Finpension Invest Review 2026 – Pros & Cons

| Updated: |

(Disclosure: Some of the links below may be affiliate links)

Finpension already manages the best third pillar and the best vested benefits account. And they have now launched Finpension Invest, their robo-advisor service. It is a very exciting time.

As usual, we will look into the advantages and disadvantages of this new service in detail. We will also look at the fees, features, and security of Finpension Invest. By the end of this review, you will know whether you should use Finpension Invest and how it compares to other alternatives.

| Management fee | 0.39% |

|---|---|

| Product Costs | 0.10% |

| Withholding Costs | 0% – 0.15% (per canton) |

| Total Costs | 0.49% – 0.64% (per canton) |

| Investing strategy | Passive |

| Investing products | ETFs and index funds |

| Minimum investment | 0 CHF |

| Currency conversion | Free |

| Customization | Very high |

| Sustainable | Not by default |

| Languages | French, German, and English |

| Custody bank | Finpension |

| Users | 60’000 |

| Established | 2016 |

| Headquarters | Lucerne, Switzerland |

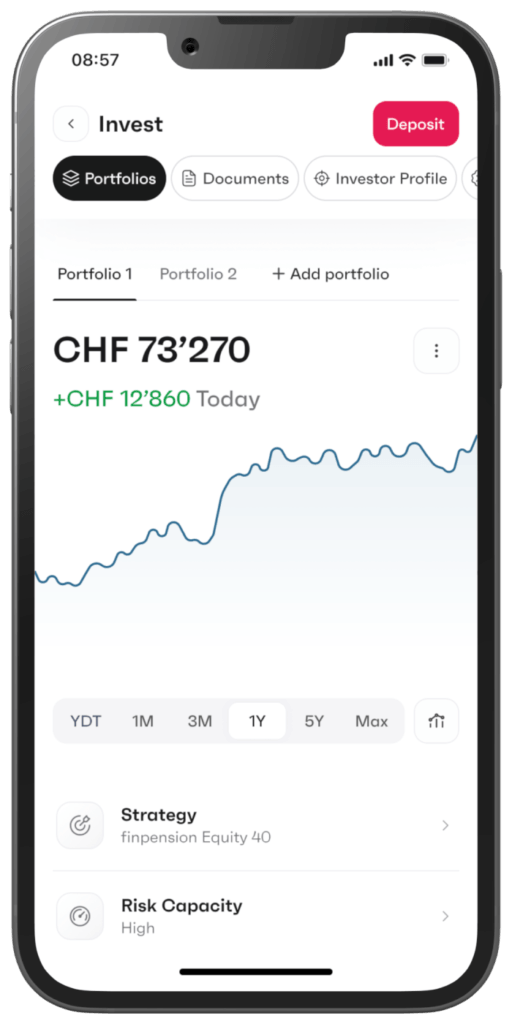

Finpension Invest

An excellent and innovative Robo-advisor by Finpension.

- Most tax-efficient Robo-advisor

- Access to private markets

I have already talked at length about Finpension on this blog. They originally had a 1e pillar account and then started to offer vested benefits because their customers wanted to keep their money with them once they quit work. And finally, they created Finpension 3a.

This company is fascinating because I consider their 3a to the best third pillar available at this time. And they also managed to get the best vested benefits account.

Since they started, they have always had an excellent reputation, and they have led several things in the way of innovation. As of 2026, they are managing over five billion CHF.

In 2024, they have now introduced another product in their lineup: Finpension Invest. This service is a robo-advisor outside the retirement system. They had been hinting at this already in 2023, so it is great to see the final product.

It is important to note that Finpension was approved as a securities firm by FINMA. It means that they can hold the securities themselves and do not need to use a custody bank.

For regulatory reasons, Finpension Invest is only offered to Swiss residents.

So, we will see in detail what Finpension Invest is.

Investing strategy

First, we will start with the investing strategy. It is essential to see how a robo-advisor invests to see whether we should use it or not.

Finpension Invest uses Exchange Traded Funds (ETFs) for stocks. For bonds, they use index funds. Using ETFs is the standard way Swiss robo-advisors work. The good news is that they only use index ETFs. Index ETFs are following an index instead of trying to pick stocks. This makes them cheap, and in practice they even beat active funds.

There is usually a tax-efficiency downside to using ETFs, but as we will see in the next chapter, Finpension Invest does not suffer from this downside.

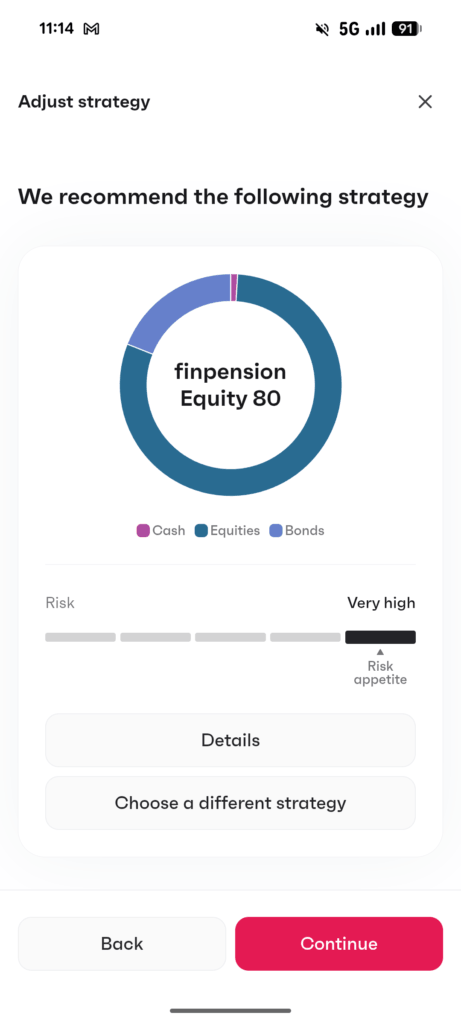

There are two main ways to set up your strategy:

- Auto-Select: Will prepare a portfolio for you.

- Self-Select: Will let you be more specific about your strategy.

In all cases, you can reach up to 99% invested (in stocks or bonds). You will need to keep 1% in cash. You can even keep 99% in a money market fund if you are really risk-averse.

The part not invested in cash, stocks or money-market will be invested in Swiss bonds. This makes sense because your bonds are here to reduce risks in your portfolio. So, you should not introduce currency risk there. And hedging would not solve it because you would pay the costs of hedging and pay higher income tax (because of higher yields in foreign bonds).

For auto-select, you can select between three focuses for stocks:

- Global: Fully diversified internationally.

- Switzerland: Invest globally but with a strong bias on Swiss stocks.

- Sustainable: Only invest in sustainable stocks (globally).

For Self-Select, you have a few more options:

- Global: Fully diversified internationally.

- Europe: Invest globally but with a strong bias on European stocks.

- Switzerland: Invest globally but with a strong bias on Swiss stocks.

- Broad Impact: Sustainable investing with a global impact.

- Climate Impact: Sustainable investing with a focus on climate.

- Social Impact: Sustainable investing with a social focus.

And finally, as is standard with Finpension, you can also do a custom portfolio with Finpension Invest. This means you can pick up the funds directly yourself, among more than 40 available funds. You are at full liberty to invest in your portfolio.

In your account, you can have up to 10 different portfolios. Each of these can have a different strategy.

Finally, you can also invest in private markets. Private markets are deals outside the public stock market. With Finpension Invest, you have access to two institutional funds for private markets investment. This is quite impressive because no other robo-advisor provides you with access to private markets.

It is important to note that private markets will only be offered to those with a very high-risk profile (based on your answers to the risk assessment). This limitation makes a lot of sense because private markets can be very volatile.

Moreover, you cannot mix private market funds with other funds in the same portfolio. You can have multiple private market funds (in different portfolios), but each of these portfolios must be invested fully in private markets. Since you can have 10 portfolios, this is not a big limitation.

Overall, the investing strategy of Finpension Invest is excellent. They have all the bases covered, and they even offer access to private markets, something no other simple robo-advisor offers at this point. This service can be an excellent tool for long-term investing.

Example portfolio

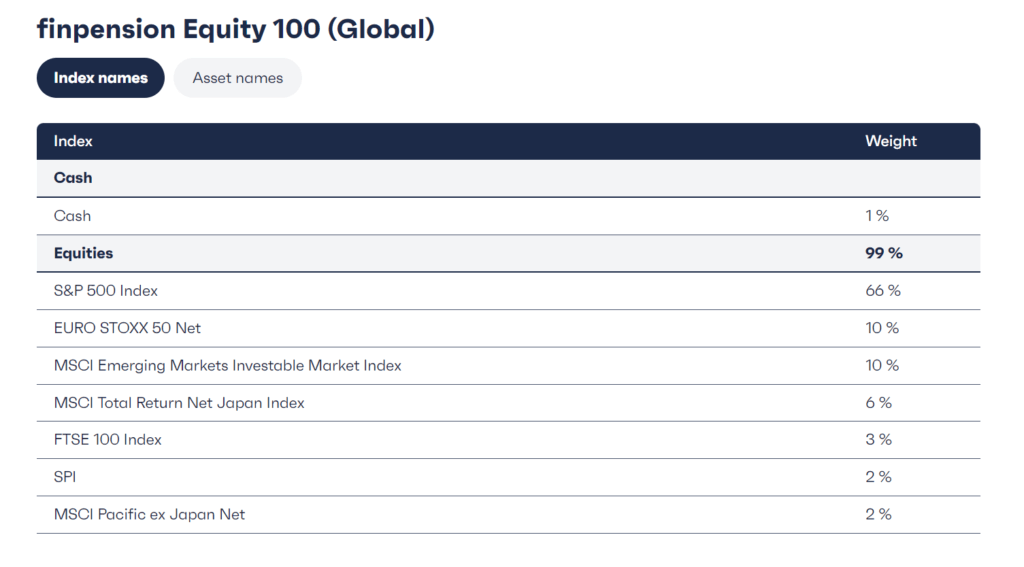

We can pick an example to look at the details of the strategies proposed by Finpension Invest. For me, the Finpension equity 80 (Global) strategy is a good example to look at.

This portfolio is very well diversified since it covers all markets. Each country and region are represented based on their market capitalization. For instance, Switzerland is about 2% of the entire world stock market, while the US is currently about 66%.

You may be surprised by the number of funds. In theory, it would be simpler to use a world fund and let the fund pick the countries and do the rebalancing. However, since Finpension Invest wants to be extra efficient with taxes, they have to pick at least one fund for the US to allow BlackRock to do the full withholding reporting for them.

So, while I would generally prefer not having tiny percentages in a portfolio, in this case it makes total sense and this is very well diversified and balanced.

Finpension Invest Fees

Typically, the best criterion to distinguish between two robo-advisors is the price. To maximize your returns, you want to minimize your fees. So, it is essential to analyze the fees of Finpension Invest in detail.

Finpension Invest has a 0.30% custody fee and a 0.09% wealth management fee. This gives us a total fee of 0.39%. These fees include VAT.

It is worth noting that on your yearly statement, you will see these two fees separated. The custody fee is something you can usually deduct custody fees from your taxes, in most cantons. So, it is nice that they provide these two numbers separated.

On top of the 0.39%, you will need to pay the TER of the funds. On average, this will range from 0.08% to 0.10%.

Finally, Swiss stamp duty is also due on the transactions (for ETFs only, not index funds) and is not included in the all-in fee. As wealth managers, Finpension is obligated to charge this.

Since they are using ETFs, there is no issuing or redemption commission when you buy or sell. The currency conversion fee is also included into the fees.

Overall, the fees of Finpension Invest are excellent. A total fee of about 0.49% is really among the best we can find in Switzerland.

US Withholding Tax

We said before that ETFs generally have a disadvantage in tax efficiency. This is because the US taxes dividends at source. With a US ETF, you can avoid this, but not with a European ETF and no Swiss robo-advisor offers US ETFs. With a European ETF, you would lose 15% of the dividends coming from US stocks.

It is easy to estimate that cost. US stocks are currently 66% of the world stock market and have an average yield of 1.50%. So, on average, losing these dividends is the same as adding an extra fee of 0.1485% (rounded to 0.15%).

Normally, this is not reclaimable. However, Finpension managed a very innovative technique. They have a deal with BlackRock (the fund provider of the ETF). BlackRock will give them all the necessary information for each of the dividend withholdings. Then, Finpension can tie this back to the shares held by the users. And from that, they can produce a statement that can be added to the tax declaration to reclaim this fee!

It is worth noting that Finpension is currently speaking to the different tax offices to validate this technique. But we already know that Lucerne accepted this claim. So there is a good chance that more cantons will follow.

The DA-1 deductions can only be claimed if you reach a minimum of 100 CHF. The total will include Finpension claims and possibly other deductions you are doing yourself.

This feature really shows that Finpension knows their stuff. This feature gives a tremendous advantage to Finpension Invest against other Swiss robo-advisors.

Opening a Finpension Invest account?

If you already have a Finpension account (for your 3a, for instance), you can directly create a Finpension Invest portfolio from it. Otherwise, you can start creating an account from scratch either from the website or from the app, it should be a fairly quick process.

As with any robo-advisor onboarding, you will need to answer the usual risk assessment questions. From there, they will define your risk capacity. And again from there, they will suggest portfolios, but you can override the choice.

If you open a Finpension 3a account, please use my code FEYKV5. This code will give you a fee credit of 25 CHF (if you deposit 1000 CHF in the first 12 months) and will help my blog as well.

Overall, it is fairly standard to open an account at Finpension Invest.

Finpension Invest joint account

As of July 2025, Finpension now supports joint accounts! This is great news because very few joint investment accounts exist in Switzerland. If one of the two persons dies, the other person can still access the account since it is in both of their names.

The two people must reside in Switzerland. Then, they both must create an account with Finpension. Then, one of them can convert a portfolio into a joint portfolio, and this portfolio will be owned by both individuals. This works with a joint bank account or two individual bank accounts (in which case, both accounts must be validated).

It is excellent to see this feature because this can be helpful to many married couples.

Deposits and withdrawals

We can also look at how to deposit and withdraw money to and from your account.

First, we should note you can start investing with as little as 1 CHF in your account. This is great because many robo-advisors have significantly higher limits.

To fund your account, you can do a simple bank transfer. However, you must declare your bank accounts in advance. This means you can only transfer money from an account you have declared, and this account must be in your name. You can register multiple accounts in the app.

You can currently only fund your account in CHF, like most robo-advisors.

Furthermore, you can also withdraw money directly from the interfaces. You can choose to which saved account you want to transfer money .

Overall, deposits, and withdrawals are really convenient at Finpension Invest. And we will see in the next section, you can make it even easier by automating it.

Extra features

On top of the basic investing features, there are also some very interesting extra features.

First, you can transfer money directly from one portfolio to another. This can be very practical. And this also allows you to transfer money from one portfolio to another service, like your 3a. I think they did an impressive job of integrating all their services together.

You can fully automate your investment thanks to the weekly reinvesting. With that, people can set up a standing order from their bank to their Finpension account, and everything will be invested at most a week later. It is akin to a savings plan.

And you can also do the contrary with a de-savings plan. This allows you to set a standing order to withdraw money automatically and regularly. For instance, you could say you want 1000 CHF per month, and Finpension Invest will automatically sell enough shares to reach that amount and send that to your bank account. Again, you can set up multiple of these plans for each of your portfolios.

Overall, it is excellent to see all these features already on the first version of Finpension Invest. From the start, they already have more features than most competitors.

Safety

Of course, we should not forget about the security of our money. You never want to send your money to a service that you cannot trust with this money.

Contrary to most robo-advisors, Finpension Invest has a securities firm license. It means they can hold securities directly themselves, without relying on a third-party custody bank. From a regulation perspective, everything is in order.

If Finpension were to go bankrupt, shares would be safe because Finpension has to segregate customer assets from their own. It would likely take a while because it would have to be transferred to a new custodian bank, but this should work well.

It is worth mentioning that Finpension has been profitable since 2019 (only a few years after creation). This is important for the long-term use of the service. Many robo-advisors in Switzerland are losing money.

I have not been aware of any technical security issue with Finpension.

The only small downside is that they are a new securities firm (since March 2024). However, Finpension itself has been managing money since 2016 and has well over 5 billion Swiss francs in assets under management. This gives them a lot of experience.

Overall, money at Finpension Invest should be as safe as with any other Swiss robo-advisor.

Alternatives

An excellent way to get an idea of how good a service is to compare it against other alternatives. There are many robo-advisors available in Switzerland. I have compared Finpension Invest against three services.

Finpension Invest vs True Wealth

TrueWealth is an excellent Swiss robo-advisor with very affordable prices, making it a great robo-advisor for serious investors.

Use code SWISS100 to receive up to 100 CHF in fee credits.

- Very customizable

True Wealth is a very affordable robo-advisor, the most mature available in Switzerland. They also have a great range of features and are serious.

The investing strategies of these two services are really similar. They both use ETFs and focus on cheap index ETFs. And you have a very high level of customization in both cases. A slight advantage of Finpension would be to offer access to private markets, but it depends on whether you want that or not.

You need 8000 CHF to start with True Wealth, while Finpension Invest lets you invest with as little as 1 CHF.

Looking at the fees, True Wealth has a total fee of about 0.63%, while Finpension Invest is at 0.49%. This is a significant difference. It is worth mentioning that True Wealth has degressive fees. So, if you have a massive portfolio, True Wealth could become cheaper.

But once we factor in the 0.15% tax advantage of Finpension Invest, it will always be cheaper than True Wealth. It is worth mentioning that True Wealth also has a feature to reclaim the US dividends. However, this will depend on which custody bank you use. If you use BLKB, you will not get any tax advantage. You will get it only with Saxo because they will then be able to use US ETFs. But this is very poorly documented by True Wealth.

Overall, both have more or less the same feature set, but Finpension Invest is significantly cheaper and has a lower minimum.

Finpension Invest vs Findependent

Findependent is a very affordable Robo-advisor with a focus on sustainable investments. Invest your money easily! Get 20CHF in your account with code PoorSwiss.

- Excellent fees

Findependent is a more recent robo-advisor with low prices and a nice range of features.

Both robo-advisors use ETFs. Findependent only lets you invest 98% in stocks, slightly below 99% of Finpension Invest. Furthermore, by default, Findependent will only use ESG ETFs. You can create a custom portfolio to go around this. So, overall, Finpension is more flexible in the choices, especially with the addition of private markets.

You need 500 CHF to start with Findependent while Finpension Invest will let you start with 1 CHF.

From a fee perspective, both are quite well priced. Findependent charges a 0.40% fee, while Finpension Invest is at 0.39%. But the currency exchange fees of Findependent are much higher (0.50% against 0.002%) and stock exchange fees are not included in Findependent. And when we factor in the extra tax efficiency of Finpension Invest, it will be cheaper than Findependent. However, it is worth mentioning that Findependent has a staggered fee (all the way to 0.29% at one million of assets).

Overall, Finpension Invest has some significant advantages over Findependent. It is cheaper, more flexible and has a lower minimum.

Finpension Invest vs Selma

Selma is another robo-advisor that has a stronger target on beginners. They aim to make investing simple, without the bells and whistles.

Selma only gives you the choice between sustainable and standard investment. Apart from this, you will have no choice on the portfolio. The portfolio will be chosen based on your answers to the questions from the risk assessment. This makes it easier for beginners, but almost much less flexible than Finpension Invest.

As for fees, Selma has a base fee of 0.68% plus about 0.22% for the ETFs, for a total fee of a 0.90%. When we compare this against the 0.49% total fee for Finpension Invest, this is a very significant difference. And if we take the extra 0.15% in tax efficiency, this gets even more significant.

It is worth mentioning that Selma’s fee can be reduced if you have a large portfolio. The minimum fee is 0.42% with 500,000 CHF, much closer to Finpension Invest.

For any medium-to-advanced investors, Finpension Invest is a significantly better option than to its flexibility and fees. Using Selma would mean paying a significant premium that should be well thought of.

Finpension Invest vs VIAC Invest

In December 2024, VIAC followed Finpension with their robo-advisor service, VIAC Invest. Since these services are quite similar, we should compare them in more detail.

One difference in how things are being done is that VIAC created its own funds and invests customer assets in them. Finpension on the other hand, uses other funds directly. In practice, this makes little difference for users, unless they want to customize. In this case, Finpension has a major customization advantage since you can choose all funds directly.

The base fees of both services are the same at 0.49%. However, VIAC Invest does not have any stamp duty included. But VIAC Invest has some small to medium redemption and subscription fees, while Finpension does not.

The main difference is how US dividends are handled. In some cantons, you can get all the withholding back with Finpension Invest (0% withholding). In other cantons, you get the usual 15% withholding. Unfortunately, VIAC invest uses Swiss funds for US stocks, resulting in 30% withholding. This makes a major difference in favor of Finpension Invest.

For me, this tax-efficiency advantage is enough to make Finpension Invest a better option.

If you would like to learn more, you can read my detailed comparison of Finpension Invest vs VIAC Invest.

Finpension Invest FAQ

How many portfolios can you have with Finpension Invest?

You can have up to 10 portfolios, each with a different strategy.

What is the minimum you can invest with Finpension Invest?

You can start investing with as little as 1 CHF.

Who can invest with Finpension Invest?

All Swiss residents that are at least 18 years old (and are not US citizens).

Who is Finpension Invest good for?

Finpension Invest is great if you want to invest in the stock market (or private markets) and want to minimize their fees.

Who is Finpension Invest not good for?

Finpension Invest is not great if you are a total beginner in invest or if you are expert enough that you can invest by yourself.

Finpension Invest Summary

Wealth management for all? Read our review of Finpension Invest. We analyze the fees and strategies of this private investment solution.

Product Brand: Finpension

5

Finpension Invest Pros

Let's summarize the main advantages of Finpension Invest:

- Outstanding fees.

- Excellent tax-efficiency.

- Can invest up to 99% in stocks.

- Can invest with as little as 1 CHF.

- Great investing strategy.

- Excellent integration with other Finpension services.

- Web and mobile applications.

- Advanced customization.

- Access to private markets.

- Very transparent.

Finpension Invest Cons

Let's summarize the main disadvantages of Finpension Invest:

- Entirely new solution.

- Stamp Duty is not included in the management fees.

- Maybe not suited to total beginners.

Conclusion

An excellent and innovative Robo-advisor by Finpension.

- Most tax-efficient Robo-advisor

- Access to private markets

Finpension did it again! Their new service, Finpension Invest, is again an excellent service. They offer a very nice set of features, excellent portfolios, and top-of-the-line fees.

This service offers very innovative features, such as the wonderful tax withholding support for US dividends. Now that I see this, I wonder why no other service went through this before. This really shows that Finpension is willing to go one step further to provide exceptional service.

Seeing all these features and fees together, I now believe that Finpension Invest is the new best robo-advisor available.

For transparency, I must mention that I am not using a robo-advisor myself. I am investing directly through a broker account. If you have the knowledge and the willingness to do so, investing by yourself with a great broker will be cheaper than investing through a robo-advisor.

What about you? What do you think about Finpension Invest?

More reading

Interview of Felix Niederer, CEO of True Wealth Robo-Advisor

Robo-Advisor insights. Read our interview with Felix Niederer, CEO of True Wealth, and learn about their mission to lower investing fees.

VIAC Invest Review 2026 – Pros & Cons

Invest without limits. Read our review of VIAC Invest. We test their private investment solution to see if it's as good as their famous 3a pillar.

Inyova Review 2026 – Pros and Cons

Invest with impact. Read our 2026 review of Inyova. We analyze their impact investing strategy and fees to see if it's right for you.

Learn easy ways to optimize your finances and save thousands in Switzerland with our exclusive e-book. Learn about the most cost-effective financial services tailored for savvy residents and expats!

Get Your FREE Swiss Money-Saving Guide

Hi Baptiste,

thank for the nice review.

The 0.30% + 0.9% fees p.a. is not bad if compared to others robo-advisors, but will impact your return over the long term.

What is not clear to me is the 0.3% deduction from taxes. Let’s say I have invested 100.000 CHF, can I recover the 300 chf from taxes? So why consider it a fee?

I asked them some details about rhe finpension plan 100 because the website shows one chart from 2014 and the factsheed from.2019… they answer me “difficult to provide you with an average growth as it fluctuates according to the markets”, that doesn’t look to professional to me”

Hi Nicola

You cannot deduct it from your taxes, but you can deduct it from your taxable income. It means you can effectively get back your marginal tax rate % of the fee.

Actually, their answer makes, they do not want to provide possible outcomes since these depend on the market and are unpredictable. This is the basis of index investing.

Hi Baptiste, thank you for your answer.

It’s good they don’t provide possibile outcomes because everything in unpredictable, but I guess that when one’s choose any investment (etfs, stocks, funds ans so on) one’s really need to know the average growth since inception, it’s also useful to compare the investment strategy to others.

In your article I read that you consider finpension global 100 a really good fund, do you think there is a way to optimize it or do you think among their equities there is one which is particularly good?

Yes, you should compare the investment strategy, but if you are doing passive investing, I am not sure it makes much sense to compare prior returns. But that’s of course debatable.

I think there is a way to optimize by removing currency hedging if you do not want it.

Hi Baptiste,

I am wondering about the Money Market fund that Finpension offer.

What is a Money Market Fund and what are the advantages and disadvantages (I could not find an article about them on this website)? It has a much better interest rate (1% vs 0.5% in Neon and 0.6% in UBS) for keeping emergency fund cash, but what is the catch? Takes a few days to take money out? Thanks!

Hi Tim

A money market fund is a fund with very safe investments only. Such funds invest in cash and short-term bonds (like treasury bonds).

The current yield of the fund (Pictet) is 0.82% after fees and once you factor the fees of Finpension invest, you end up at about the same level as Neon and UBS. It’s mostly a way to make the portfolio safer by adding in some “cash”.

Hi Baptiste,

Thanks a lot. OK, does not make that much sense.

Is it possible to build a “safe portfolio” for some (perhaps one half or two thirds) of one’s emergency fund that can earn 2-3% instead of only getting around 0.5% in a bank? I guess the whole definition of an emergency fund is that it is not invested, however there seems like some optimisation potential for emergency funds.

I don’t think emergency fund should be invested. If you feel like it should be invested, it is likely your emergency is too large. The whole point is to have it available in case of emergency. For me, the best we can achieve with an emergency is to have it in an interest-bearing savings account (with no wihtdrawal restrictions).

If you really want to be aggressive, you can reduce your emergency fund to zero and rely on margin loan for emergencies. But that’s not for everybody.

Hi Baptiste

Considering the Credit-Suisse crash just two years ago, what are the risks of using finpension, in your opinion, considering that they still work with Credit-Suisse?

Thank you

Florin

Hi Florin

I think there are zero risks considering. They were using Credit Suisse while it “failed” and nothing happened. Now they are using a subsidiary of UBS. And if UBS fails, they will be bailed out. So I think there is no risk in using UBS or CS.

All of these robo advisors have a questionnaire for assessing your risk level. Finpension does not give you access to higher risk portfolios if your assessment shows you have a low risk. What happens if you cheat the questionnaire to get access to all risk levels? The purpose of this would be to experiment with a relatively small amount of money in a maximum risk portfolio and have a larger amount invested in a second portfolio at the recommended risk level (deduced by completing the questionnaire honestly). Are there any hidden problems with this or is it fine if you are confident in your ability to assess the risk yourself?

Hi Tom,

These questions are mostly for protecting themselves rather than for protecting you. They want to avoid investing aggressively for people that are not ready so that these people cannot then complain they did not know what you are doing. If you are “cheating” the questionnaire, you are basically waiving your right to say that this portfolio was not adapted to you.

I do not think this is a big deal, but it may also mean you are investing beyond your risk capacity. You have to make sure you can weather the risk if you are doing that.

What would be the advantage to using finpension invest compared to say Neon invest? With Neon, you don’t pay a custody fee, paying 0.39% on my entire portfolio seems high.

Hi,

The advantage of a Robo-advisor is to make investing easier, at the cost of higher fees. The 4 Investing Levels: Control vs Fees

Interestingly, sometimes Robo-advisors can be cheaper: Can Robo-advisors be cheaper than brokers?

Hi Baptiste,

First of all let me congratulate you for your blog, I never miss an episode, fascinating work you are doing, many thanks!

Reading your review of Selma a few years ago I opened an account with them (and with IBKR too!) but I’m considering migrating the funds to Finpension as the fees are higher on Selma for a comparable service. Do you see anything speaking against moving the funds?

Thanks, Dom!

I don’t see anything against moving the funds. This will indeed save you some fees. Just be careful about not moving too often. Moving funds should be for the long term. When you are moving funds, you are staying out of the market for a little while, potentially losing out.

True Wealth has now witdrawn the management fees for the 3a pillar. Wonder if you could please provide us with an updated comparison vs FP and Viac. Thanks!

I don’t understand your comment. This article is about Finpension Invest, nothing like 3a.

Do you believe that finpension could be a good place to open investment for a child ? Or Ibkr is better ? Thank you

I would say it mostly depends on your investing.

If you are already using Finpension, creating a second portfolio for your child makes total sense. If you are already using IB, a second account makes sense.

Were using both (finpension for 3a). Wondering what will be better and easier, ae have 2 children and thought to add 1 child to each parent account. Currently investing in the bank and the costs are too high. Thank you again I really use your blog a lot !

Hi Adi

If you already have a Finpension account, I think that starting with it is a good option. The fees are very low and until you reach a high amount (20k+), it can be on the same level of fees as IB. It is probably the only option apart from IB that I would recommend.

Many many thanks, have a great weekend.

Adi

Hi Baptiste,

Nice work as usual :)

I am currently investing with IBKR for a long term strategy (around 30 years period), with a portfolio based on a high percentage of ETF’s with a rebalancing every year. Considering the fees and the tax declaration in Switzerland, do you think the Finpension Invest can be a better solution?

Thank you !

Gio

Hi Gio,

No, Finpension Invest cannot compete with IBKR. Finpension Invest can compete well with Swiss brokers up to a certain portfolio size, but not with IBRK.

Hi Baptiste,

Thanks a lot for all your research and advice. I recently used your code for the third pillar and I am very happy with Finpension so far.

For investing in ETFs, I was also considering IBKR vs this robo-advisor and, please, could you elaborate a little bit on the “cannot compete”? Is it because of the fees only? In terms of tax declaration I think the robo makes your life much easier.

Thank you!

Hi Ivan

Thanks for using my code and I am glad you enjoy FP.

In terms of fees, a robo-advisor cannot compare with IB indeed. If you invest only once a month, the difference in tax declaration is really small. It’s mostly a matter of not having to choose ETFs by yourself and relying on a good Robo-advisor for doing that.

As always, awesome work, Baptiste!

Ive read the finpension invest review on http://www.schwiizerfranke.com before and it was really deep already. But with yours I feel, that Ive got all the informations now!

Thanks!

Thanks, Sabine!