars 2024). Cependant, Finpension elle-même gère de l’argent depuis 2016 et dispose de bien plus de 5 milliards de francs suisses d’actifs sous gestion. Cela leur permet d’acquérir une grande expérience.

Dans l’ensemble, l’argent chez Finpension Invest devrait être aussi sûr qu’avec n’importe quel autre robo-advisor suisse.

Alternatives

Un excellent moyen de se faire une idée de la qualité d’un service est de le comparer à d’autres solutions. Il existe de nombreux robo-advisors disponibles en Suisse. J’ai comparé Finpension Invest à trois services.

Finpension Invest vs True Wealth

TrueWealth est un excellent Robo-Advisor, à un prix très abordable. C'est le Robo-Advisor le plus adapté pour les investisseurs sérieux.

Utilisez le code SWISS100 pour recevoir un crédit de frais de 100 CHF.

- Très personnalisable

True Wealth est un robo-advisor très abordable, le plus mature disponible en Suisse. Ils disposent également d’un large éventail de fonctionnalités et sont sérieux.

Les stratégies d’investissement de ces deux services sont très similaires. Ils utilisent tous deux des ETF et se concentrent sur des ETF indiciels bon marché. Dans les deux cas, vous disposez d’un niveau de personnalisation très élevé. Un léger avantage de Finpension serait d’offrir un accès aux marchés privés, mais cela dépend de ce que vous souhaitez ou non.

Vous avez besoin de 8000 CHF pour démarrer avec True Wealth, tandis que Finpension Invest vous permet d’investir avec seulement 1 CHF.

En ce qui concerne les frais, True Wealth a des frais totaux d’environ 0,63 %, tandis que Finpension Invest est à 0,49 %. Il s’agit d’une différence importante. Il convient de mentionner que True Wealth a des frais dégressifs. Ainsi, si vous disposez d’un portefeuille important, True Wealth pourrait devenir moins cher.

Mais une fois que l’on tient compte de l’avantage fiscal de 0,15 % de Finpension Invest, il sera toujours moins cher que True Wealth. Il convient de mentionner que True Wealth dispose également d’une fonction permettant de récupérer les dividendes américains. Toutefois, cela dépend de la banque dépositaire que vous utilisez. Si vous utilisez la BLKB, vous ne bénéficierez d’aucun avantage fiscal. Vous ne l’obtiendrez qu’avec Saxo, car ils pourront alors utiliser des ETF américains. Mais cela est très mal documenté par True Wealth.

Dans l’ensemble, les deux ont plus ou moins les mêmes caractéristiques, mais Finpension Invest est nettement moins cher et a un minimum plus bas.

Finpension Invest vs Findependent

Findependent est un Robo-advisor très bon marché avec un focus durable, qui veut rendre l'investissement facile. Utilisez mon code PoorSwiss pour recevoir 20 CHF.

- Excellent frais

Findependent est un робо-conseiller plus récent avec des prix bas et une belle gamme de fonctionnalités.

Les deux robo-advisors utilisent des ETF. Findependent ne vous permet d’investir que 98 % en actions, soit un peu moins que les 99 % de Finpension Invest. De plus, par défaut, Findependent n’utilise que des ETF ESG. Vous pouvez créer un portefeuille personnalisé pour contourner ce problème. Dans l’ensemble, Finpension est donc plus flexible dans les choix, surtout avec l’ajout des marchés privés.

Vous avez besoin de 500 CHF pour commencer avec Findependent alors que Finpension Invest vous permet de commencer avec 1 CHF.

Du point de vue des frais, les deux sont très bien positionnés. Findependent facture des frais de 0,40 %, tandis que Finpension Invest facture des frais de 0,39 %. Mais les frais de change de Findependent sont beaucoup plus élevés (0,50 % contre 0,002 %) et les frais de bourse ne sont pas inclus dans Findependent. Et si l’on tient compte de l’efficacité fiscale supplémentaire de Finpension Invest, elle sera moins chère que Findependent. Toutefois, il convient de mentionner que Findependent applique des frais échelonnés (jusqu’à 0,29 % à partir d’un million d’actifs).

Dans l’ensemble, Finpension Invest présente des avantages significatifs par rapport à Findependent. Il est moins cher, plus flexible et comporte un minimum moins élevé.

Finpension Invest vs Selma

Selma est un autre robo-advisor qui cible davantage les débutants. Ils visent à rendre l’investissement simple, sans artifices.

Selma ne vous donne le choix qu’entre l’investissement durable et l’investissement standard. En outre, vous n’aurez pas le choix du portefeuille. Le portefeuille sera choisi en fonction de vos réponses aux questions de l’évaluation des risques. Il est donc plus facile à utiliser pour les débutants, mais il est presque moins flexible que Finpension Invest.

En ce qui concerne les frais, Selma a des frais de base de 0,68%, plus environ 0,22% pour les ETF, soit des frais totaux de 0,90%. Si l’on compare ce chiffre aux 0,49 % de frais totaux de Finpension Invest, la différence est très importante. Et si l’on tient compte des 0,15 % supplémentaires en termes d’efficacité fiscale, ce chiffre est encore plus significatif.

Il est important de mentionner que les frais de Selma peuvent être réduits si vous avez un portefeuille important. Les frais minimums sont de 0,42 % avec 500 000 CHF, ce qui est beaucoup plus proche de Finpension Invest.

Pour tout investisseur de niveau intermédiaire à avancé, Finpension Invest est une option bien meilleure en raison de sa flexibilité et de ses frais. L’utilisation de Selma impliquerait le paiement d’une prime importante qui devrait être bien réfléchie.

Finpension Invest contre VIAC Invest

En décembre 2024, VIAC a suivi Finpension avec son service de robo-advisor, VIAC Invest. Étant donné que ces services sont assez similaires, nous devrions les comparer plus en détail.

Une différence dans la façon dont les choses sont faites est que VIAC a créé ses propres fonds et investit les actifs des clients dans ceux-ci. Finpension, en revanche, utilise directement d’autres fonds. En pratique, cela fait peu de différence pour les utilisateurs, à moins qu’ils ne souhaitent personnaliser. Dans ce cas, Finpension a un avantage majeur en matière de personnalisation puisque vous pouvez choisir tous les fonds directement.

Les frais de base des deux services sont les mêmes à 0,49%. Cependant, VIAC Invest n’inclut aucun droit de timbre. Mais VIAC Invest a des frais de rachat et de souscription petits à moyens, tandis que Finpension n’en a pas.

La principale différence réside dans la manière dont les dividendes américains sont traités. Dans certains cantons, vous pouvez récupérer toute la retenue à la source avec Finpension Invest (0% de retenue). Dans d’autres cantons, vous obtenez la retenue habituelle de 15%. Malheureusement, VIAC Invest utilise des fonds suisses pour les actions américaines, ce qui entraîne une retenue de 30%. Cela fait une différence majeure en faveur de Finpension Invest.

Pour moi, cet avantage en termes d’efficacité fiscale est suffisant pour rendre Finpension Invest une meilleure option.

Si vous souhaitez en apprendre davantage, vous pouvez consulter ma comparaison détaillée entre Finpension Invest et VIAC Invest.

Finpension Invest FAQ

Combien de portefeuilles pouvez-vous détenir avec Finpension Invest ?

Vous pouvez avoir jusqu'à 10 portefeuilles, chacun avec une stratégie différente.

Quel est le montant minimum que vous pouvez investir avec Finpension Invest ?

Vous pouvez commencer à investir à partir de 1 CHF.

Qui peut investir avec Finpension Invest ?

Tous les résidents suisses âgés d'au moins 18 ans (et qui ne sont pas citoyens américains).

À qui s'adresse Finpension Invest ?

Finpension Invest est idéal si vous souhaitez investir en bourse (ou sur les marchés privés) et si vous voulez minimiser les frais.

À qui Finpension Invest ne convient-il pas ?

Finpension Invest n'est pas idéal si vous êtes un débutant en matière d'investissement ou si vous êtes suffisamment expert pour pouvoir investir par vous-même.

Finpension Invest Résumé

La gestion de patrimoine pour tous ? Lis notre évaluation de Finpension Invest. Nous analysons les frais et les stratégies de cette solution d’investissement privée.

Marque du produit: Finpension

5

Finpension Invest Avantages

- Frais impayés.

- Excellente efficacité fiscale.

- Vous pouvez investir jusqu'à 99 % en actions.

- Vous pouvez investir à partir de 1 CHF.

- Excellente stratégie d'investissement.

- Excellente intégration avec les autres services de Finpension.

- Applications web et mobiles.

- Personnalisation avancée.

- Accès aux marchés privés.

- Très transparent.

Finpension Invest Inconvénients

- Une solution entièrement nouvelle.

- Le droit de timbre n'est pas inclus dans les frais de gestion.

- Ne convient peut-être pas aux débutants.

Conclusion

Un excellent Robo-advisor, optimisé au maximum, par Finpension.

- Optimisé pour les impôts

- Accès au marché privé

Finpension l’a encore fait ! Leur nouveau service, Finpension Invest, est à nouveau un excellent service. Ils offrent un très bel ensemble de fonctionnalités, d’excellents portefeuilles et des frais de premier ordre.

Ce service offre des fonctionnalités très innovantes, telles que la prise en charge de la retenue à la source pour les dividendes américains. Maintenant que je vois cela, je me demande pourquoi aucun autre service n’est passé par là avant. Cela montre vraiment que Finpension est prête à faire un pas de plus pour fournir un service exceptionnel.

En voyant toutes ces fonctionnalités et ces frais ensemble, je crois maintenant que Finpension Invest est le nouveau meilleur robo-advisor disponible.

Par souci de transparence, je dois mentionner que je n’utilise pas moi-même de robo-advisor. J’investis directement par l’intermédiaire d’un courtier. Si vous avez les connaissances et la volonté de le faire, investir par vous-même avec un excellent courtier sera moins cher que d’investir par l’intermédiaire d’un robo-advisor.

Et toi ? Que pensez-vous de Finpension Invest ?

Prochains articles

Interactive Advisors Review 2026 – Avantages et inconvénients

Le Robo d'IBKR. Consulte notre évaluation d'Interactive Advisors. Ce robo-conseiller à bas coût peut-il rivaliser avec les alternatives suisses pour l'investissement automatisé ?

Revue de clevercircles 2026 – Pour et Contre

clevercirlcles est un nouveau robot-conseiller suisse, avec un petit quelque chose en plus. Ils ajoutent une fonction communautaire au système. Est-ce suffisant pour briller ? Nous allons le découvrir.

True Wealth Review 2026 – Avantages et inconvénients

Nous testons True Wealth, le Robo-Advisor suisse, afin de déterminer si ses faibles frais et ses stratégies ETF en font le meilleur choix pour votre argent.

Apprenez des moyens faciles d'optimiser vos finances et d'économiser des milliers de francs en Suisse avec notre e-book exclusif. Découvrez les services financiers les plus rentables adaptés aux résidents avisés et aux expatriés!

Obtenez votre guide suisse d'économies GRATUIT

Bonjour Baptiste,

Merci pour vos articles, grace à vous j’ai enfin ouvert un 3a chez Finpension (j’avais « peur » d’investir avant de vous lire :)! Je voudrais aujourd’hui ouvrir un Finpension invest (long terme, 100% actions), et je n’arrive pas à savoir ce qui ferait le plus sens: le Global 100 monde (celui de votre exemple, TER 0.08) ou un portefeuille personnalisé 85% MSCI ACWI + 15 % SPI (TER 0.18)? Est-ce que vous pensez que je perdrais les optimisation pour récupérer les dividendes US avec le portefeuille personalisé par exemple? ou les frais plus élevés « tueraient » mon bénéfice? Je ne sais pas sur quoi baser ma décision. Un grand merci :)

Bonjour corinne

Je suis content que vous ayez réussi à commencer à investir. J’espère que vous allez réussir à rester investie pendant de longues années.

Les deux portefeuilles sont très bien. Des frais de 0,18 % ne vont pas tuer votre bénéfice, ce sont des frais encore raisonnables. Si vous préférez avoir un portefeuille plus simple avec un plus grand biais suisse, le 85/15 me semble bien. Si vous préférez garder le défaut de Finpension, Monde 100 est pas mal du tout.

Bonjour Baptiste, merci pour la réponse! me voilà prête à investir :) C’est vrai que le Global 100 n’a pas de biais domestique (et je comprends pas de « buffer » contre la volatilité liée au change)…dans ce cas, j’envisage que mon portefeuille idéal chez Finpension pourrait être uniquement le MSCI ACWI à 99%, il serait plus simple (aucun rééqulibrage, moins de droit de timbre) et peut-être les rendements seraient meilleures qu’avec le Global 100 à long terme. J’ai 43 ans et j’ai envie d’une approche assez agressive, car ce portefeuille restera investi entre 20-30 ans. Si c’était le vôtre, vous auriez une préférence entre ces 2? Merci encore pour votre site, c’est un monde passionnant!

C’est probable en effet que ça soit un portefeuille plus agressif. Et c’est une approche très simple.

Ça dépend de ce que vous avez à côté. Avec un gros second pilier, on peut se permettre moins de biais domestiques, par exemple. Dans mon cas, comme j’ai un bon second pilier, je peux investir dedans et je peux réduire mon biais domestique, donc je pourrais avoir un seul ETF world.

Mais j’ai personnellement quand même un biais de 15% que je garde dans mon portefeuille.

Je ne peux pas choisir pour vous, les deux portefeuilles sont très bons :)

Bonjour, sur finpension invest on peut opérer que via un robots conseiller ou je peux le désactiver et tout faire moi-même.

Bonjour,

On peut faire un portefeuille customisé, mais on ne peut pas faire les opérations soi-même, c’est vraiment un robot-conseiller avec un haut niveau de personnalisation.

Bonjour,

En ouvrant un compte Finpension Invest, le mandat de gestion de fortune spécifie que » En acceptant par voie électronique le présent mandat de gestion de fortune, le client déclare accepter le statut d’investisseur qualifié ».

Pourriez vous me dire ce que cela signifie et implique au niveau règlementaire et fiscal car je ne suis qu un investisseur privé ?

Bonjour,

Je crois que ça donne simplement le droit d’accéder à certains investissements. Je vais me renseigner pour être sûr.

J’ai eu la confirmation de Finpension que c’était pour avoir accès à toutes les options d’investissement. Ça ne devrait rien changer autre que de pouvoir accéder à ces fonds.

Bonjour,

Merci de votre réponse. C est surtout au niveau fiscal pour un investisseur qualifié que j aimerai avoir plus d informations alors que je ne suis qu un simple particulier.

Merci à l avance

Bonjour,

Investisseur qualifié ne veut pas dire investisseur professionnel, ça ne devrait donc faire aucune différence.

Bonsoir Baptiste,

merci encore pour ces articles. Finpension me semble particulièrement adapté à mon cas.

Frais réduits et une gestion semi-automatisée.

J’étais en train de tester Neon Invest, qui permet certainement de comprendre certaines choses, mais en tant que débutant, j’ai du mal à avoir une vue d’ensemble claire sur l’état actuel de mon portefeuille.

En revanche, Finpension devrait aussi être moins cher que les portefeuilles proposés par les banques (certains commencent à 100 CHF par an).

Évaluation similaire pour le troisième pilier : pouvoir obtenir un rendement annuel de 4 à 5 % est nettement mieux que 0,5 % bancaire.

Bonjour Benno

Merci pour le partage de ton cas.

En effet, Finpension Invest est une excellente alternative pour avoir quelque chose de simple pour un débutant et sera clairement moins cher que les banques, même si plus cher qu’un courtier très bon marché.

Bonjour Baptiste,

Merci beaucoup pour ton article, ayant un nouveau 3a chez finpension, je me posais la question pour l’invest.

Si j’ai bien compris, il faut ajouter la taxe Droit de timbre suisse à chaque achat/vente ?

Ce qui veut dire qu’à chaque rééquilibrage on va être taxé ?

Bonjour Alexandra,

Oui, les frais de timbre sont dus sur les rééquilibrages, mais c’est proportionnel à la quantité de vente/achat, donc pas énorme en général à moins d’être très imbalancé. Mais c’est la même chose pour tous les Robo-advisors Suisses.

Bonsoir Baptiste,

Merci pour ta réponse, ça me permet d’y voir plus clair.

Je me posais la question suite à une réponse que tu as donné pour une autre personne. Tu as écrit: « Mais en pratique, c’est le contraire, la plupart des Robo-advisors font trop de changement et cela coute cher en frais et en performance »

Donc finpension invest c’est le cas ? Il y a le risque de trop de changements ?

Bonne question. Il faudrait voir en pratique après quelques années. Mais c’est probablement la même chose avec tous les robo-advisors.

Par contre, on peut désactiver le rééquilibrage avec Finpension Invest, ce qui n’est pas possible avec tous les services.

Hello Baptiste,

Merci pour la comparaison, super boulot.

Tu dis dans un commentaire qu’il est préfèrable d’investir soit même sur des ETF pour s’affranchir des frais des robots advisor.

Mais quid de l’arbitrage ?

J’ai remarqué que Truewealth par exemple, parfois vend, très rarement mais ça arrive.

J’imagine que cela participe à la performance.

Comment répliquer cela si on investit soit même ?

J’ai actuellement une performance chez Truewealth entre 12 et 15%.

Est-ce facilement accessible en investissant soit même sur des ETF world, sans arbitrer ?

Merci.

Bonjour Mathieu,

Quel arbitrage? Il y pleins de forme d’arbitrage. Il est vrai qu’en théorie pourrait faire mieux qu’une approche passive. Mais en pratique, c’est le contraire, la plupart des Robo-advisors font trop de changement et cela coute cher en frais et en performance. Je pense donc qu’il n’est pas intéressant de faire cela.

Salut Baptiste,

Un grand bravo pour ton travail, ta réactivité et tes articles que je suis régulièrement. Toujours un plaisir de te lire et d’en apprendre plus sur la finance personnelle.

Comme d’autres et après avoir lu ton article, j’ai démarré mon 3a avec Finpension et j’avais déjà remarqué l’option invest. Ce n’était plus qu’une question de temps avant que tu fasses ta review.

Il y a quelque temps, j’ai également lu ton article sur Investart qui est un robo-advisor aussi bon marché avec IB comme banque dépositaire… donc la possibilité d’avoir accès au ETF américains dont le fameux VT-Vanguard Total World Stock.

Cette app mobile peut elle soutenir la comparaison avec Finpension Invest ?

Merci d’avance pour ton retour.

Meilleurs messages !

Salut Marc

Merci, je suis content que ça te plaise!

Bonne question. Je dirais que Investart est encore moins cher que Finpension. Et, en théorie, encore plus efficace car ils utilisent les ETFs américains directement.

La grosse différence, c’est que Investart utilise Interactive Broker et garde donc l’argent à l’étranger, ce qui le place dans une autre catégorie. Mais c’est sûrement le robo-advisor le moins cher grâce à ça.

Salut Baptiste,

Merci beaucoup pour cet article claire et complet comme d’habitude.

J’ai déjà mon troisième pilier chez Finpension 3a et je suis très content.

J’apprécie beaucoup ta comparaison de Finpension Invest aux autres robo-advisors.

Si je veux changer mon robo-advisor actuel pour Finpension Invest à quoi faut-il faire attention (procédure complexe et couteuse) ?

Bien cordialement

Bonjour Ivan

Je suis ravi que l’article vous plaise :)

Il n’y a pas grand chose à faire attention, je dirais, à condition que ça soit pour le long-terme. Ca va faire des couts de vente d’un coté et des couts d’achat de l’autre. ET vous allez potentiellement être hors du marché pour au moins une semaine. Mais sur le long terme, c’est vite amorti si vous passez à un meilleur service.

Bonjour Baptiste et merci pour ton excellent article. J’ai grace à toi déjà investit dans le 3eme pillier de finpension (et pour la première fois je gagne vraiment de l’argent!).

J’ai commencé également à investir quelque centaine de Francs en ETF dans l’app Neon, que je trouve bien plus Beginner Friendly et stressant qu’un Interactive Broker par exemple (même si je passe également par ce service pour faire mes armes).

Derrière ce pavé ce cache une petite question en lien avec la fin de ta conclusion : passer par un Robot Advisor serait-il une bonne solution pour diversifier ses investissements? Ou le simple fait de diversifier ses ETF via son broker du coin suffit-il?

Bonjour Ed,

Merci pour le partage. Neon Invest est excellent pour faire ses armes!

Je ne pense pas qu’un Robo-advisor offre beaucoup de diversification si vous avez déjà un portefeuille diversifié avec un bon courtier. Ca permet de réduire le risque en évitant d’avoir tout dans un même service et certaines personnes apprécient ça, mais c’est pas nécessaire.

L’avantage d’un Robo-advisor c’est de tout simplifier pour les gens qui ne veulent pas investir eux-mêmes.

Hello, merci pour ta réponse.

Je pense que je vais tout de même investir une partie de mon épargne via finpension invest un peu pour les tester et aussi pour voir si en faisant les choses de mon coté via IB ou Neon j’arrive à reproduire les résultats ou à les dépasser.